TSX lower as gold rally takes a breather

Introduction & Market Context

Bandwidth Inc. (NASDAQ:BAND) presented its Q2 2025 earnings results on July 29, 2025, revealing solid performance across key metrics. The company’s stock closed up 8.14% at $16.21 in the previous session and showed additional momentum with a 2.41% gain to $16.60 in premarket trading, reflecting positive investor sentiment following the results.

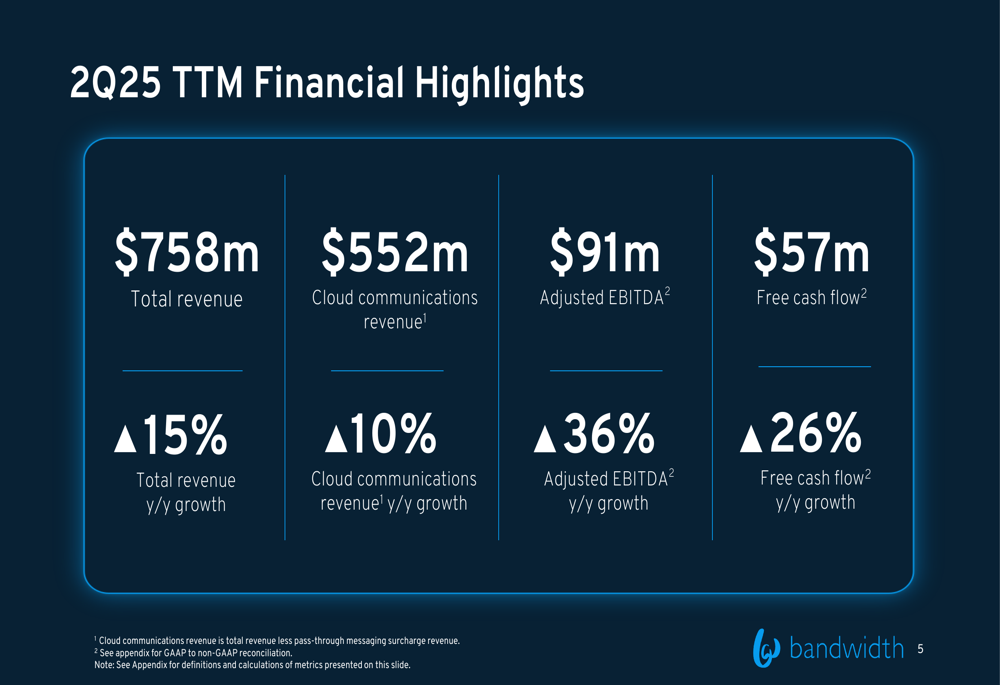

The cloud communications platform provider reported 9% year-over-year revenue growth (normalized for political campaign revenue) and raised its full-year EBITDA guidance, driven particularly by strong performance in its Enterprise Voice segment, which grew by 29% compared to the same period last year.

Quarterly Performance Highlights

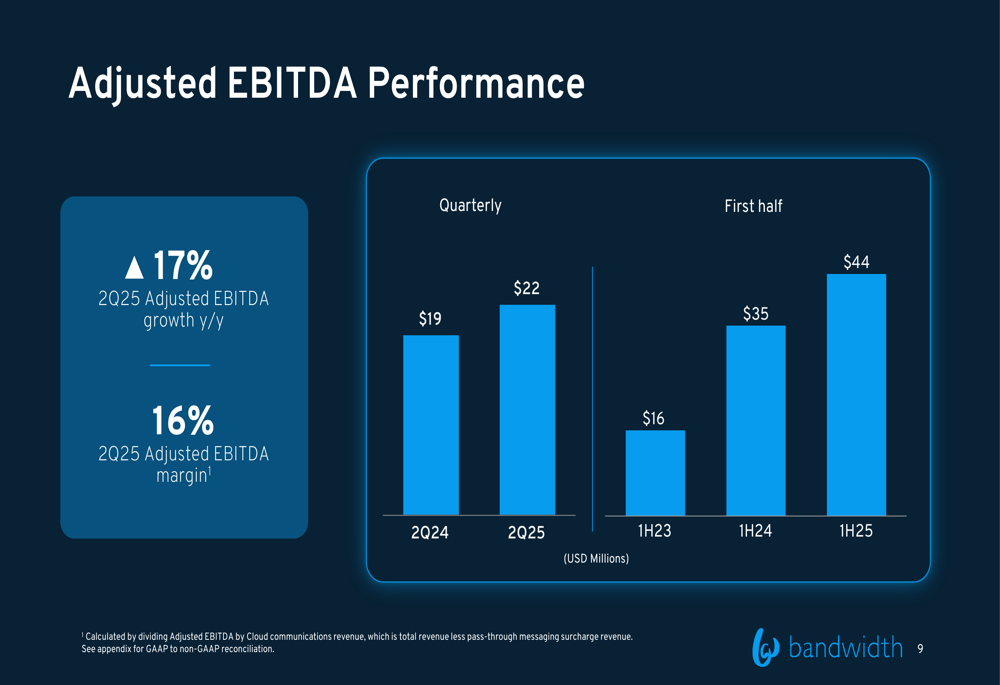

Bandwidth reported Q2 2025 total revenue of $180 million, representing 9% year-over-year growth when normalized for political campaign revenue. The company’s adjusted EBITDA reached $22 million, increasing 17% year-over-year, with an adjusted EBITDA margin of 16%.

As shown in the following financial highlights chart, Bandwidth’s trailing twelve months performance demonstrates consistent growth across key metrics:

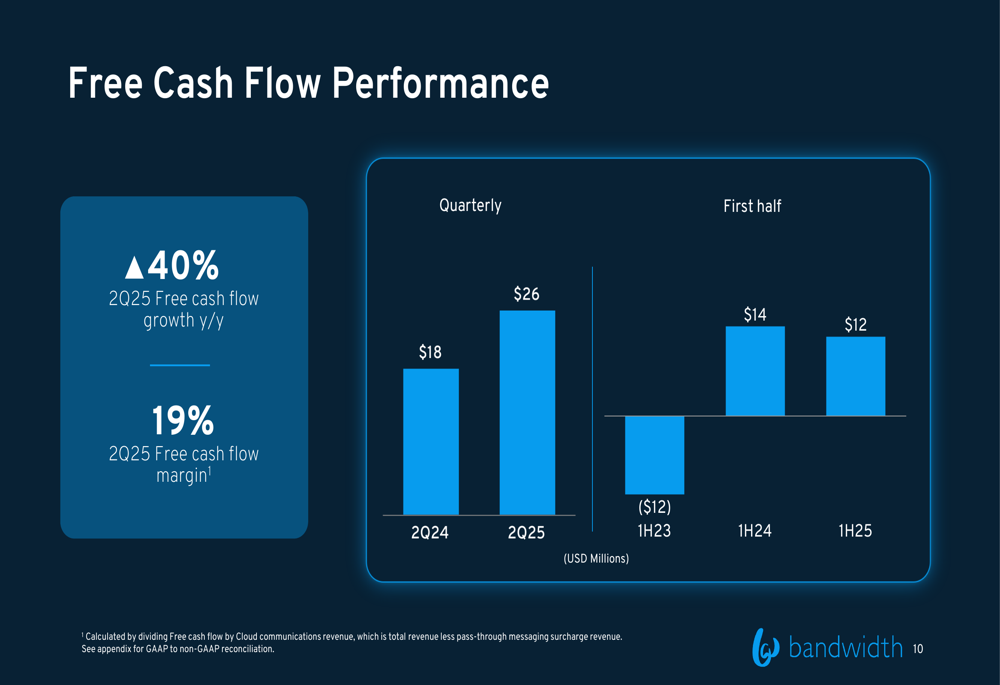

Free cash flow performance was particularly impressive, reaching $26 million in Q2 2025, a 40% increase compared to the same period last year. The free cash flow margin expanded to 19%, highlighting the company’s improving operational efficiency and scalable business model.

As illustrated in the quarterly free cash flow comparison:

Revenue Breakdown & Customer Metrics

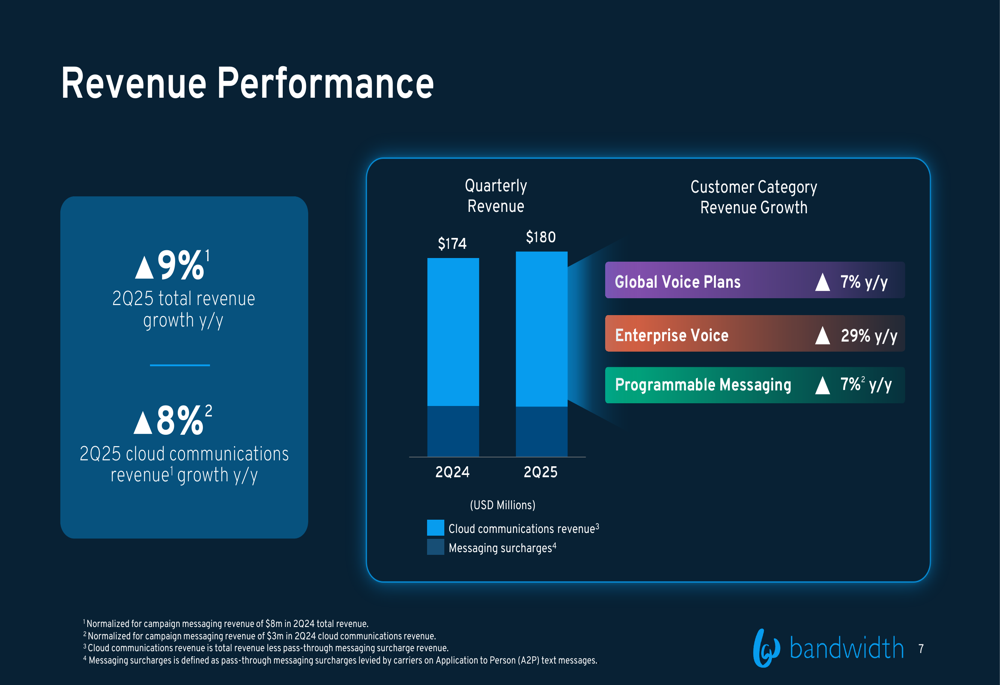

Bandwidth’s revenue growth was distributed across all three of its customer categories, with Enterprise Voice leading the way at 29% year-over-year growth. Global Voice Plans and Programmable Messaging each contributed 7% year-over-year growth.

The following chart breaks down the company’s revenue performance by customer category:

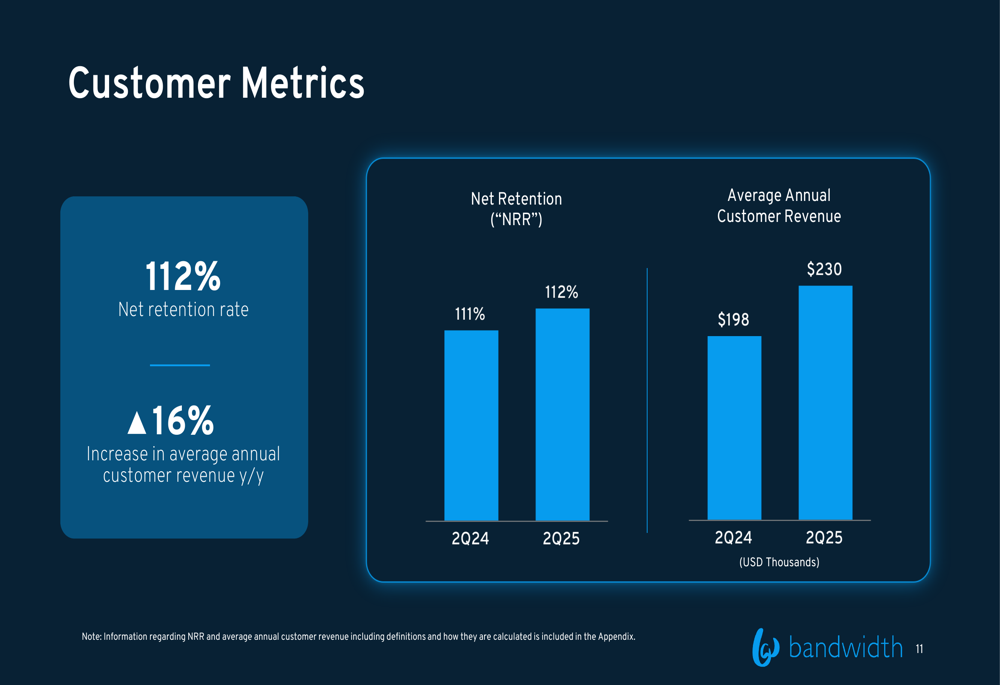

Customer loyalty metrics remain strong, with Bandwidth maintaining a name retention rate exceeding 99% and improving its net retention rate to 112% in Q2 2025, up from 111% in Q2 2024. The company’s top 20 customers have a median tenure of 11 years, demonstrating the stickiness of Bandwidth’s communications platform.

Average annual customer revenue increased 16% year-over-year to $230,000, compared to $198,000 in Q2 2024, indicating successful upselling and expansion within the existing customer base.

Margin Expansion & Cash Flow

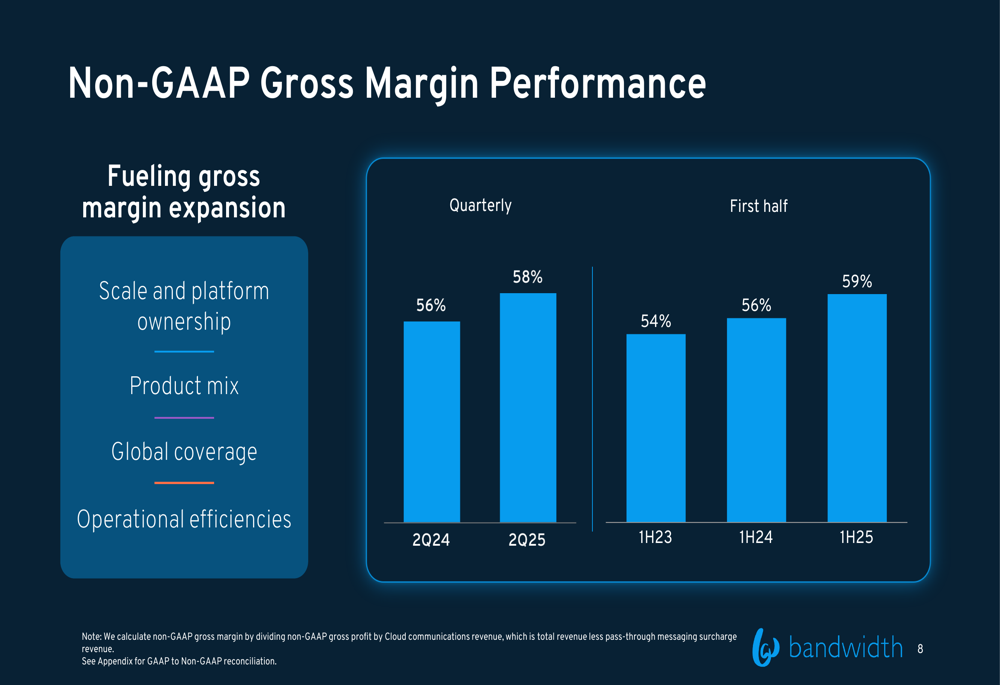

Bandwidth’s non-GAAP gross margin expanded to 58% in Q2 2025, up from 56% in the same period last year. The company attributes this improvement to scale and platform ownership, product mix, global coverage expansion, and operational efficiencies.

The following chart illustrates the company’s gross margin performance:

This margin expansion, coupled with disciplined operational execution, contributed to the 17% year-over-year growth in adjusted EBITDA, reaching $22 million for the quarter.

Forward Guidance & Strategic Focus

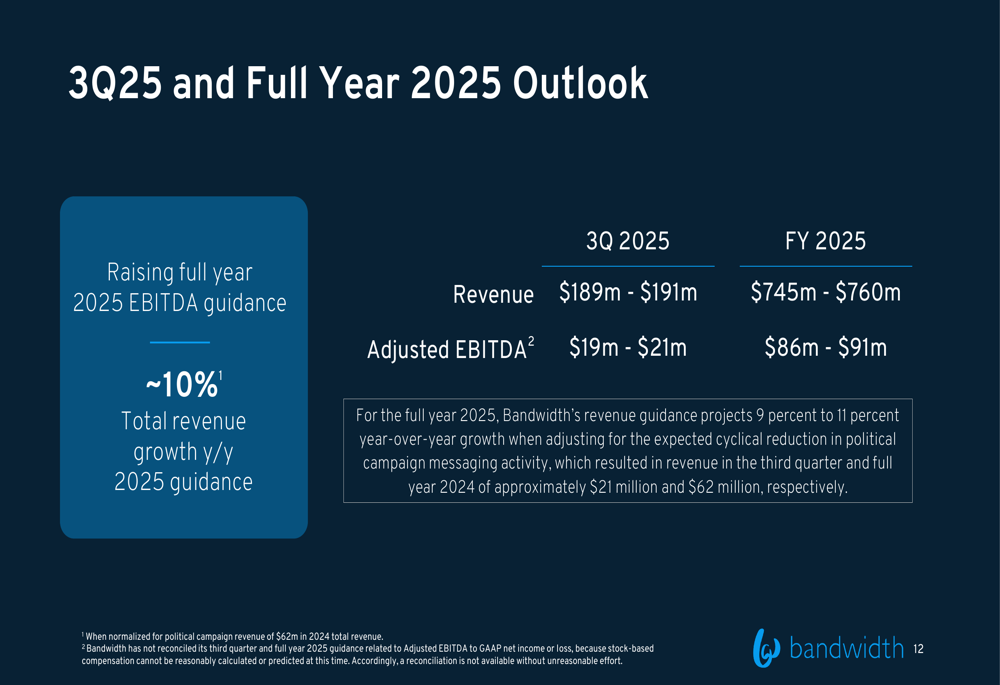

Bandwidth raised its full-year 2025 EBITDA guidance while maintaining its revenue outlook. For Q3 2025, the company expects revenue between $189 million and $191 million, with adjusted EBITDA between $19 million and $21 million. For the full year 2025, Bandwidth forecasts revenue of $745 million to $760 million and adjusted EBITDA of $86 million to $91 million.

The company’s outlook represents approximately 10% year-over-year organic revenue growth for 2025, normalized for political campaign revenue.

A key strategic focus highlighted in the presentation is the growing adoption of AI voice integrations among enterprise customers. Bandwidth noted that its Maestro and AlBridge software APIs and orchestration capabilities are seeing "meaningful traction" as enterprises increasingly incorporate AI into their voice communications.

The company’s global communications platform serves a diverse customer base across three categories, as illustrated in this overview:

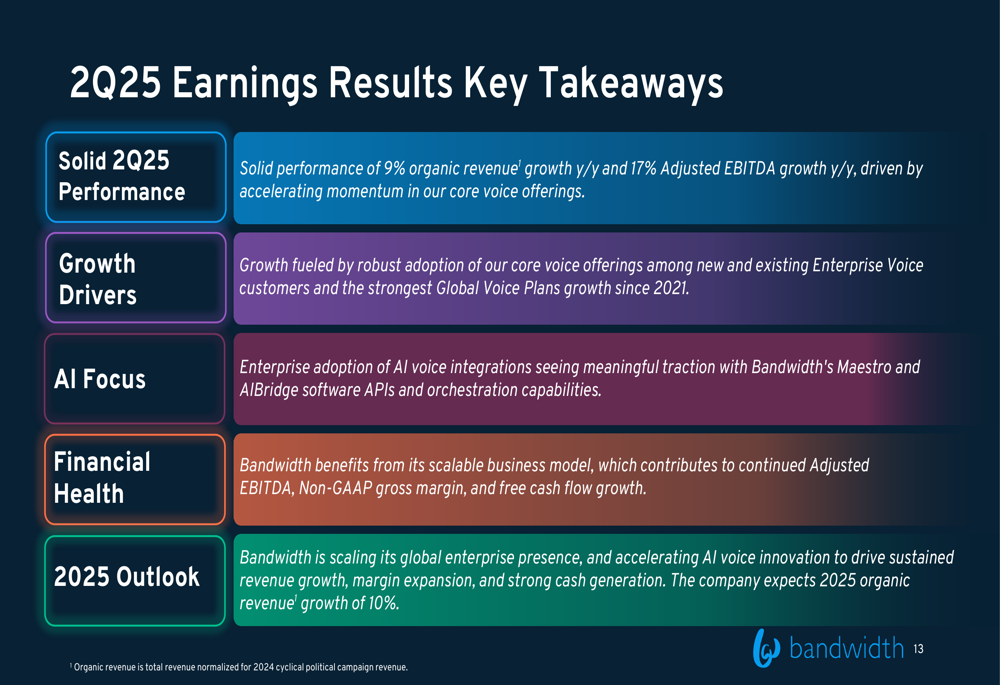

Key Takeaways

Bandwidth summarized its Q2 2025 performance with five key messages that emphasize its growth trajectory and strategic positioning:

These results build on the momentum reported in Q1 2025, when Bandwidth exceeded analyst expectations with EPS of $0.36 against forecasts of $0.26. The company’s consistent performance across multiple quarters suggests its strategy of expanding AI capabilities and global network reach is yielding positive results.

With strong customer retention metrics, expanding margins, and accelerating growth in the Enterprise Voice segment, Bandwidth appears well-positioned to deliver on its full-year guidance while continuing to benefit from enterprise adoption of AI-enhanced communications solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.