Micron to exit server chips business in China after 2023 ban- Reuters

Introduction & Market Context

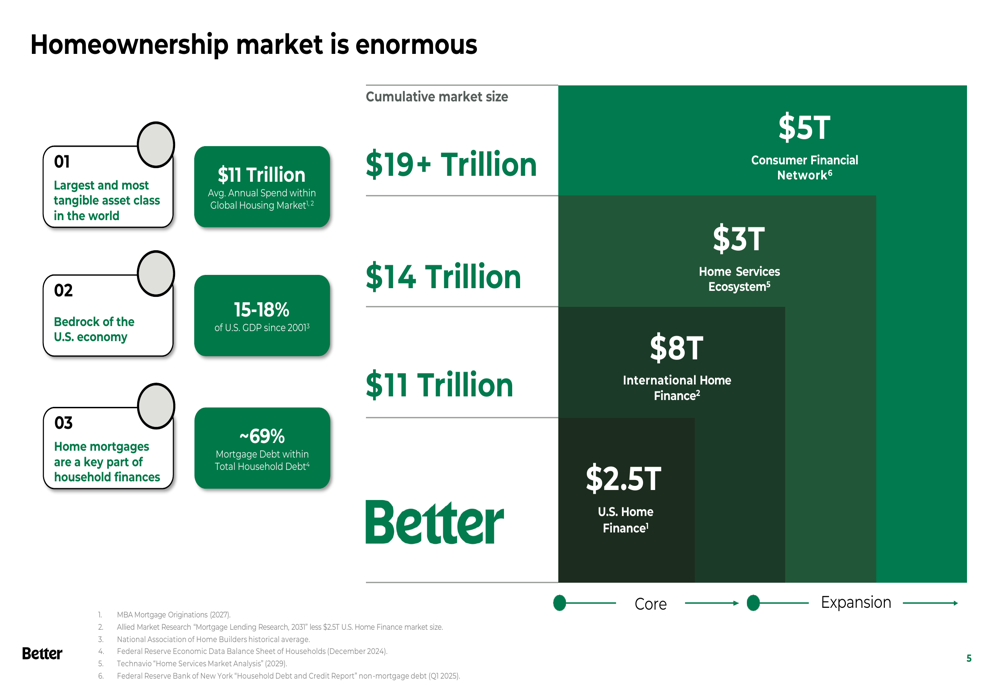

Better Home and Finance Holding Company (NASDAQ:BETR) unveiled its latest investor presentation in August 2025, positioning itself as a " Next (LON:NXT) Generation AI Mortgage Platform" in a market with enormous potential. The company estimates the U.S. home finance market at $2.5 trillion, with additional opportunities in international home finance ($8 trillion), home services ecosystem ($3 trillion), and consumer financial networks ($5 trillion).

The presentation highlights how the traditional mortgage process remains broken - expensive (with fees to up to 10 intermediaries accounting for ~10% of home price), slow (underwriting taking up to 45 days), and complicated (mortgage documents reaching 500 pages). Better aims to disrupt this status quo through technology.

As shown in the following market size visualization:

Strategic Initiatives

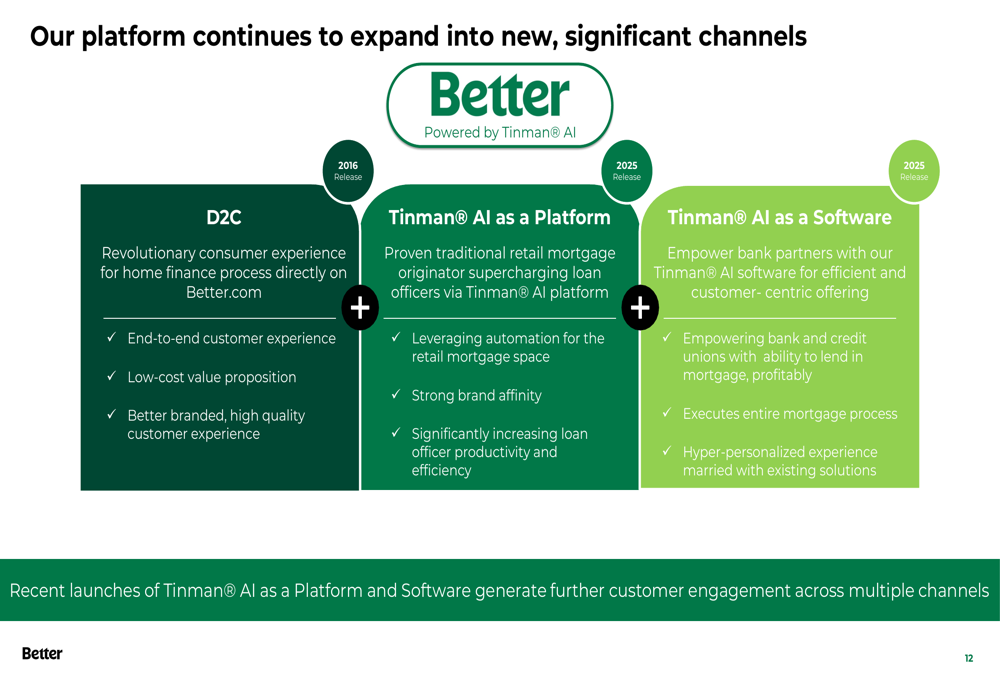

Better’s strategy centers on three core offerings: Direct-to-Consumer mortgage services, Tinman® AI as a Platform, and Tinman® AI as Software (ETR:SOWGn). The company claims its technology enables mortgages that cost 43% less than the industry average, while delivering superior customer experience with a Net Promoter Score of 64 and Trustpilot score of 4.1/5.

The platform expansion represents a significant evolution from Better’s initial direct-to-consumer focus in 2016 to its current B2B offerings that enable other financial institutions to leverage its technology:

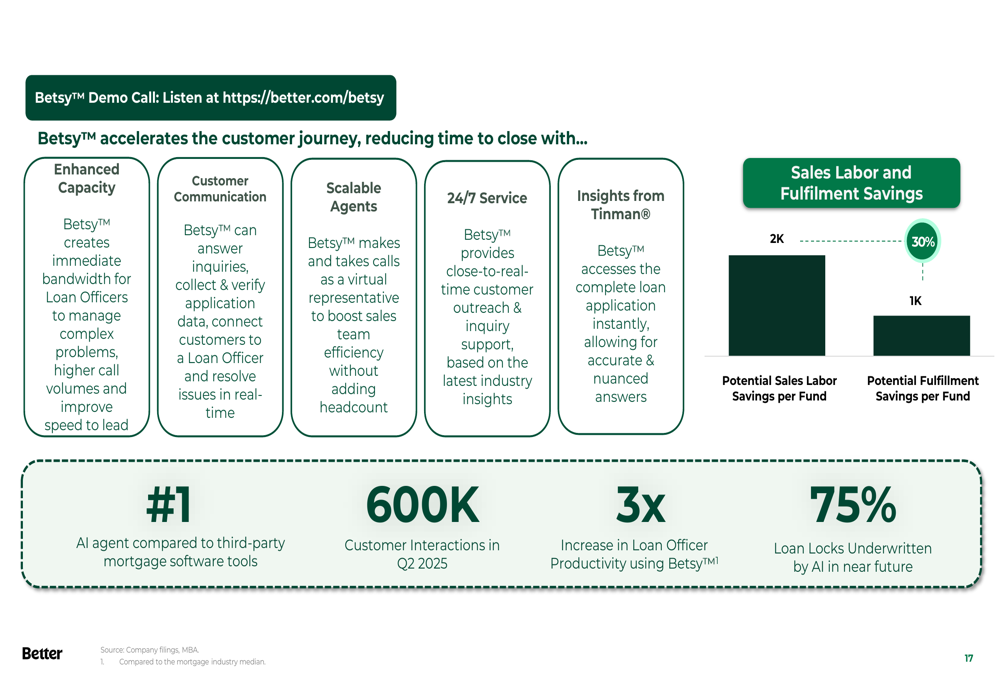

A key component of Better’s AI strategy is "Betsy," its virtual assistant programmed to handle mortgage inquiries, collect data, and resolve customer issues in real-time. According to the presentation, Betsy handled 600,000 customer interactions in Q2 2025 and has enabled a 3x increase in loan officer productivity. The company projects that 75% of loan locks will be underwritten by AI in the near future.

The impact of this AI assistant on operations is substantial:

Quarterly Performance Highlights

Better’s Q2 2025 performance showed improvement across several key metrics. The company funded 2,974 loans in Q2, up from 2,196 in Q1 2025. This aligns with the 31% year-over-year increase in funded loan volume to $868 million reported in the Q1 2025 earnings call.

The company’s NEO platform, which provides mortgage services to partner institutions, demonstrated particularly strong growth, with funded loan volume increasing from $163 million in Q1 2025 to $429 million in Q2 2025 - a 163% quarter-over-quarter increase. This growth trajectory supports management’s projection from the Q1 earnings call of "over 450 million dollars in Neo originations" representing 250% growth.

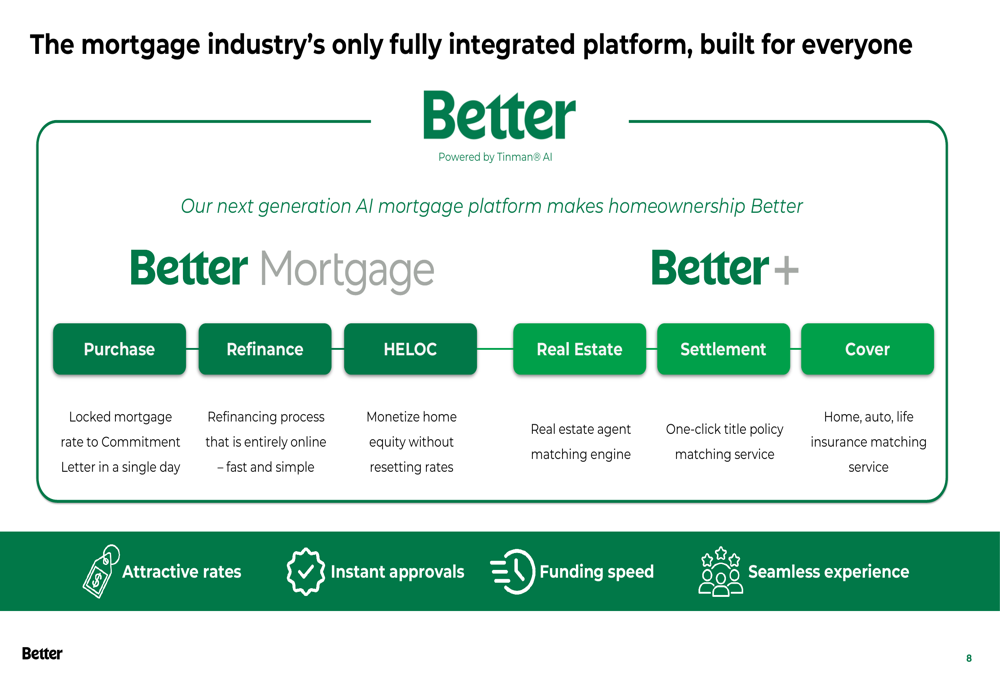

Better’s integrated platform approach encompasses both mortgage products (purchase, refinance, and HELOC) and complementary services through Better+, including real estate, settlement, and insurance solutions:

Detailed Financial Analysis

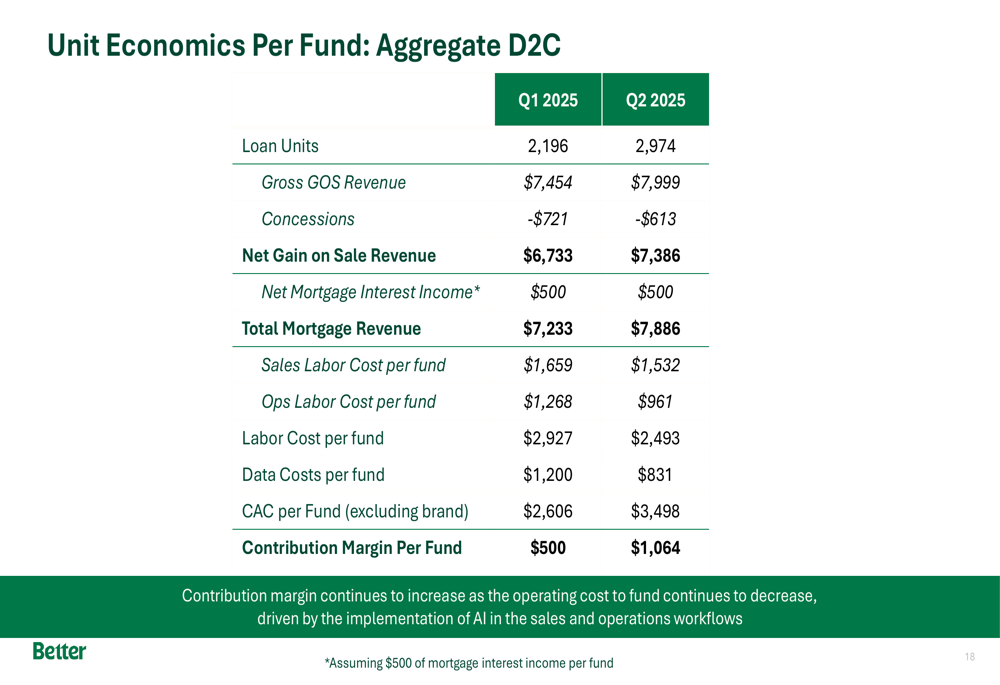

The presentation reveals improving unit economics, with contribution margin per funded loan more than doubling from $500 in Q1 2025 to $1,064 in Q2 2025. This improvement was driven by both revenue growth and cost reductions. Gross gain-on-sale revenue increased from $7,454 to $7,999 per loan, while concessions decreased from -$721 to -$613.

Notably, Better has made significant progress in reducing labor costs, with total labor cost per fund decreasing from $2,927 in Q1 to $2,493 in Q2 - a 15% reduction. Data costs per fund also declined substantially from $1,200 to $831, reflecting increased operational efficiency.

The detailed unit economics are illustrated in this comprehensive breakdown:

Despite these improvements, it’s important to note that Better continues to operate at a loss. The Q1 2025 earnings report showed an adjusted EBITDA loss of $40.4 million and a GAAP net loss of $50.6 million, highlighting the company’s ongoing challenges despite revenue growth of 46% year-over-year.

Forward-Looking Statements

Better outlined a path to breakeven by Q3 2026, focusing on four key areas: revenue diversification, increased efficiency, cost optimization, and strategic divestitures. This timeline suggests the company anticipates continued losses for at least another year, though the improving unit economics indicate progress toward profitability.

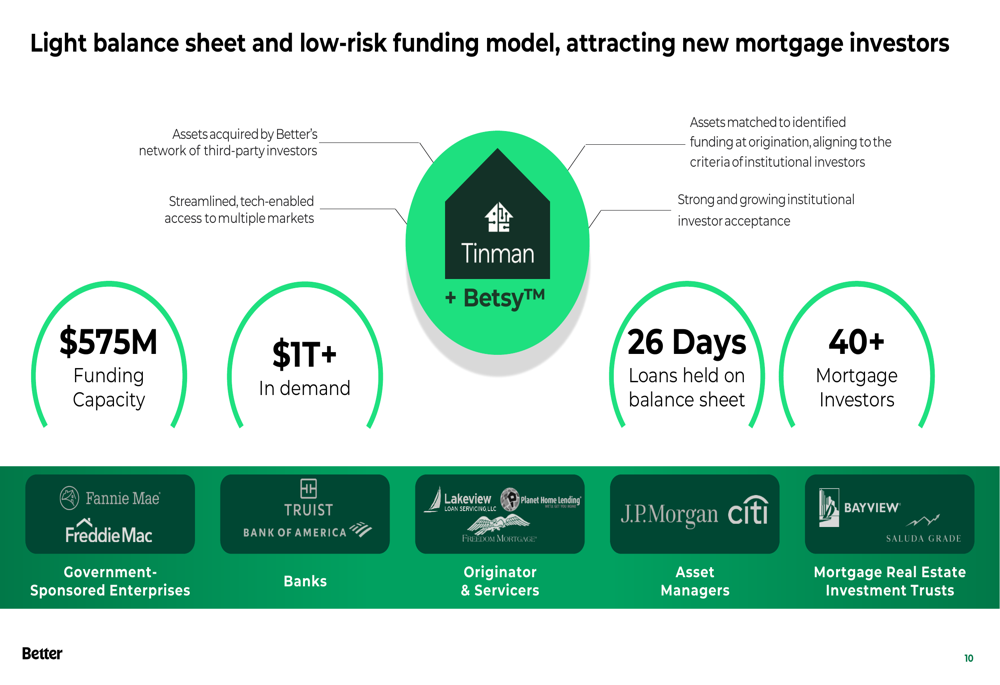

The company’s funding model relies on a network of third-party investors rather than holding loans on its balance sheet long-term. Better reports having $575 million in funding capacity, with loans held on its balance sheet for an average of 26 days before being acquired by its network of over 40 mortgage investors, including major institutions like Fannie Mae (OTC:FNMA), Freddie Mac (OTC:FMCC), Truist, Bank of America, and J.P. Morgan.

Better’s customer-facing experience emphasizes speed and simplicity, with rate quotes in 3 seconds, pre-approval in 3 minutes, and loan closing in 3 weeks - significantly faster than industry averages. The company claims its home purchase process is 12 days faster than traditional lenders and saves customers approximately $20,000 on average.

The company’s average customer has a loan balance of $299,000, is 44 years old, has a FICO score of 747, and a household income of $194,000 - representing a relatively affluent, prime borrower demographic.

As Better continues its transformation into an AI-powered mortgage platform, investors will be watching closely to see if the improving unit economics and growing loan volumes translate into the projected path to profitability by Q3 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.