Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Bravida Holding AB (STO:BRAV) presented its Q2 2025 results on July 11, showing improved profitability despite declining sales as the Nordic technical installation and service provider continues to prioritize margins over volume in a challenging market environment.

Introduction & Market Context

Bravida, which operates across 190 locations in the Nordic countries with 14,000 employees, reported a 9% decline in net sales for Q2 2025, but managed to increase its EBITA margin to 5.4% from 4.5% in the same period last year. The company’s stock closed at SEK 96.60 on the presentation day, down 0.93% according to available market data.

The presentation was led by Group President & CEO Mattias Johansson and newly appointed Group CFO Petra Vranjes, who joined the company’s management team recently.

Quarterly Performance Highlights

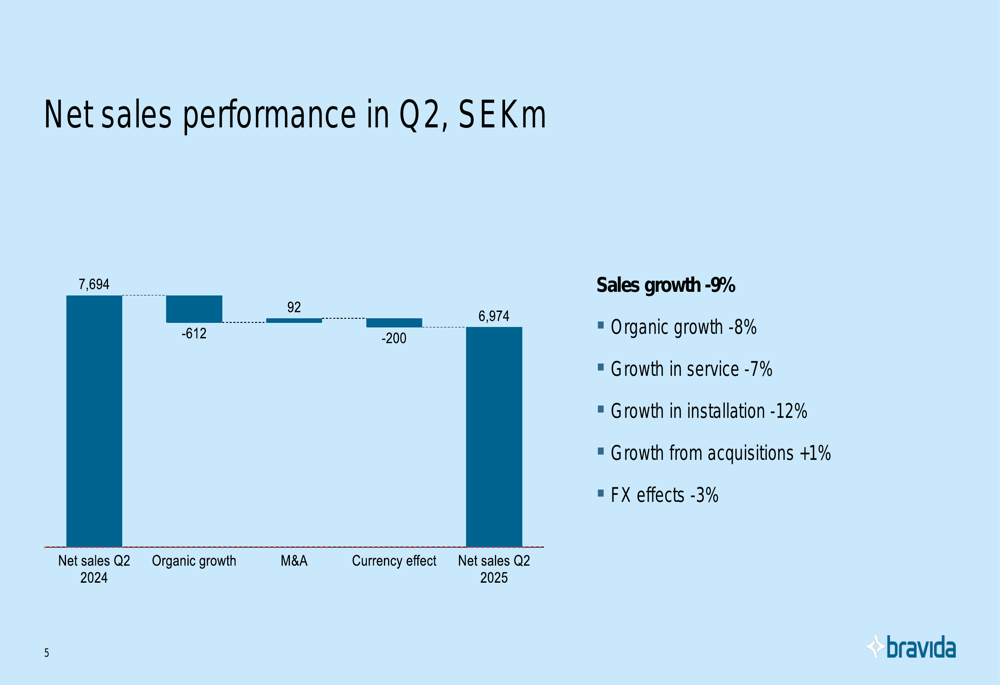

Bravida’s Q2 2025 results showed mixed performance with declining sales but improved profitability. Net sales decreased to SEK 6,974 million, down 9% compared to Q2 2024 (SEK 7,694 million). This decline was attributed to organic growth of -8%, currency effects of -3%, partially offset by acquisition growth of +1%.

As shown in the following chart of quarterly net sales performance:

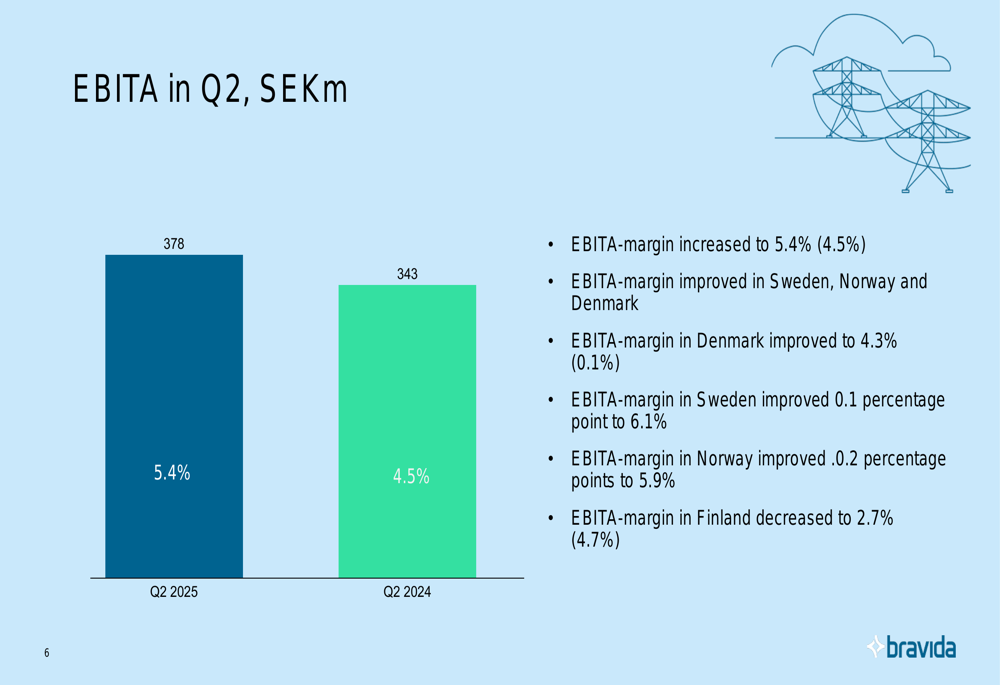

Despite the sales decline, EBITA improved to SEK 378 million (5.4% margin) from SEK 343 million (4.5% margin) in Q2 2024. This improvement was primarily driven by better performance in Denmark, which saw its EBITA margin jump to 4.3% from just 0.1% in the same period last year. Sweden and Norway also showed margin improvements.

The company’s quarterly EBITA performance is illustrated here:

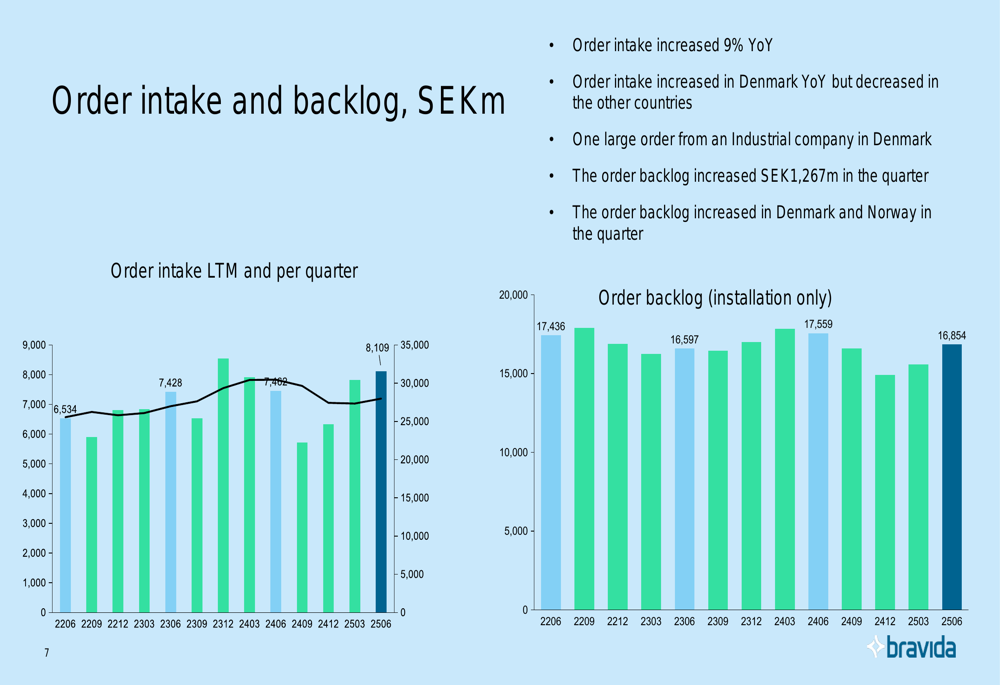

Order intake provided a positive signal, increasing by 9% year-over-year, largely due to strong performance in Denmark where a large order from an industrial company was secured. The order backlog increased by SEK 1,267 million during the quarter, with notable gains in Denmark and Norway.

The following chart shows the order intake and backlog trends:

Cash flow performance was weaker, with cash conversion declining to 80% from 112% in the previous year. The company attributed this to "a temporary increased contract asset in one large project" and noted two larger unpaid receivables expected to be resolved within six months, plus one large unpaid receivable expected to be resolved by 2028.

Regional Performance Analysis

Bravida’s performance varied significantly across its four Nordic markets:

Sweden: Net sales decreased by 9% to SEK 3,385 million, with organic growth at -10% and acquisition growth at +1%. The decline was particularly pronounced in southern Sweden, which saw sales drop by SEK 230 million year-over-year. Despite this, the EBITA margin improved slightly to 6.1%, and Sweden remains the most profitable region for Bravida.

Denmark: The standout performer with sales growth of 1% (organic growth +6%, FX effect -5%) and a dramatic improvement in EBITA margin to 4.3% from just 0.1% in Q2 2024. Order intake surged 78% year-over-year, boosted by a large industrial order, and the order backlog increased by SEK 1,148 million during the quarter.

Norway: Experienced an 18% sales decline (organic -13%, FX -5%), with installation business down 27% and service business down 10%. Despite these challenges, the EBITA margin improved to 5.9%, and the order backlog increased by SEK 143 million during the quarter.

Finland: Showed the weakest performance with a 15% sales decline and EBITA margin decreasing to 2.7% from 4.7% in Q2 2024. The decline was attributed to weaker margins in the service business.

Strategic Initiatives

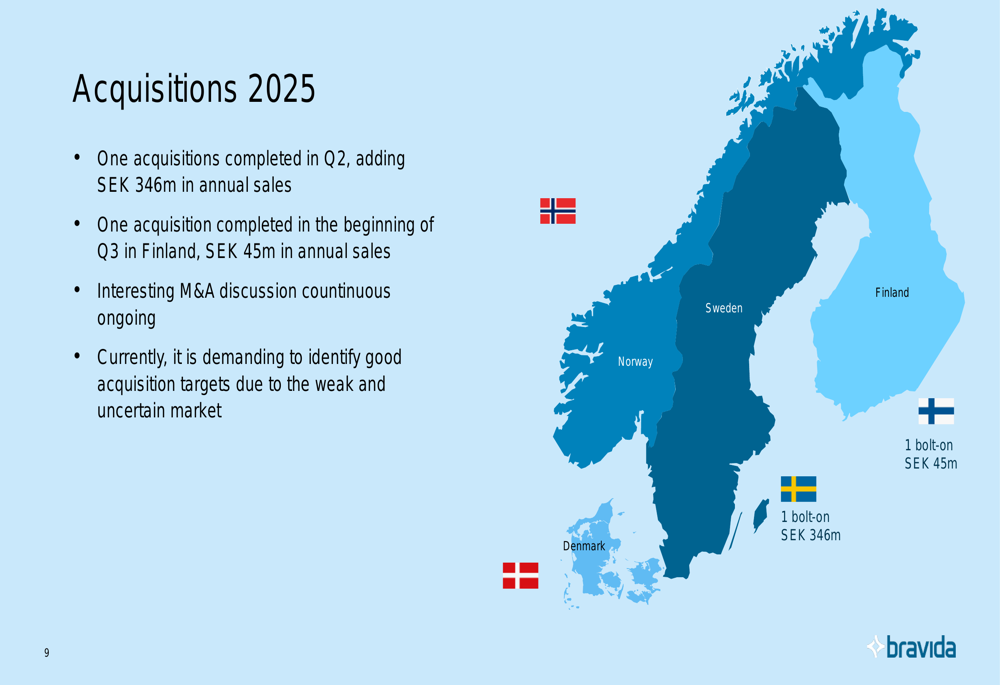

Bravida continues to pursue strategic acquisitions, albeit at a measured pace given current market conditions. The company completed one acquisition in Denmark during Q2, adding SEK 346 million in annual sales, and another in Finland at the beginning of Q3, adding SEK 45 million in annual sales.

The company noted that while M&A discussions are ongoing, "it is currently demanding to identify good acquisition targets due to the weak and uncertain market."

The following map shows Bravida’s recent acquisition activity:

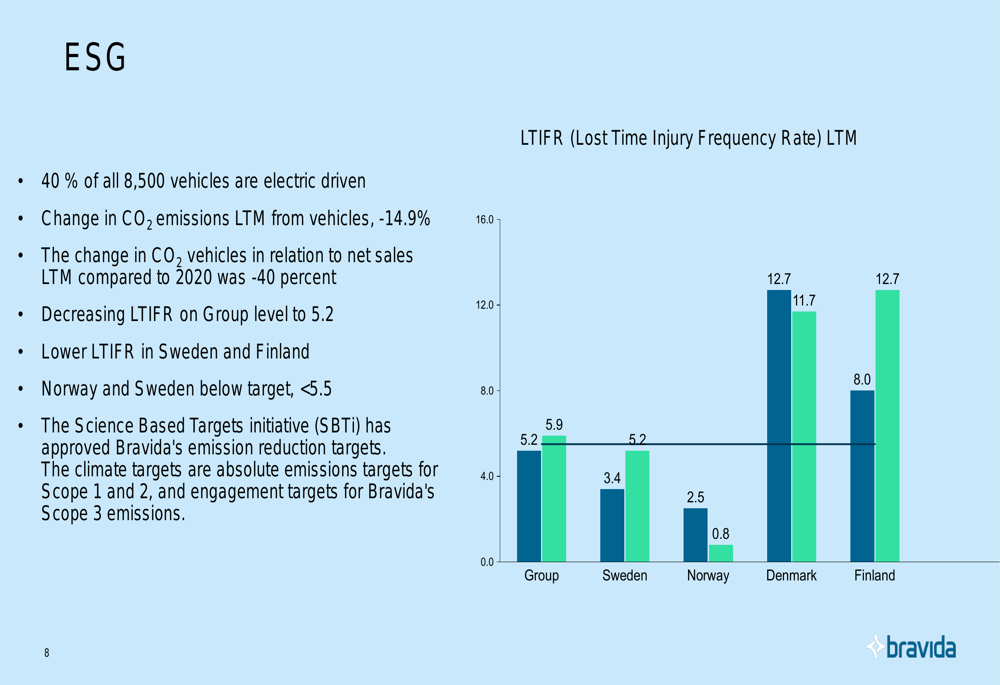

On the sustainability front, Bravida reported progress in its ESG initiatives. The company has converted 40% of its 8,500-vehicle fleet to electric vehicles, resulting in a 14.9% reduction in CO2 emissions over the last twelve months. Safety performance also improved, with the Lost Time Injury Frequency Rate (LTIFR) decreasing by 12% to 5.2.

The company’s ESG performance is illustrated in this chart:

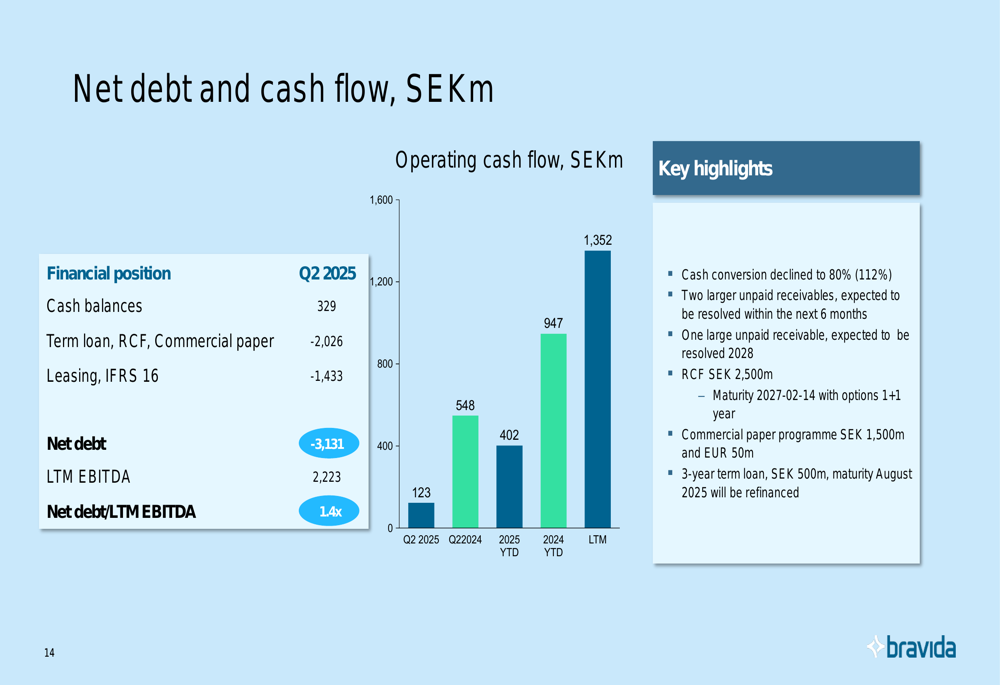

Bravida’s financial position remains solid with a net debt of SEK 3,131 million, representing 1.4x EBITDA (up from 1.1x previously). The company has a revolving credit facility of SEK 2,500 million maturing in February 2027 with extension options, and plans to refinance a SEK 500 million term loan maturing in August 2025.

The following chart details Bravida’s debt and cash flow position:

Forward-Looking Statements

Looking ahead, Bravida expects service activity to remain stable while challenges in the installation business will continue, with variations across geographic regions. The company sees favorable market conditions in infrastructure, industry, defense facilities, and civil engineering, which should provide business opportunities.

Bravida emphasized that it will maintain its "project-selective strategy with continued focus on cost control across all projects," reinforcing its ’margin over volume’ approach. This strategy appears to be yielding results, as evidenced by the improved EBITA margin despite declining sales.

Comparing Q2 results with the Q1 2025 performance reported earlier, Bravida shows a consistent focus on margin improvement amid market challenges. The Q1 earnings call described 2025 as a "transition year" with expectations that the market would "bottom out" during this period. The Q2 results suggest this outlook remains valid, with the steeper 9% sales decline in Q2 (compared to 5% in Q1) indicating continued market weakness, while the improved profitability demonstrates the effectiveness of the company’s strategic focus on margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.