Apple investigating outages affecting Apple TV+, Apple Music services

Introduction & Market Context

Atea ASA (OB:ATEA), the Nordic region’s leading IT infrastructure provider, presented its Q2 2025 financial results on July 16, 2025, showcasing strong performance across all key metrics. The company reported double-digit growth in gross sales, revenue, and profitability, driven primarily by robust software sales and strong performance in Denmark and the Baltics.

The results come amid increasing demand for IT infrastructure solutions across the Nordic and Baltic regions, particularly in defense, cybersecurity, and AI-related technologies. Atea’s strategic positioning in these growth areas has enabled it to capitalize on market opportunities and strengthen its competitive advantage.

Quarterly Performance Highlights

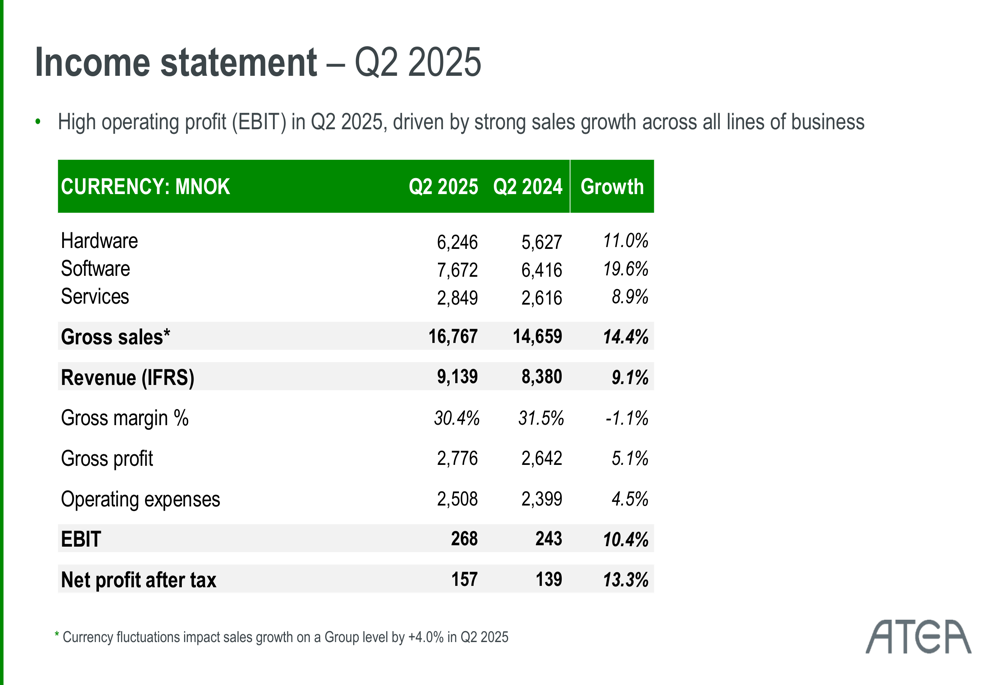

Atea reported impressive financial results for Q2 2025, with gross sales reaching NOK 16.8 billion, representing a 14.4% increase compared to the same period last year. Revenue (IFRS) grew by 9.1% to NOK 9.1 billion, while EBIT increased by 10.4% to NOK 268 million. Net profit saw the highest growth rate at 13.3%, reaching NOK 157 million for the quarter.

As shown in the following quarterly highlights slide, all key performance indicators demonstrated solid growth:

The company’s income statement reveals that software sales were the primary growth driver, increasing by 19.6% to NOK 7.7 billion compared to Q2 2024. Hardware sales also performed well, growing by 11.0% to NOK 6.2 billion, while services sales increased by 8.9% to NOK 2.8 billion. However, gross margin decreased slightly to 30.4% from 31.5% in the same period last year.

The detailed income statement provides a comprehensive view of Atea’s financial performance:

Segment Performance Analysis

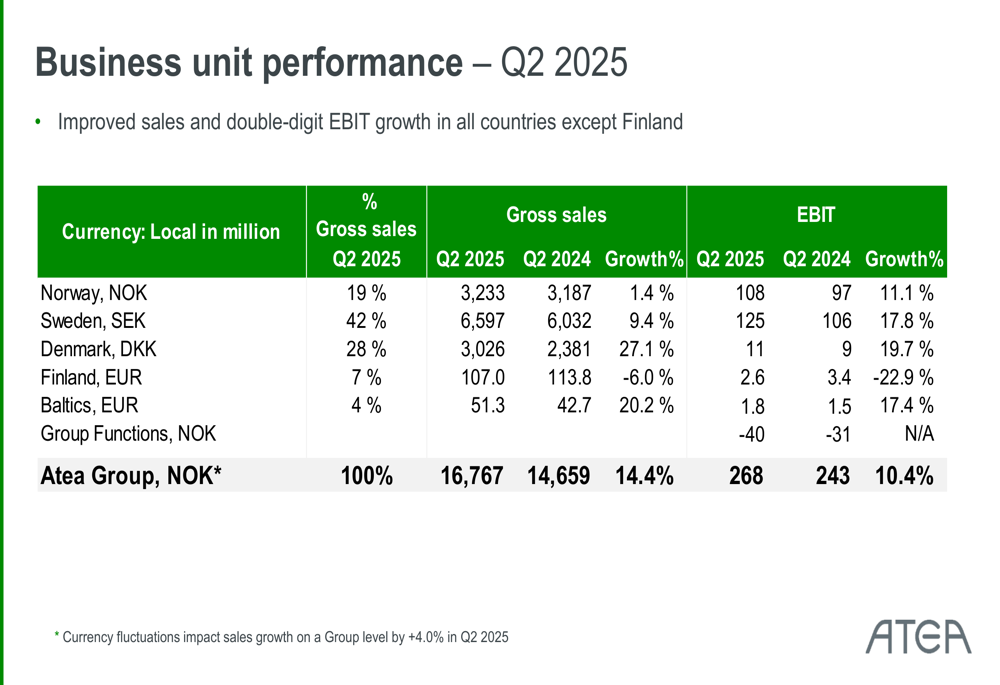

Atea’s performance varied across its geographic segments, with Denmark and the Baltics showing the strongest growth in local currency terms. Denmark’s gross sales increased by 27.1% year-over-year, while the Baltics grew by 20.2%. Sweden, which accounts for 42% of total gross sales, delivered solid growth of 9.4%. Norway showed modest growth of 1.4%, while Finland was the only region to experience a decline, with gross sales decreasing by 6.0%.

The following slide illustrates the business unit performance across different regions:

In terms of profitability, all regions except Finland showed EBIT growth. Sweden, which contributed the largest share to group EBIT, saw its operating profit increase by 17.8%. Denmark’s EBIT grew by 19.7%, while Norway and the Baltics recorded EBIT growth of 11.1% and 17.4%, respectively. Finland’s EBIT declined by 22.9%, reflecting challenges in that market.

Financial Position and Cash Flow

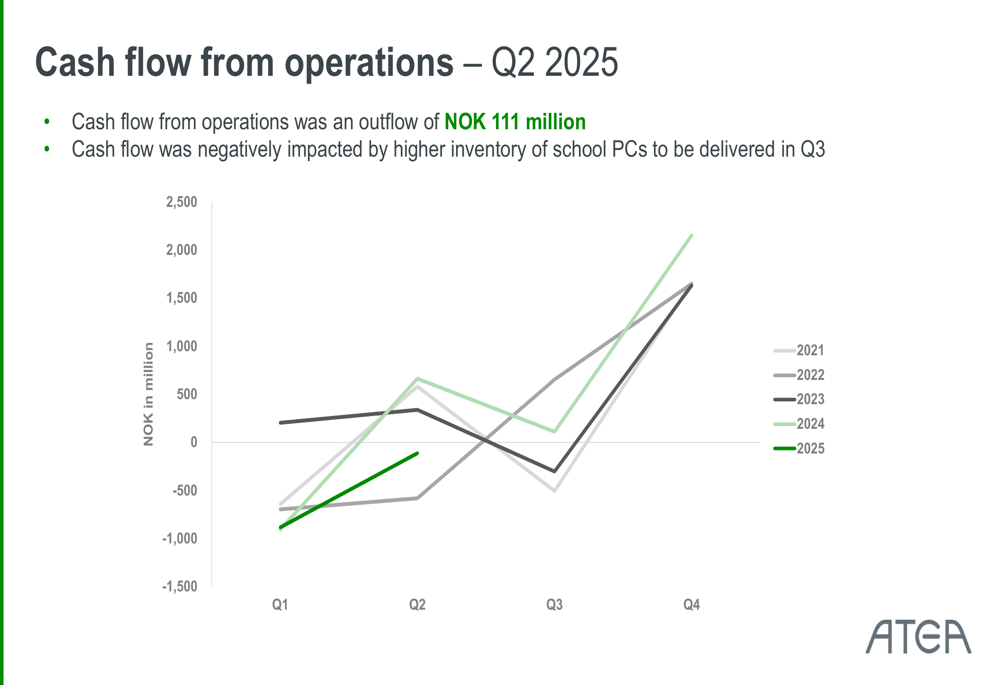

Atea’s cash flow from operations was negative in Q2 2025, with an outflow of NOK 111 million. According to the company, this was primarily due to higher inventory of school PCs that will be delivered in Q3 2025. The following chart shows the quarterly trend in cash flow from operations:

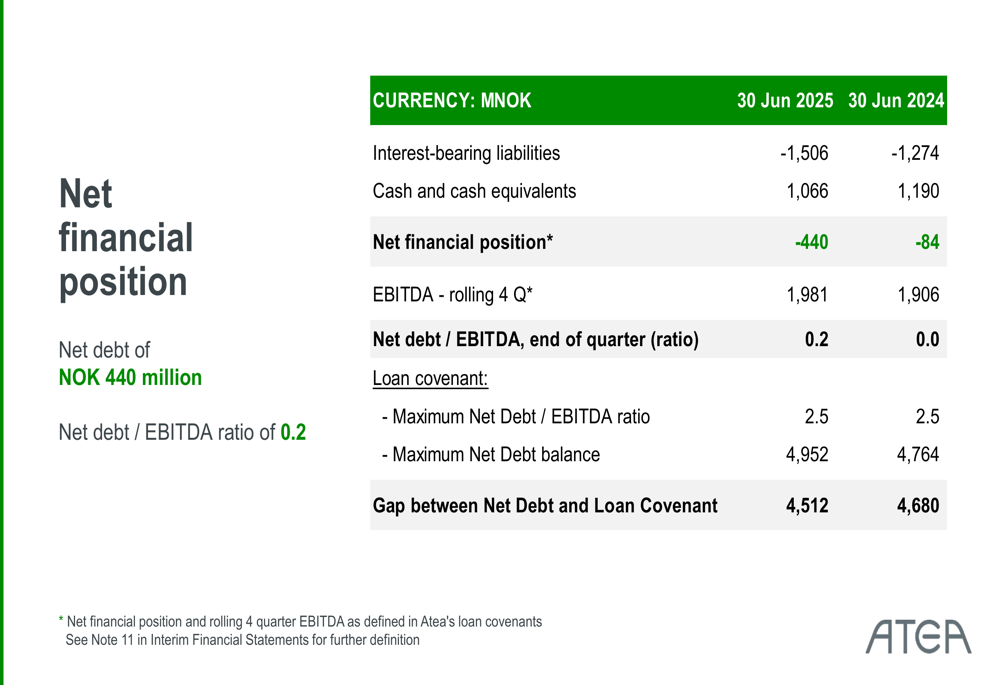

Despite the negative cash flow in Q2, Atea maintains a strong financial position with a net debt of NOK 440 million as of June 30, 2025, resulting in a net debt to EBITDA ratio of just 0.2. This is well below the company’s loan covenant maximum of 2.5, indicating significant financial flexibility for future investments or acquisitions.

The company’s net financial position is detailed in the following slide:

Business Outlook and Growth Drivers

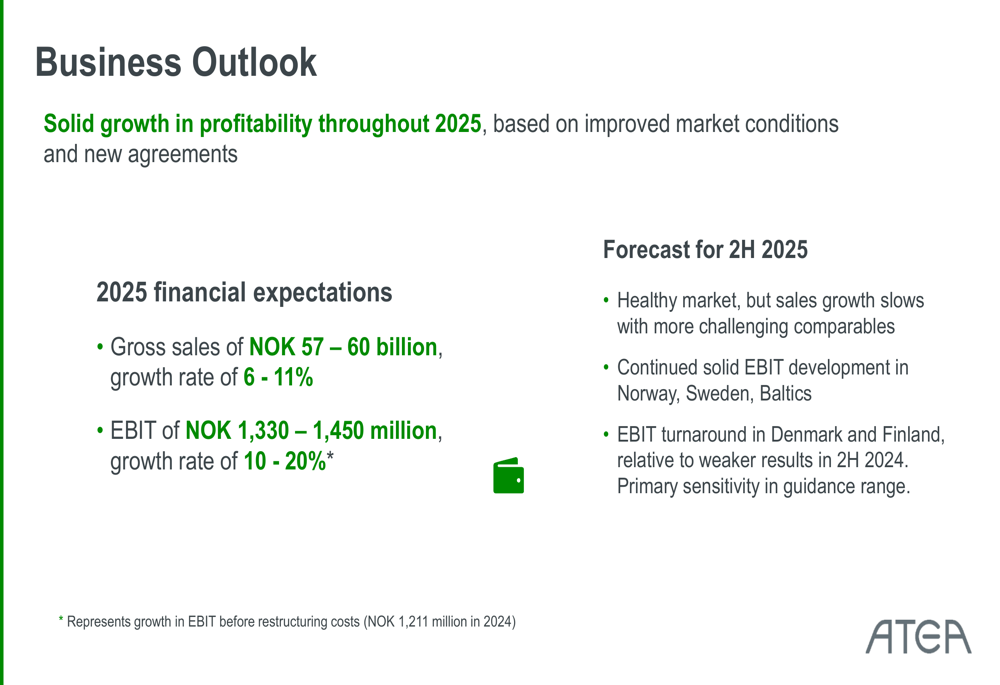

Looking ahead, Atea provided a positive outlook for the remainder of 2025, expecting gross sales of NOK 57-60 billion (representing 6-11% growth) and EBIT of NOK 1,330-1,450 million (representing 10-20% growth). The company anticipates continued solid EBIT development in Norway, Sweden, and the Baltics, with a turnaround expected in Denmark and Finland in the second half of 2025.

The business outlook slide highlights these financial expectations:

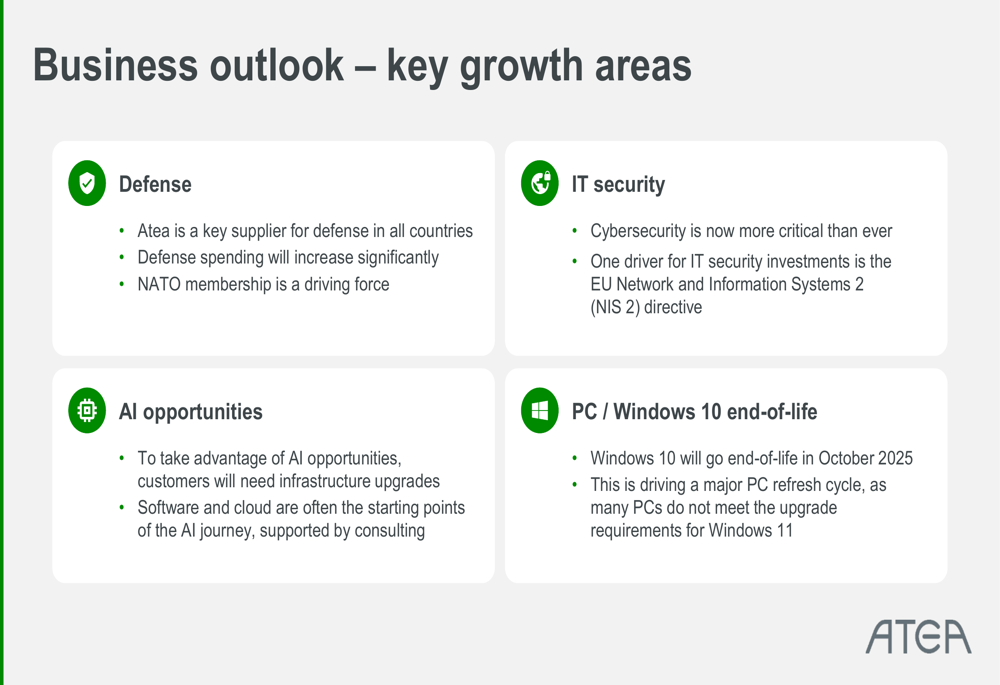

Atea identified several key growth areas that will drive its performance in the coming years. These include defense spending (boosted by NATO membership), IT security investments (driven by the EU’s NIS 2 directive), AI opportunities (requiring infrastructure upgrades), and the Windows 10 end-of-life in October 2025 (driving a major PC refresh cycle).

The following slide outlines these growth drivers in detail:

Forward-Looking Statements

For the first half of 2025, Atea reported gross sales of NOK 30.0 billion, up 15.3% from the same period last year. Revenue (IFRS) increased by 10.7% to NOK 17.7 billion, while EBIT grew by 10.1% to NOK 549 million. These results provide a solid foundation for achieving the company’s full-year targets.

The H1 2025 summary slide shows the strong performance across all key metrics:

While the company expects healthy market conditions to continue, it anticipates that sales growth will slow in the second half of 2025 due to more challenging comparables. However, Atea remains confident in its ability to deliver solid EBIT development, particularly in Norway, Sweden, and the Baltics, with improvements expected in Denmark and Finland.

The company’s strong market position, combined with its strategic focus on high-growth areas such as defense, cybersecurity, AI, and the upcoming Windows refresh cycle, positions it well for continued success in the Nordic and Baltic IT infrastructure market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.