Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

BrightSpire Capital Inc (NYSE:BRSP) released its first quarter 2025 financial results on April 29, 2025, showing steady performance in a challenging real estate market. The commercial mortgage REIT maintained its quarterly dividend of $0.16 per share, representing an attractive 13.4% annualized yield based on current share prices. With a focus on floating-rate senior loans and a diversified portfolio, BrightSpire continues to navigate the commercial real estate landscape while trading at a significant discount to its book value.

Quarterly Performance Highlights

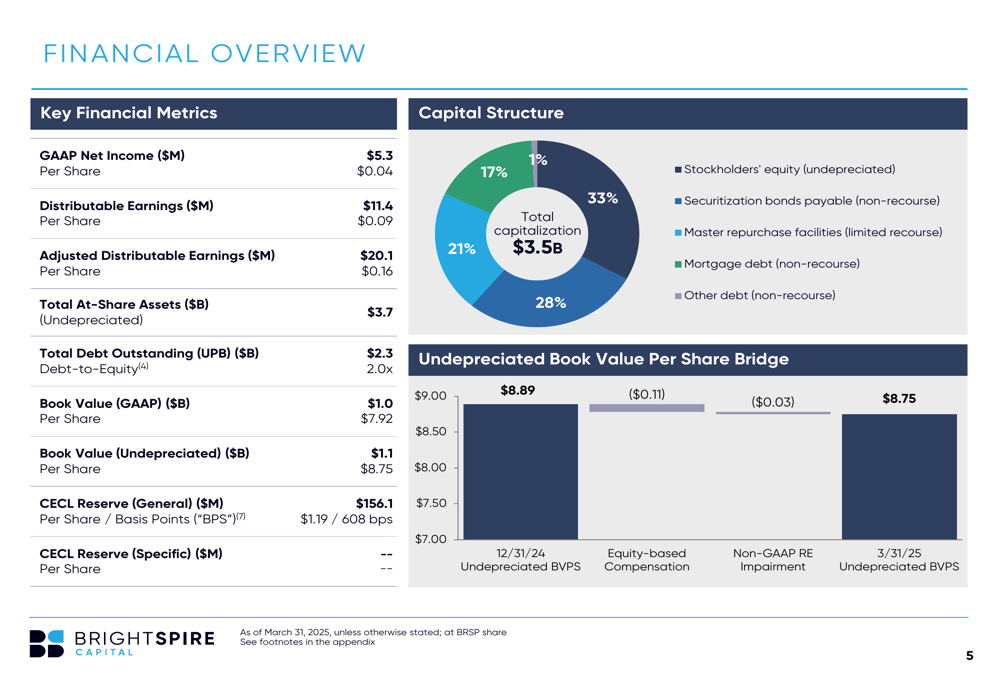

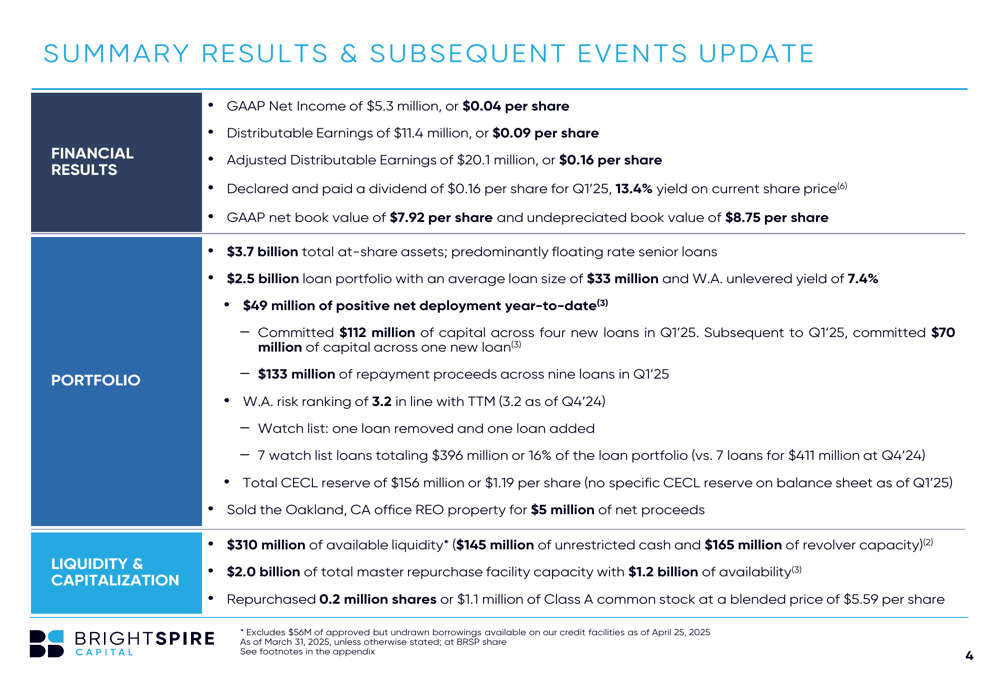

BrightSpire reported GAAP net income of $5.3 million ($0.04 per share) for Q1 2025, with distributable earnings of $11.4 million ($0.09 per share) and adjusted distributable earnings of $20.1 million ($0.16 per share). The company’s undepreciated book value stood at $8.75 per share, representing a slight decrease from $8.89 at the end of 2024.

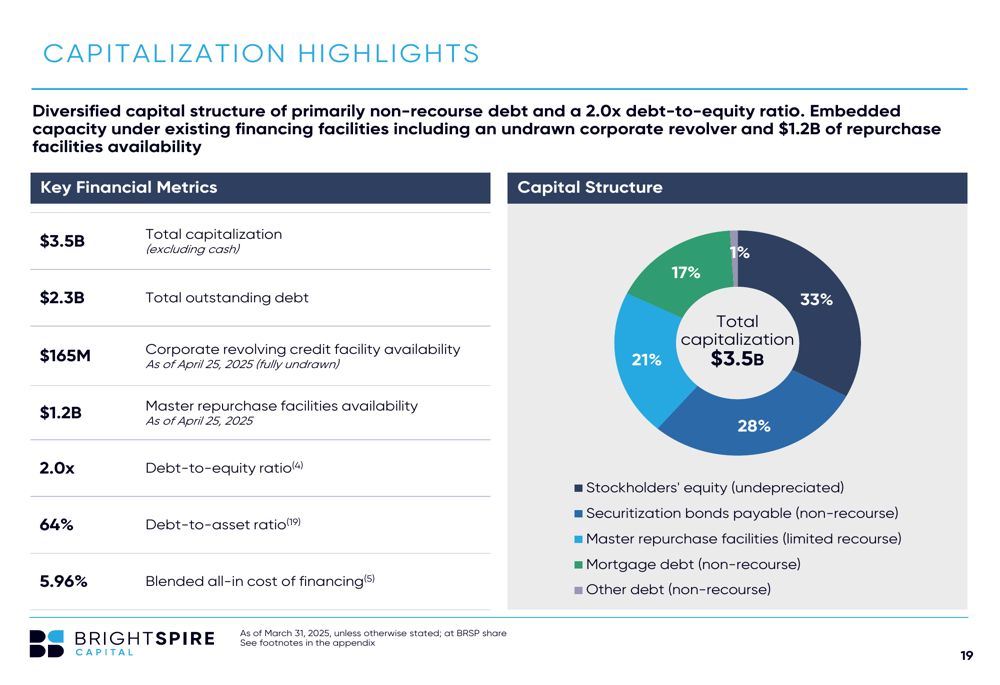

As shown in the following financial overview, BrightSpire maintains a diversified capital structure with a 2.0x debt-to-equity ratio:

The company committed $112 million of capital across four new loans during the quarter, while receiving $133 million in repayment proceeds from nine loans. Subsequent to quarter-end, BrightSpire committed an additional $70 million to one new loan. The company also completed the sale of its Oakland, CA office REO property for $5 million in net proceeds, continuing its strategy of optimizing its real estate portfolio.

The following slide highlights BrightSpire’s key metrics and subsequent events:

Portfolio Composition & Strategy

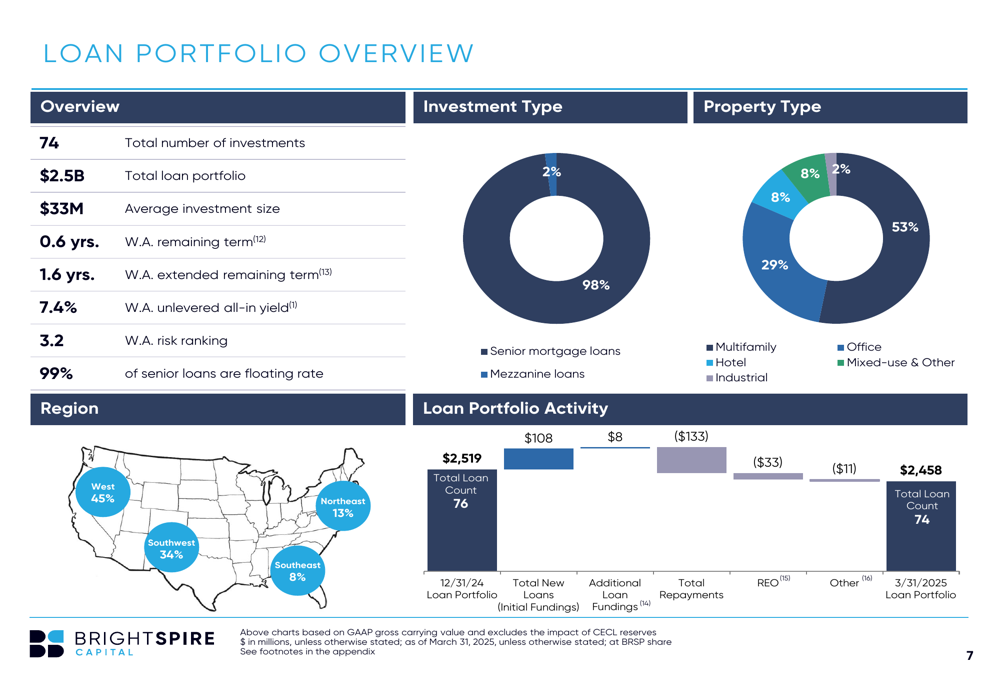

BrightSpire’s total at-share assets stood at $3.7 billion as of March 31, 2025, with a loan portfolio of $2.5 billion spread across 74 loans. The portfolio remains predominantly focused on floating-rate senior loans (97%), positioning the company well in the current interest rate environment. The average loan size is $33 million, with 86% of loans below $50 million, demonstrating the company’s focus on diversification.

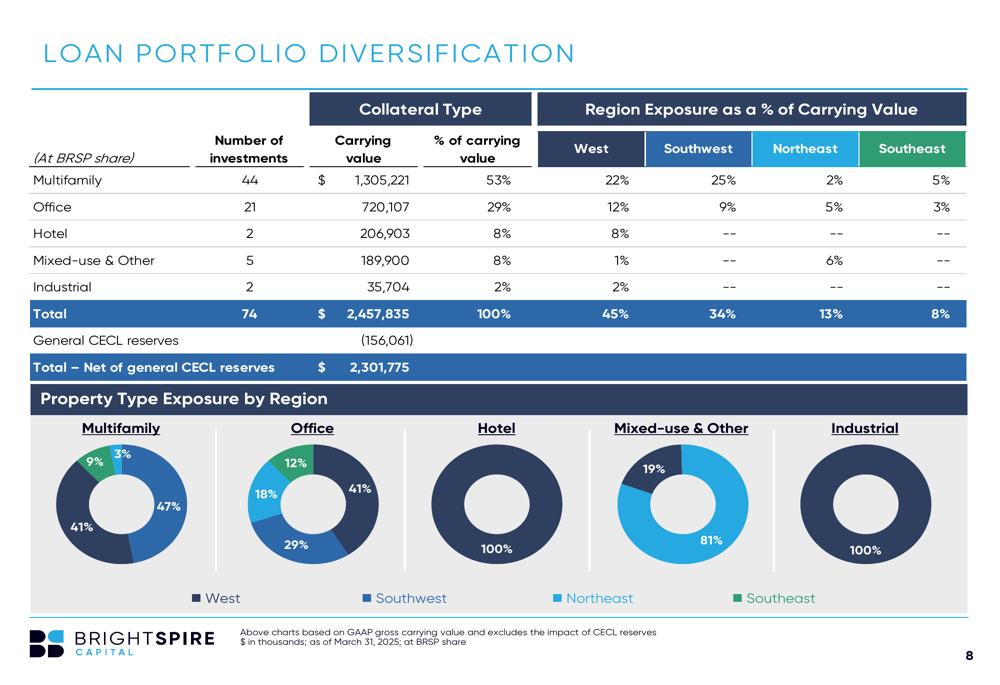

The company’s loan portfolio by property type shows a strong emphasis on multifamily (53%), with limited exposure to office properties (2%):

BrightSpire’s portfolio diversification by region and property type provides a balanced approach to commercial real estate lending:

The company’s watch list includes seven loans totaling $396 million, representing 16% of the loan portfolio, which is slightly down from $411 million in Q4 2024. The weighted average risk ranking remained stable at 3.2, indicating consistent credit quality quarter-over-quarter.

Liquidity & Capital Structure

BrightSpire maintained a strong liquidity position with $310 million available, consisting of $145 million in unrestricted cash and $165 million in undrawn corporate revolver capacity. The company also has $1.2 billion of availability under its master repurchase facilities.

The following slide details BrightSpire’s capitalization highlights:

The company’s debt-to-equity ratio stands at 2.0x, with a blended all-in cost of financing of 5.96%. BrightSpire’s capital structure includes 17% securitization bonds payable (non-recourse), 21% master repurchase facilities (limited recourse), 28% mortgage debt (non-recourse), 1% other debt (non-recourse), and 33% stockholders’ equity.

During the quarter, BrightSpire repurchased 0.2 million shares of Class A common stock for $1.1 million at a blended price of $5.59 per share, taking advantage of the significant discount to book value. The current share price of $5.05 represents approximately 58% of the undepreciated book value of $8.75 per share.

Interest Rate Sensitivity

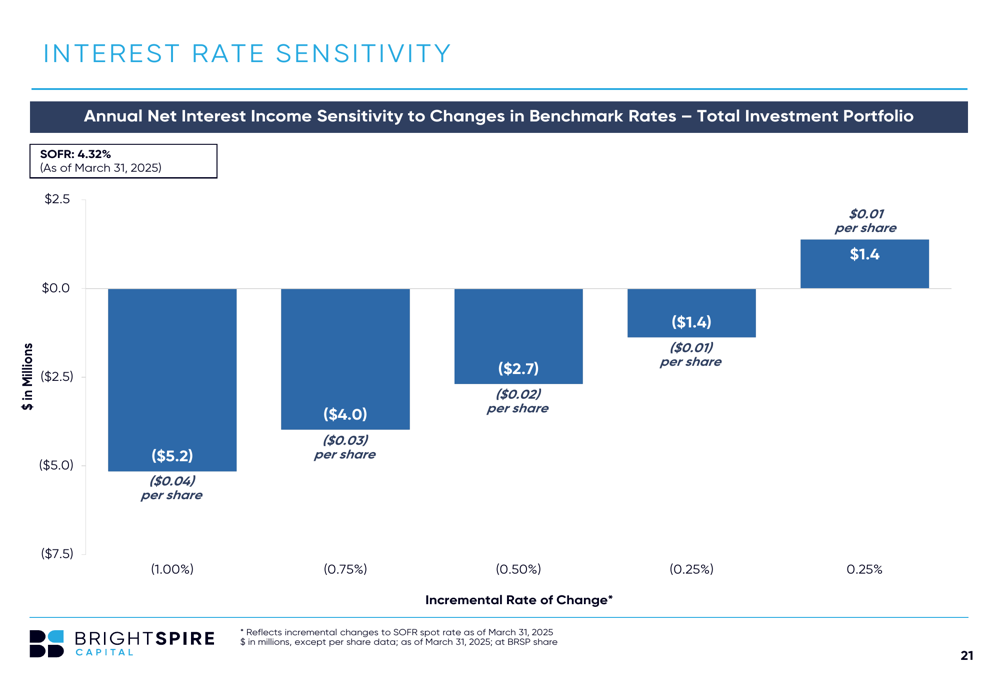

With 97% of the loan portfolio consisting of floating-rate loans, BrightSpire’s earnings are sensitive to changes in benchmark interest rates. The company’s analysis shows that a 25 basis point increase in rates would increase annual net interest income by $1.4 million ($0.01 per share), while a 25 basis point decrease would reduce it by $1.4 million ($0.01 per share).

The following slide illustrates BrightSpire’s interest rate sensitivity:

Forward-Looking Statements

BrightSpire continues to focus on maintaining portfolio stability while selectively pursuing growth opportunities. The company’s CECL reserve stands at $156.1 million ($1.19 per share), providing a buffer against potential credit issues. With no specific CECL reserves on the balance sheet as of Q1 2025, the company appears confident in its current portfolio quality.

Looking ahead, BrightSpire’s strategy involves:

1. Managing its existing portfolio with a focus on maximizing returns

2. Selectively originating new loans with attractive risk-adjusted returns

3. Optimizing its capital structure to enhance shareholder value

4. Continuing share repurchases at significant discounts to book value

This approach aligns with management’s previous statements from Q3 2024 about increasing the portfolio size to approximately $3.6 billion by the end of 2025, a target they have already exceeded with the current $3.7 billion portfolio.

Conclusion

BrightSpire Capital’s Q1 2025 results demonstrate steady performance in a challenging commercial real estate market. With adjusted distributable earnings covering the dividend, a stable risk profile, and strong liquidity position, the company appears well-positioned to navigate current market conditions. The significant discount to book value provides potential upside for investors, while the 13.4% dividend yield offers attractive income in the current environment.

Investors should monitor the company’s progress in managing its watch list loans and its ability to deploy capital into new opportunities with attractive risk-adjusted returns. As interest rates potentially begin to decline later in 2025, BrightSpire’s predominantly floating-rate loan portfolio could face some headwinds to net interest income, though this may be offset by increased transaction activity in the commercial real estate market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.