Tesla shares drop after third-quarter profit falls short of estimates

Introduction & Market Context

Barclays PLC (LSE:BARC) presented its third quarter 2025 results on October 22, showing a mixed performance with income growth of 9% year-over-year to £7.2 billion, while profit before tax declined 7% to £2.1 billion. Despite the profit dip, the bank upgraded its 2025 Return on Tangible Equity (RoTE) guidance to over 11%, previously around 11%, while maintaining its 2026 target of more than 12%.

Following the earnings presentation, Barclays’ stock showed minimal movement, with a modest increase of 0.02%. The stock has performed strongly over the past year, with a 40.9% return, and currently trades at a P/E ratio of 9.43, suggesting potential undervaluation according to market analysts.

Quarterly Performance Highlights

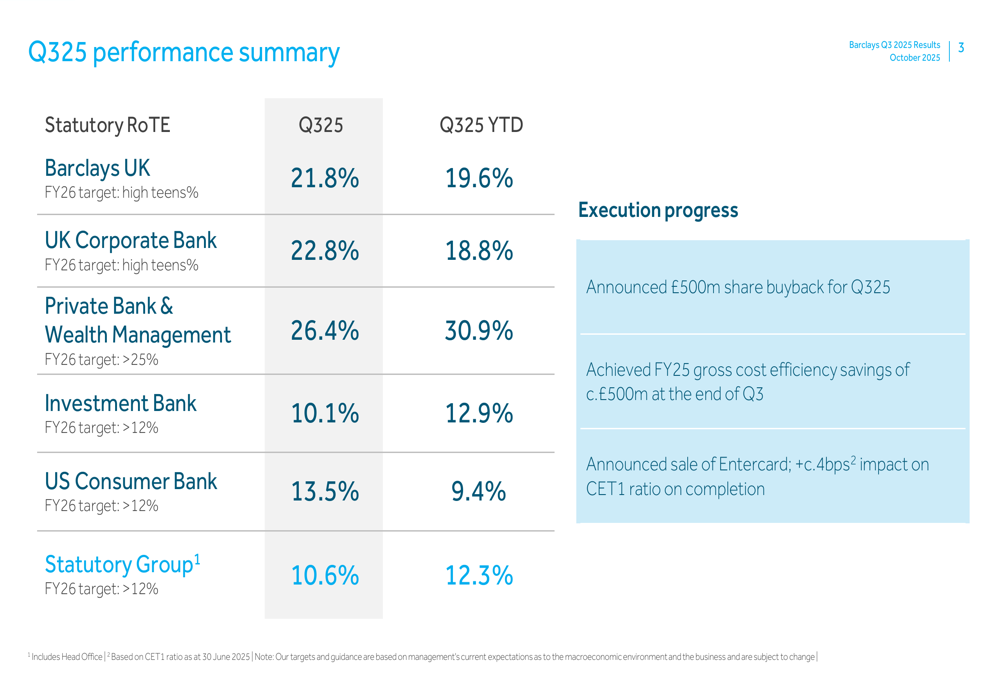

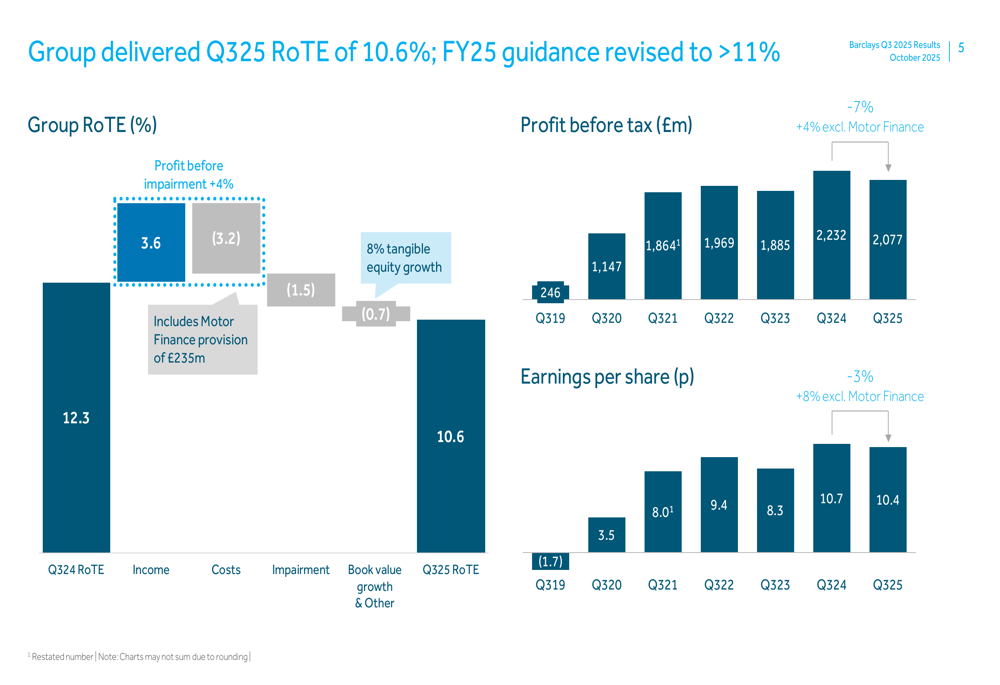

Barclays reported a statutory RoTE of 10.6% for Q3 2025, down from 12.3% in Q3 2024, though the year-to-date figure remains strong at 12.3%. The bank’s CET1 ratio improved to 14.1%, up from 13.8% in September 2024, reflecting a strengthened capital position.

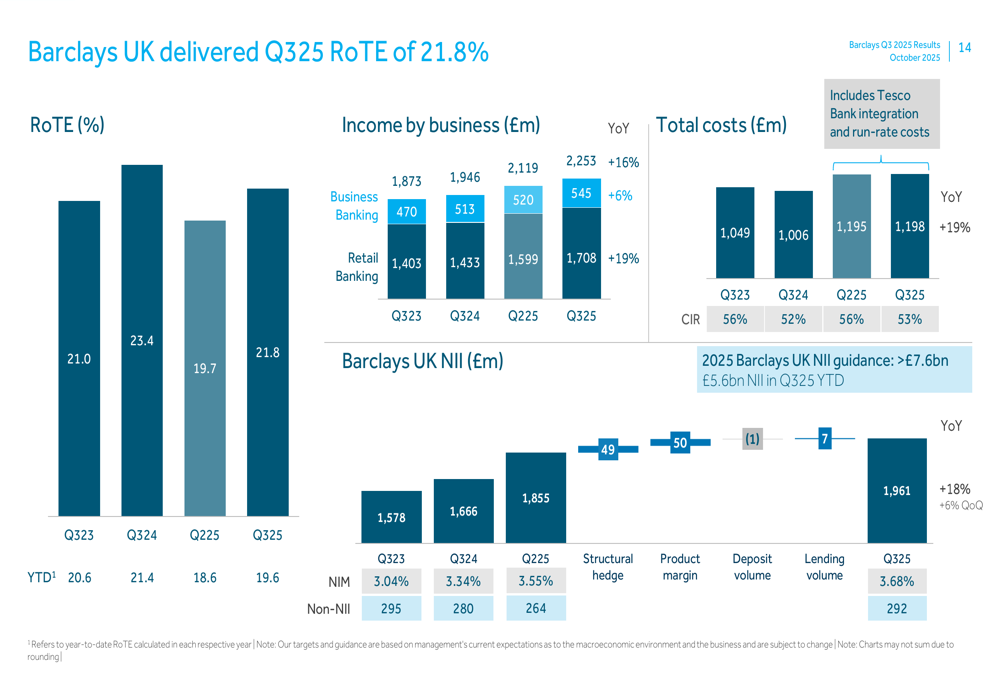

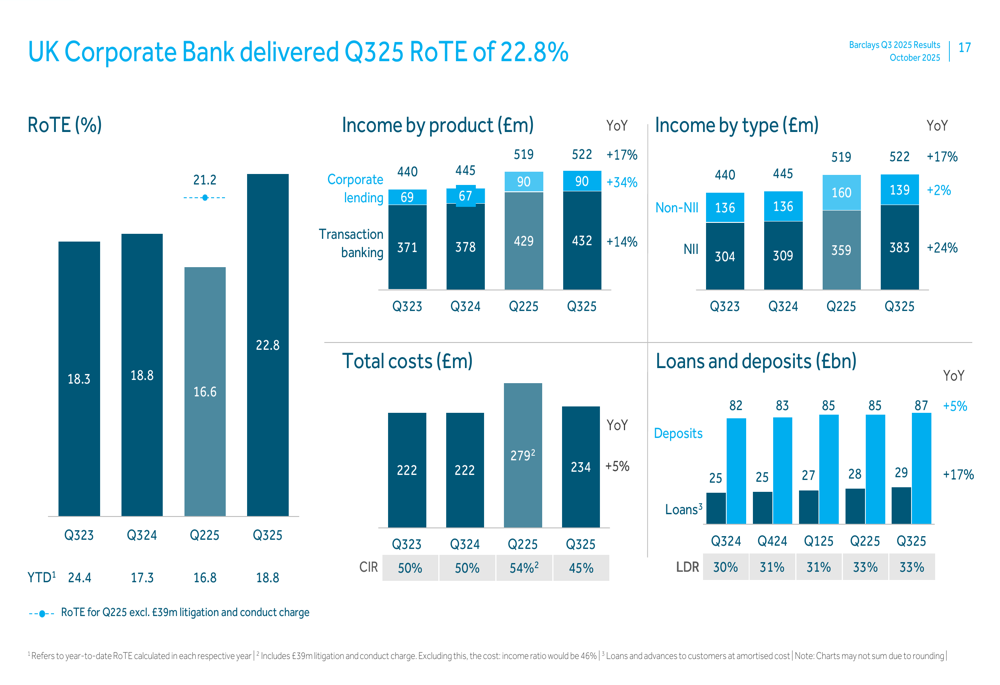

As shown in the following performance summary, Barclays’ UK-focused businesses delivered particularly strong results, with Barclays UK achieving a 21.8% RoTE and the UK Corporate Bank reaching 22.8%:

Earnings per share declined slightly to 10.4p from 10.7p in the same period last year, representing a 3% decrease. However, excluding the impact of Motor Finance provisions, EPS would have grown by 8%. The profit bridge below illustrates the factors affecting the quarterly performance:

Detailed Financial Analysis

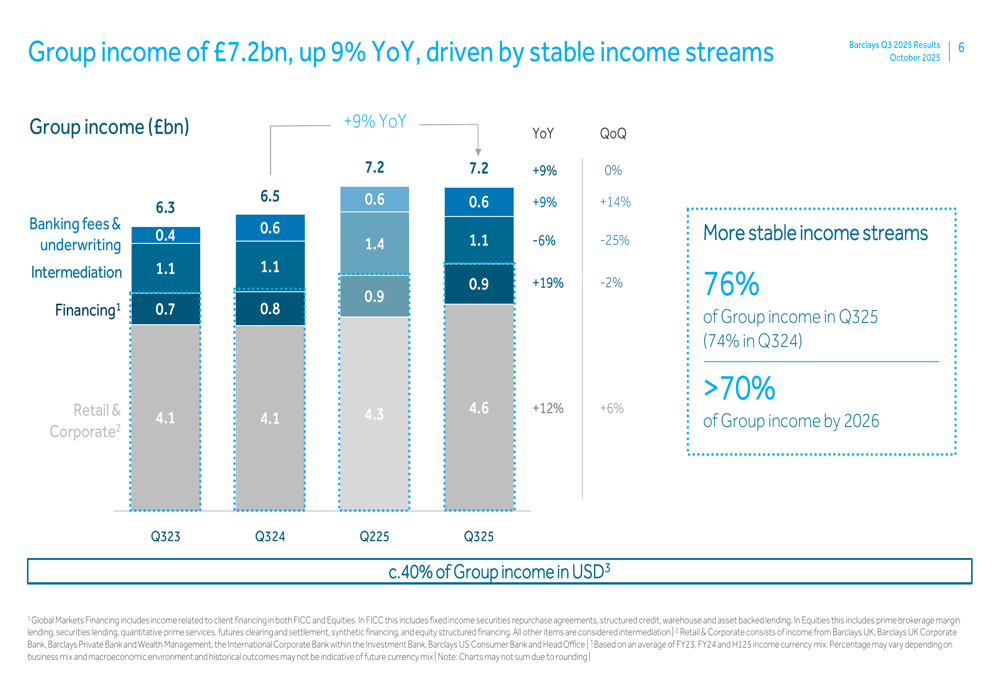

Group income increased by 9% year-over-year to £7.2 billion, with 76% coming from stable income streams, up from 74% in Q3 2024. The bank continues to benefit from its diversified business model, as shown in the income breakdown:

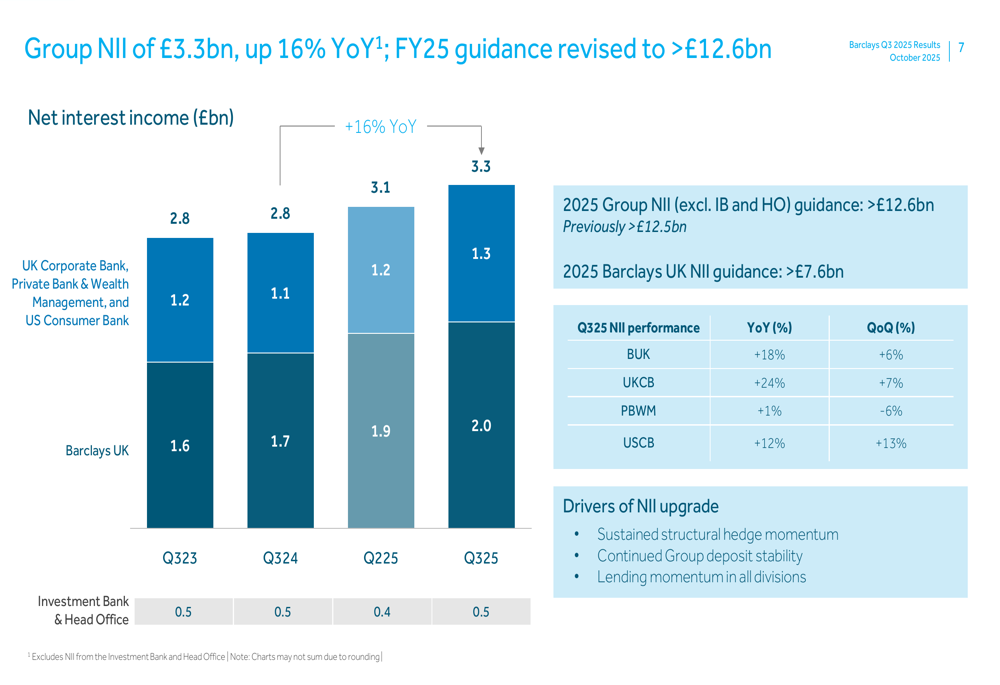

Net Interest Income (NII) showed particularly strong growth, increasing by 16% year-over-year to £3.3 billion. Based on this performance, Barclays upgraded its 2025 Group NII guidance (excluding Investment Bank and Head Office) to over £12.6 billion, previously over £12.5 billion. The NII growth was driven by strong performance across most divisions:

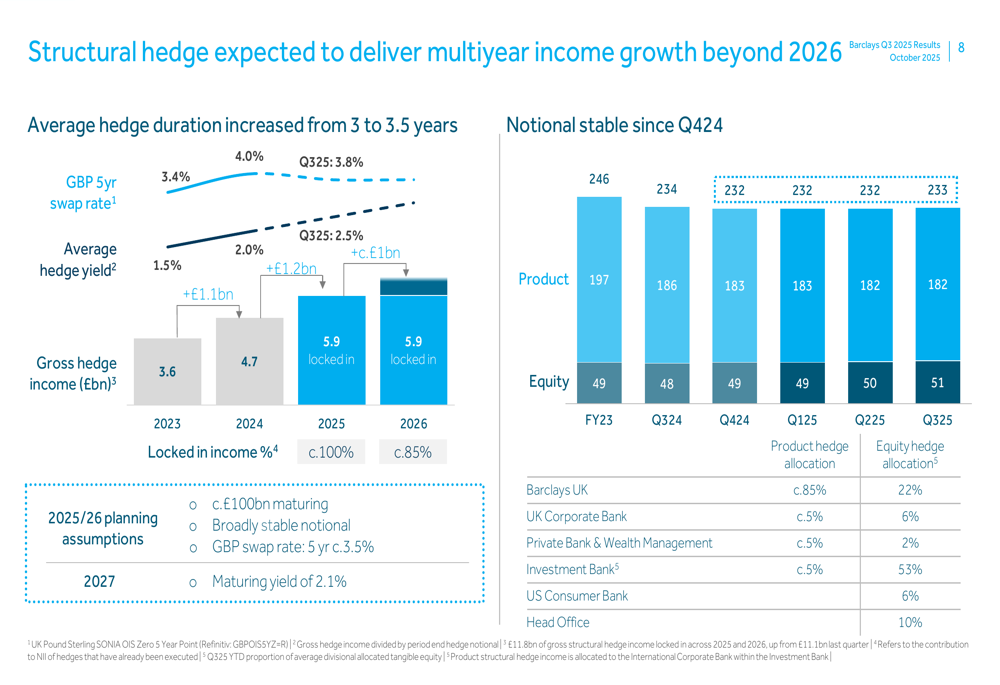

The structural hedge continues to be a significant contributor to income stability, with an average hedge yield of 1.5% and locked-in income for 2025 and 2026. The bank has increased its average hedge duration from 3 to 3.5 years, providing greater visibility on future income:

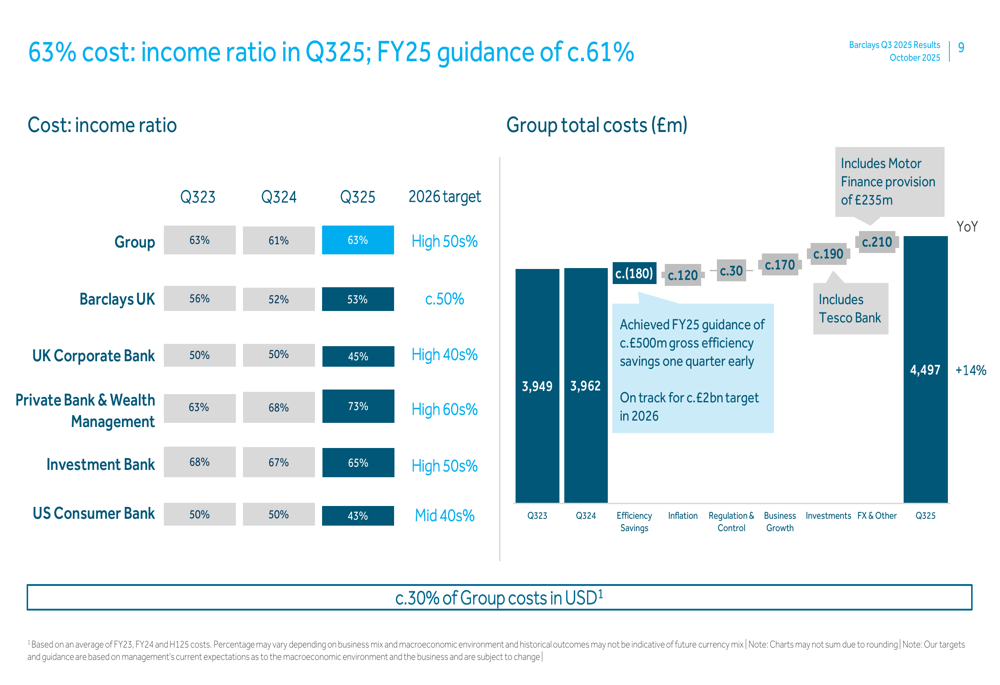

On the cost side, Barclays reported a cost-to-income ratio of 63% for Q3 2025, unchanged from Q3 2023 but up slightly from 61% in Q3 2024. The bank has already achieved its full-year 2025 gross cost efficiency savings target of approximately £500 million by the end of Q3:

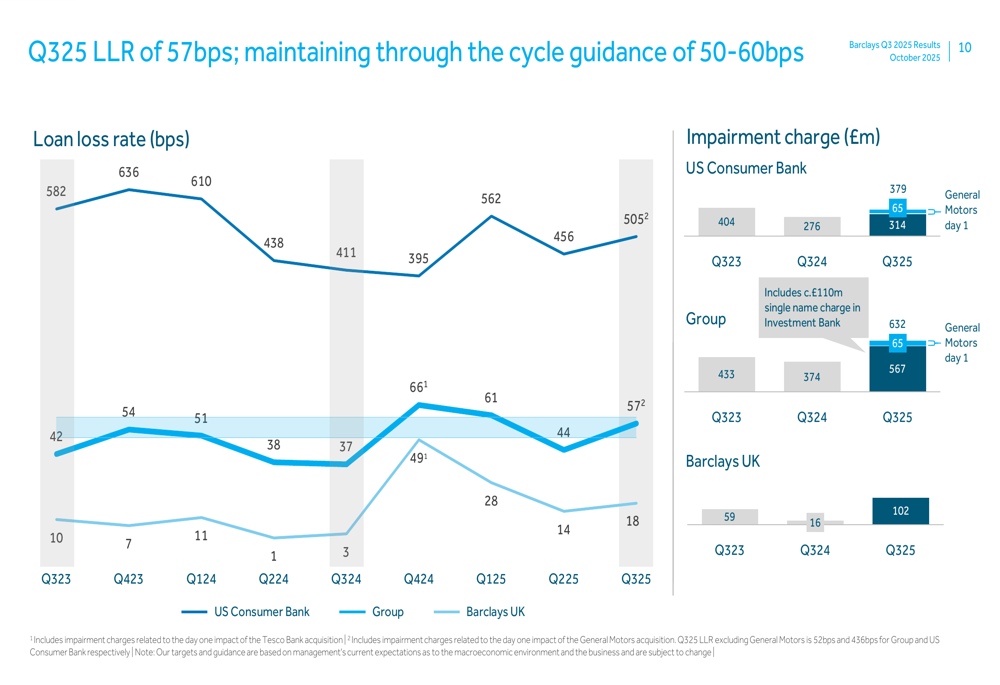

Credit quality remains within expectations, with a loan loss rate of 57bps for Q3 2025, within the bank’s through-the-cycle guidance of 50-60bps. The impairment charge increased to £632 million, partly due to day one impacts from the General Motors and Tesco Bank acquisitions:

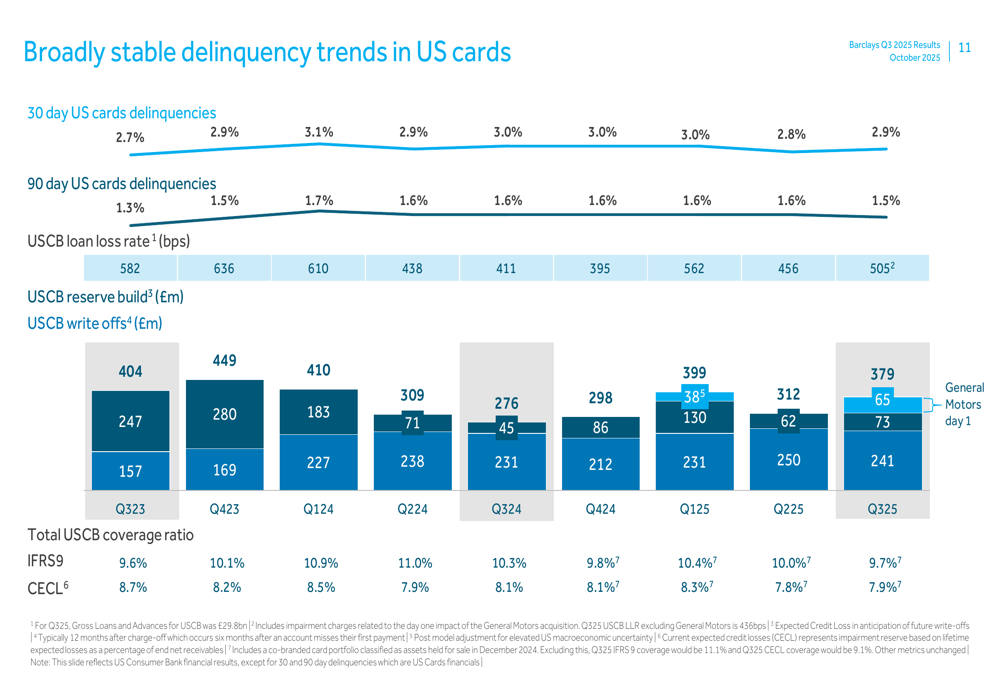

In the US Consumer Bank, credit card delinquencies have remained broadly stable, with 30-day delinquencies at 2.9% and 90-day delinquencies at 1.5%:

Business Unit Performance

Barclays UK delivered strong results with a 21.8% RoTE for Q3 2025, driven by an 18% year-over-year increase in Net Interest Income to £2.0 billion. The division’s income grew by 21% to £2.3 billion, while profit before tax increased by 11% to £1.0 billion:

The UK Corporate Bank also performed well, with a 22.8% RoTE for Q3 2025. The division saw strong growth in both deposits (up 5% year-over-year) and loans (up 17% year-over-year):

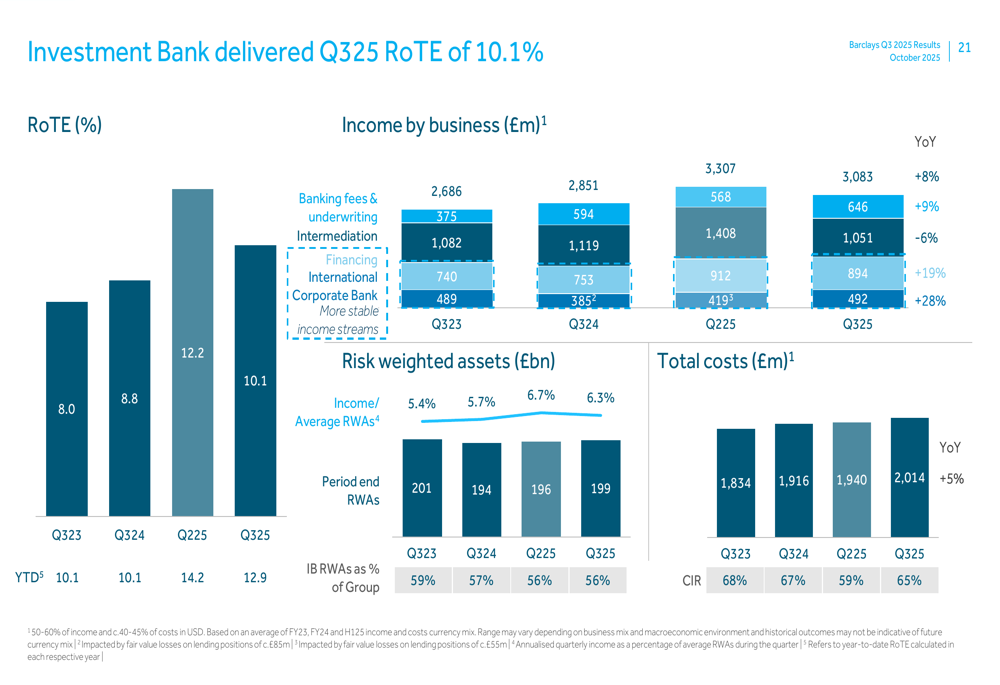

The Investment Bank delivered a more moderate performance with a 10.1% RoTE for Q3 2025, though its year-to-date RoTE remains strong at 12.9%. The division’s income breakdown shows varied performance across business lines:

Strategic Initiatives & Forward-Looking Statements

Barclays announced a £500 million share buyback for Q3 2025, continuing its capital return strategy. The bank has also made progress on its strategic initiatives, including the announced sale of Entercard, which is expected to have a positive impact of approximately 4 basis points on the CET1 ratio upon completion.

The bank has upgraded its 2025 RoTE guidance to over 11% (previously around 11%) while maintaining its 2026 target of more than 12%. Group NII guidance for 2025 (excluding Investment Bank and Head Office) has been raised to over £12.6 billion, reflecting the strong performance in interest-earning businesses.

During the earnings call, Group Chief Executive C.S. Venkatakrishnan noted, "We are seven quarters into our 12-quarter plan and remain on track to deliver our goals," emphasizing the support of a stronger outlook for stable income. Group Finance Director Anna Cross added that certain businesses should achieve "mid-teens" returns.

Looking ahead, Barclays plans to announce new targets for 2028 in February, aiming to further enhance returns across its businesses. The bank continues to focus on operational efficiency improvements and strategic growth in its UK and US businesses, while maintaining a balanced approach to risk and capital management.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.