United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Bio-Rad Laboratories Inc. (NYSE:BIO) released its second quarter 2025 financial results on July 31, 2025, showing modest revenue growth despite challenging market conditions. The company’s stock closed at $303.71 on the day of the presentation, up 0.44% in regular trading, though it experienced a slight decline of 0.39% in aftermarket trading.

The quarter was marked by the completion of the Stilla Technologies acquisition on June 30, 2025, a strategic move that strengthens Bio-Rad’s position in the life sciences market. The company continues to navigate varied market conditions across regions, with particular softness noted in China while showing positive trends in Korea and Japan, according to the earnings call.

Quarterly Performance Highlights

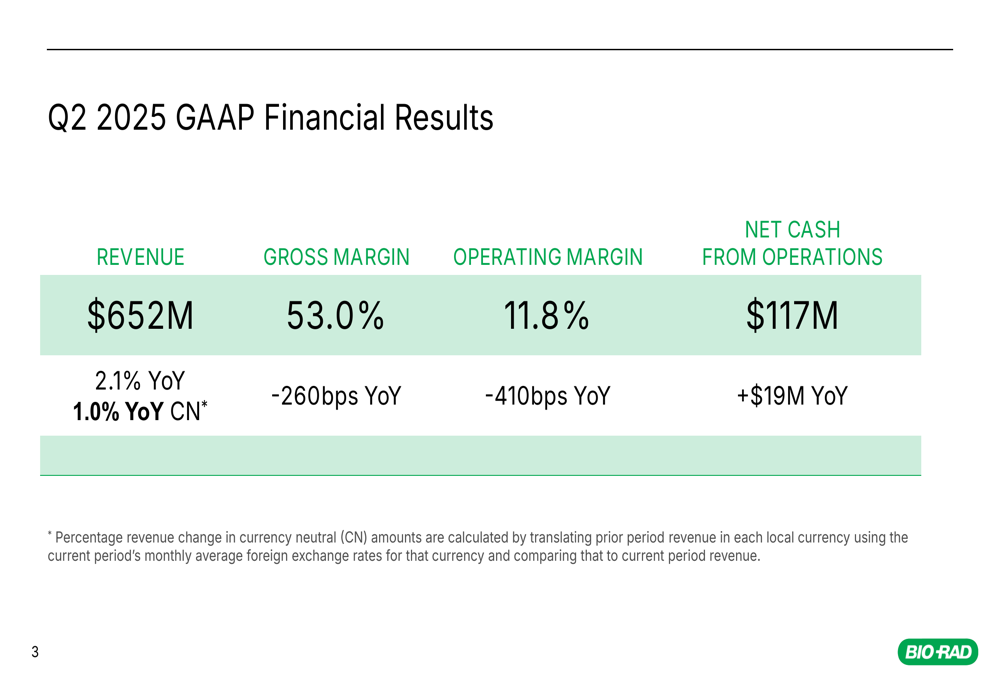

Bio-Rad reported Q2 2025 revenue of $652 million, representing a 2.1% year-over-year increase (1.0% on a currency-neutral basis). Despite this growth, the company experienced margin pressure during the quarter.

As shown in the following GAAP financial results:

The company’s GAAP gross margin declined 260 basis points year-over-year to 53.0%, while operating margin fell 410 basis points to 11.8%. However, net cash from operations improved by $19 million year-over-year to reach $117 million.

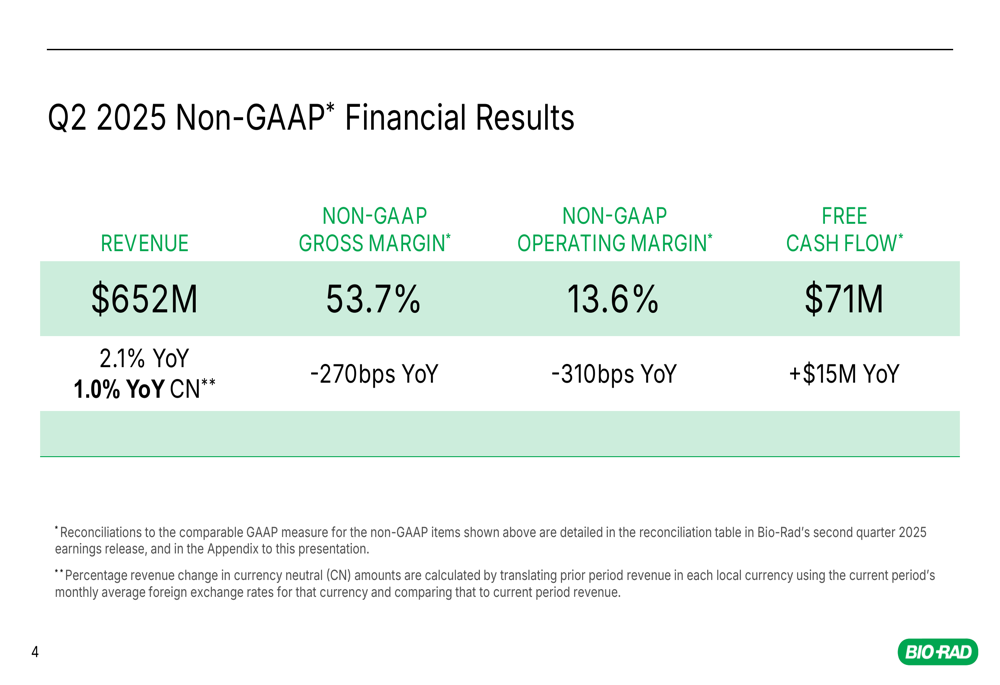

On a non-GAAP basis, the results showed similar trends with some improvements:

Non-GAAP gross margin came in at 53.7%, down 270 basis points year-over-year, while non-GAAP operating margin was 13.6%, representing a 310 basis point decline. Free cash flow reached $71 million, a $15 million improvement compared to the same period last year.

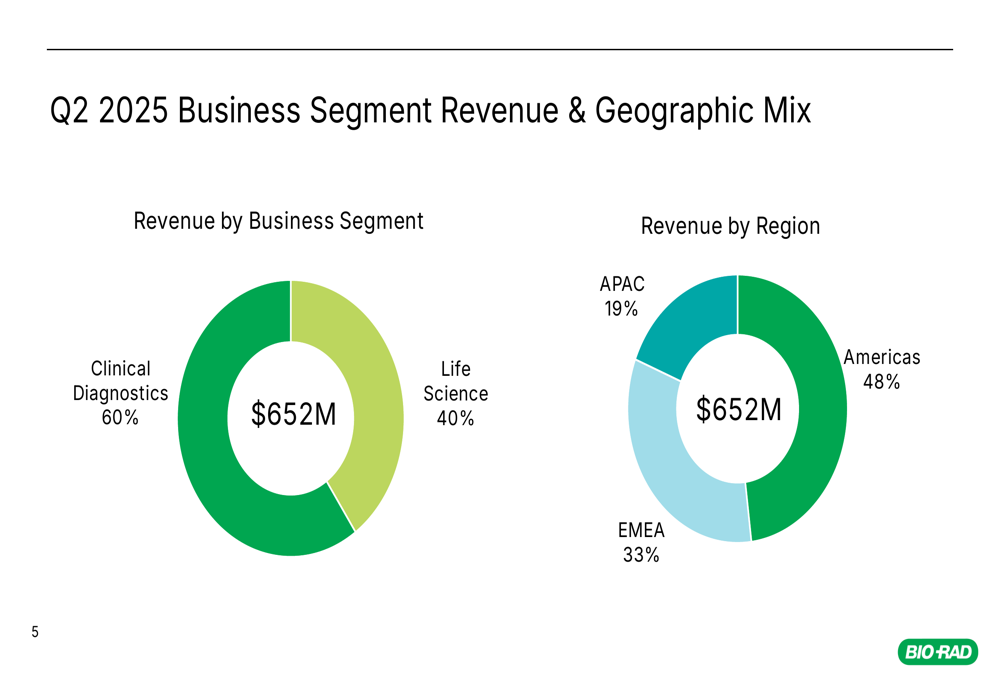

Bio-Rad’s revenue was well-balanced across business segments and geographic regions, as illustrated in this breakdown:

Segment Performance Analysis

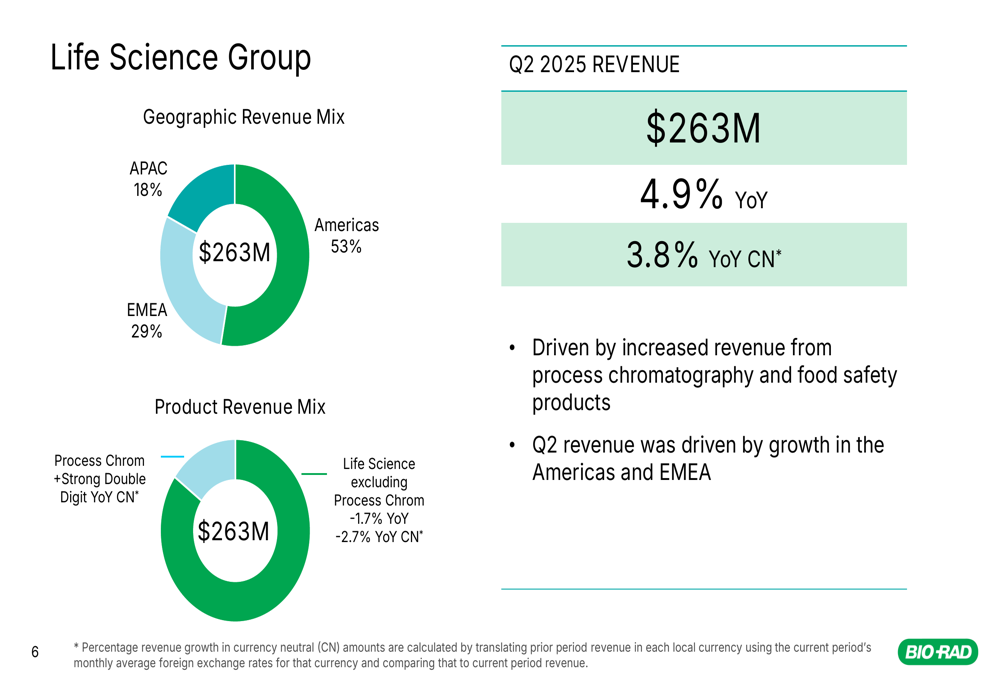

The Life Science segment emerged as the growth driver for Bio-Rad during Q2 2025, with revenue increasing by 4.9% year-over-year (3.8% currency-neutral) to $263 million. This growth was primarily driven by strong performance in process chromatography products, which showed double-digit currency-neutral growth.

The segment’s performance across regions and product lines is detailed below:

The Americas represented the largest market for Life Science products at 53% of segment revenue, followed by EMEA at 29% and APAC at 18%. Growth was strongest in the Americas and EMEA regions, helping offset challenges elsewhere.

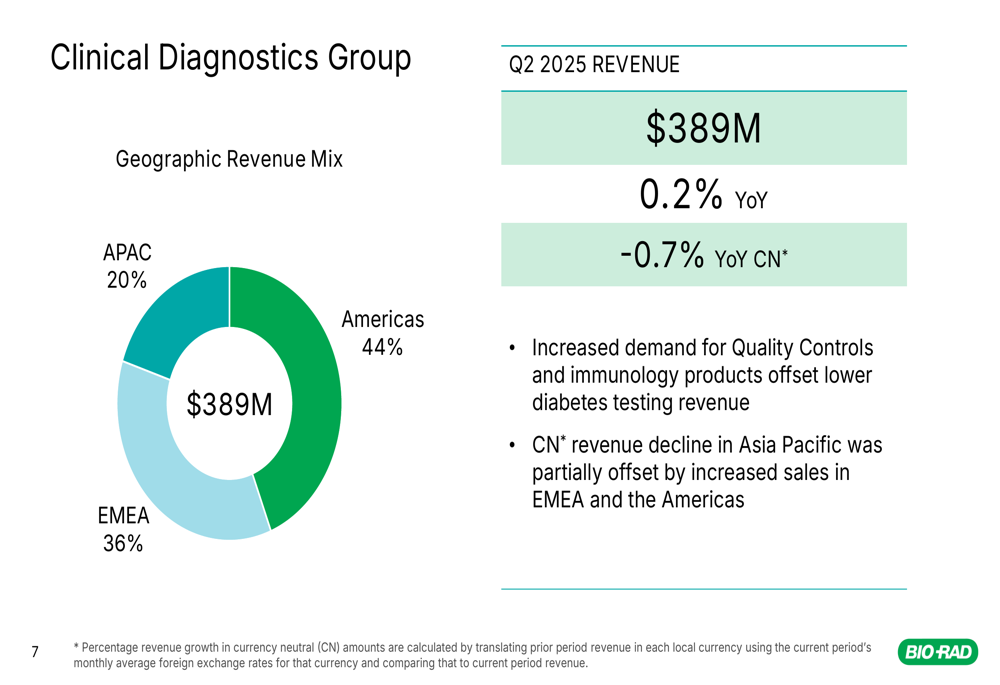

Meanwhile, the Clinical Diagnostics segment, which accounts for 60% of Bio-Rad’s total revenue, reported relatively flat performance with revenue of $389 million, representing just 0.2% growth year-over-year and a 0.7% decline on a currency-neutral basis:

Within Clinical Diagnostics, increased demand for Quality Controls and immunology products was offset by lower diabetes testing revenue. Geographically, the segment saw revenue declines in Asia Pacific, partially offset by increased sales in EMEA and the Americas.

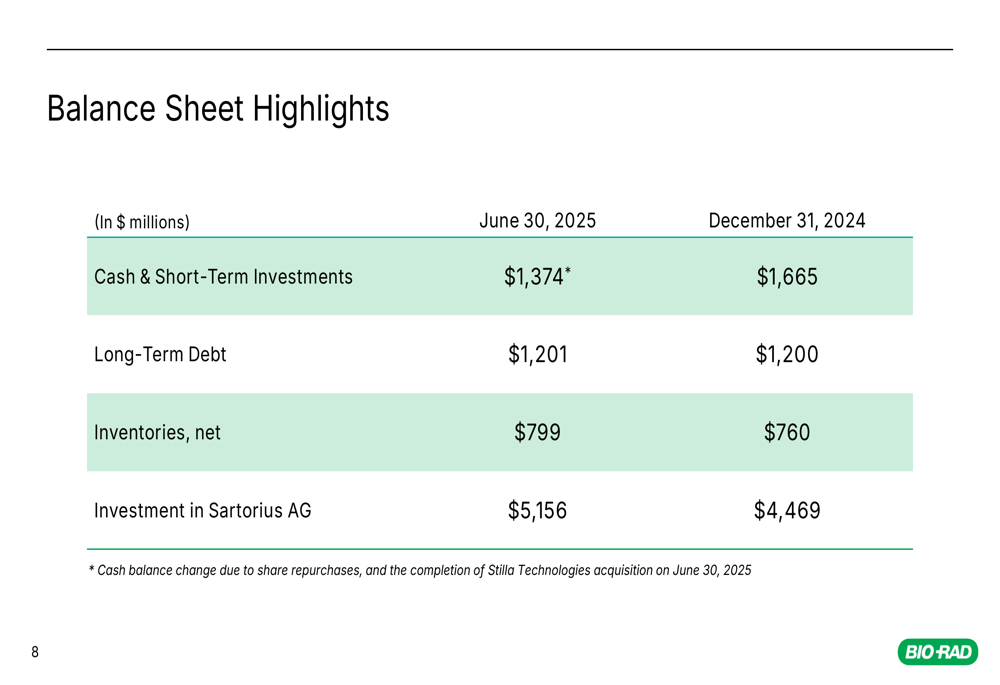

Balance Sheet and Cash Flow

Bio-Rad’s balance sheet showed some notable changes during the first half of 2025:

Cash and short-term investments decreased to $1,374 million as of June 30, 2025, compared to $1,665 million at the end of 2024. This reduction was primarily due to share repurchases and the completion of the Stilla Technologies acquisition.

The company’s investment in Sartorius AG increased significantly to $5,156 million, up from $4,469 million at the end of 2024, representing a substantial appreciation in this strategic holding. Long-term debt remained relatively stable at $1,201 million.

Inventory levels increased slightly to $799 million, up from $760 million at the end of 2024, indicating potential preparation for future growth or reflecting slower inventory turnover.

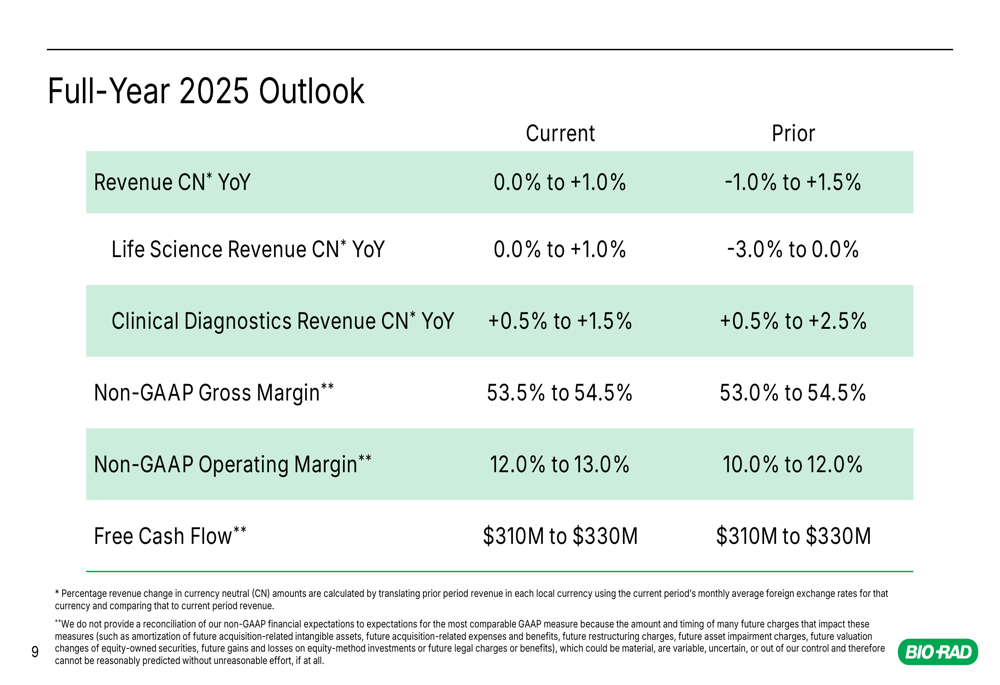

Revised 2025 Outlook

Based on first-half performance, Bio-Rad has updated its full-year 2025 guidance:

The company narrowed its currency-neutral revenue growth expectations to 0.0% to 1.0%, compared to the previous range of -1.0% to 1.5%. Life Science revenue outlook improved significantly, now projected at 0.0% to 1.0% growth versus the prior expectation of -3.0% to 0.0%.

Clinical Diagnostics revenue growth forecast was slightly trimmed to 0.5% to 1.5%, down from the previous 0.5% to 2.5% range.

Notably, Bio-Rad raised its non-GAAP operating margin guidance to 12.0% to 13.0%, up from the previous 10.0% to 12.0%, suggesting improved operational efficiency despite the revenue growth challenges. Non-GAAP gross margin expectations were also slightly raised at the lower end to 53.5% to 54.5%.

Free cash flow projections remained unchanged at $310 million to $330 million for the full year.

Strategic Initiatives

During the earnings call that accompanied this presentation, management highlighted several strategic initiatives, including the launch of the QX Continuum platform, which wasn’t detailed in the slides but represents an important product innovation. The acquisition of Stilla Technologies, completed on the last day of the quarter, is expected to strengthen Bio-Rad’s position in digital PCR technology.

According to John DiVincenzo, President and COO, "We are pleased to share our second quarter 2025 results, which reflect solid execution across the business," while CEO Norman Schwartz added, "We remain resilient and continue to advance our business on many fronts."

The company faces ongoing challenges including market softness in China, funding constraints in government research markets, and potential impacts from tariffs and supply chain issues. However, Bio-Rad’s strategic acquisitions, product innovations, and improved margin outlook suggest management is actively addressing these challenges while positioning for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.