Street Calls of the Week

Atlantic Sapphire (OB:ASA) presented its H1 2025 results on September 1, highlighting a significant operational turnaround with doubled revenue and improved biological performance as the company positions itself as the leading land-based salmon producer in the United States.

Introduction & Market Context

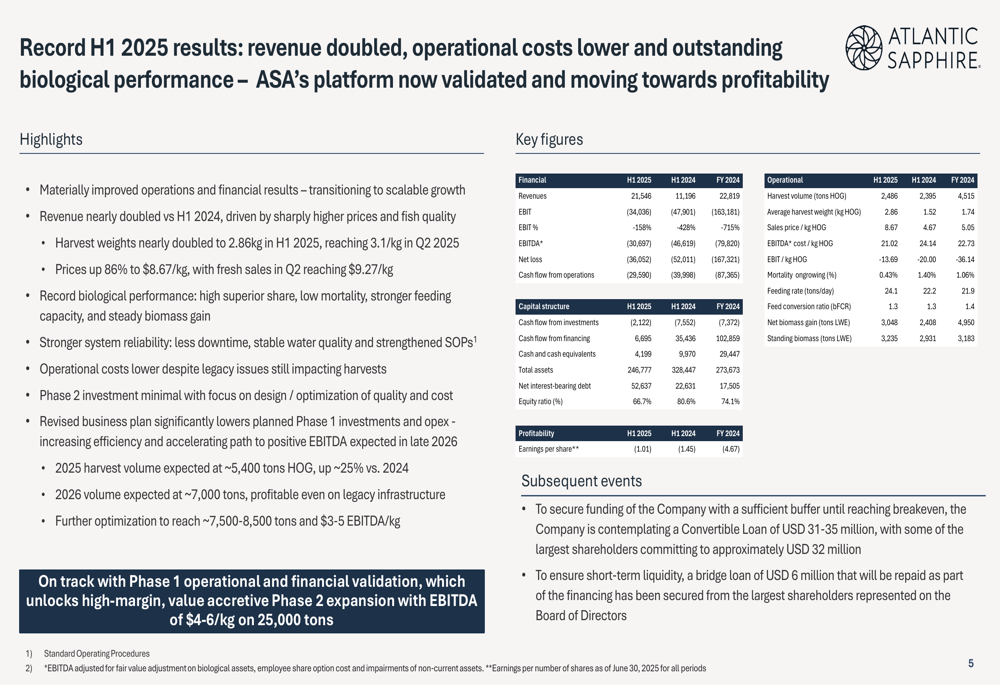

Atlantic Sapphire reported record H1 2025 results, with revenue nearly doubling year-over-year to USD 21.5 million, up from USD 11.2 million in H1 2024. The company is capitalizing on its first-mover advantage in the massive U.S. salmon market, estimated to reach $7-8 billion by 2030, where currently only about 2% of consumption comes from domestic production.

The company’s stock closed at 9.67 on August 29, 2025, representing a significant recovery from its 52-week low of 4.12, though still well below its 52-week high of 94.92.

As shown in the following chart of the company’s financial performance:

Quarterly Performance Highlights

Atlantic Sapphire’s H1 2025 results showed substantial improvement across key metrics compared to the same period last year:

- Net loss reduced to USD 36.1 million from USD 52.0 million in H1 2024

- EBITDA improved to USD -30.7 million from USD -46.6 million

- Harvest volume increased slightly to 2,486 tons HOG from 2,395 tons

- Average harvest weight jumped to 2.86 kg HOG from 1.52 kg

- Sales price per kg nearly doubled to USD 8.67 from USD 4.67

- EBITDA cost per kg improved to USD 21.02 from USD 24.14

- Mortality rates in ongrowing dropped to 0.43% from 1.40%

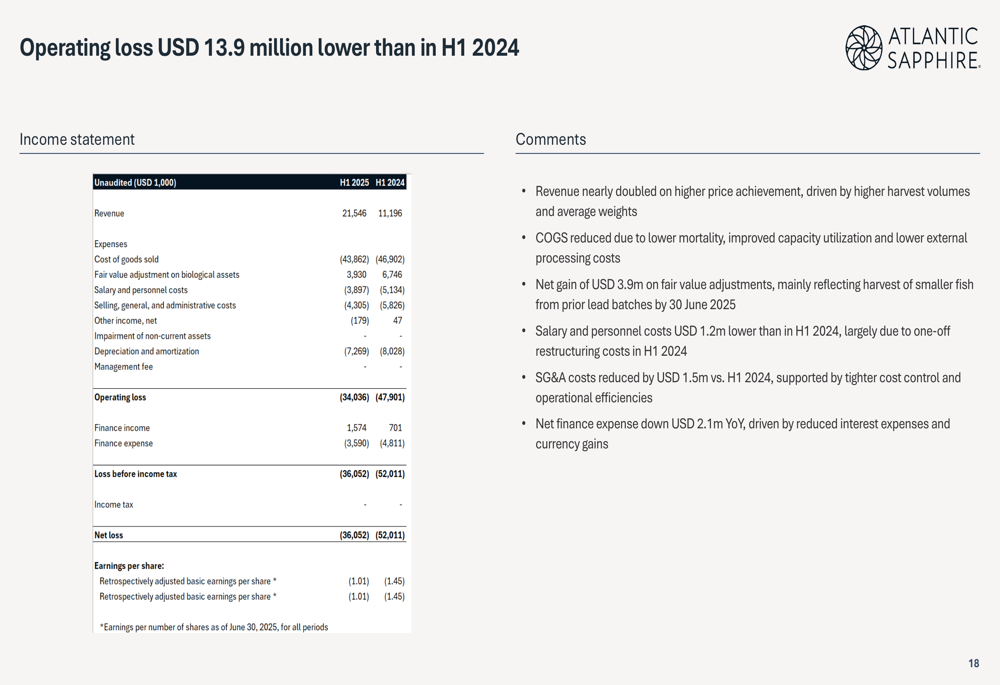

The company’s operating loss improved to USD 34.0 million in H1 2025 from USD 47.9 million in H1 2024, while operating cash flow improved to USD -29.6 million from USD -40.0 million.

The following slide illustrates the company’s operating loss improvement:

Operational Improvements

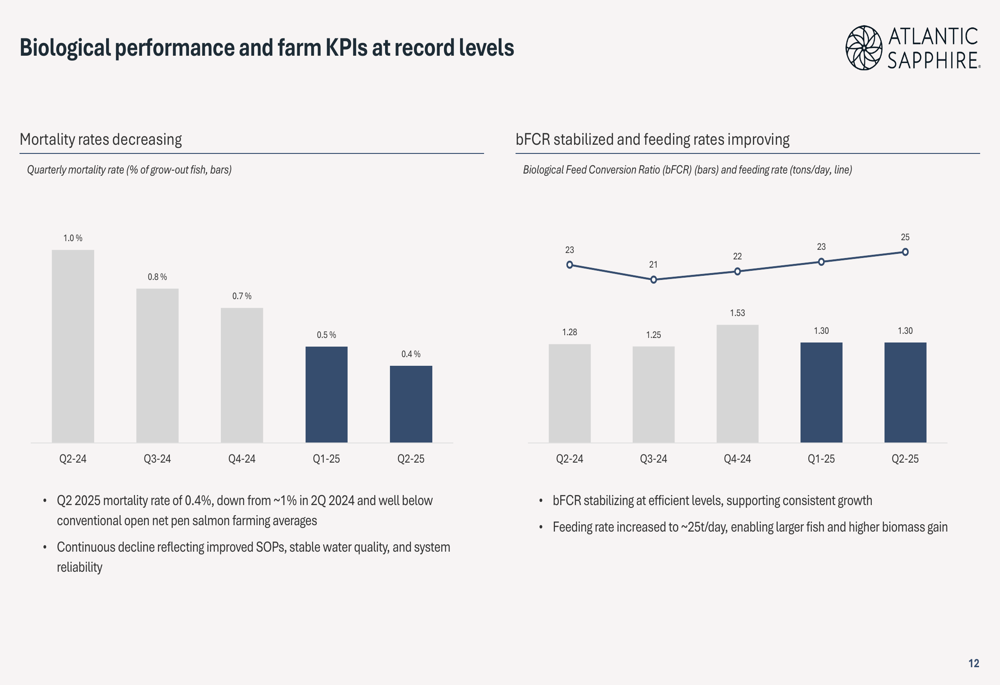

Atlantic Sapphire has made significant strides in biological performance, a critical factor for the land-based salmon farming model. Mortality rates have steadily decreased, reaching 0.4% in Q2 2025 compared to 1.0% in Q2 2024, while feeding rates have improved.

The company’s biological improvements are clearly demonstrated in the following chart:

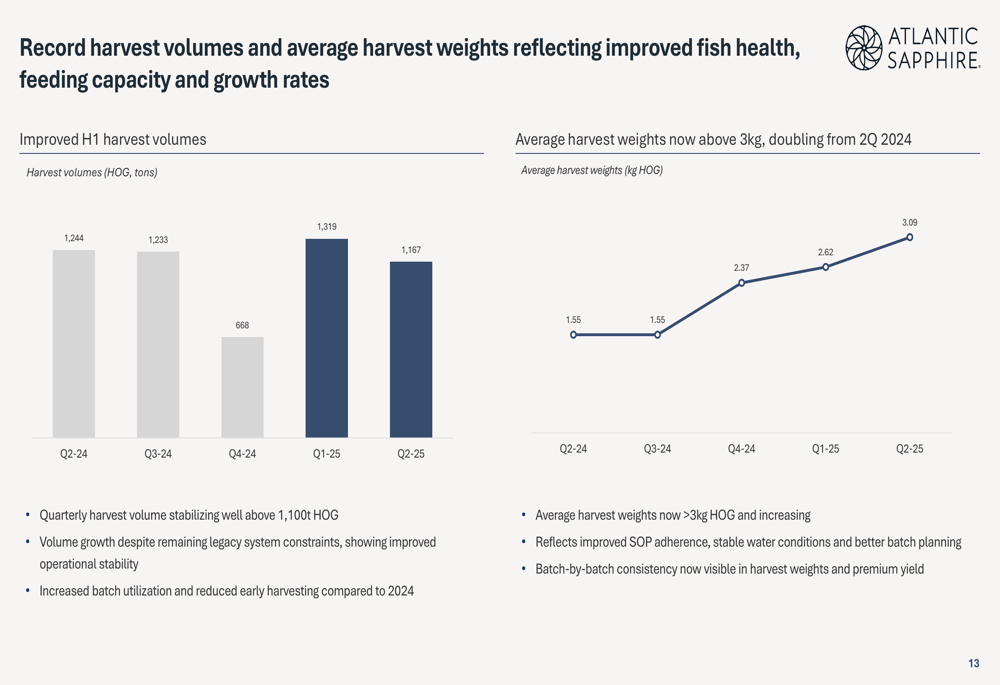

Perhaps most importantly, average harvest weights have increased substantially, reaching 3.09kg in Q2 2025 compared to just 1.55kg in Q2 2024. This improvement directly impacts profitability as larger fish typically command better prices and improve overall economics.

The harvest weight improvements are illustrated in this chart:

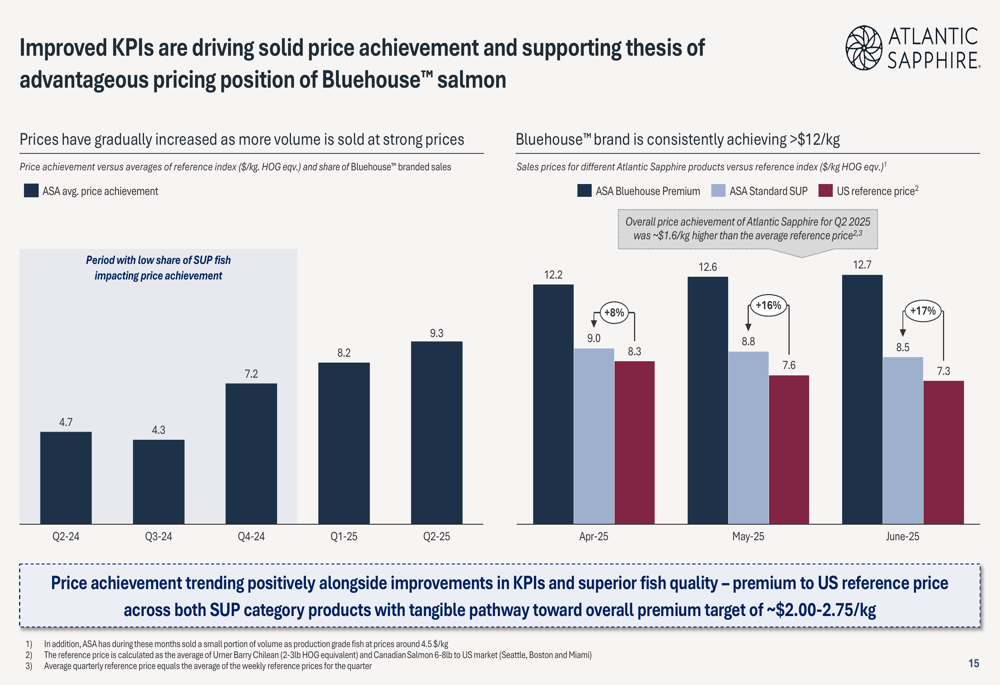

These operational improvements have enabled Atlantic Sapphire to achieve premium pricing for its products. The company has established two main sales channels: Bluehouse Premium (targeted at 60-70% of sales volume) with expected sale prices of ~$12/kg, and Fresh SUP fillets (30-40% of sales) at prevailing market prices +/- ~20%.

The company’s price achievement versus U.S. reference prices is shown in the following slide:

Strategic Initiatives

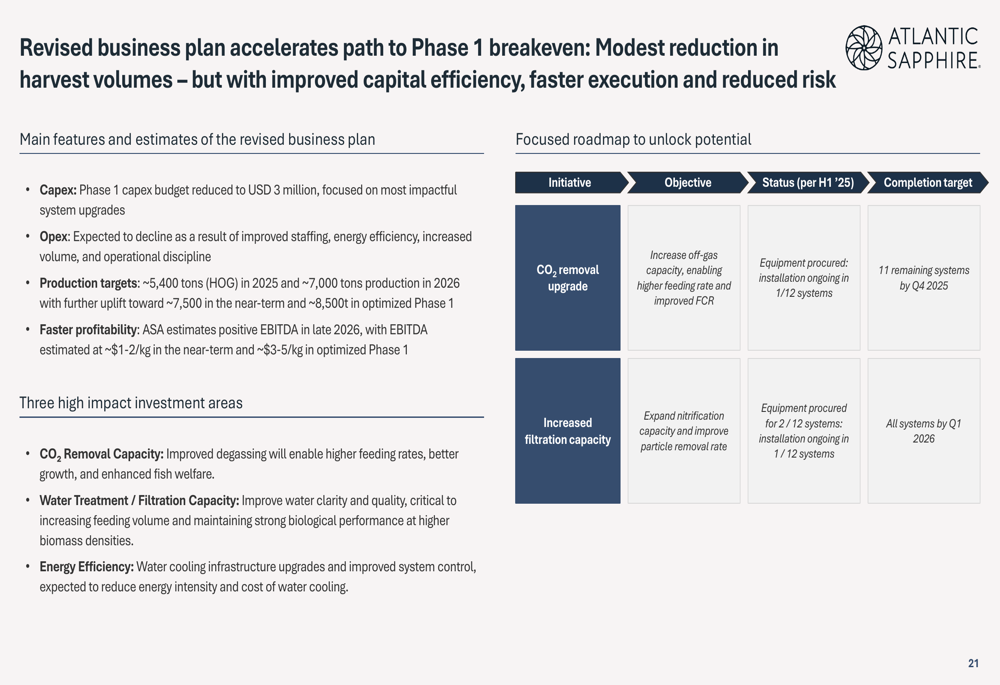

Atlantic Sapphire has revised its business plan to accelerate the path to breakeven, focusing on modest harvest volumes with improved capital efficiency and reduced risk. The company has reduced its capex plan to USD 3 million, concentrating on the most impactful system upgrades.

The roadmap for these improvements is outlined here:

The company is targeting production of ~5,400 tons (HOG) in 2025 and ~7,000 tons in 2026, with a goal of achieving positive EBITDA by late 2026. This represents a significant inflection point for Atlantic Sapphire as it transitions toward a self-funding business model.

To fund these initiatives, the company is contemplating raising USD 31-35 million in new financing through a convertible loan, which it estimates will fully fund the revised business plan. Atlantic Sapphire maintains a relatively strong balance sheet with an equity ratio of 66.7% and total assets of USD 246.8 million as of June 30, 2025.

Forward-Looking Statements

Atlantic Sapphire’s long-term strategy remains focused on its Phase 2 expansion, which the company describes as "shovel ready" with approximately USD 110 million already invested. The company has secured all major permits and completed freshwater systems with capacity for both Phases 1 and 2.

The potential scale of this expansion is illustrated in the following image:

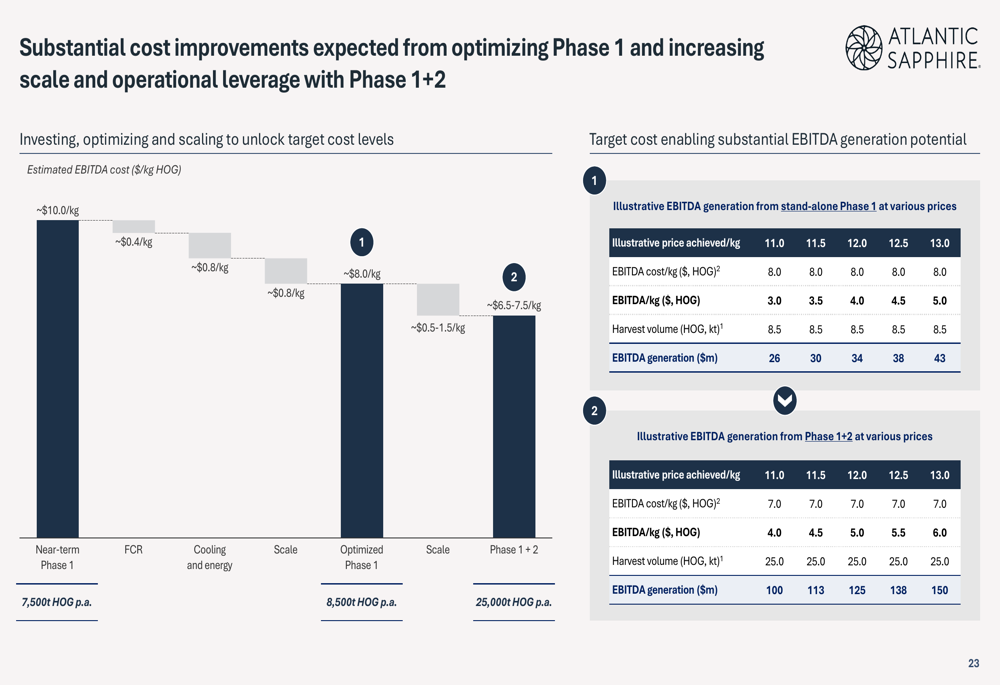

The company projects substantial cost improvements as it scales operations, with EBITDA costs expected to decrease with increased production volume. For the optimized Phase 1, Atlantic Sapphire targets EBITDA of USD 3.0-5.0 per kg at an annual harvest volume of 8,500 tons, potentially generating USD 26-43 million in EBITDA. With Phase 2 completion (25,000 tons capacity), the company projects EBITDA of USD 100-150 million.

These projections are detailed in the following slide:

Looking further ahead, Atlantic Sapphire maintains its long-term vision of creating a 100,000+ ton production platform in the U.S., which it estimates could generate over USD 500 million in annual EBITDA.

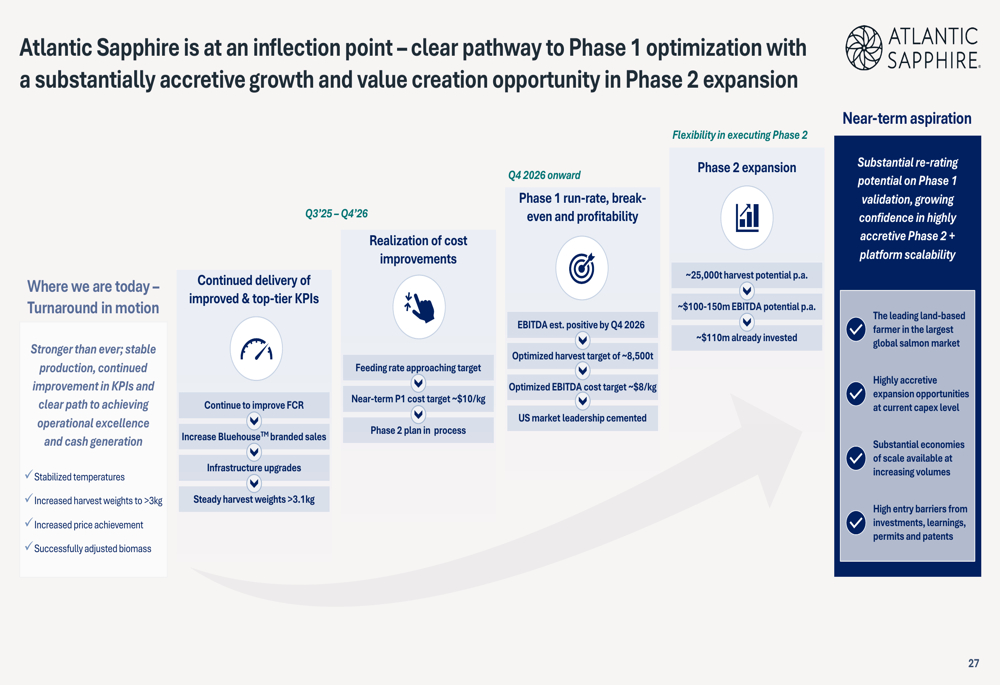

The company’s management believes Atlantic Sapphire is at an inflection point, with stabilized operations, increasing harvest weights, and a clear path to cost improvements and profitability, as summarized in this final slide:

While the presentation paints an optimistic picture of Atlantic Sapphire’s turnaround and future prospects, investors should note that the company has faced significant challenges in the past, including a USD 73 million impairment write-down of fixed assets reported in its 2024 results. The company’s ability to execute on its revised business plan and achieve its targeted profitability timeline will be crucial for long-term success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.