Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

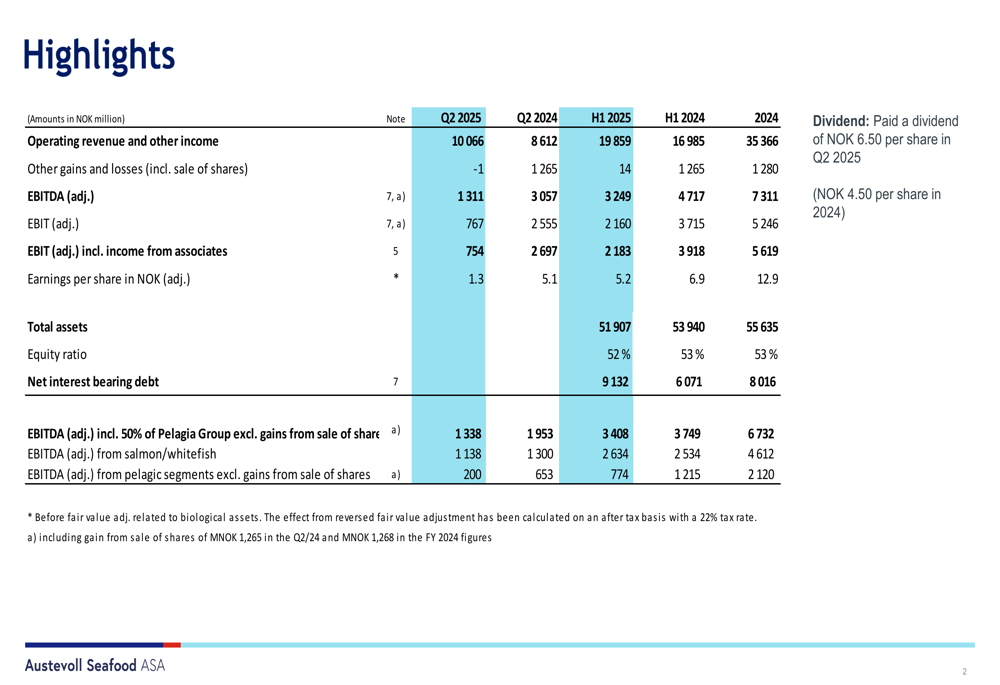

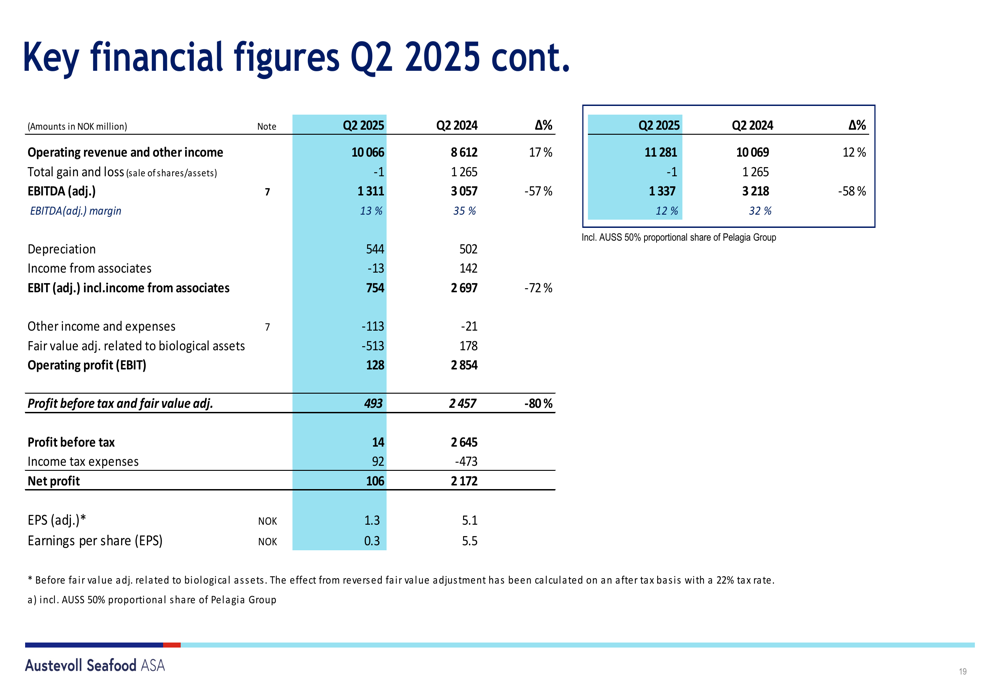

Austevoll Seafood ASA (OB:AUSS) reported mixed results for the second quarter of 2025, with substantial revenue growth overshadowed by significant margin pressure across its business segments. The company achieved a 17% year-over-year increase in operating revenue to NOK 10,066 million, but experienced a steep 57% decline in adjusted EBITDA to NOK 1,311 million compared to the same period last year.

The quarter was characterized by higher production volumes in the salmon segment, offset by lower salmon prices and challenging conditions in the fishmeal and fish oil markets. The company’s diversified business model across fishing, aquaculture, and processing operations provided some resilience amid sector-specific headwinds.

Quarterly Performance Highlights

Austevoll Seafood’s financial performance for Q2 2025 showed significant revenue growth but substantial pressure on profitability metrics. The company reported adjusted EBIT of NOK 767 million, down 70% from NOK 2,555 million in Q2 2024, while adjusted earnings per share fell to NOK 1.3 from NOK 5.1 in the same period last year.

As shown in the following comprehensive financial summary:

Despite the profitability challenges, the company maintained a solid financial position with an equity ratio of 52% and distributed a dividend of NOK 6.50 per share during the quarter, up from NOK 4.50 per share in Q2 2024.

Detailed Financial Analysis

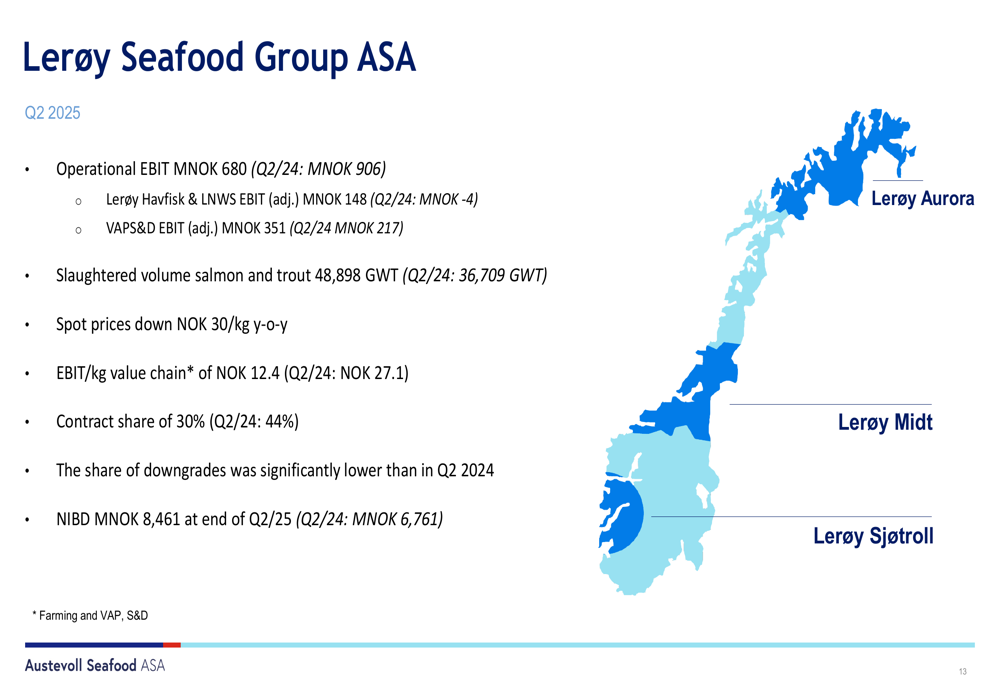

The company’s largest subsidiary, Lerøy Seafood Group ASA, reported an operational EBIT of NOK 680 million in Q2 2025, down from NOK 906 million in Q2 2024. This decline occurred despite a 33% increase in slaughtered salmon and trout volume to 48,898 GWT, as spot prices fell by NOK 30/kg year-over-year. The contract share decreased to 30% from 44% in the same period last year.

The key performance metrics for Lerøy Seafood Group are illustrated below:

The consolidated financial figures for Q2 2025 show the significant impact of price pressure across segments, with EBITDA declining by 57% despite the 17% revenue growth:

In the pelagic segment, Austral Group S.A.A. in Peru reported revenue of NOK 691 million, with raw material intake of 233,000 tons. While sales volumes increased substantially year-over-year, fishmeal prices declined by 11% and fish oil prices plummeted by 58% compared to Q2 2024, significantly impacting profitability.

FoodCorp Chile S.A. showed positive operational developments with revenue of NOK 400 million in Q2 2025, benefiting from an increased quota of 81 KMT in 2025 compared to 65 KMT in 2024. The company reported high activity in the quarter with increased sales volumes for frozen products and fishmeal.

Market Context

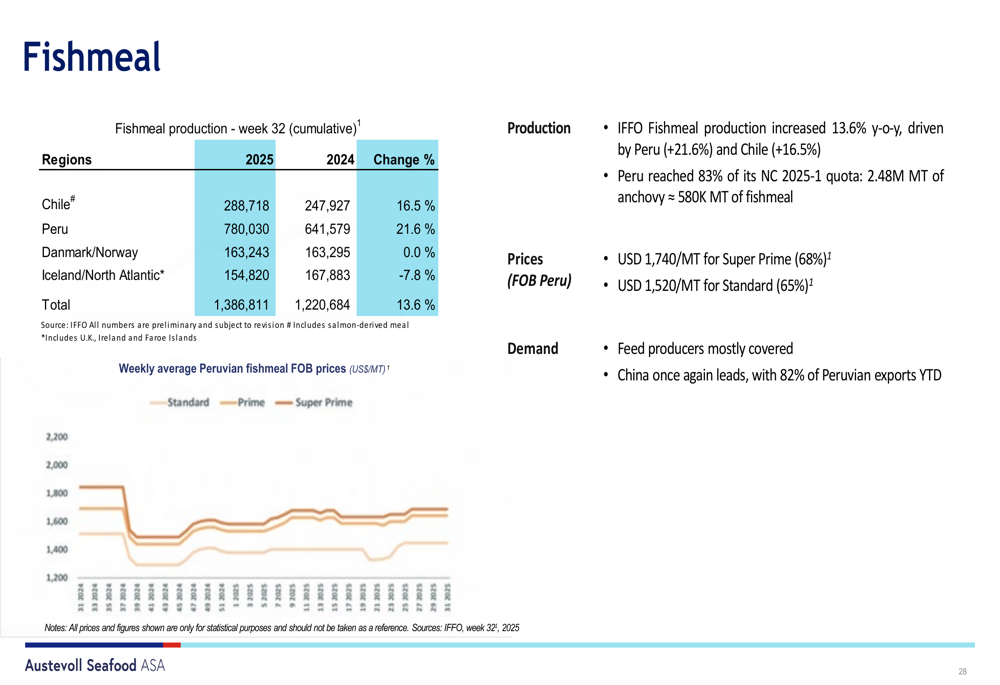

The fishmeal market faced challenges in Q2 2025, with Peru reaching 83% of its North-Central 2025-1 anchovy quota, translating to approximately 580,000 MT of fishmeal production. Prices for Super Prime (68%) fishmeal stood at USD 1,740/MT, while Standard (65%) was at USD 1,520/MT.

The following chart provides an overview of the fishmeal market outlook:

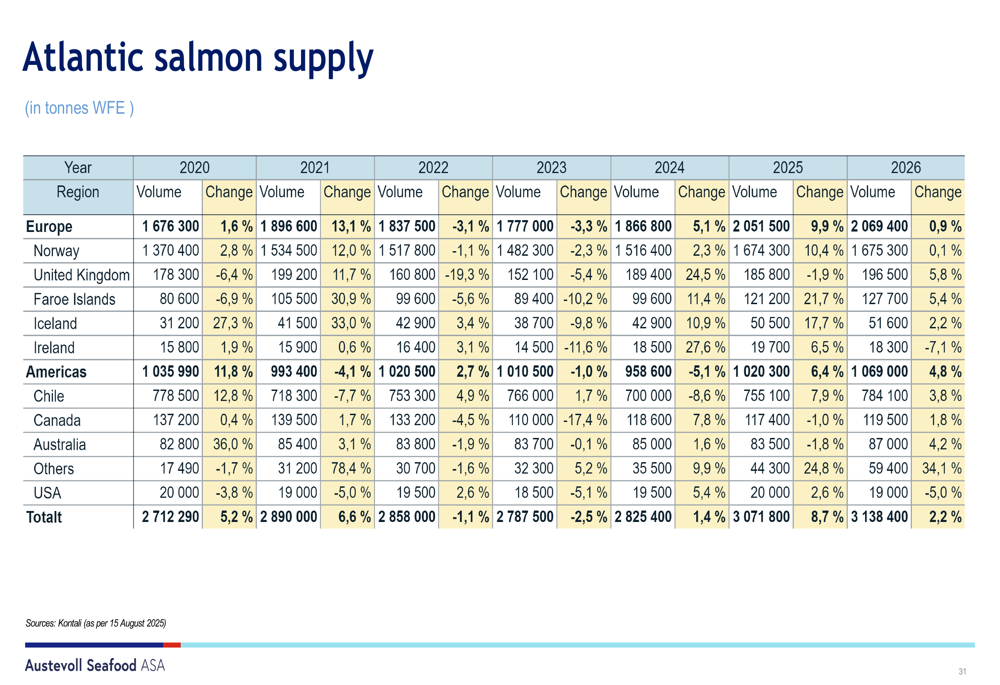

In the salmon market, supply is projected to grow modestly through 2026, with Atlantic salmon harvest volumes in Europe showing a 19.4% increase compared to the prior period:

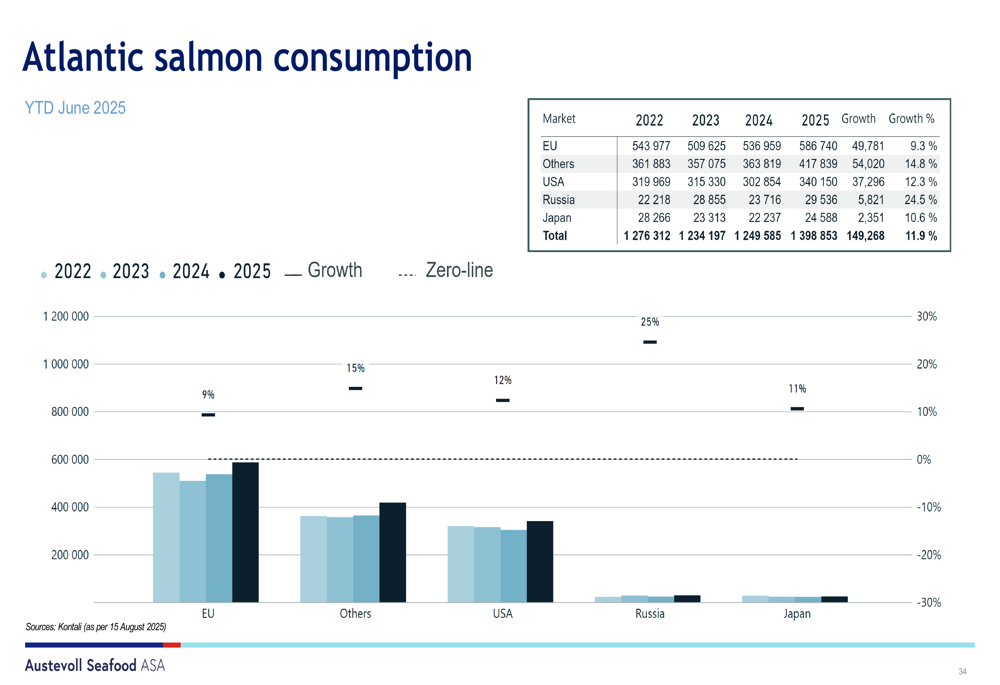

Salmon consumption continues to show strong growth trends across global markets, with an 11.9% increase from 2022 to 2025 levels, with the EU remaining the largest consumption market:

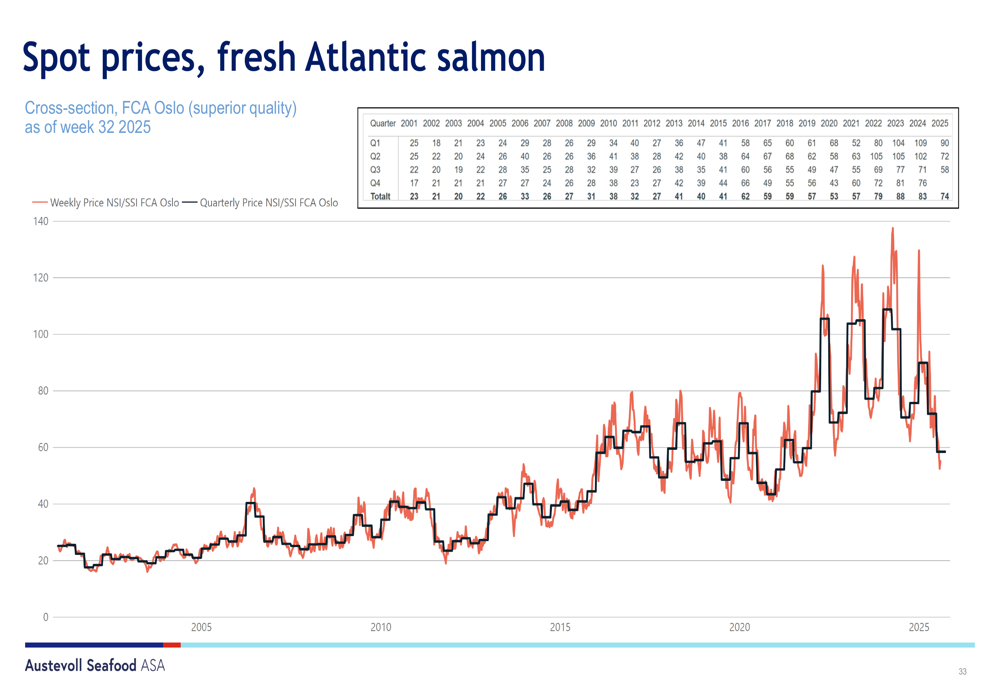

Spot prices for fresh Atlantic salmon have shown significant volatility over time, with current prices below historical averages:

Forward-Looking Statements

Looking ahead, Austevoll Seafood highlighted several key points for the remainder of 2025. The company noted positive biological development in the salmon segment quarter-to-date in H2 2025, with lower salmon and trout prices helping to build markets. While facing a challenging quota situation in some fishing areas, the company observed positive price development.

The company’s key conclusions are summarized below:

For South America, the first fishing season started on April 22 with a total quota of 3 million tons, though the fishery faced challenges with a significantly slower daily catch rate. In Chile, the company will benefit from a 25% increase in jack mackerel quota for 2025.

In the North Atlantic (Pelagia Holding AS), the blue whiting season continued in Q2 for feed production, but decreasing prices, especially for marine oils, put pressure on margins and total earnings. The company noted ICES recommendations for 2025 quotas, including a 5% decrease for blue whiting, 22% decrease for mackerel, and 3% increase for NVG herring.

Strategic Initiatives

Despite the challenging market conditions, Austevoll Seafood continued to invest in its future growth. The company reported investments in two new second-hand fishing vessels during the quarter, strengthening its fishing fleet capacity. The company maintained its focus on operational efficiency and biological performance in its salmon operations, which should position it well when market conditions improve.

The company’s diversified business model across different seafood segments and geographies provides some resilience against segment-specific challenges, though the current quarter demonstrated that price pressure across multiple segments can still significantly impact overall profitability.

With a solid financial position and continued operational improvements, Austevoll Seafood appears positioned to navigate the current market challenges while maintaining its long-term growth strategy. However, investors should monitor the development of salmon prices and fishmeal/fish oil markets closely, as these will be key determinants of the company’s financial performance in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.