Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Biotage AB (STO:BIOT) presented its Q1 2025 interim results on April 22, 2025, revealing a significant revenue decline offset by strategic initiatives and underlying growth in key segments. Despite reporting a 19.9% drop in revenue, Biotage shares surged 55.72% following the presentation, closing at 141 SEK, signaling strong investor confidence in the company’s strategic direction and long-term growth potential.

The Swedish life science company, which specializes in separation technology and consumables for analytical testing and drug discovery, is navigating a transition period following its Astrea acquisition while maintaining focus on high-growth areas within its core business.

Quarterly Performance Highlights

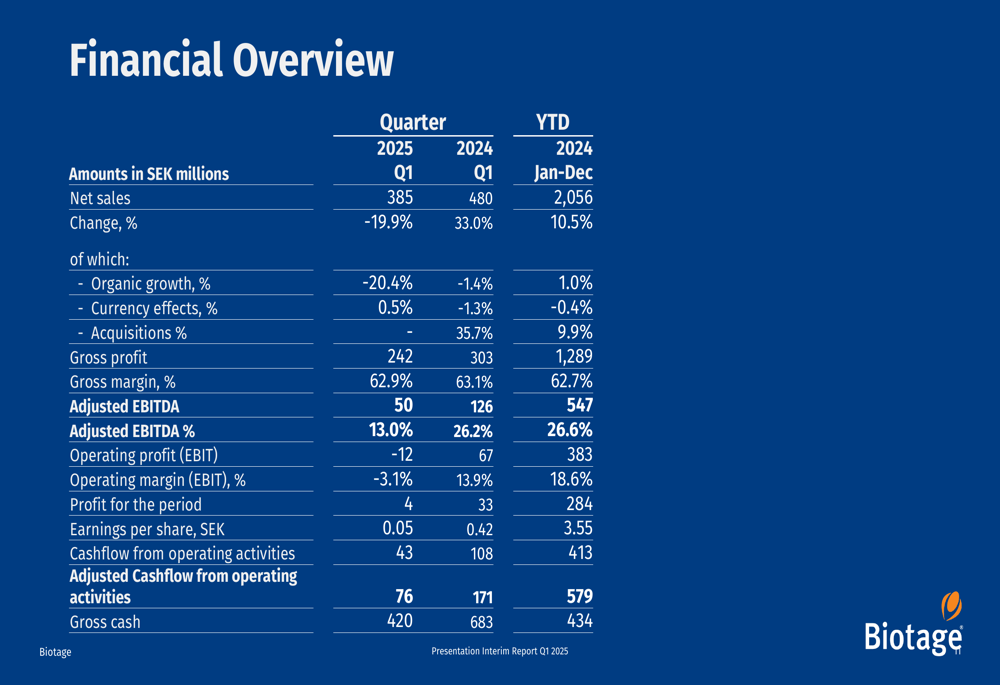

Biotage reported Q1 2025 revenues of 385 MSEK, representing a 19.9% decline compared to the same period last year. This decrease was primarily attributed to the absence of plasma revenue in the Astrea business segment, which contributed 91 MSEK in Q1 2024. However, several bright spots emerged, including 3% growth in Astrea’s non-plasma business, 16% growth in China, and 3% growth in the small molecule segment.

As shown in the following financial overview, despite the revenue decline, Biotage maintained a stable gross margin of 62.9%, nearly identical to the 63.1% reported in Q1 2024:

Adjusted EBITDA fell to 50 MSEK, a 60% decrease from the previous year, with margins compressing to 13.0% from 26.2%. The company ended the quarter with a net cash position of 182 MSEK, comparable to its position at the end of December 2024, demonstrating effective cash management despite operational challenges.

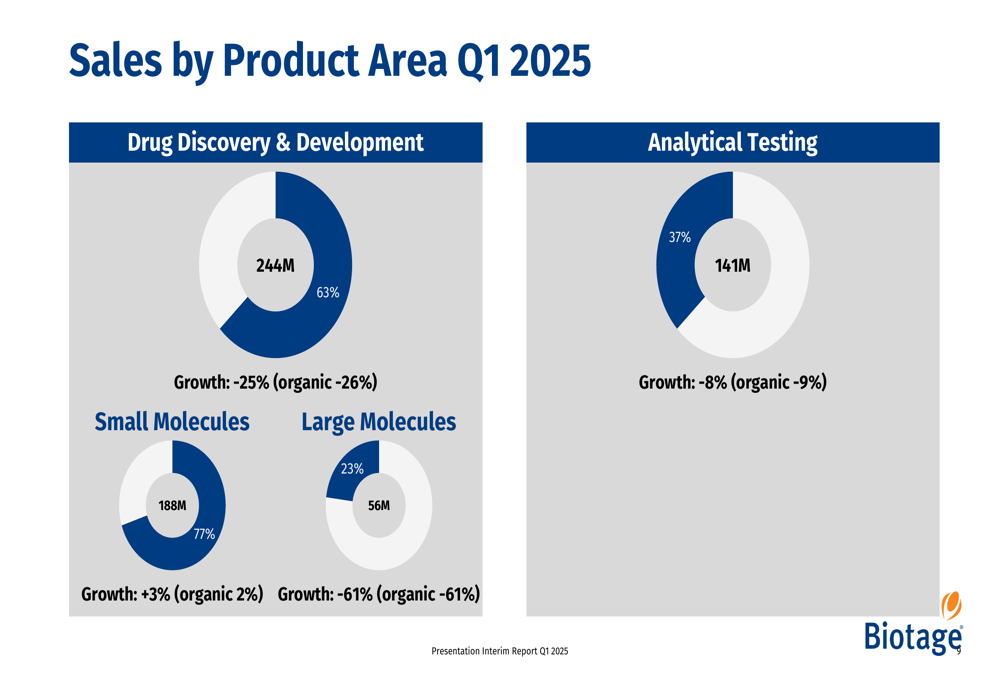

The revenue breakdown by product area reveals the impact of the Astrea transition, with large molecules experiencing a 61% decline while small molecules grew by 3%:

Strategic Initiatives

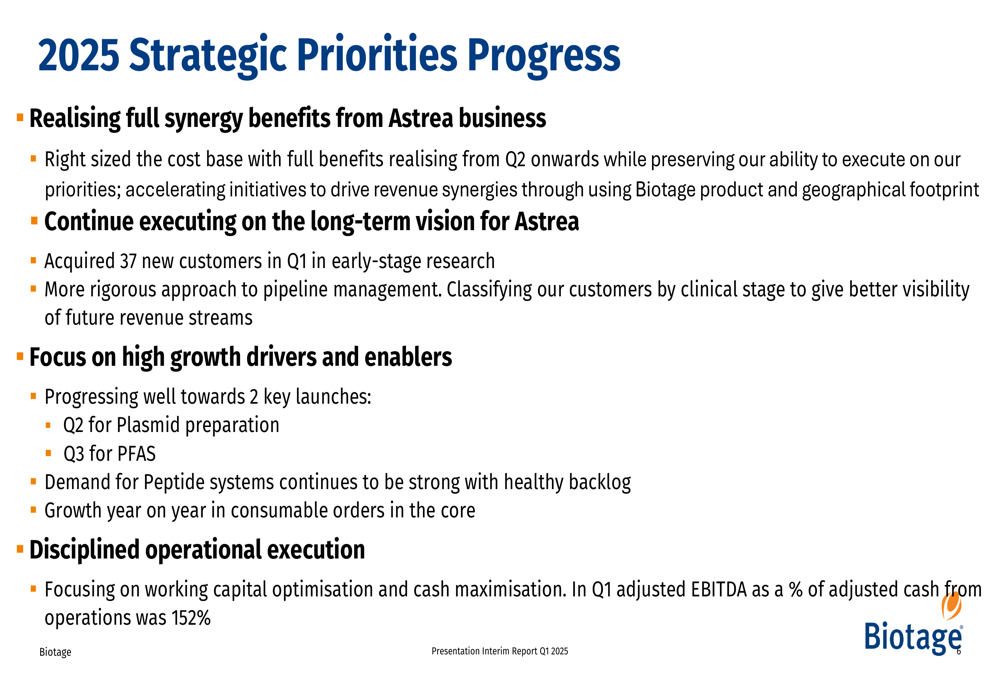

Biotage outlined four key strategic priorities for 2025, focusing on maximizing synergies from the Astrea acquisition, executing on Astrea’s long-term vision, driving high-growth initiatives, and maintaining disciplined operational execution.

The company has implemented cost-cutting measures in the Astrea business, with full benefits expected to materialize from Q2 2025 onward. Simultaneously, Biotage is accelerating revenue synergy initiatives by leveraging its existing product portfolio and geographical footprint.

As illustrated in the strategic priorities slide, Biotage is making progress on several fronts:

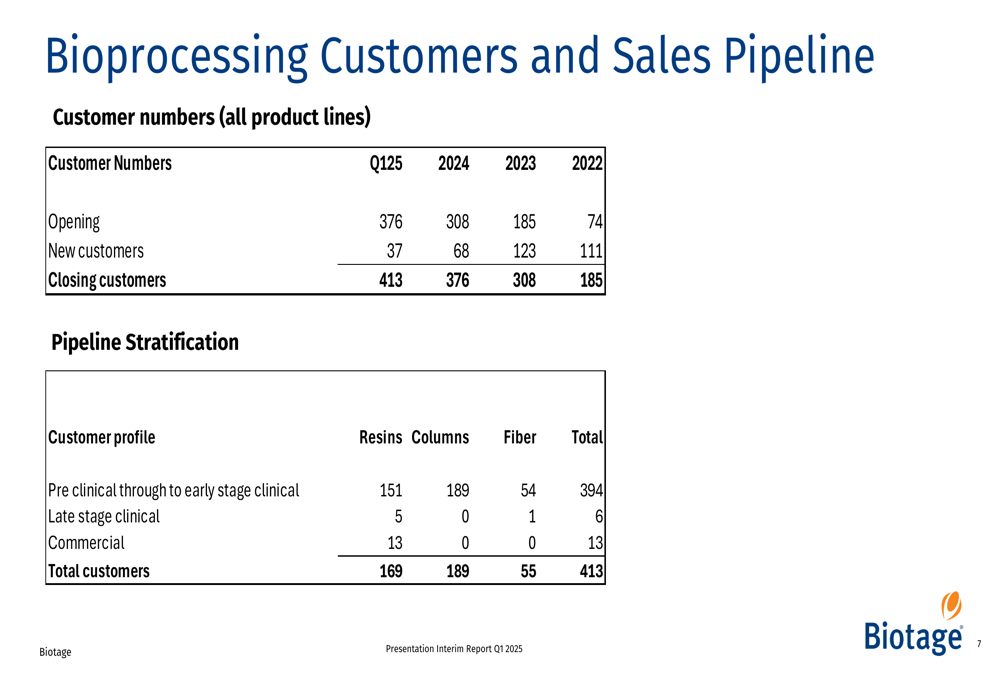

In the bioprocessing segment, Biotage continues to expand its customer base, adding 37 new customers in Q1 2025. The company now serves 413 bioprocessing customers across various product lines, up from 376 at the start of the quarter and 308 at the beginning of 2024, demonstrating strong momentum in this high-growth area.

The following chart illustrates Biotage’s consistent customer acquisition in the bioprocessing segment:

Detailed Financial Analysis

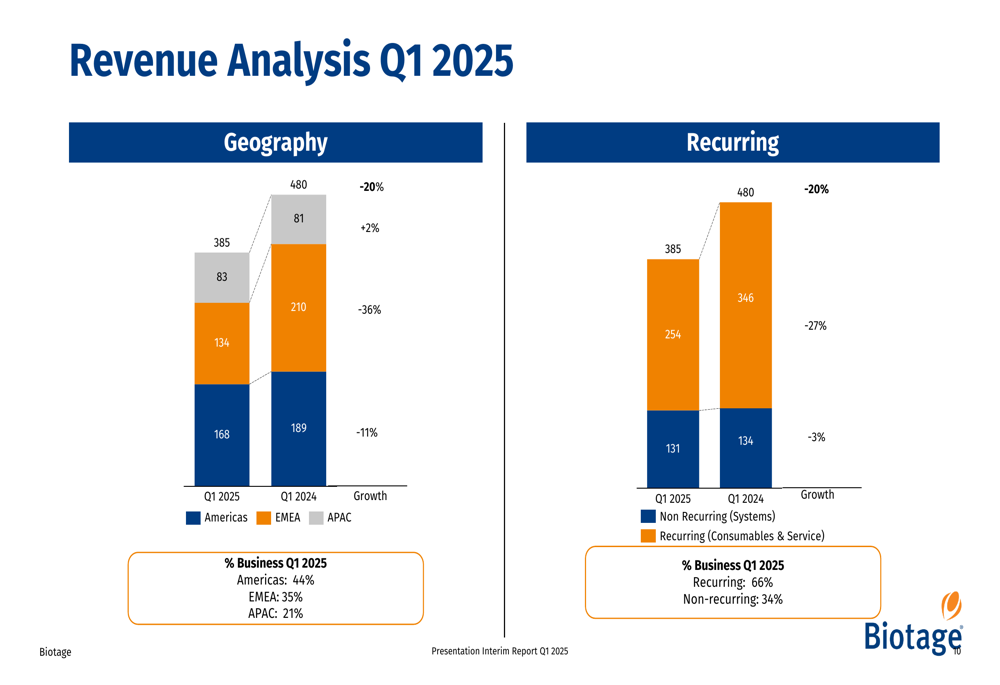

Biotage’s revenue analysis reveals significant geographical variations, with the Americas accounting for 44% of Q1 2025 revenue, followed by EMEA (35%) and APAC (21%). While EMEA experienced a 36% decline, the Americas saw an 11% decrease, and APAC showed modest 2% growth, primarily driven by China’s 16% expansion.

The company’s revenue composition continues to be dominated by recurring revenue, which accounted for 66% of total revenue in Q1 2025:

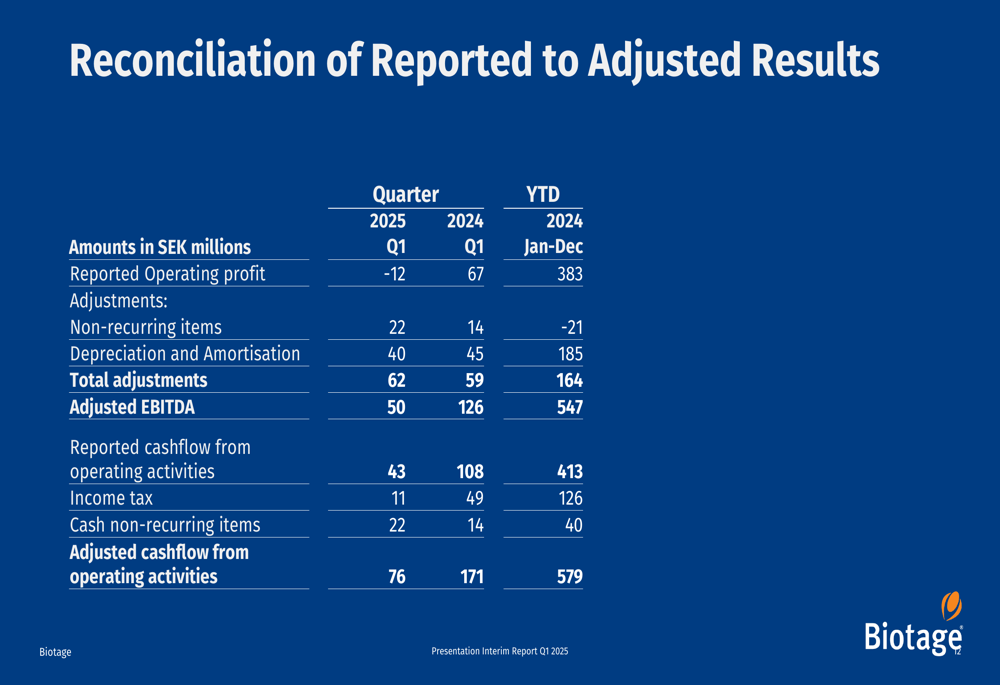

Biotage’s reconciliation of reported to adjusted results shows non-recurring items of 22 MSEK in Q1 2025, primarily related to integration and rationalization costs. Despite the challenging quarter, the company demonstrated strong cash conversion, with adjusted cash flow from operations reaching 76 MSEK, representing 152% of adjusted EBITDA.

Forward-Looking Statements

Looking ahead, Biotage is positioned for potential recovery in the coming quarters as it realizes the full benefits of its cost optimization initiatives in the Astrea business. The company is progressing toward two key product launches: a plasmid preparation solution in Q2 and a PFAS (per- and polyfluoroalkyl substances) solution in Q3, both targeting high-growth market segments.

The company’s vision to be "the best partner for advancing health solutions" and mission to "empower customers to simplify and accelerate discovery and development" underpin its strategic focus on high-value, high-growth segments within the life sciences industry.

Biotage’s strong customer acquisition in bioprocessing, coupled with its disciplined approach to pipeline management and working capital optimization, suggests the company is laying the groundwork for sustainable growth beyond the current transition period. The positive market reaction to the Q1 results indicates investor confidence in Biotage’s strategic direction despite the near-term revenue challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.