United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Bonheur ASA (OSE:BONHR) presented its second quarter 2025 results on July 10, revealing a complex financial picture characterized by declining revenue but improved bottom-line performance. The company’s stock closed at NOK 216 following the announcement, representing a 2.31% decrease and placing it closer to its 52-week low of NOK 205.5 than its high of NOK 287.5.

The Norwegian industrial investment company, which operates across renewable energy, wind service, cruise, and other investment segments, faced varied market conditions during the quarter, including volatile power prices across European markets and challenging conditions in the wind service sector.

Quarterly Performance Highlights

Bonheur reported consolidated revenues of NOK 3,251 million for Q2 2025, down from NOK 4,283 million in the same period last year. EBITDA declined to NOK 1,053 million from NOK 1,229 million in Q2 2024. Despite these decreases, the company’s net result improved significantly to NOK 920 million, up from NOK 694 million in the previous year, representing a NOK 226 million increase.

As shown in the following consolidated financial summary, the company’s bottom-line improvement was largely driven by positive net finance results, primarily from the divestment of UWL:

The divestment of UWL, completed on April 30, 2025, resulted in a profit of EUR 29 million (NOK 347 million) reflected in the accounts as financial income. This transaction had a total cash effect of EUR 51.2 million across Q1 and Q2.

Segment Analysis

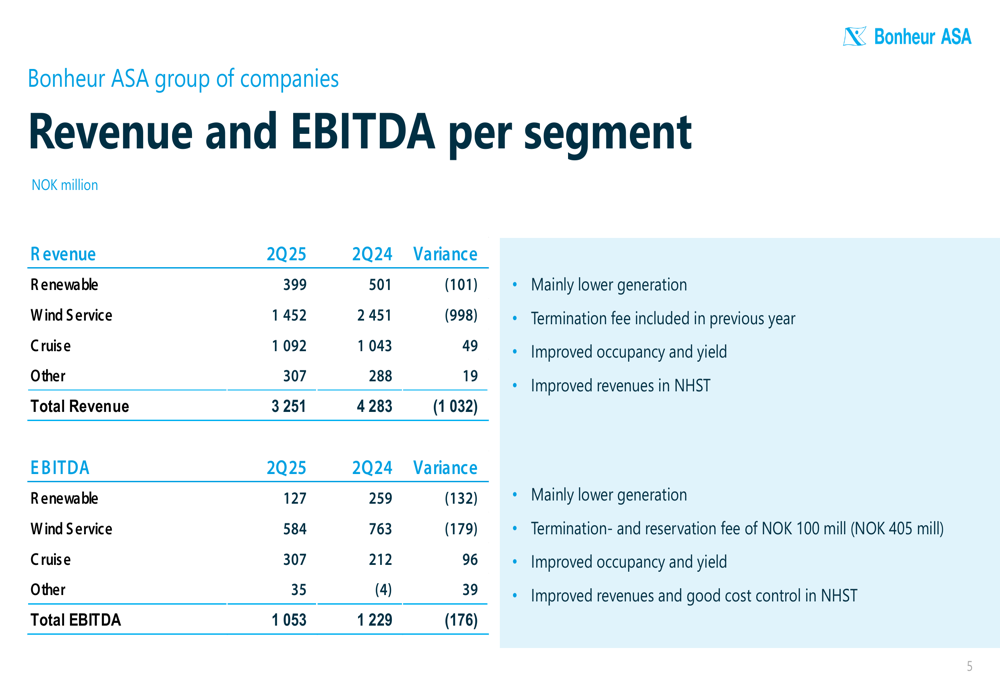

Bonheur’s performance varied significantly across its four business segments. The following table provides a clear breakdown of revenue and EBITDA by segment, comparing Q2 2025 with Q2 2024:

The Renewable Energy segment experienced a challenging quarter, with EBITDA falling to NOK 127 million from NOK 259 million in Q2 2024. This decline was primarily attributed to lower generation, which was 20% below P50 due to downtime and low wind conditions in Scotland. Additionally, while power prices were 10% higher in the UK, they were 56% lower in Sweden.

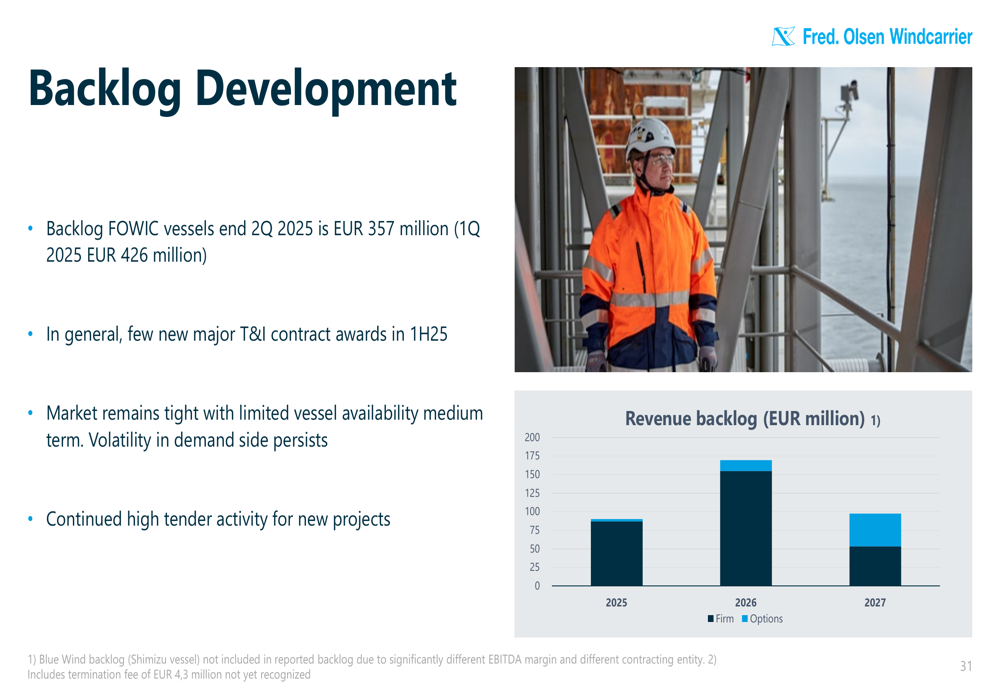

The Wind Service segment reported EBITDA of NOK 584 million, down from NOK 763 million in Q2 2024. This decrease was largely due to a termination and reservation fee of NOK 100 million in Q2 2025, compared to NOK 405 million in the same period last year. Vessel utilization was at 73% due to yard stays, though the company reported a backlog of EUR 357 million, up from EUR 325 million in Q2 2024.

In contrast, the Cruise segment showed strong improvement with EBITDA of NOK 307 million, up from NOK 212 million in Q2 2024. This growth was driven by improved occupancy (79% vs. 77%) and higher net ticket income per passenger day (GBP 210 vs. GBP 196). Booking numbers were reported to be 11% higher compared to last year.

The Other Investments segment also improved, with EBITDA of NOK 35 million compared to NOK -4 million in Q2 2024, primarily due to improved revenues and cost control in NHST.

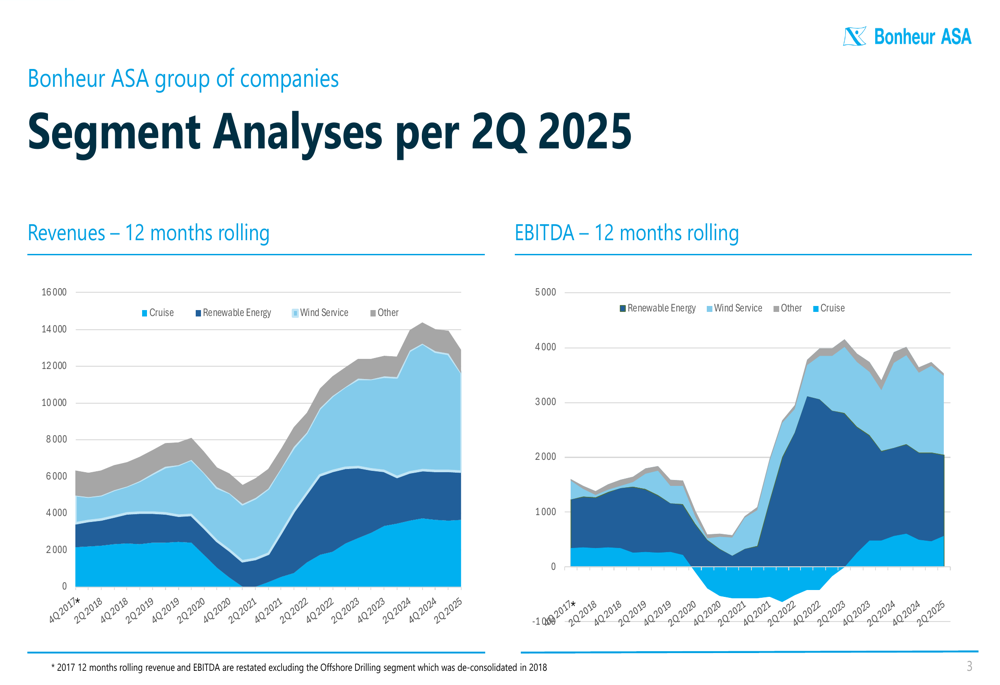

The following chart illustrates the 12-month rolling revenue and EBITDA trends across segments:

Strategic Initiatives and Project Updates

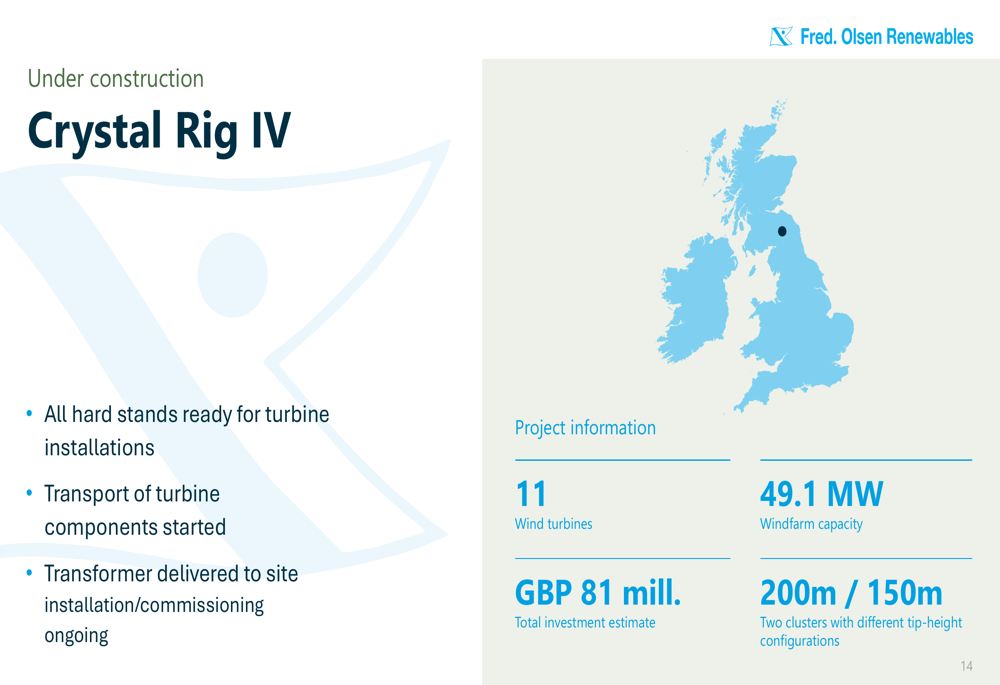

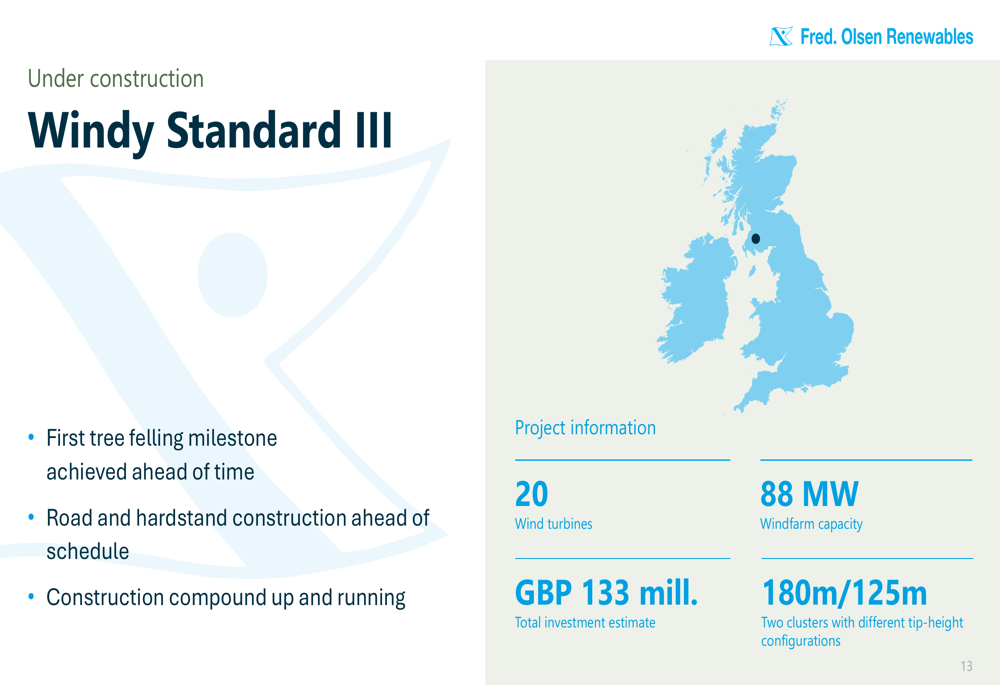

Bonheur continued to advance several key projects across its business segments during the quarter. In the Renewable Energy segment, construction of Crystal Rig IV and Windy Standard III wind farms in the UK is progressing well.

The Crystal Rig IV project has completed all hard stands for turbine installations, with component transport underway:

Similarly, the Windy Standard III project is ahead of schedule on road and hardstand construction:

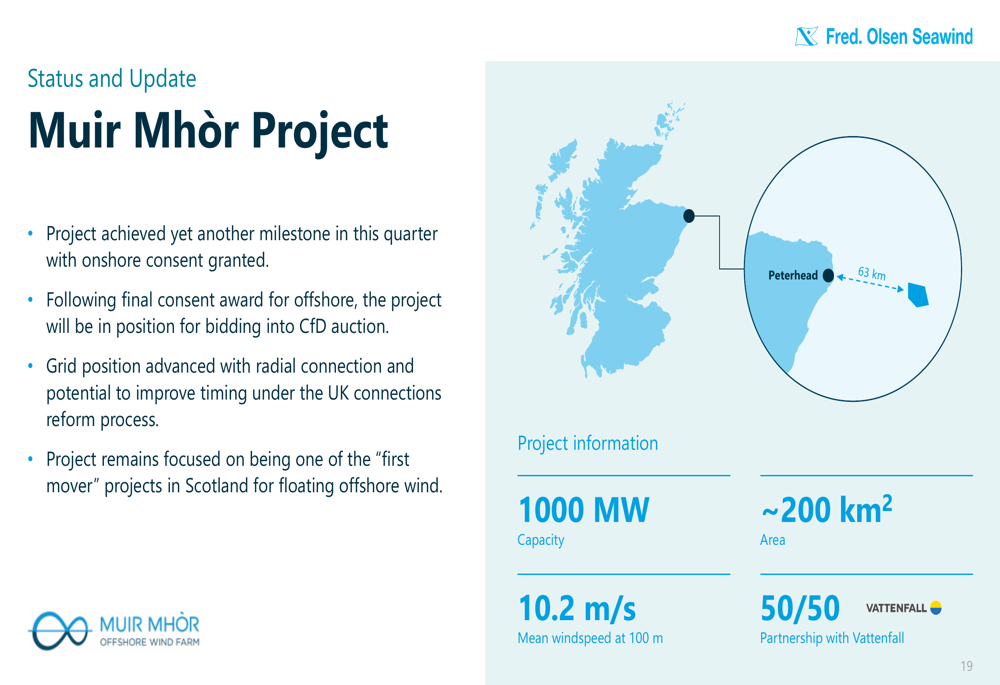

In the offshore wind sector, Bonheur’s Muir Mhòr project (a 50/50 joint venture with Vattenfall) achieved a significant milestone with the award of onshore consent:

Fred. Olsen Windcarrier reported a backlog development of EUR 357 million at the end of Q2 2025, down from EUR 426 million in Q1 2025. The company noted that the vessel market remains tight with limited availability in the medium term:

Financial Position and Outlook

Bonheur maintained a strong financial position with cash holdings of NOK 5,679 million for 100% owned entities, against external debt of NOK 3,508 million, resulting in a net cash position of NOK 2,171 million. However, less than 100% but more than 50% owned entities carried a net debt position of NOK 4,915 million.

The company’s Wind Service segment expects to see the end of a period with high yard activity in Q3, with one vessel in dry dock. The Cruise segment is targeting continued improvement, with cumulative sales for 2025, 2026, and 2027 up 11% compared to previous years.

In the Renewable Energy segment, Bonheur noted that onshore wind continues to play a core part in the future energy mix, with the company benefiting from presence in committed markets and a strong pipeline. However, the segment faces challenges from weak power prices and curtailed generation in Sweden, despite high wind conditions.

The company’s financial policy emphasizes maintaining a strong financial and liquidity position, with subsidiaries optimizing their own non-recourse financing. To accelerate growth within capital-intensive industries, Bonheur is considering various means of external capital, including joint ventures, public markets, and M&A opportunities.

Looking ahead, Bonheur faces both opportunities and challenges across its diverse business portfolio, with particular focus on advancing its renewable energy projects and maintaining strong performance in its cruise business while navigating the volatile conditions in the wind service market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.