Bank of America, Morgan Stanley, Nvidia and Dollar Tree rise premarket

Introduction & Market Context

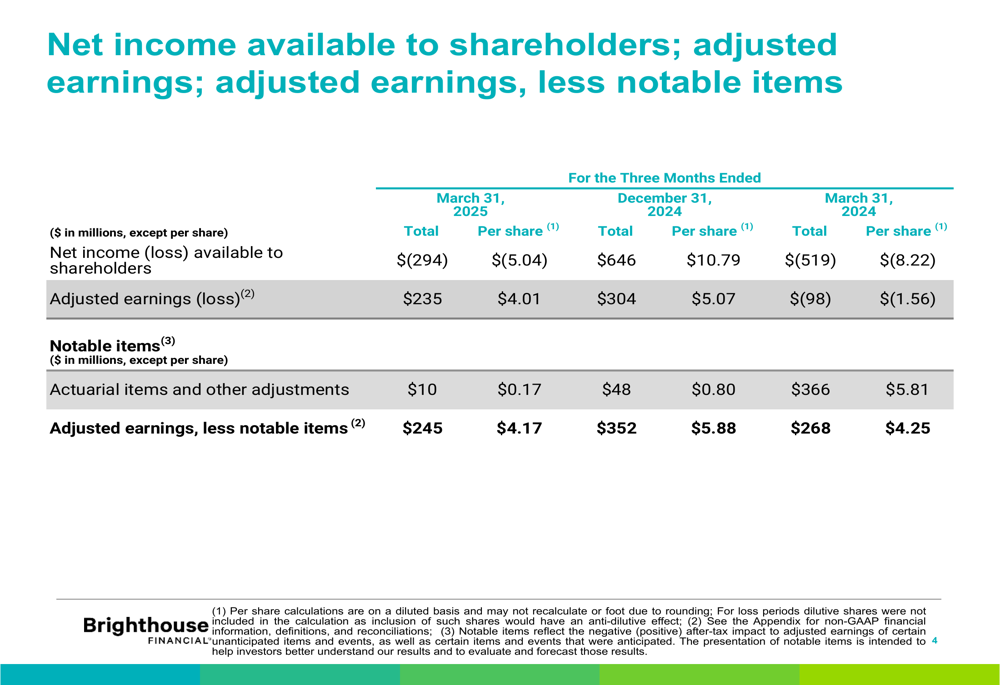

Brighthouse Financial , Inc. (NASDAQ:BHF) presented its first quarter 2025 earnings results on May 9, 2025, reporting adjusted earnings, less notable items, of $245 million, or $4.17 per share. Despite these solid adjusted results, the company posted a net loss of $294 million, highlighting the ongoing volatility in its financial performance.

The insurance provider’s stock closed at $57.89 on May 8, down 0.89% ahead of the earnings presentation, but showed a slight uptick of 0.16% in after-hours trading.

Quarterly Performance Highlights

Brighthouse Financial’s Q1 2025 results revealed a mixed financial picture. While the company maintained strong capital metrics, its adjusted earnings declined sequentially from the previous quarter.

As shown in the following comparison of key financial metrics:

The company reported a net loss available to shareholders of $294 million ($5.04 per share) for Q1 2025, compared to net income of $646 million in Q4 2024 and a net loss of $519 million in Q1 2024. This volatility in net income primarily reflects market impacts on derivatives and market risk benefits.

Adjusted earnings, which exclude notable items and market impacts, stood at $245 million ($4.17 per share) for Q1 2025, down from $352 million in Q4 2024 and $268 million in Q1 2024. Management noted that Q1 2025 adjusted earnings were $15 million below quarterly run rate expectations, primarily due to lower-than-expected alternative investment income.

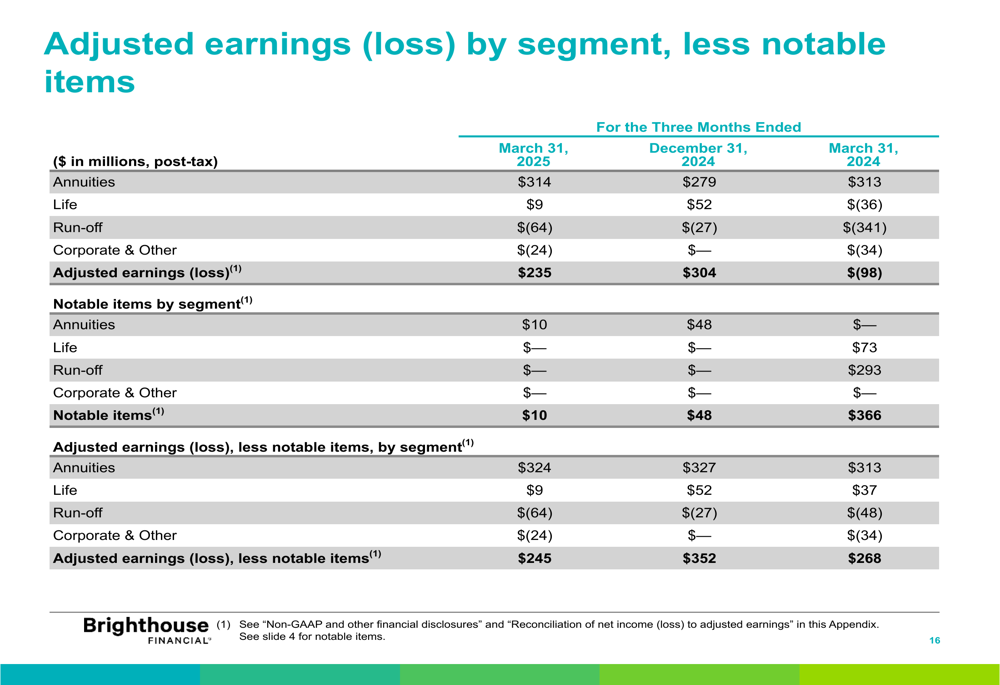

Segment Performance

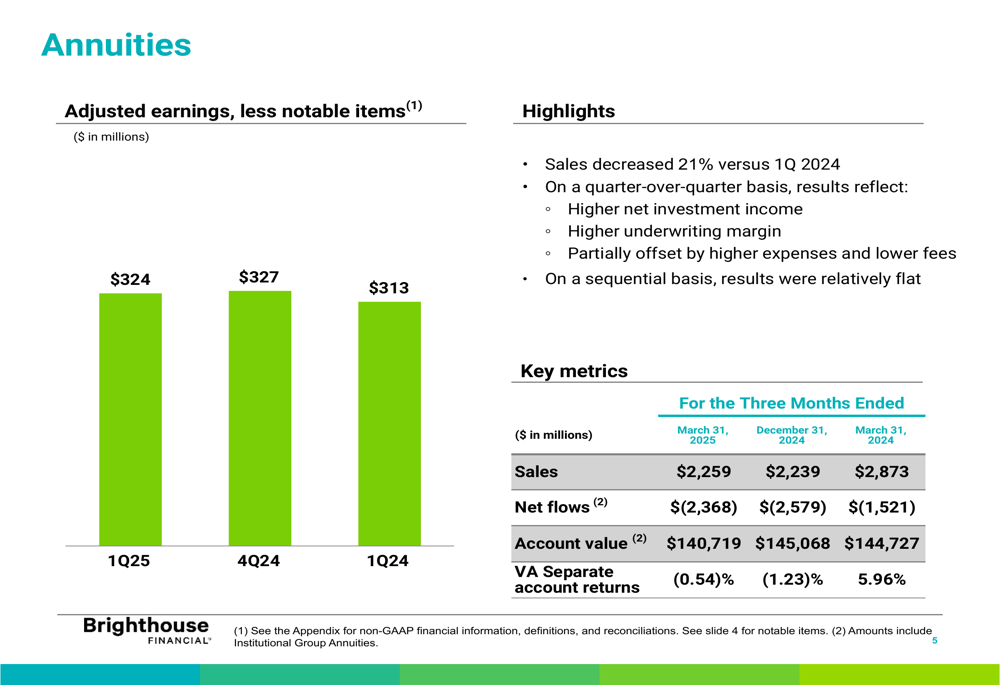

The Annuities segment, Brighthouse’s largest business line, delivered relatively stable performance with adjusted earnings of $324 million in Q1 2025, compared to $327 million in Q4 2024 and $313 million in Q1 2024. However, annuity sales decreased 21% year-over-year.

The following chart illustrates the Annuities segment performance:

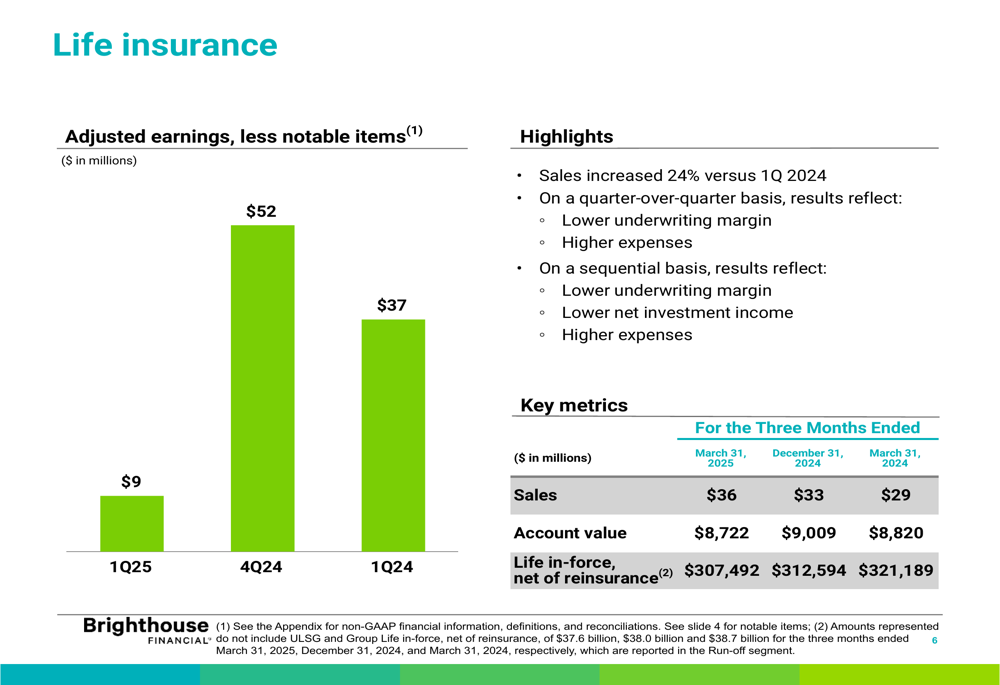

The Life Insurance (NSE:LIFI) segment showed a significant decline in performance, with adjusted earnings dropping to just $9 million in Q1 2025 from $52 million in Q4 2024. The company attributed this decrease to lower underwriting margin and higher expenses. Despite this earnings decline, life insurance sales increased 24% compared to Q1 2024.

The Life Insurance segment results are illustrated here:

The Run-off segment, which contains the company’s legacy businesses, reported a loss of $64 million in Q1 2025, a deterioration from the $27 million loss in Q4 2024. The company cited lower net investment income as the primary factor, partially offset by a higher underwriting margin.

Capital Position and Liquidity

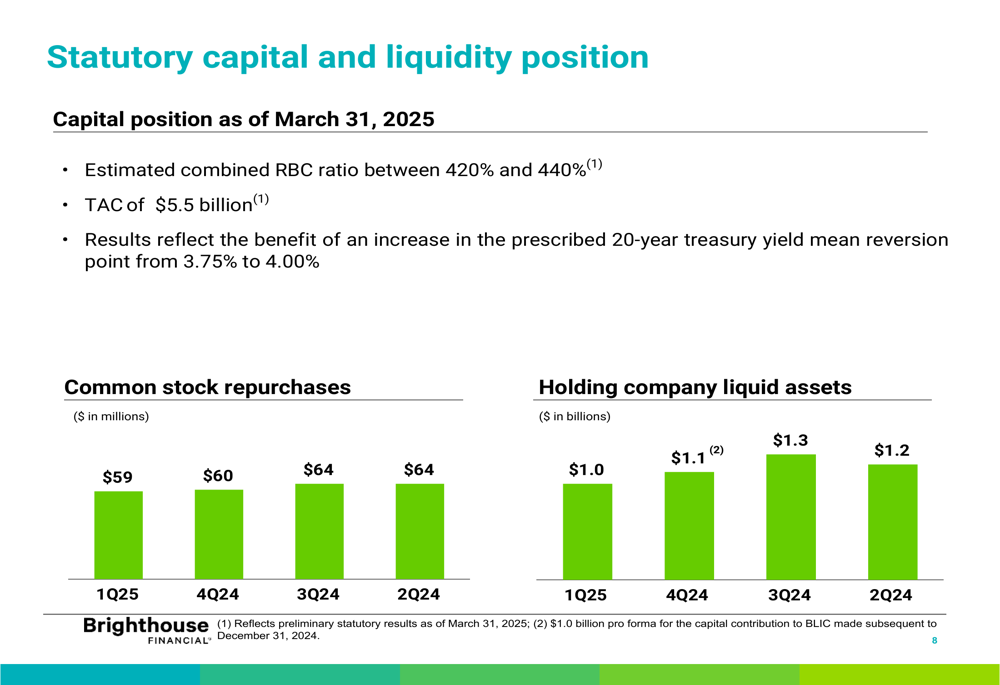

Brighthouse Financial maintained a strong capital position in Q1 2025, with an estimated combined risk-based capital (RBC) ratio between 420% and 440%, well above regulatory requirements. This represents a significant improvement from the 365-385% range reported in Q3 2024, indicating successful capital management efforts.

The company’s statutory total adjusted capital (TAC) stood at $5.5 billion, while holding company liquid assets were $1.0 billion as of March 31, 2025. These metrics reflect the company’s continued focus on maintaining financial flexibility.

The following chart shows the company’s capital and liquidity position:

Brighthouse continued its share repurchase program, buying back $59 million of common stock during Q1 2025, with an additional $26 million repurchased through May 6, 2025. This consistent approach to capital return aligns with the company’s previous quarters, where it repurchased $60 million, $64 million, and $64 million in Q4, Q3, and Q2 of 2024, respectively.

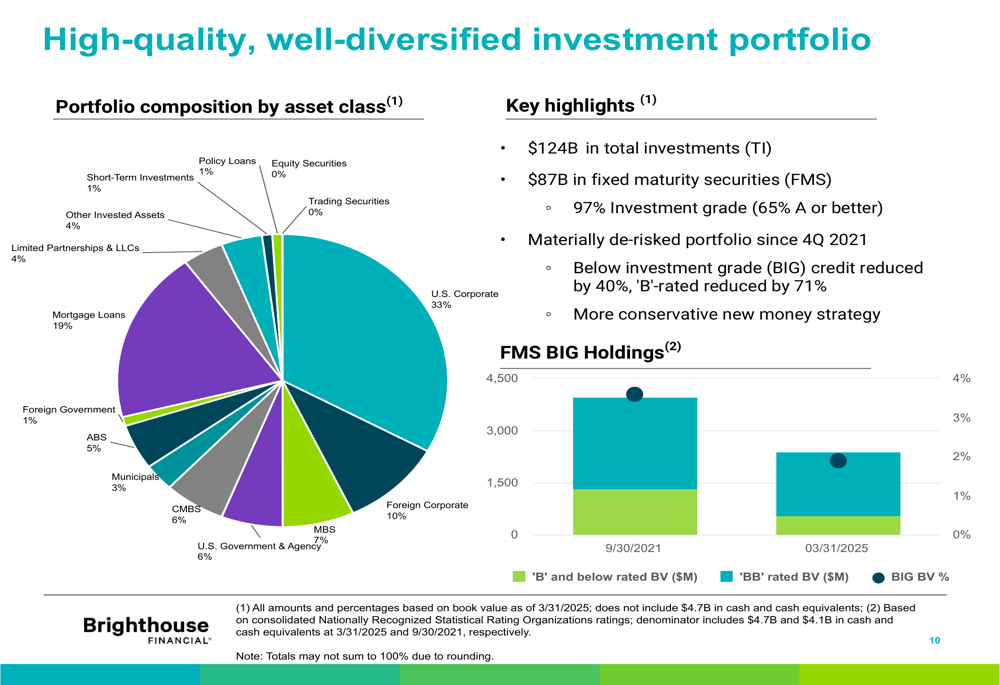

Investment Portfolio

Brighthouse Financial maintains a high-quality, well-diversified investment portfolio totaling $124 billion. Fixed maturity securities, which comprise the majority of the portfolio, are 97% investment grade, with 65% rated A or better.

The company’s investment portfolio composition is illustrated in the following chart:

The company has materially de-risked its portfolio since Q4 2021, reducing below investment grade credit exposure. This conservative approach is designed to provide stability during market fluctuations.

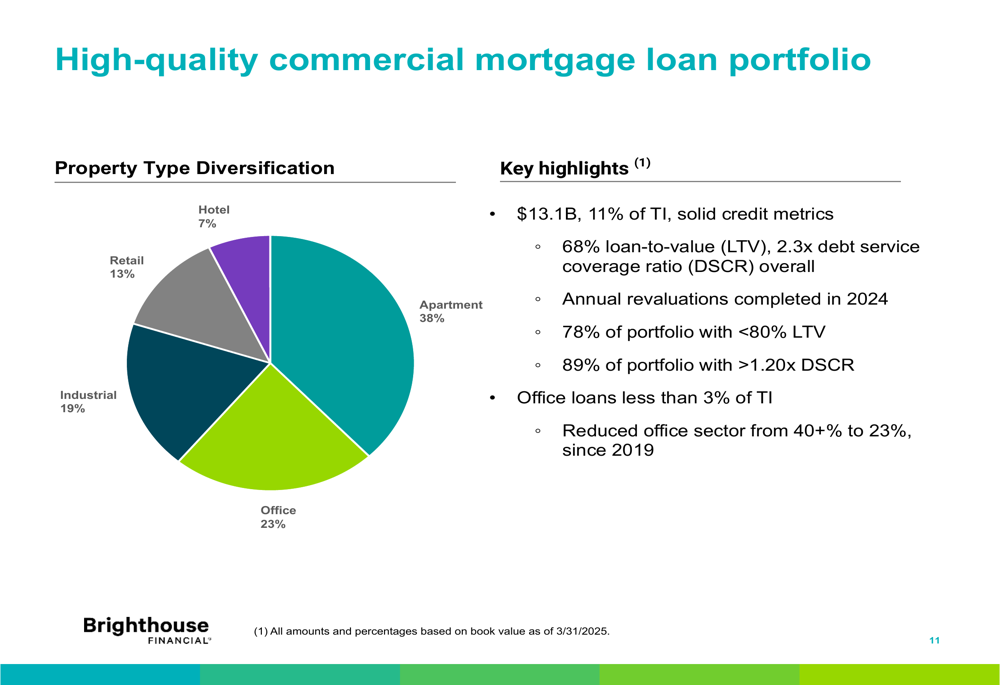

Brighthouse’s commercial mortgage loan portfolio, representing $13.1 billion or 11% of total investments, maintains solid credit metrics with a 68% loan-to-value ratio and 2.3x debt service coverage ratio. The company has strategically reduced its office sector exposure from over 40% to 23% since 2019, mitigating potential risks in the commercial real estate market.

The commercial mortgage loan portfolio diversification is shown here:

Forward-Looking Statements

While Brighthouse Financial did not provide specific earnings guidance for upcoming quarters, the company’s presentation emphasized its focus on maintaining capital strength and continuing share repurchases. The normalized statutory earnings of $0.3 billion in Q1 2025 suggest underlying business stability despite the volatility in reported net income.

The company’s alternative investment income yield of 1.4% in Q1 2025 fell significantly below its long-term expectation of 9-11% per year, indicating potential upside if these investments return to historical performance levels.

Brighthouse’s continued share repurchase activity signals management’s confidence in the company’s financial position and intrinsic value, even as it navigates the challenges of market volatility and segment-specific performance issues, particularly in its Life Insurance and Run-off businesses.

The detailed breakdown of adjusted earnings by segment provides insight into the company’s performance drivers:

As Brighthouse Financial moves forward in 2025, investors will likely focus on whether the company can maintain its strong capital position while improving performance in its underperforming segments and navigating ongoing market volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.