Sana Biotechnology stock higher after Eric Jackson touts 100-bagger potential

Introduction & Market Context

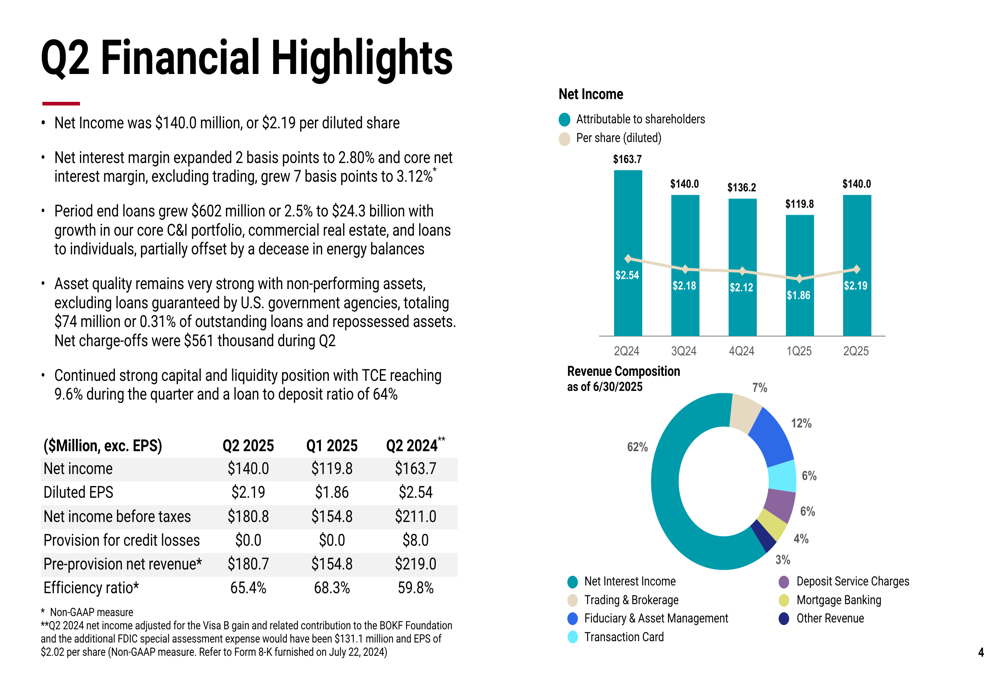

BOK Financial Corporation (NASDAQ:BOKF) reported second-quarter 2025 earnings of $140.0 million, or $2.19 per diluted share, according to the company’s Q2 earnings presentation. This represents a significant improvement from the first quarter’s $1.86 per share, which had fallen short of analyst expectations.

The bank’s stock closed up 1.37% at $105.43 on the day of the earnings release and gained an additional 0.76% in after-hours trading, reflecting positive investor reaction to the results. This performance marks a reversal from the previous quarter when the stock declined 2.58% following disappointing earnings.

Quarterly Performance Highlights

BOK Financial’s second-quarter performance showed notable improvement across several key metrics. Net income increased to $140.0 million from $119.8 million in the previous quarter, though it remained below the $163.7 million reported in the same quarter last year.

The company’s efficiency ratio improved to 65.4% from 68.3% in Q1 2025, indicating better expense management, though it still lags behind the 59.8% reported in Q2 2024.

As shown in the following financial highlights chart:

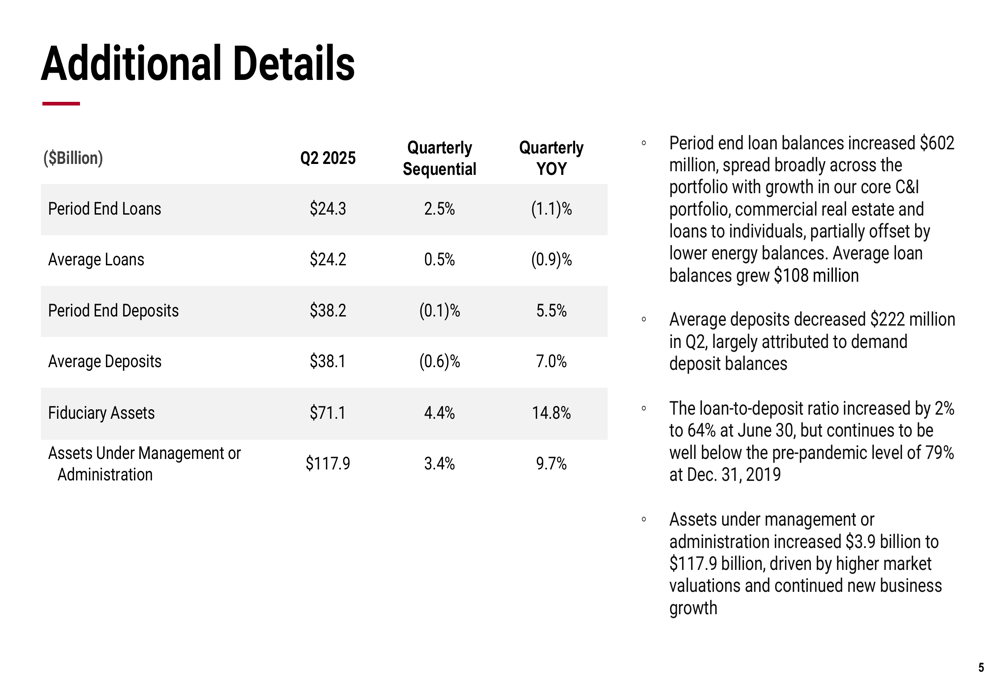

Period-end loans grew by $602 million or 2.5% to $24.3 billion, while the company maintained strong asset quality. The loan-to-deposit ratio increased by 2% to 64% as of June 30, reflecting the loan growth against relatively stable deposits.

Assets under management or administration increased by $3.9 billion to $117.9 billion, demonstrating continued growth in the company’s wealth management business.

Loan Portfolio and Credit Quality

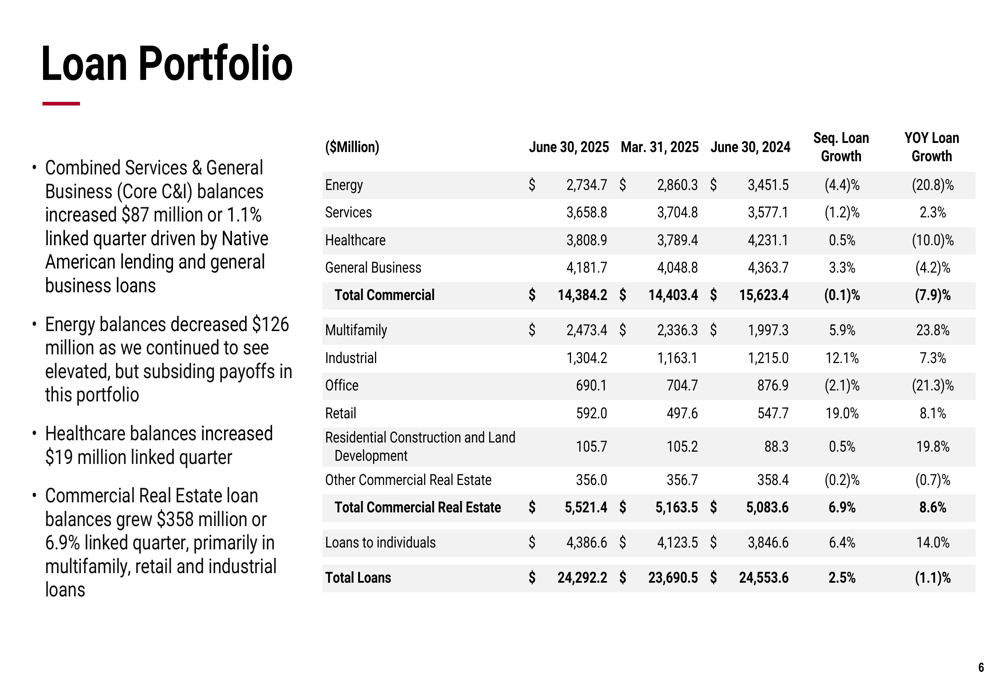

BOK Financial’s loan portfolio showed mixed performance across different segments. Commercial real estate loans grew significantly by 6.9% sequentially and 8.6% year-over-year to $5.5 billion, with particularly strong growth in multifamily (5.9%), industrial (12.1%), and retail (19.0%) segments.

Commercial loans, which make up the largest portion of the portfolio at $14.4 billion, decreased slightly by 0.1% sequentially and declined 7.9% year-over-year. Within this category, energy loans decreased by 4.4% sequentially and 20.8% year-over-year, while general business loans increased by 3.3% sequentially.

Loans to individuals showed robust growth of 6.4% sequentially and 14.0% year-over-year, reaching $4.4 billion.

The detailed breakdown of the loan portfolio is presented below:

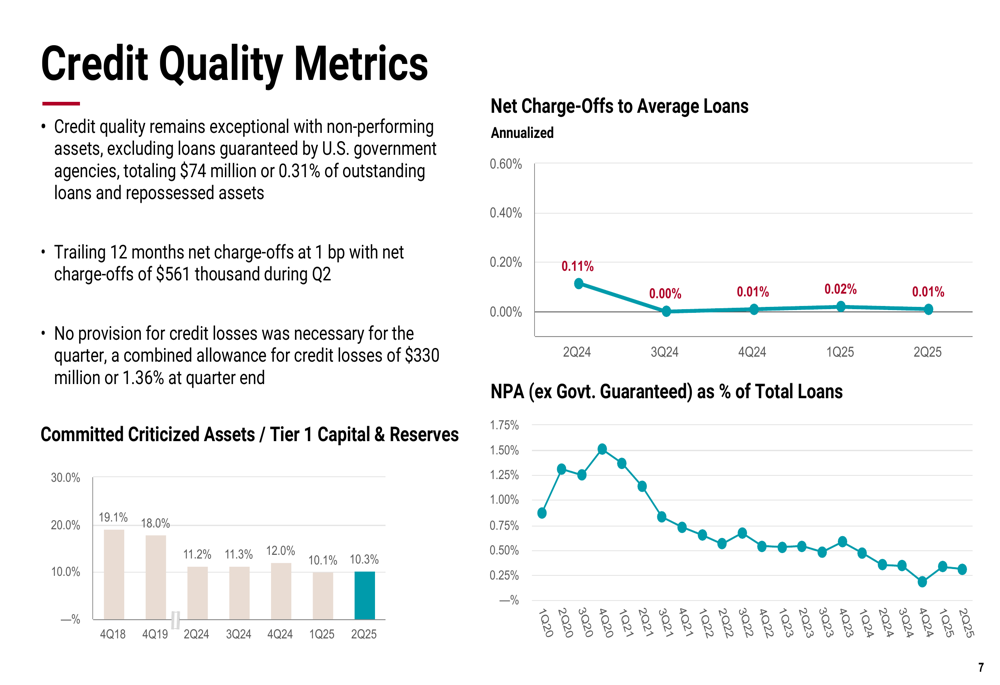

Credit quality metrics continued to improve, with trailing 12-month net charge-offs at just 1 basis point. The company recorded net charge-offs of only $561,000 during Q2 and determined that no provision for credit losses was necessary for the quarter. The combined allowance for credit losses stood at $330 million or 1.36% of loans at quarter end.

Non-performing assets as a percentage of total loans (excluding government-guaranteed loans) decreased significantly from 1.73% in Q1 2024 to 0.35% in Q2 2025, demonstrating the bank’s strong credit risk management.

Fee Income and Revenue Diversification

BOK Financial’s revenue composition remains well-diversified, with net interest income accounting for 62% of total revenue, while various fee income categories make up the remaining 38%.

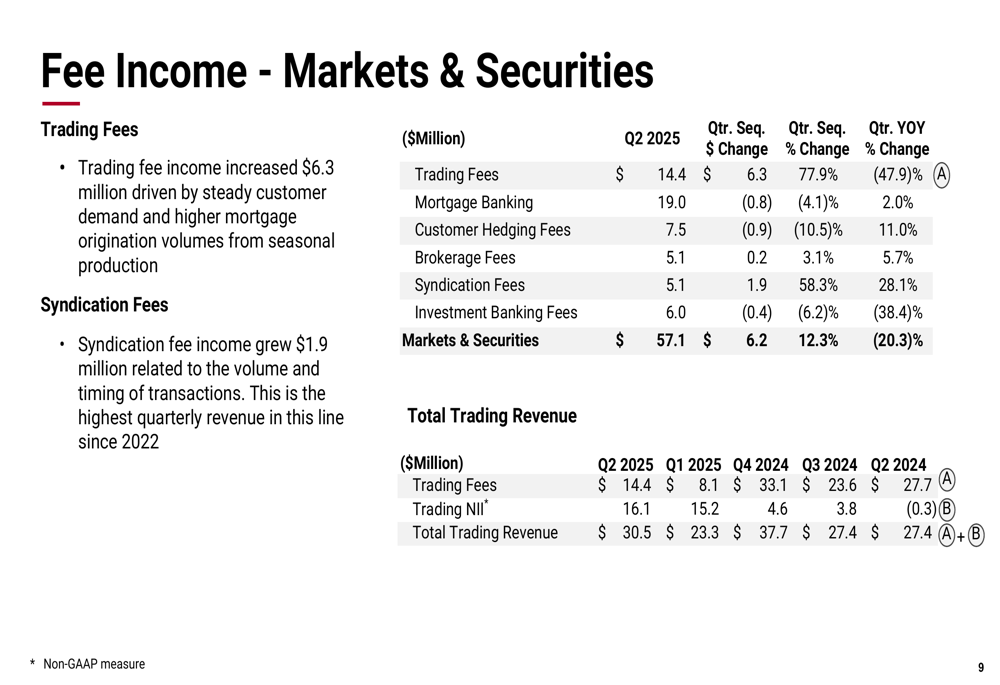

Fee income from markets and securities totaled $57.1 million in Q2 2025, a 12.3% increase from the previous quarter. Trading fees showed particularly strong growth of 77.9%, while syndication fees increased by 58.3%. These gains were partially offset by declines in mortgage banking (-4.1%), customer hedging fees (-10.5%), and investment banking fees (-6.2%).

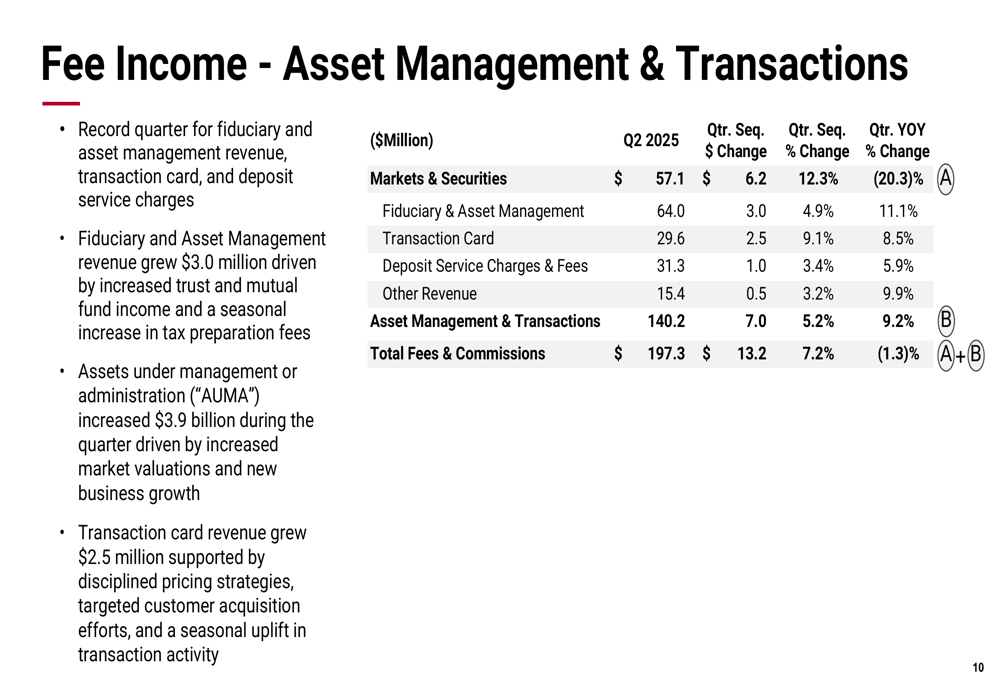

Asset management and transaction-related fee income reached $140.2 million, up 5.2% sequentially and 9.2% year-over-year. Fiduciary and asset management fees increased by 4.9% sequentially and 11.1% year-over-year to $64.0 million, while transaction card revenue grew by 9.1% sequentially to $29.6 million.

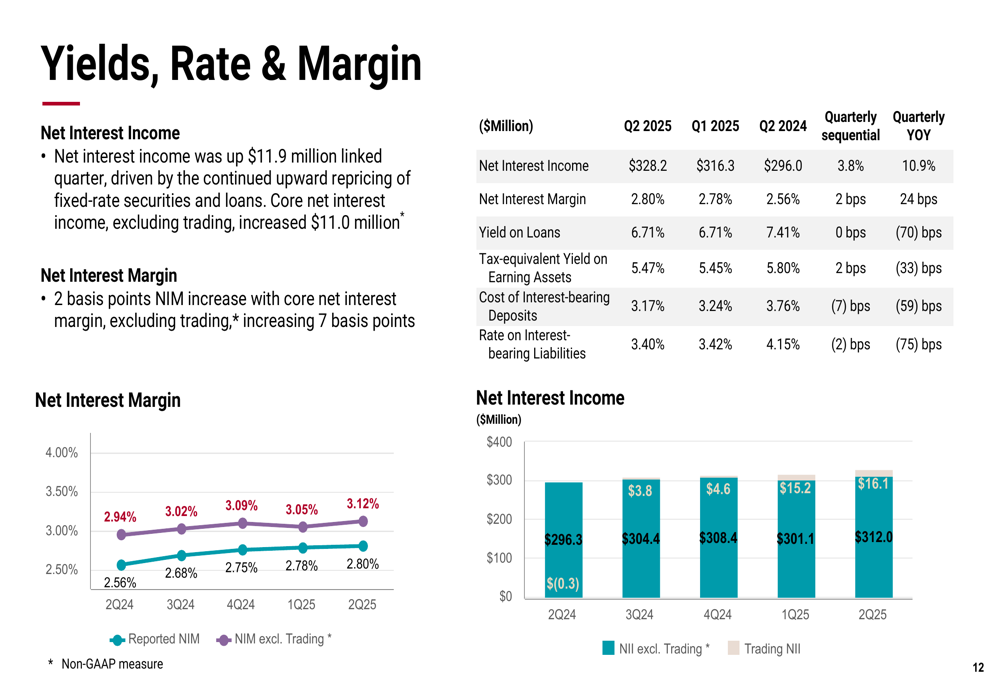

Net Interest Income and Margin

Net interest income increased to $328.2 million, up 3.8% from the previous quarter and 10.9% from the same period last year. The net interest margin expanded by 2 basis points to 2.80%, while the core net interest margin (excluding trading) grew by 7 basis points to 3.12%.

The yield on loans remained stable at 6.71% compared to the previous quarter but decreased by 70 basis points year-over-year. Meanwhile, the cost of interest-bearing deposits declined by 7 basis points sequentially to 3.17%, contributing to margin expansion.

The following chart illustrates the trends in net interest income and margin:

Total (EPA:TTEF) operating expenses increased by 2.0% sequentially and 5.3% year-over-year to $354.5 million. Personnel expenses, which account for the largest portion of operating costs at $214.7 million, remained relatively flat with a 0.2% sequential increase but rose 12.4% year-over-year. Other operating expenses increased by 4.8% sequentially but decreased by 4.0% year-over-year to $139.8 million.

Forward-Looking Statements

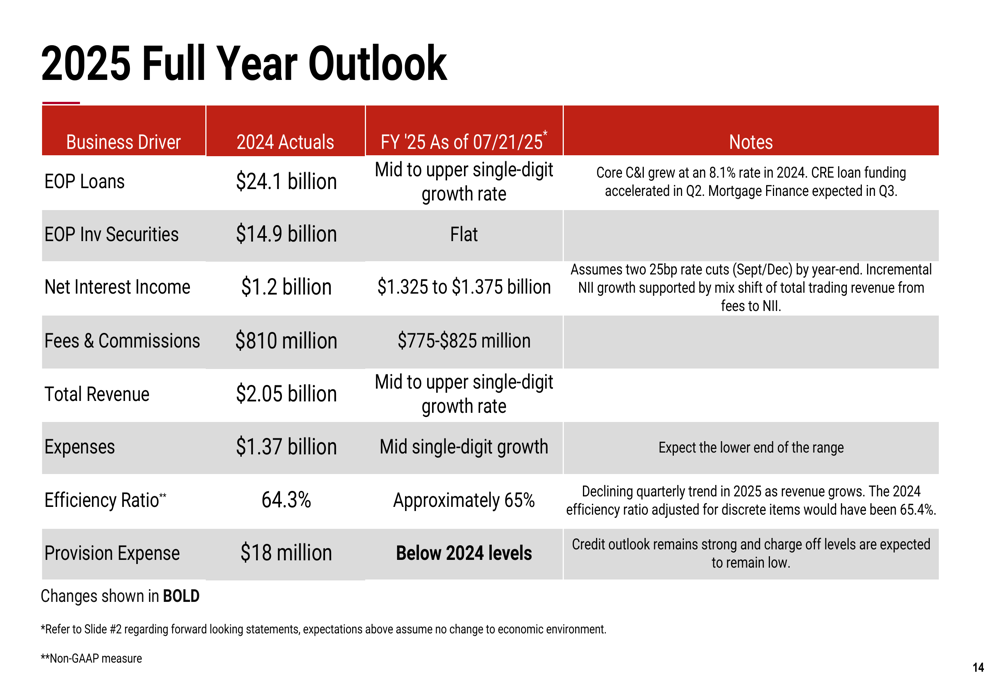

BOK Financial’s management provided a positive outlook for the remainder of 2025, projecting mid to upper single-digit loan growth for the full year. The company expects net interest income to reach $1.325-1.375 billion and fees and commissions to range between $775-825 million.

Total revenue is forecast to grow at a mid to upper single-digit rate, while expenses are expected to increase at a mid-single-digit pace. The efficiency ratio is projected to be approximately 65%, and provision expenses are anticipated to remain below 2024 levels.

The full-year outlook is summarized in the following table:

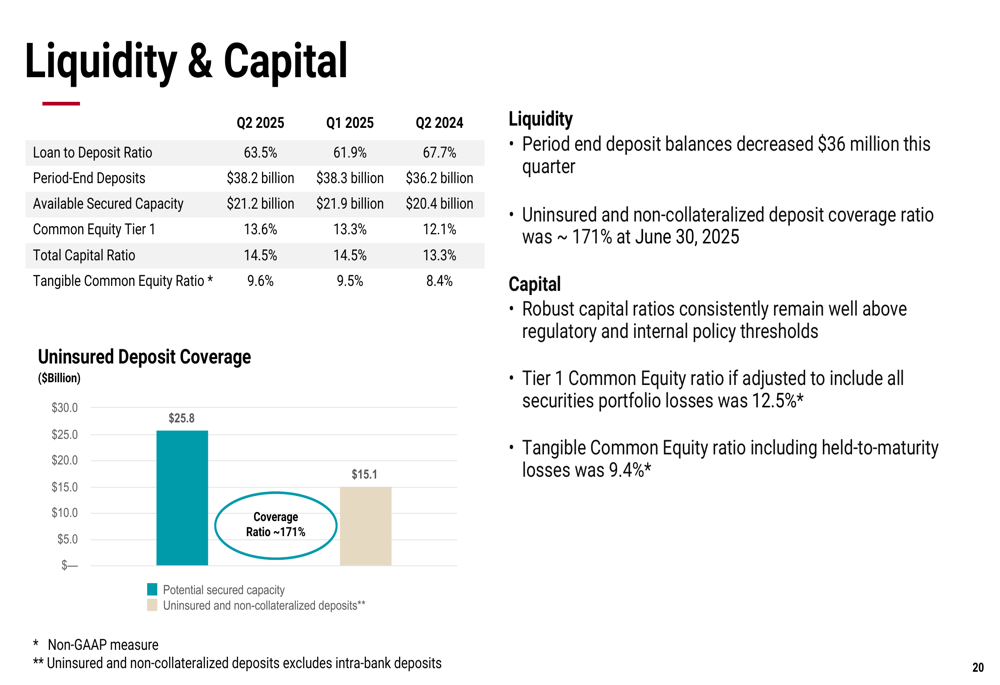

The company maintains a strong capital position with a Common Equity Tier 1 ratio of 13.6% and a total capital ratio of 14.5%. The tangible common equity ratio stands at 9.6%, providing ample capacity for continued growth and potential shareholder returns.

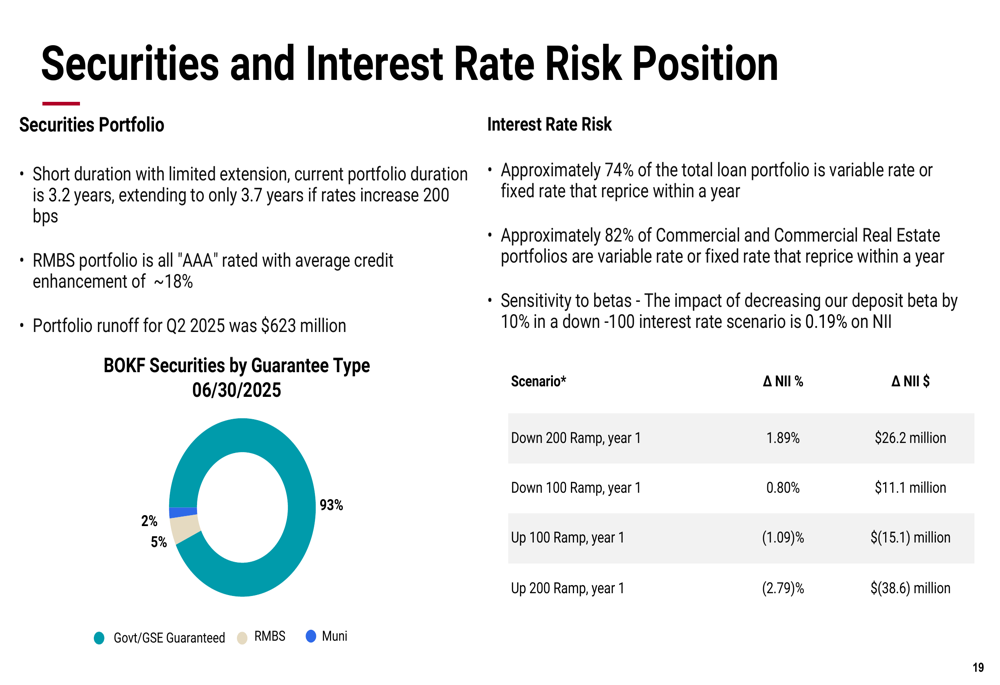

BOK Financial’s securities portfolio remains conservatively positioned, with 93% of securities backed by government or GSE guarantees. The company’s interest rate risk is well-managed, with approximately 74% of the total loan portfolio either variable rate or fixed rate that reprices within a year.

Overall, BOK Financial’s Q2 2025 results demonstrate a significant improvement from the previous quarter, with strong loan growth, expanding margins, and solid credit quality positioning the company well for the remainder of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.