Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Avanos Medical (TASE:BLWV) Inc (NYSE:AVNS) presented its Q1 2025 earnings results on May 6, 2025, showcasing continued organic growth in its strategic segments while lowering full-year earnings guidance due to tariff headwinds. The medical device company’s stock rose 6.07% to $12.93 following the presentation, reflecting investor optimism despite the guidance reduction.

The company, which focuses on specialty nutrition systems and pain management solutions, reported modest revenue growth and improved earnings per share compared to the same period last year, continuing the positive momentum seen in its Q4 2024 results when it exceeded analyst expectations.

Quarterly Performance Highlights

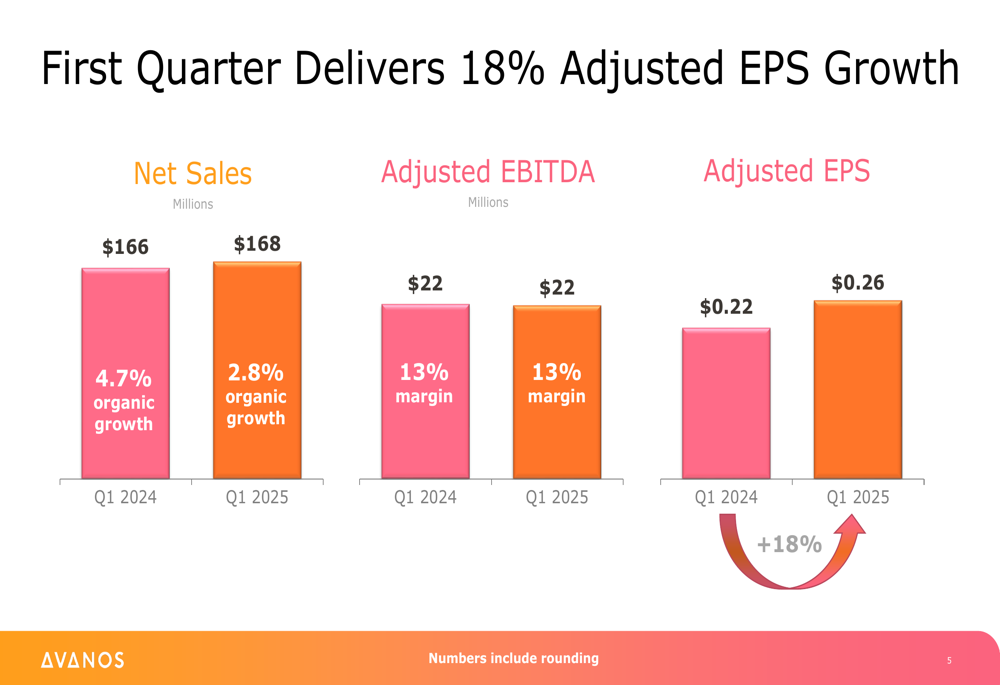

Avanos reported Q1 2025 net sales of $168 million, a slight increase from $166 million in Q1 2024, with organic growth of 4.7%. Adjusted EBITDA remained steady at $22 million, maintaining a 13% margin year-over-year. Notably, adjusted earnings per share increased 18% to $0.26 from $0.22 in the prior year period.

As shown in the following financial performance comparison:

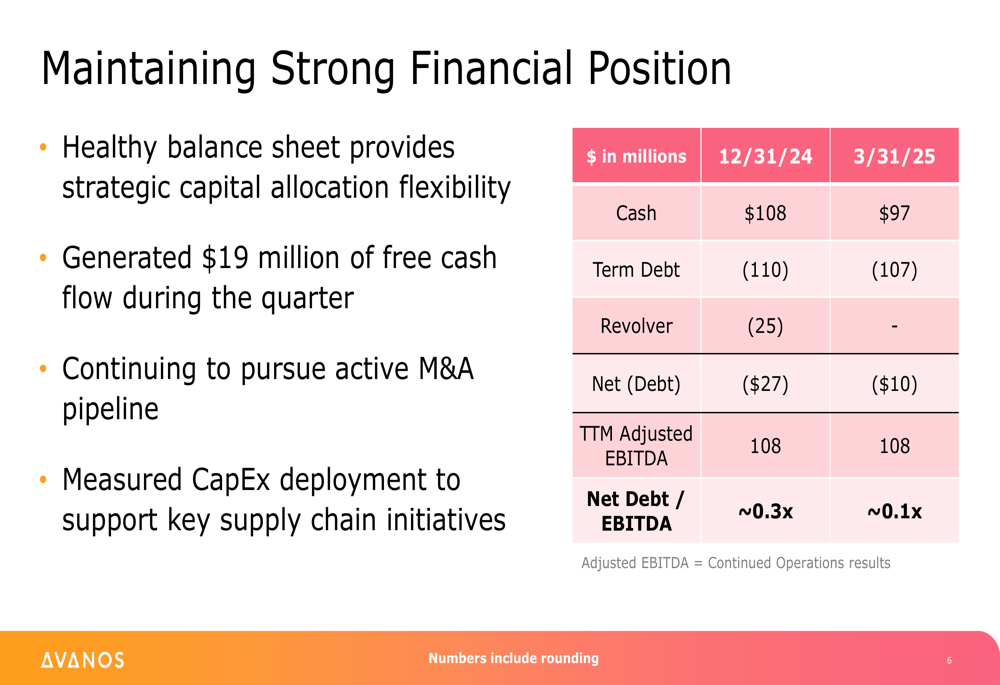

The company highlighted its solid commercial execution and mid-single-digit organic growth in strategic segments as key drivers of the quarterly performance. Free cash flow generation was strong at $19 million during the quarter, contributing to an improved balance sheet position.

Avanos has significantly strengthened its financial position, reducing its net debt to EBITDA ratio from approximately 0.3x at the end of 2024 to approximately 0.1x by March 31, 2025, as illustrated in this financial data:

Segment Analysis

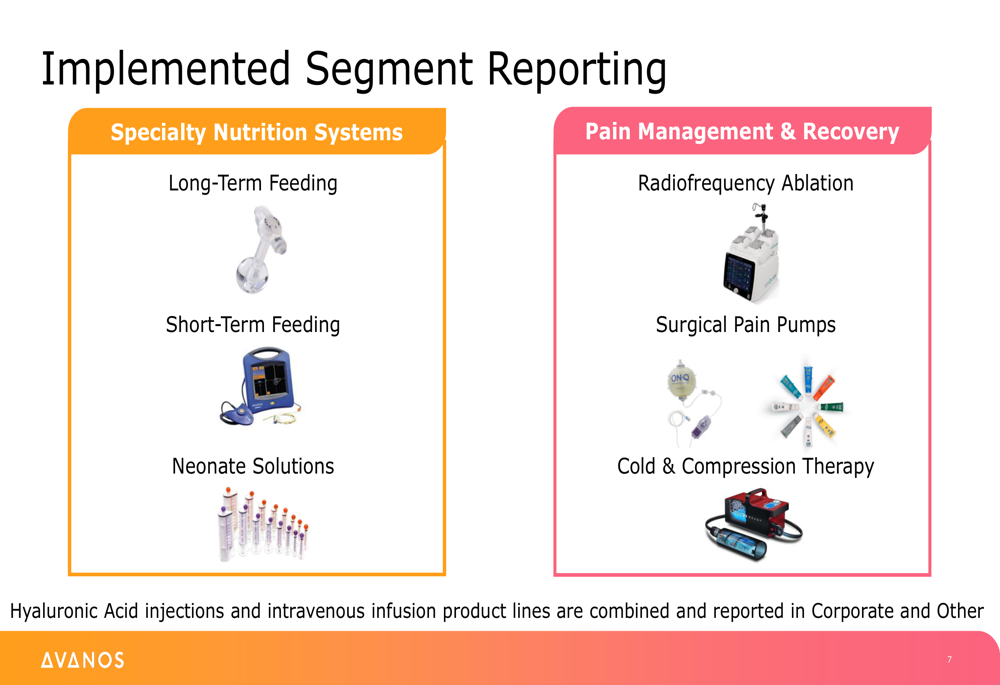

During the quarter, Avanos implemented formal segment reporting, dividing its business into two primary segments: Specialty Nutrition Systems and Pain Management & Recovery. This new structure provides greater transparency into the performance of different business lines.

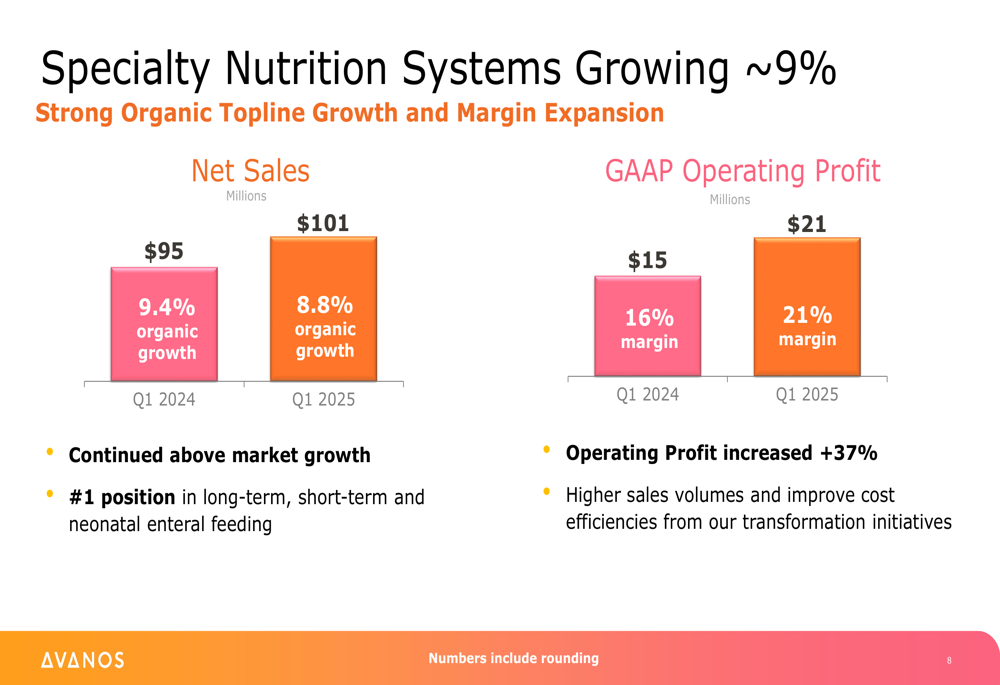

The Specialty Nutrition Systems segment, which includes long-term feeding, short-term feeding, and neonate solutions, emerged as the standout performer. This segment grew approximately 9%, with net sales increasing from $95 million in Q1 2024 to $101 million in Q1 2025. More impressively, GAAP operating profit for this segment jumped 37% to $21 million, with margins expanding from 16% to 21%.

The following chart illustrates the segment’s strong performance:

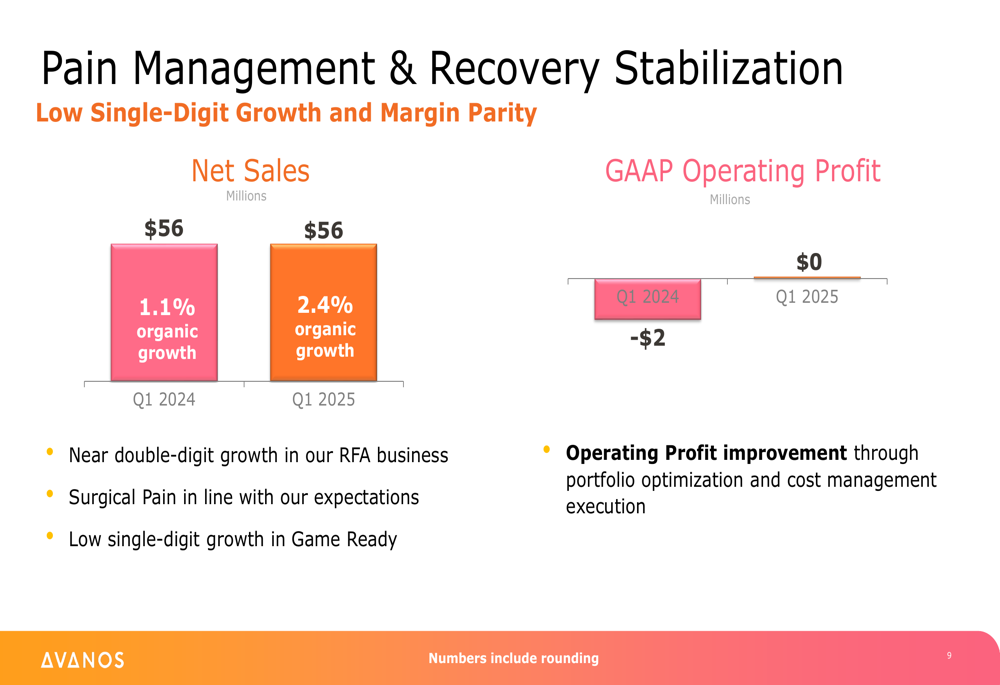

In contrast, the Pain Management & Recovery segment showed signs of stabilization with flat net sales of $56 million but improved from a $2 million operating loss in Q1 2024 to breakeven in Q1 2025. This segment, which includes radiofrequency ablation, surgical pain pumps, and cold & compression therapy, saw near double-digit growth in the RFA business while Game Ready products achieved low single-digit growth.

Strategic Initiatives & Transformation

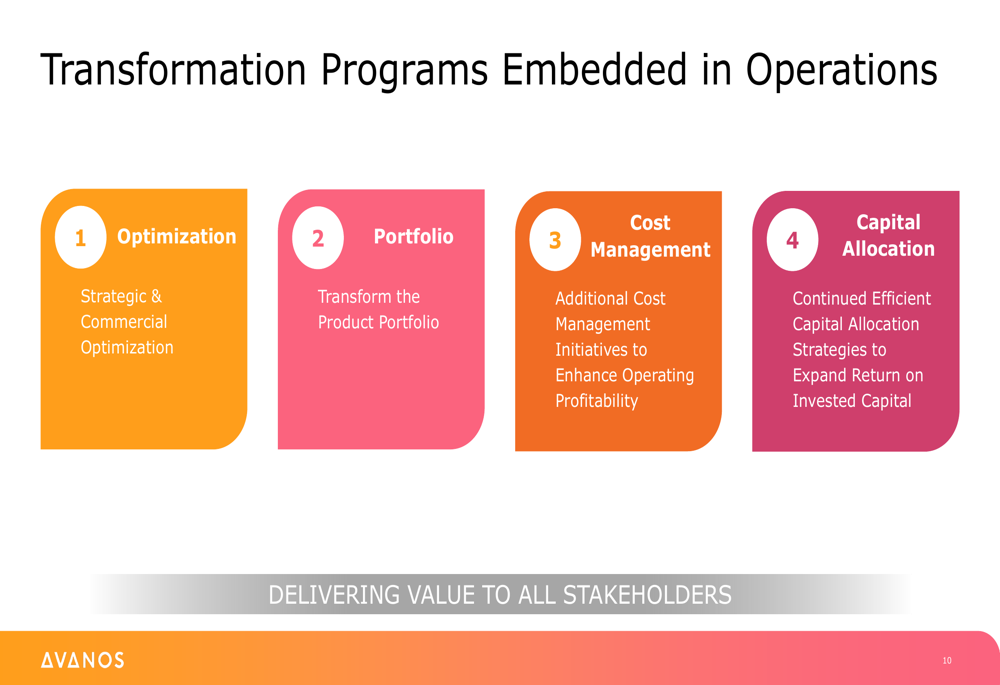

Avanos continues to execute on four key transformation programs designed to enhance shareholder value. These initiatives focus on strategic and commercial optimization, portfolio transformation, cost management, and efficient capital allocation.

CEO Dave Pacitti emphasized that these transformation efforts are already yielding results, particularly in the Specialty Nutrition Systems segment where improved cost efficiencies contributed to the significant margin expansion. The Pain Management & Recovery segment’s improved operating profit was attributed to portfolio optimization and cost management execution.

The company also noted it maintains an active M&A pipeline, suggesting potential strategic acquisitions, particularly in the higher-growth Specialty Nutrition Systems segment.

Outlook & Guidance

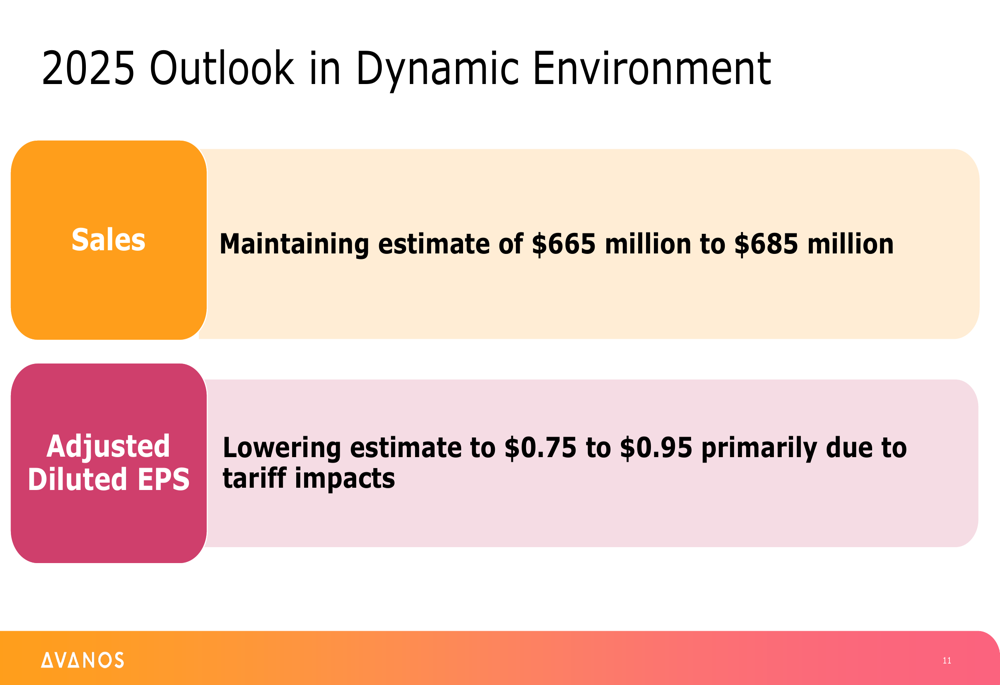

While Avanos maintained its 2025 sales guidance of $665 million to $685 million, it lowered its adjusted diluted EPS forecast to $0.75-$0.95 from the previous $1.05-$1.25 range provided during the Q4 2024 earnings call. The company attributed this significant reduction primarily to tariff impacts affecting its supply chain.

This guidance reduction represents approximately a 25% decrease at the midpoint and marks a notable shift from the more optimistic outlook presented just one quarter ago. The tariff challenges appear to be affecting margins despite ongoing cost management initiatives.

Conclusion

Avanos Medical’s Q1 2025 results present a mixed picture for investors. The company continues to demonstrate solid organic growth, particularly in its Specialty Nutrition Systems segment, and has strengthened its balance sheet. However, the significant downward revision to full-year EPS guidance due to tariff impacts raises concerns about margin pressure in the coming quarters.

The market’s positive reaction suggests investors may be focusing on the company’s improved financial position and segment performance rather than the reduced guidance. As Avanos continues to execute its transformation initiatives, the company’s ability to mitigate tariff impacts and maintain growth momentum will be crucial factors to watch throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.