Nvidia AI chips targeted in China customs crackdown- FT

Introduction & Market Context

Atlas Energy Solutions Inc. (NYSE:AESI) released its Q1 2025 investor presentation on May 6, highlighting $298 million in quarterly revenue while emphasizing its strategic initiatives in autonomous logistics and power generation. The company, which positions itself as the largest Permian Basin frac sand provider, is trading at $14.07, significantly below its 52-week high of $26.86, reflecting ongoing market concerns following its Q4 2024 earnings miss.

The presentation comes as Atlas continues to navigate a competitive Permian Basin environment while expanding its service offerings beyond traditional proppant supply. With an enterprise value of $2.2 billion and market capitalization of $1.8 billion, the company is emphasizing its integrated approach to energy services.

Q1 2025 Financial Performance

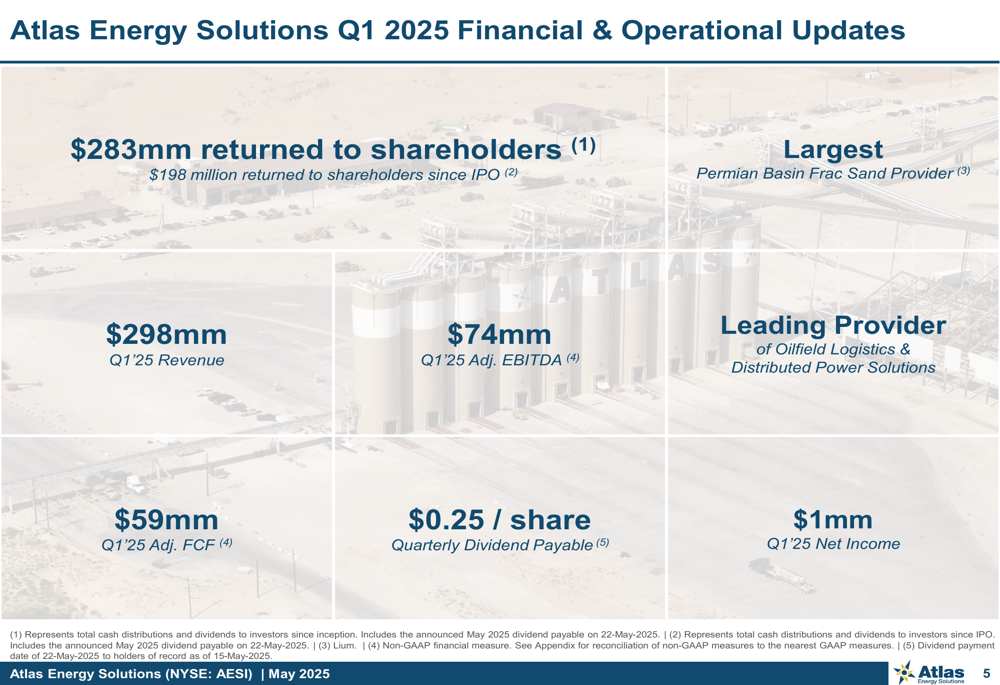

Atlas reported Q1 2025 revenue of $298 million, generating Adjusted EBITDA of $74 million and Adjusted Free Cash Flow of $59 million. However, net income was just $1 million for the quarter, highlighting significant margin pressure despite strong top-line performance. The company maintained its quarterly dividend of $0.25 per share and emphasized its capital return program, noting $283 million returned to shareholders overall, including $198 million since its IPO.

As shown in the following financial highlights slide:

The company’s Q1 2025 Adjusted EBITDA of $74.3 million represents a decline from $78.1 million in Q4 2024, though it improved from $60.6 million in Q1 2024. This sequential decline in EBITDA despite strong revenue suggests continued cost pressures and operational challenges.

Strategic Initiatives and Operational Highlights

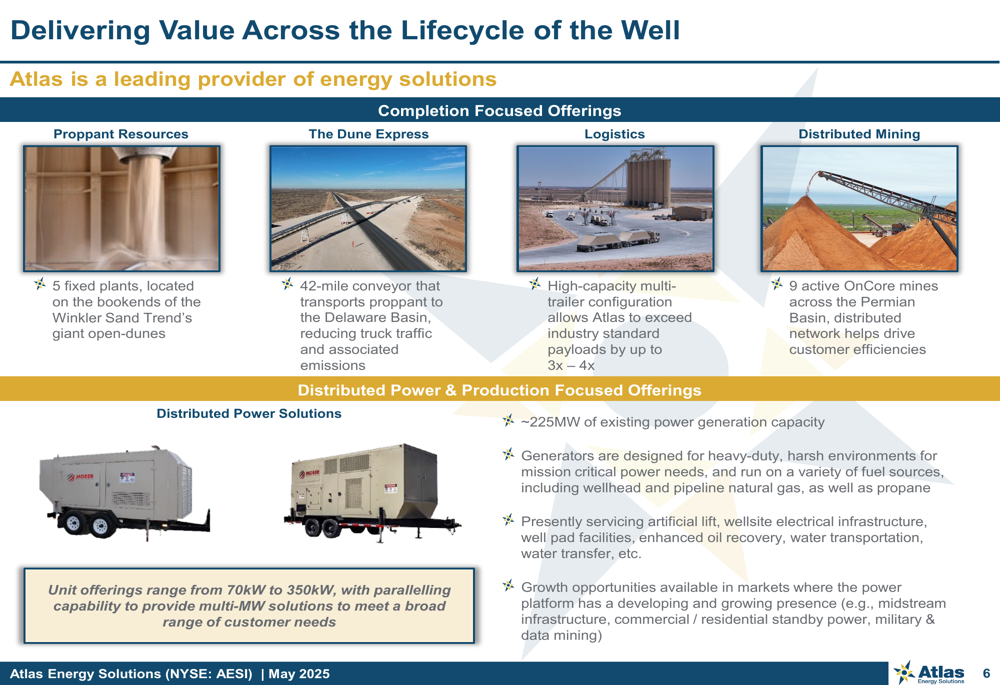

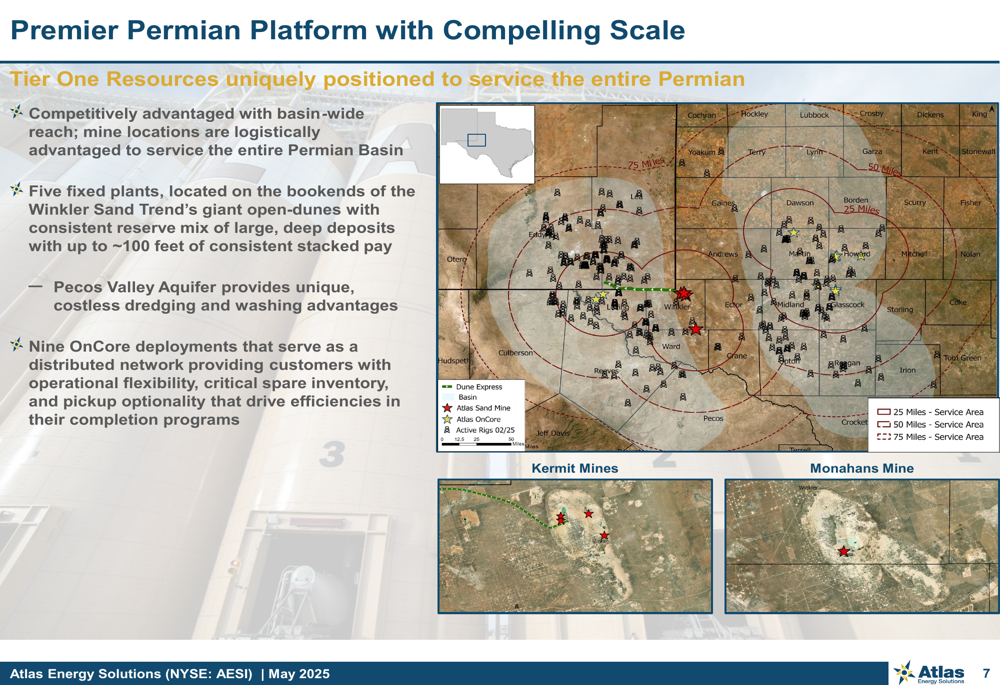

Atlas is emphasizing its integrated approach to serving energy producers across the entire well lifecycle, from proppant resources to logistics and power solutions. The company operates five fixed plants, a 42-mile conveyor system (Dune Express), nine active OnCore mobile mines, and approximately 225MW of existing power generation capacity.

The following slide illustrates Atlas’s comprehensive service offerings:

The company’s strategic positioning across the Permian Basin provides competitive advantages through basin-wide reach. Atlas highlighted that its access to the Pecos Valley Aquifer provides unique, costless dredging and washing advantages for its sand operations.

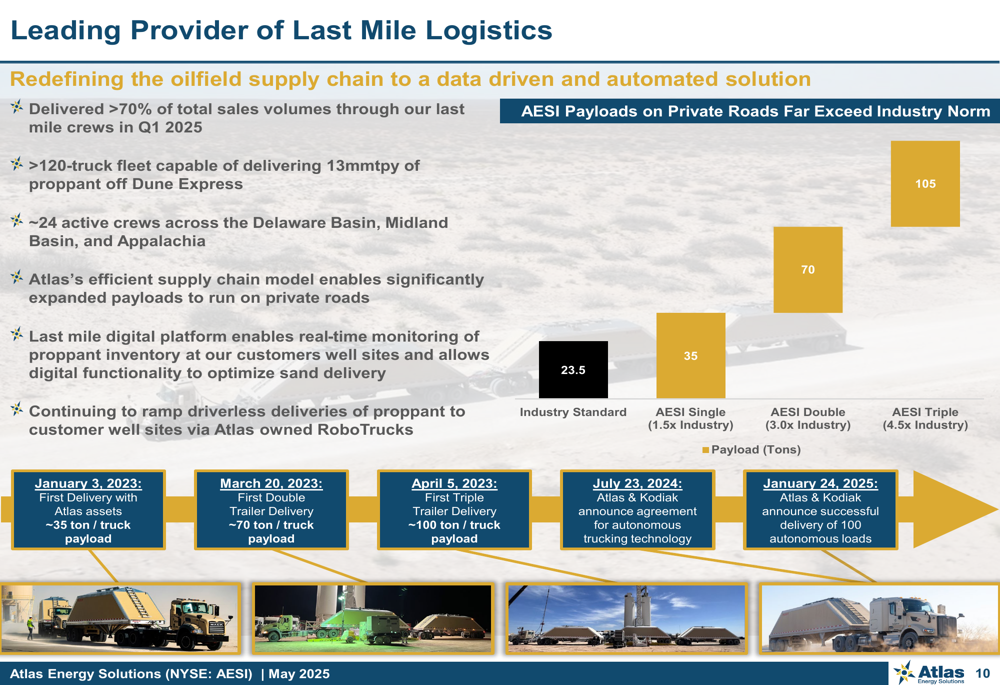

Logistics Innovation and Efficiency Gains

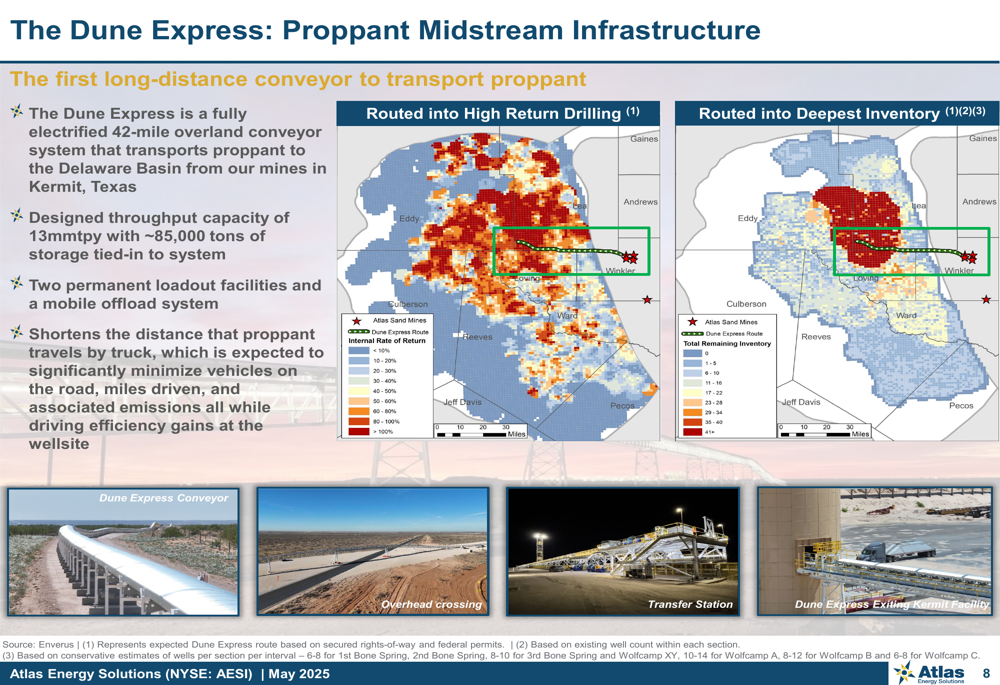

A central focus of Atlas’s presentation was its logistics innovations, particularly the Dune Express conveyor system and autonomous delivery capabilities. The Dune Express, a fully electrified 42-mile overland conveyor, offers 13 million tons per year throughput capacity and approximately 85,000 tons of storage, significantly reducing truck traffic and emissions.

The following slide details the Dune Express infrastructure:

Atlas is also pioneering autonomous delivery with its Kodiak RoboTrucks program, which is expected to complete more than 625 driverless deliveries by the end of May 2025. This initiative represents a significant step toward a fully autonomous proppant supply chain, potentially enabling 24/7 delivery capabilities.

The company’s logistics advantages translate to significantly higher payload capacity compared to industry standards:

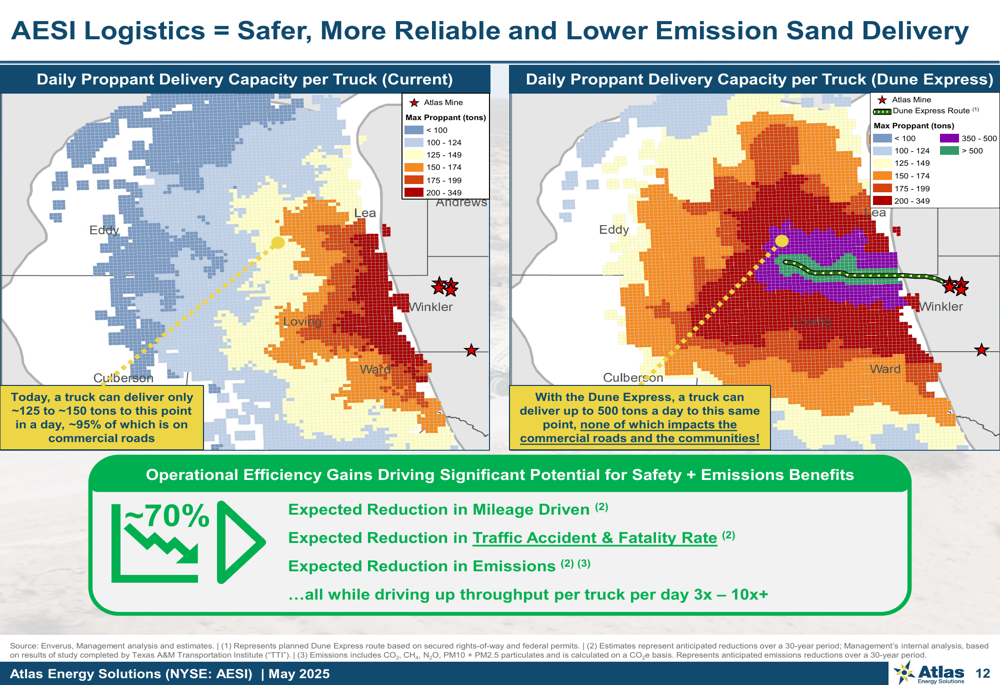

These logistical innovations are expected to yield substantial safety and environmental benefits, with Atlas projecting a 70% reduction in mileage driven and corresponding decreases in traffic accidents and emissions:

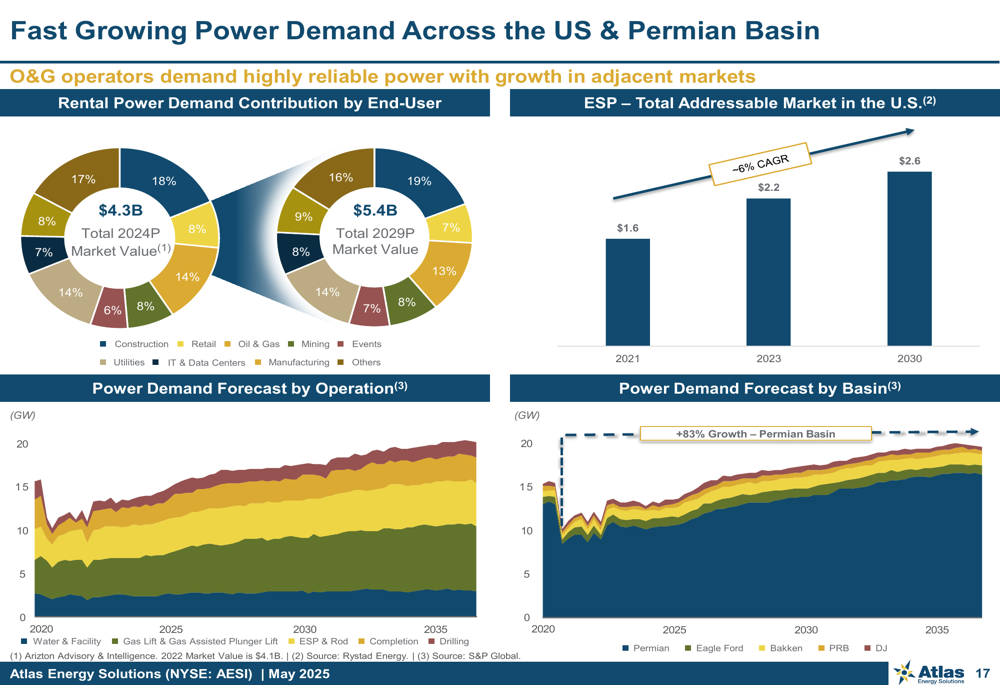

Power Generation (HM:PGV) Expansion

Atlas is diversifying its revenue streams through expansion into power generation, leveraging its Moser Energy Systems acquisition. The company currently operates over 900 natural gas-powered generators with approximately 225MW of existing capacity, offering units ranging from 70kW to 350kW.

The power generation market represents a significant growth opportunity, as illustrated in the following market forecast:

The company highlighted its in-house manufacturing and remanufacturing capabilities, noting that remanufacturing reduces costs by approximately 50%. This vertical integration approach aligns with Atlas’s broader strategy of controlling critical elements of its supply chain.

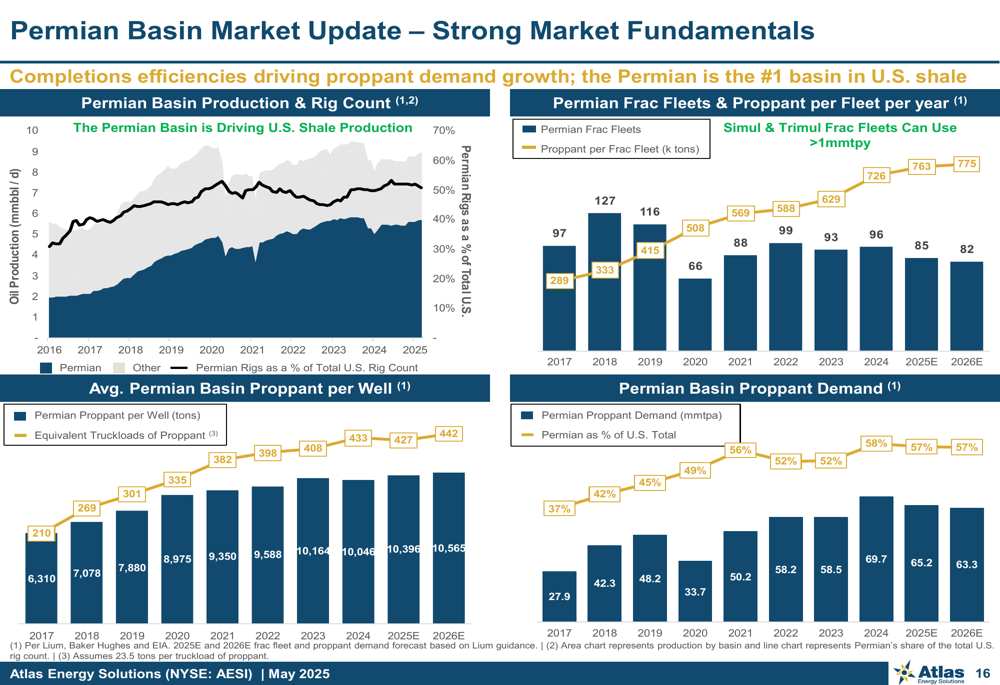

Market Outlook and Forward Guidance

Atlas’s presentation emphasized strong market fundamentals in the Permian Basin, which continues to drive U.S. shale production. The company highlighted increasing proppant demand per well and rising overall basin demand:

While the presentation did not provide specific forward guidance for full-year 2025, the previous earnings report indicated expectations for Adjusted EBITDA to exceed $400 million in 2025, with plans to sell over 25 million tons of proppant, up from 20 million in 2024.

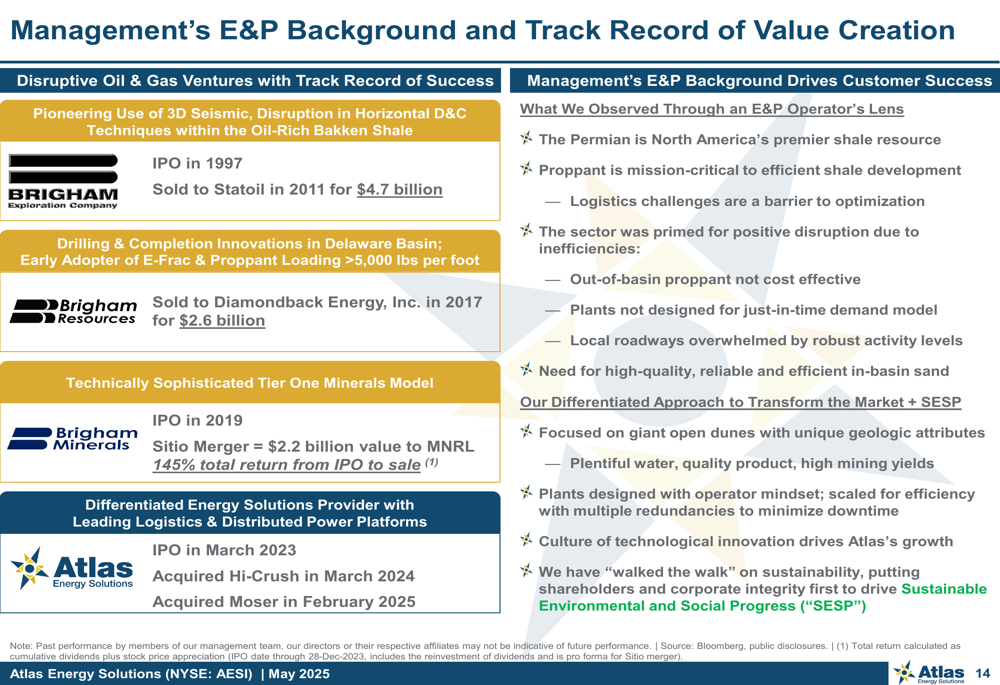

Management Experience and Track Record

Atlas emphasized its management team’s extensive experience in the energy sector, highlighting previous successful ventures including the sale of Brigham Exploration Company to Statoil (OL:EQNR) in 2011 for $4.7 billion and Brigham Resources to Diamondback (NASDAQ:FANG) Energy in 2017 for $2.6 billion.

This track record is presented as evidence of management’s ability to create shareholder value and navigate industry cycles effectively.

Conclusion

Atlas Energy Solutions’ Q1 2025 presentation reflects a company in transition, balancing current financial challenges with ambitious strategic initiatives. While revenue remains strong at $298 million, the minimal net income of $1 million suggests significant margin pressure. The company is betting heavily on logistics innovations and diversification into power generation to drive future growth and profitability.

Investors will likely focus on whether these strategic initiatives can translate into improved bottom-line performance in coming quarters, particularly as the stock continues to trade well below its 52-week high. The company’s continued commitment to shareholder returns through its dividend program provides some support for the stock, but execution on operational improvements will be critical to restoring investor confidence following recent earnings disappointments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.