U.S. stocks rise on Fed cut bets; earnings continue to flow

Bank of America Corp (NYSE:BAC) delivered impressive third-quarter results according to its October 15, 2025 earnings presentation, with revenue growing 11% year-over-year and earnings per share jumping 31%. The stock responded positively, rising 5.26% following the announcement to reach $52.73, approaching its 52-week high of $52.88.

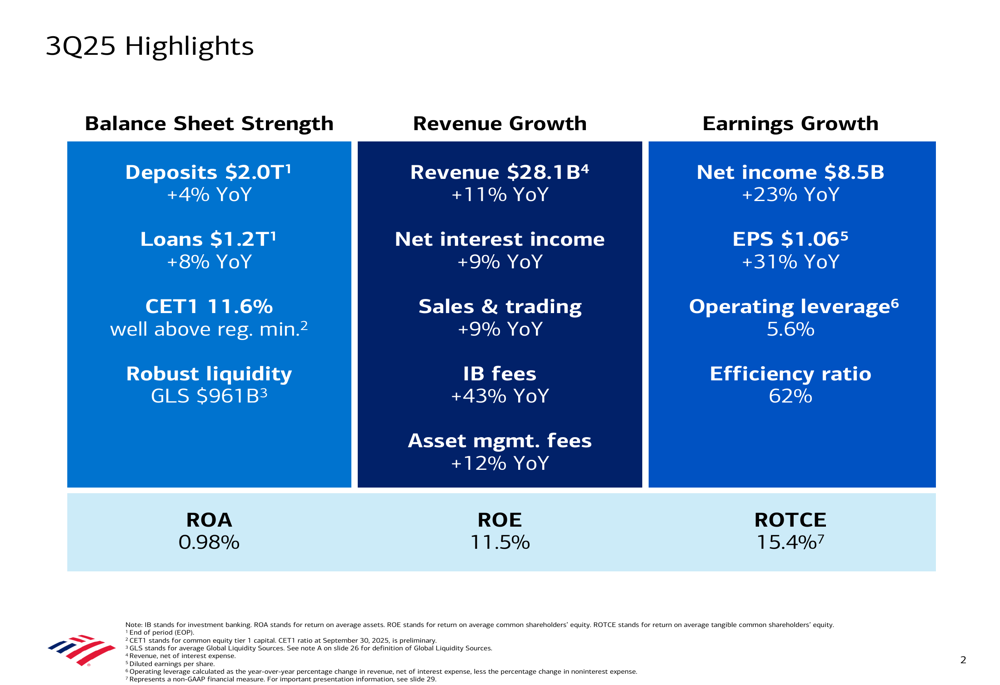

Quarterly Performance Highlights

The banking giant reported net income of $8.5 billion for Q3 2025, representing a 23% increase from the same period last year. Earnings per share reached $1.06, significantly outpacing analyst expectations of $0.95. Revenue rose to $28.1 billion, up 11% year-over-year, driven by growth across all business segments.

As shown in the following comprehensive financial highlights chart, the bank demonstrated strength across key metrics:

The bank’s efficiency ratio improved to 62%, down from 65% in the third quarter of 2024, generating operating leverage of 5.6%. Return on tangible common equity (ROTCE) reached 15.4%, while return on equity (ROE) and return on assets (ROA) came in at 11.5% and 0.98%, respectively.

The income statement reveals consistent improvement across key financial metrics compared to both the previous quarter and the same period last year:

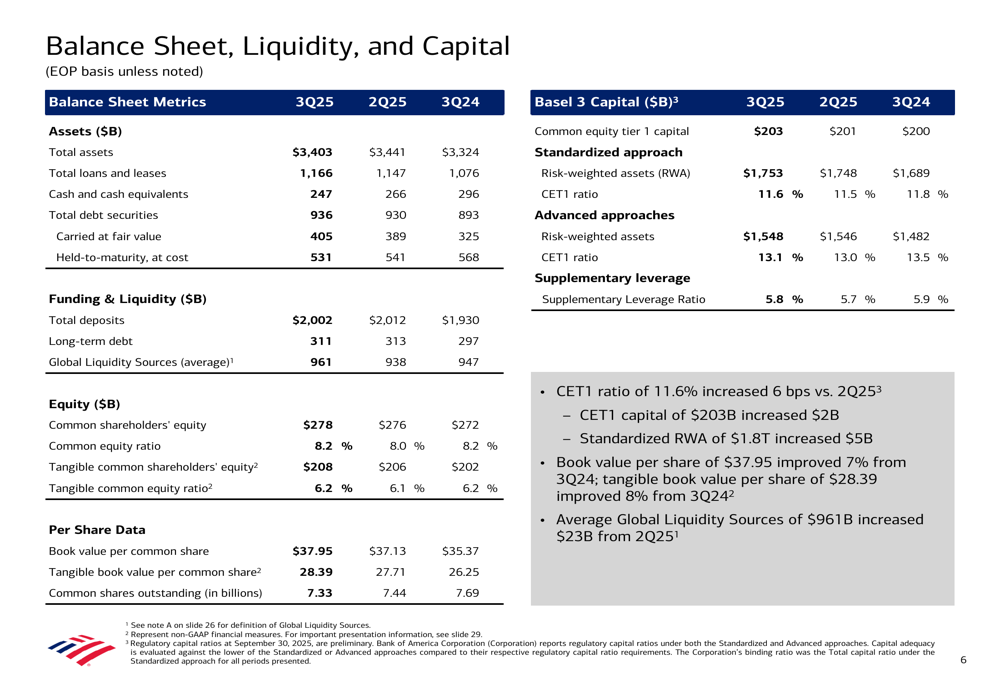

Balance Sheet Strength & Capital Return

Bank of America maintained a robust balance sheet with total deposits of $2.0 trillion, up 4% year-over-year, and loans of $1.2 trillion, increasing 8% from the previous year. The bank’s Common Equity Tier 1 (CET1) ratio stood at 11.6%, well above regulatory requirements.

The following chart illustrates the bank’s strong balance sheet position:

During the quarter, Bank of America returned $7.4 billion to shareholders, including $2.1 billion in common dividends and $5.3 billion in share repurchases, demonstrating confidence in its financial position and commitment to shareholder returns.

Segment Performance

All four business segments contributed to the bank’s strong performance. Investment banking fees were particularly impressive, surging 43% year-over-year, while asset management fees grew 12%.

The Consumer Banking segment added approximately 212,000 net new checking accounts, marking 27 consecutive quarters of net growth. Consumer investment assets reached $580 billion, up 17% year-over-year.

As illustrated in the following organic growth chart, the bank continues to expand its customer base and deepen relationships across segments:

The Global Wealth & Investment Management division reported client balances of $4.6 trillion, up 11% year-over-year, with assets under management reaching $2.1 trillion, a 13% increase.

In Global Banking, Bank of America improved to #3 in investment banking fee ranking, gaining 136 basis points of market share compared to the third quarter of 2024. Average deposits in this segment grew 15% year-over-year to $632 billion.

Net Interest Income Growth

Net interest income, a key revenue driver for banks, increased 9% year-over-year to $15.2 billion ($15.4 billion on a fully taxable equivalent basis). The net interest yield improved to 2.48%, up from 2.40% in the third quarter of 2024.

The following chart details the steady improvement in net interest income:

Asset Quality

Bank of America’s asset quality remained strong, with net charge-offs decreasing to $1.37 billion in Q3 2025 from $1.53 billion in Q3 2024. The provision for credit losses also declined to $1.30 billion from $1.54 billion in the same period last year.

The following chart illustrates the improving trend in asset quality:

Digital Transformation

The bank continues to make significant progress in its digital transformation initiatives. In Consumer Banking, digital adoption remains strong with increasing engagement across platforms.

The following chart highlights key digital metrics in the consumer segment:

In Global Banking, digital adoption is also accelerating, with increasing mobile app sign-ins and CashPro app payments. The bank’s AI-powered virtual assistant, Erica, continues to gain traction with both consumer and commercial clients.

Forward Outlook

Looking ahead, Bank of America expects net interest income growth of 5-7% in 2026, with Q4 2025 net interest income projected to be $15.6 billion or higher. The bank remains focused on organic growth and technology investment, with plans to provide a detailed long-term outlook during its Investor Day in November.

CEO Brian Moynihan emphasized the benefits of the bank’s diversified business model during the earnings call, stating, "Our results underscore the benefits of a diversified business model." He also highlighted the role of technology, noting, "We believe applied technology... provides constant leverage and constant reinvestment with the same expense base."

With its strong balance sheet, improving efficiency, and growth across all business segments, Bank of America appears well-positioned to continue delivering solid results in the coming quarters, despite potential challenges from interest rate changes and economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.