Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Swedish packaging and paper manufacturer Billerud (STO:BILL) presented its Q2 2025 interim report on July 18, revealing a stark contrast between its regional operations. The company reported solid performance in North America while facing significant headwinds in Europe, where weakening demand continues to pressure results.

The presentation, delivered by President & CEO Ivar Vatne and CFO Andrei Krés, highlighted a challenging quarter overall with net sales declining 5% year-over-year to 10,244 million SEK. This represents a significant reversal from the company’s strong Q1 2025 performance, when Billerud reported 7% sales growth and 19% EBITDA improvement.

The stock closed at 96.65 SEK on July 17, down 1.18% ahead of the earnings presentation, and has traded between 90.5 SEK and 122.2 SEK over the past 52 weeks.

Quarterly Performance Highlights

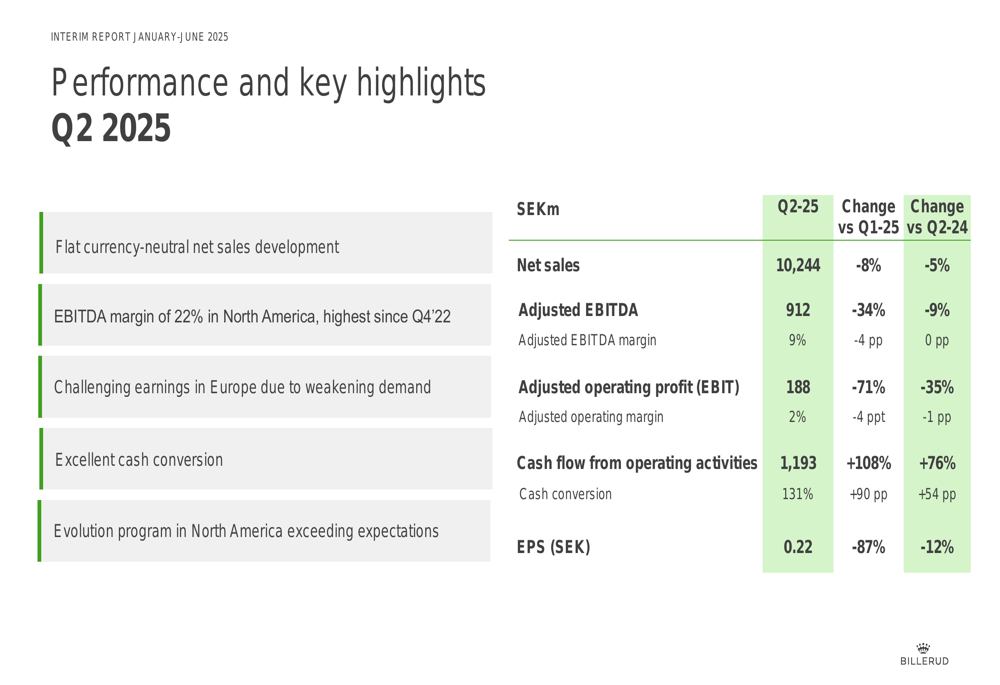

Billerud’s Q2 2025 results showed mixed performance across key metrics. While overall figures declined compared to both the previous quarter and the same period last year, cash flow demonstrated remarkable strength.

As shown in the following financial summary:

Net sales decreased to 10,244 million SEK, down 8% quarter-over-quarter and 5% year-over-year. Adjusted EBITDA fell to 912 million SEK, representing a 34% decline from Q1 2025 and a 9% drop compared to Q2 2024. The EBITDA margin remained flat year-over-year at 9% but decreased 4 percentage points sequentially.

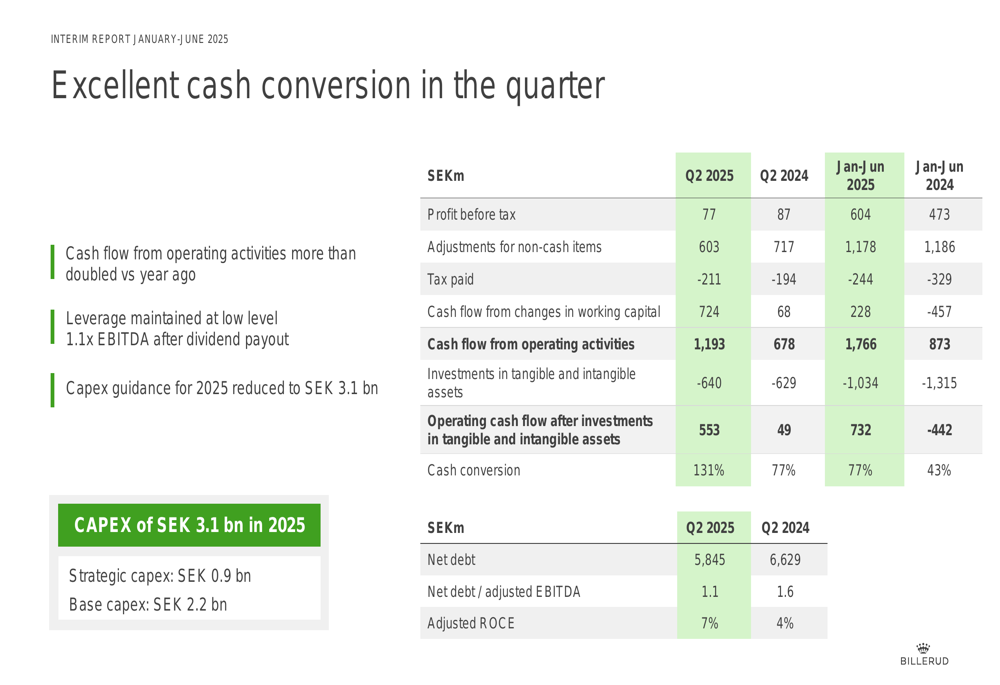

Particularly noteworthy was the company’s cash flow from operating activities, which surged to 1,193 million SEK, up 108% from the previous quarter and 76% year-over-year. This translated to an impressive cash conversion rate of 131%, significantly exceeding the company’s target of 80%.

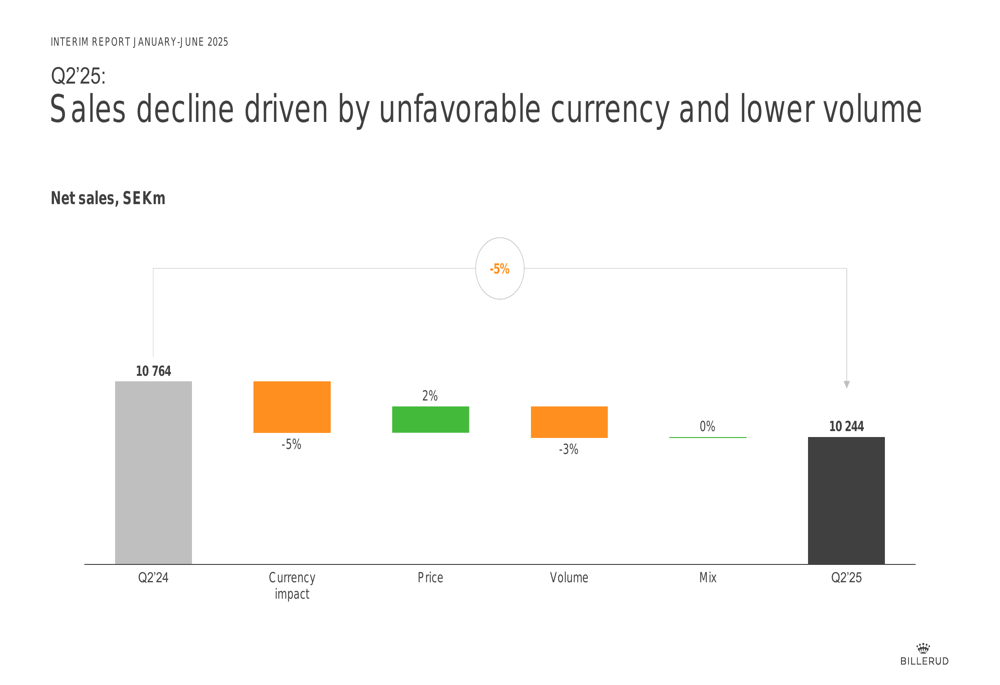

The sales decline was primarily attributed to unfavorable currency effects and lower volumes, as illustrated in this breakdown:

Currency impacts reduced sales by 5%, while volume decreased by 3%. These negative factors were partially offset by a 2% positive price impact, resulting in the overall 5% year-over-year sales decline.

Regional Performance Analysis

The stark contrast between Billerud’s regional operations was a central theme of the presentation, with North America delivering exceptional results while Europe struggled with weakening demand.

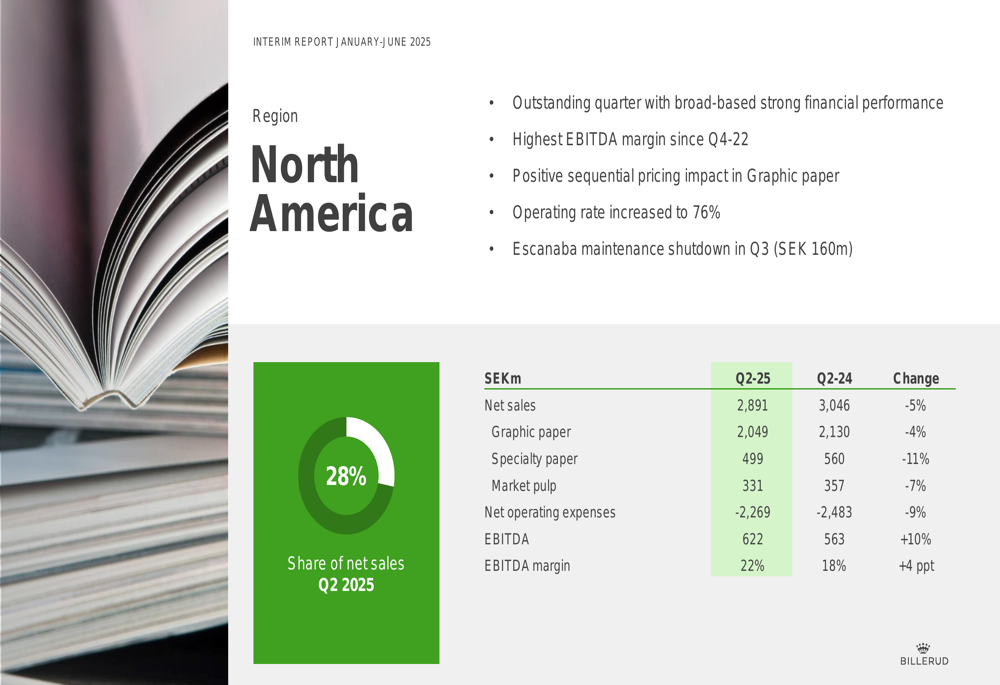

In North America, which accounts for 28% of net sales, the company reported its highest EBITDA margin since Q4 2022 at 22%, representing a 4 percentage point improvement year-over-year:

Despite a 5% decline in North American net sales to 2,891 million SEK, EBITDA increased by 10% compared to Q2 2024. The region benefited from positive sequential pricing impact in graphic paper and an improved operating rate of 76%.

Conversely, Europe, which represents 63% of net sales, faced significant challenges:

European operations reported an 8% decline in net sales to 6,481 million SEK, with EBITDA plummeting 47% year-over-year. The EBITDA margin contracted to just 5%, down 4 percentage points from Q2 2024. Management cited macro uncertainty and weaker sales volumes as primary factors, with planned maintenance shutdowns expected to further impact Q3 results by approximately 280 million SEK.

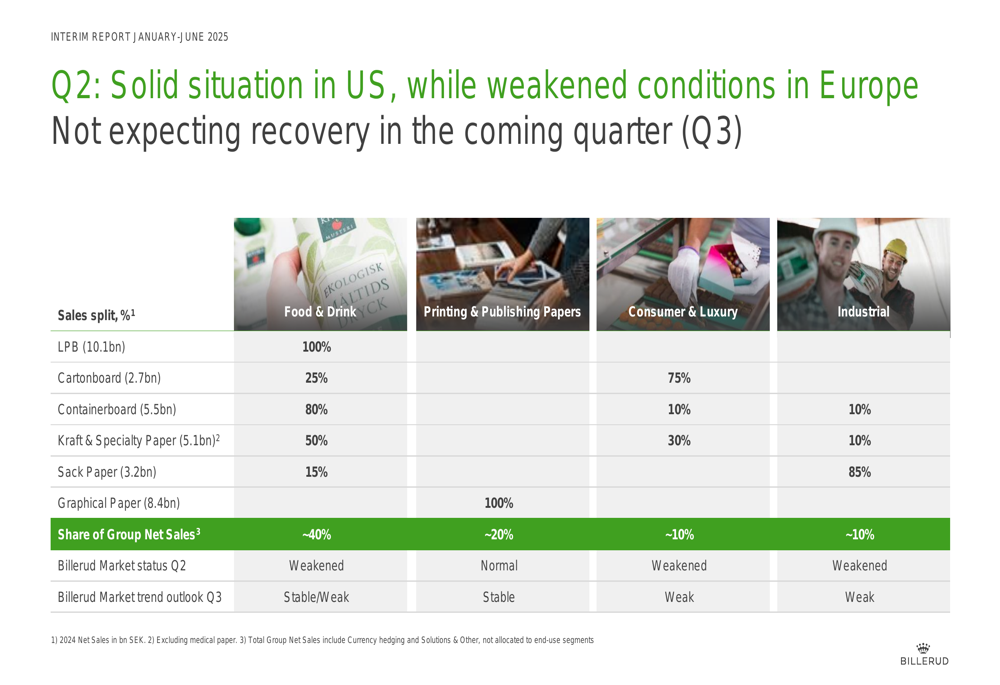

The company’s market outlook varies significantly by segment, with particularly weak conditions in consumer, luxury, and industrial segments:

Cash Flow and Capital Allocation

A standout positive in Billerud’s Q2 results was its exceptional cash flow performance, which more than doubled year-over-year:

The company maintained a low leverage ratio of 1.1x EBITDA even after dividend payout. In a notable development, Billerud reduced its capital expenditure guidance for 2025 to 3.1 billion SEK, with 0.9 billion allocated to strategic investments and 2.2 billion to base maintenance capex.

This capital discipline aligns with management’s stated focus on protecting cash flow, with a target cash conversion rate exceeding 80%. The actual Q2 conversion rate of 131% significantly outperformed this target, representing a 54 percentage point improvement from Q2 2024.

Strategic Initiatives and Outlook

Despite market challenges, Billerud reported encouraging progress on its strategic Evolution program in North America:

The program has already sold 1,000 tons of bleached liner (Tribute®) and low-grammage cartonboard (Voyager®) to customers, with approximately 50 ongoing product trials exceeding commercial expectations. Management confirmed the investment program is progressing as planned.

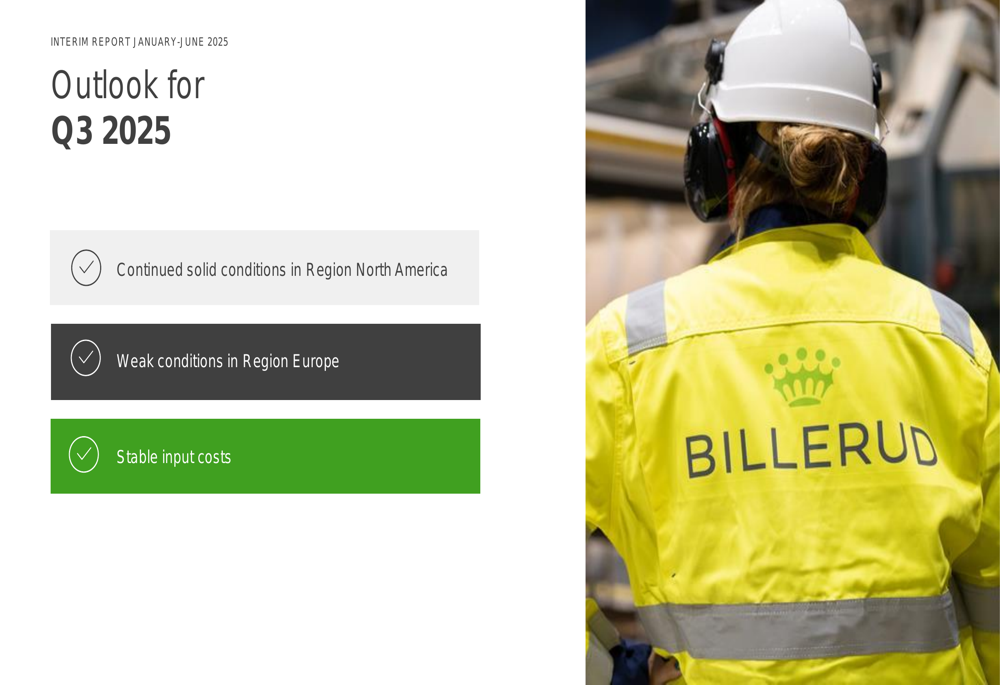

Looking ahead to Q3 2025, Billerud expects continued divergence in regional performance:

The company anticipates solid conditions to persist in North America while European markets remain weak. Input costs are expected to remain stable. Management highlighted four key focus areas: challenging the fixed cost base, protecting cash flow, driving profitable mix, and ensuring mill efficiency and supply chain reliability.

This cautious outlook represents a continuation of the challenging conditions that emerged in Q2, contrasting with the more optimistic tone following Q1 results. With no recovery expected in European markets during Q3, Billerud’s ability to maintain strong North American performance and exceptional cash conversion will be crucial to navigating the current environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.