Infosys, Wipro decline despite upbeat Q2 earnings; margin concerns weigh

Introduction & Market Context

Berry Global Group Inc (NYSE:BERY) presented its fourth quarter and fiscal year 2024 results on November 19, 2024, highlighting the company's transformation into a more focused packaging solutions provider following the completion of its Health, Hygiene, & Specialties (HHNF) spin-off transaction.

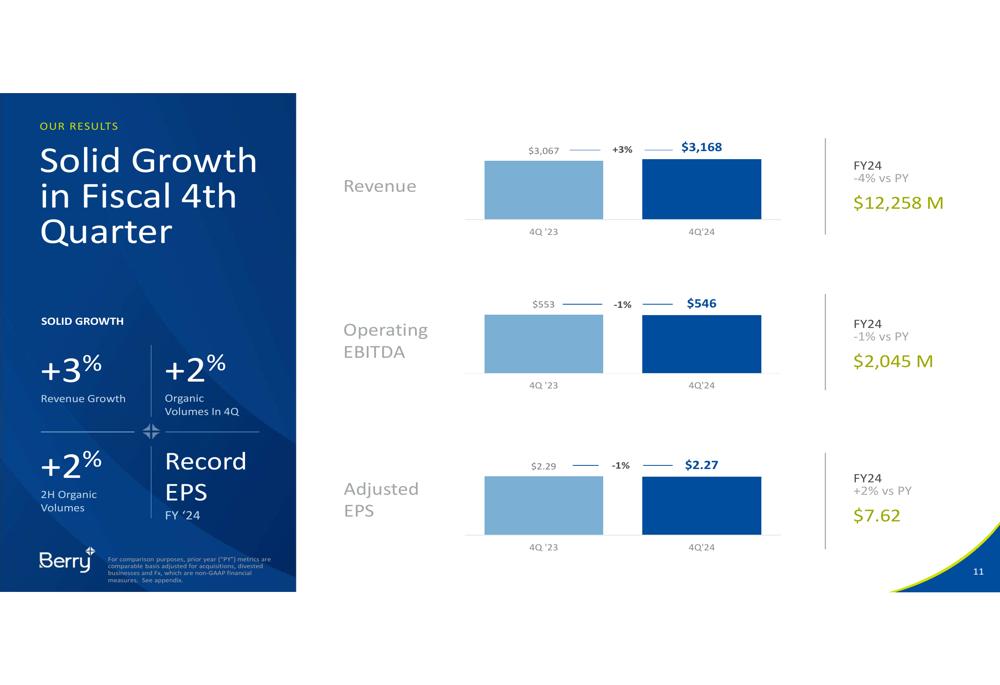

The company reported modest growth in the fourth quarter, with revenue increasing 3% year-over-year to $3.17 billion, slightly exceeding analyst expectations of $3.13 billion. Adjusted earnings per share came in at $2.27, beating consensus estimates of $2.06 despite being down 1% from the prior year.

Berry's presentation emphasized its evolution into what it calls "The New Berry" – a pure-play consumer packaging solutions leader with enhanced stability, consistent organic earnings growth, and higher return on invested capital.

As shown in the following slide, the company has positioned itself as a leader in fast-moving consumer products with a simplified portfolio and clear strategic focus:

Quarterly Performance Highlights

Berry Global achieved 2% organic volume growth in both the fourth quarter and second half of fiscal 2024, demonstrating resilience in challenging market conditions. While operating EBITDA decreased slightly by 1% to $546 million compared to the prior year, the company delivered record adjusted EPS of $7.62 for the full fiscal year, representing a 2% increase from fiscal 2023.

The quarterly performance data reveals varying results across Berry's business segments:

- Consumer Packaging International: Revenue increased 2% to $999 million with 1% organic volume growth

- Consumer Packaging North America: Revenue rose 5% to $840 million with 3% organic volume growth

- Flexibles: Revenue grew 2% to $687 million with 1% organic volume growth

- Health, Hygiene, & Specialties: Revenue increased 4% to $642 million with flat organic volume growth

The following chart illustrates the company's fourth quarter financial performance:

Segment performance was driven by a combination of volume improvements, price adjustments, and structural cost reductions. Consumer Packaging North America showed the strongest organic volume growth at 3%, while the Flexibles segment experienced margin pressure due to timing of raw material pass-throughs.

Strategic Initiatives

Berry Global outlined several strategic initiatives aimed at driving future growth and enhancing shareholder value. A key focus is the company's investment in sustainability-focused products, which continue to be strong growth drivers with significant long-term potential as more post-consumer recycled (PCR) supply becomes available.

The company is targeting strategic investments in four key areas as illustrated in the following slide:

Perhaps most notably, Berry announced a significant $250 million digital investment program over three fiscal years (FY25-27), split evenly between capital expenditures and operating expenses. This digital transformation initiative is expected to generate $100 million in annual EBITDA by fiscal 2028 through enhanced commercial capabilities, operational excellence, and lean transformation.

The digital investment will support organic growth through improved customer relationship management and price optimization, while also driving operational efficiencies through AI-enabled process automation, back office consolidation, factory automation, and streamlined global business systems.

Financial Outlook

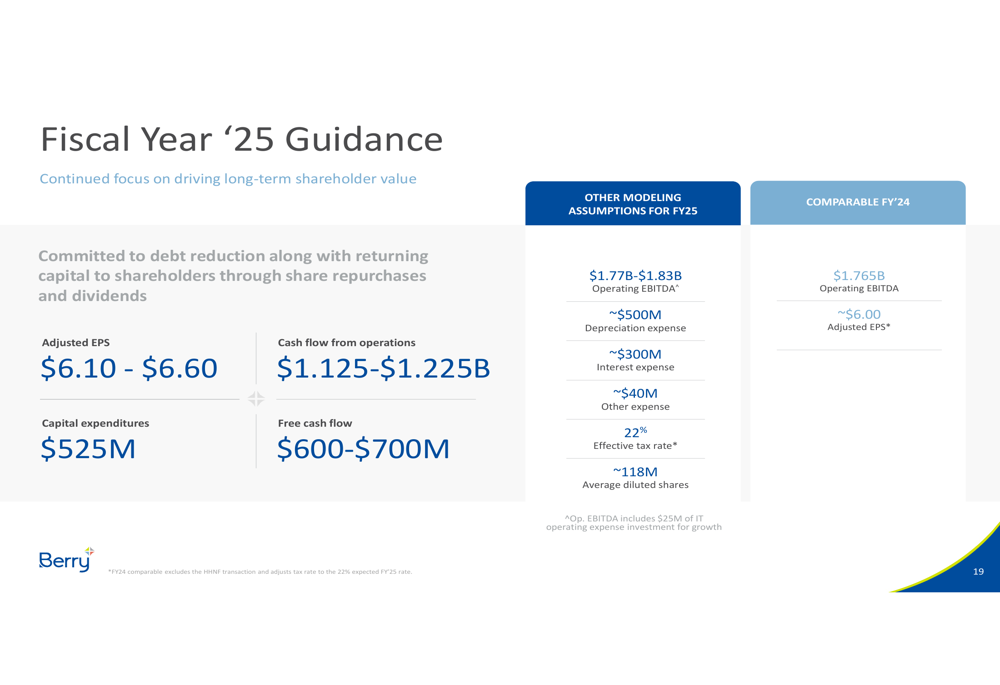

For fiscal year 2025, Berry Global provided guidance that includes:

- Adjusted EPS of $6.10-$6.60

- Cash flow from operations of $1.125-$1.225 billion

- Free cash flow of $600-$700 million

- Capital expenditures of $525 million

- Operating EBITDA between $1.77-$1.83 billion

While this guidance falls short of the analyst consensus estimate of $7.59 for adjusted EPS, investors appeared encouraged by the company's outlook for continued volume growth and strong free cash flow generation, as evidenced by the 4% stock gain noted in recent market activity.

The company's fiscal 2025 guidance is detailed in the following slide:

Berry also outlined its long-term financial targets, which include:

- Total (EPA:TTEF) shareholder return growth of 10-15%

- EBITDA growth of 4-6% (5-year average has been 6%)

- Adjusted EPS growth of 7-12% (5-year average has been 12%)

- Leverage ratio target of 2.5x-3.5x (ended FY24 at 3.5x with further reduction expected in FY25)

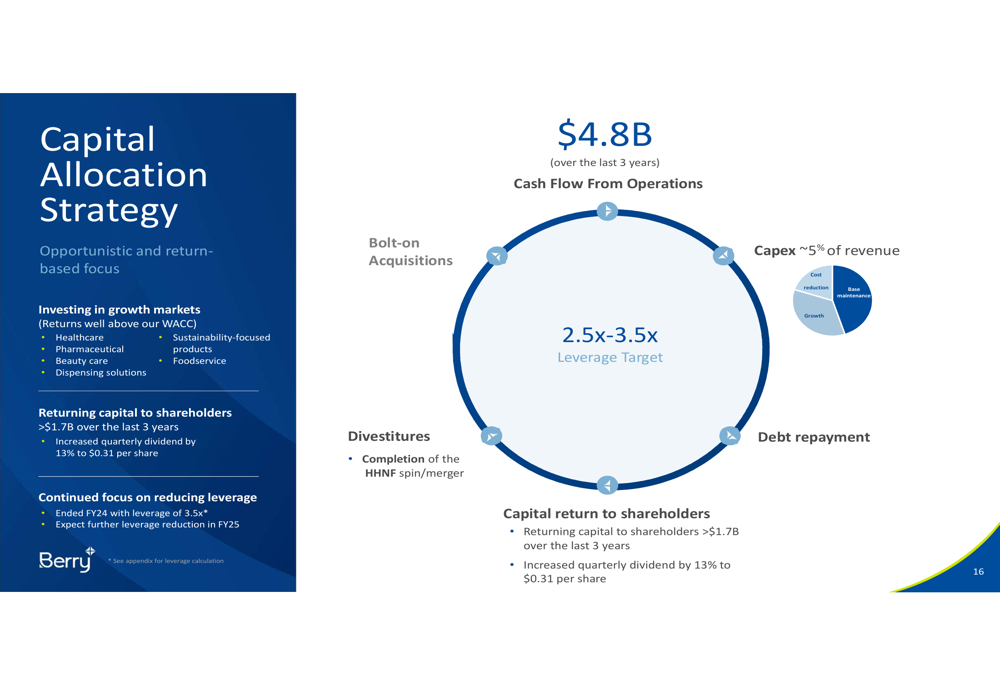

Capital Allocation Strategy

Berry Global emphasized its disciplined approach to capital allocation, focusing on opportunistic and return-based investments. The company has returned over $1.7 billion to shareholders over the past three years and recently increased its quarterly dividend by 13% to a new annualized rate of $1.24 per share.

The company's capital allocation priorities include:

- Investing in growth markets

- Bolt-on acquisitions

- Returning capital to shareholders

- Debt repayment to achieve target leverage of 2.5x-3.5x

As illustrated in the following slide, Berry's capital allocation strategy is designed to maximize shareholder value:

The company expects to return over $6.1 billion of value to shareholders over a six-year period through a combination of debt reduction and capital returns. Since the RPC acquisition, Berry has reduced its debt by approximately $4 billion while returning approximately $2 billion to shareholders.

Competitive Industry Position

Berry Global highlighted its strong competitive position, noting that it holds the #1 or #2 position in over 75% of the markets it serves. The company's focus on fast-moving consumer products provides stability and resilience, with 40% of revenue coming from food and beverage markets and 30% from home, health, and personal care segments.

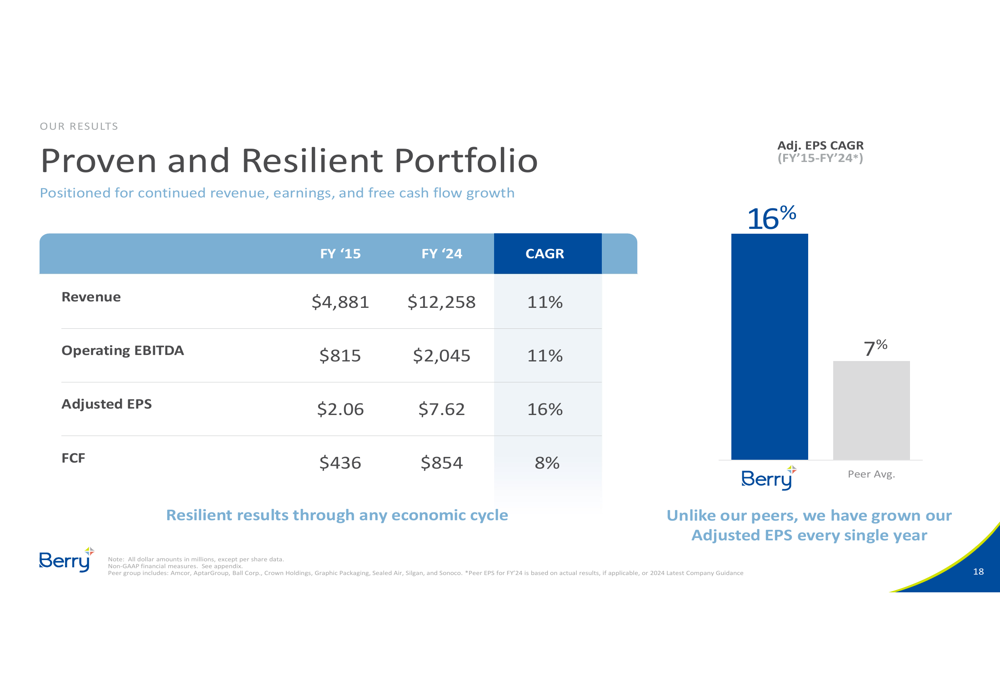

The presentation emphasized Berry's historical performance compared to peers, showing that the company has grown its adjusted EPS every year with a compound annual growth rate of 16%, significantly outpacing the peer average of 7%. Peers mentioned include Amcor, AptarGroup, Ball Corp (NYSE:BALL)., Crown Holdings, Graphic Packaging, Sealed Air (NYSE:SEE), Silgan, and Sonoco.

This consistent performance is illustrated in the following slide showing Berry's proven and resilient portfolio:

Notably, while the earnings presentation focused on organic growth and portfolio optimization, it did not mention the recently announced definitive merger agreement with Amcor Plc, which was referenced in a separate press release.

Berry's transformation into a pure-play consumer packaging solutions provider, combined with its strategic investments in sustainability and digital capabilities, positions the company to continue delivering value to shareholders despite challenging market conditions. The company's focus on deleveraging, returning capital to shareholders, and driving operational efficiencies provides a solid foundation for future growth.

Full Presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.