Top U.S. Defense Stocks to Watch According to Jefferies Analysis

Introduction & Market Context

Business First Bancshares, Inc. (NASDAQ:BFST) released its Q2 2025 presentation on July 28, 2025, highlighting the company’s financial performance and strategic initiatives. The Louisiana-headquartered bank reported continued growth across key metrics while advancing its acquisition strategy. The stock closed at $25.40, down 1.28% on the day, but remains well above its 52-week low of $20.07, reflecting overall investor confidence in the company’s direction.

Building on its Q1 2025 performance, when the bank beat earnings expectations with EPS of $0.65 versus a forecasted $0.61, Business First continues to demonstrate resilience in a competitive banking environment. The company maintains operations across Louisiana, Texas, and Mississippi, with Texas markets now representing 40% of its credit exposure.

Quarterly Performance Highlights

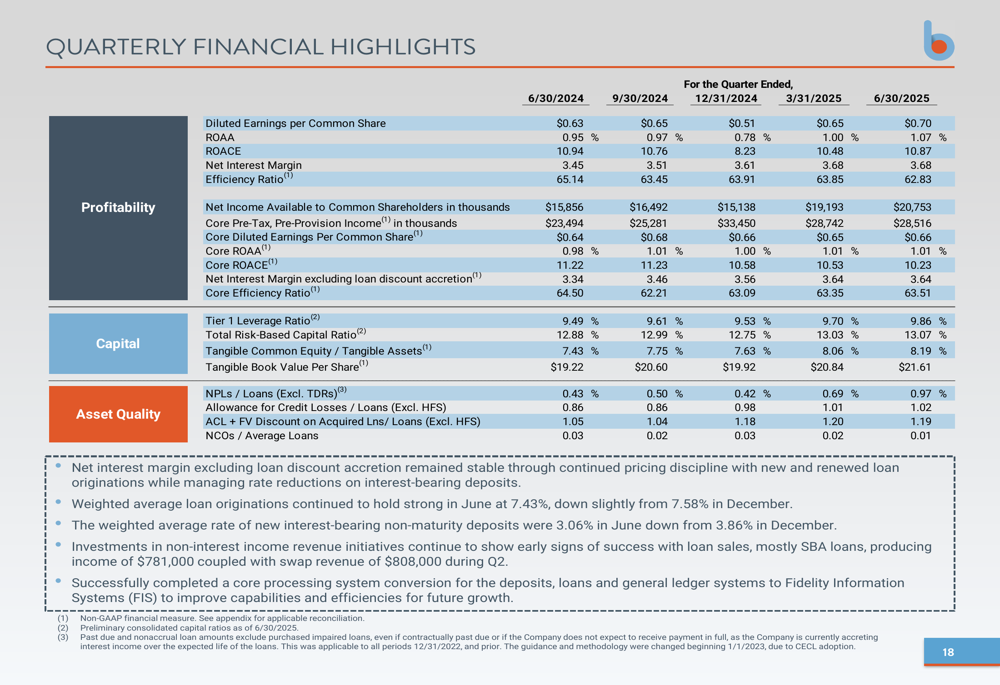

For Q2 2025, Business First reported solid financial results with net income available to common shareholders contributing to a return on average assets (ROAA) of 1.07% and return on average common equity (ROACE) of 10.87%. Core metrics showed similar strength, with core ROAA at 1.01% and core ROACE at 10.23%.

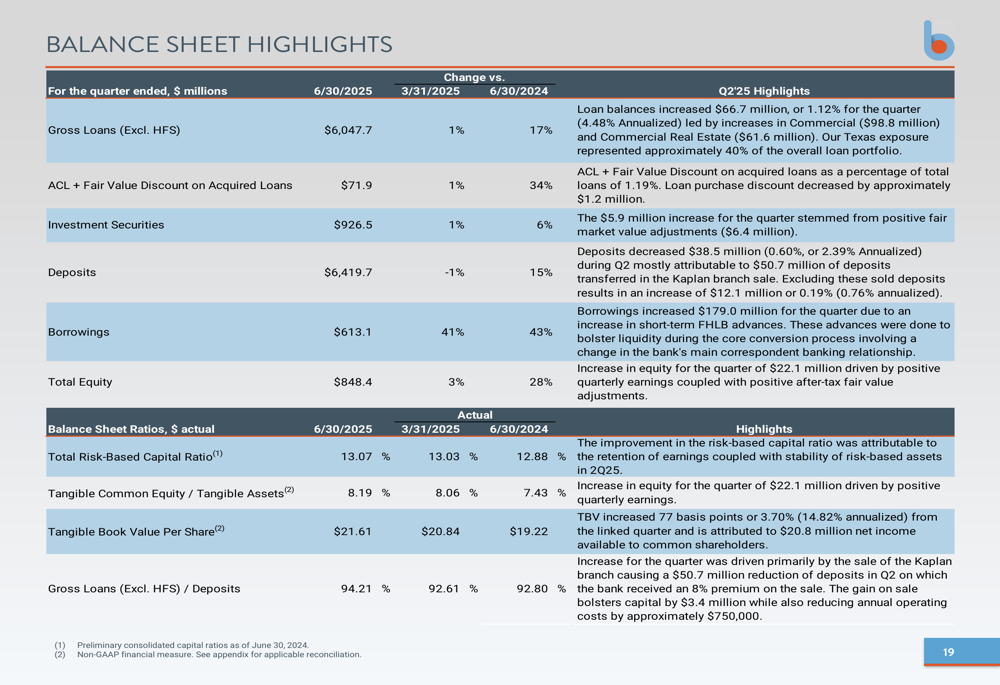

The company’s balance sheet expanded to $7.95 billion in assets, with gross loans of $6.05 billion and deposits of $6.42 billion, resulting in a loan-to-deposit ratio of 94.2%. Asset quality remained stable with non-performing loans to total loans at 0.97%, while capital ratios remained strong with a total risk-based capital ratio of 13.07% and tangible common equity to tangible assets at 8.19%.

As shown in the following quarterly financial highlights table, Business First has maintained consistent performance across key metrics:

The bank’s balance sheet highlights for Q2 2025 demonstrate year-over-year growth in most categories, with gross loans increasing 17% compared to Q2 2024 and deposits growing 15% over the same period:

Strategic Growth Initiatives

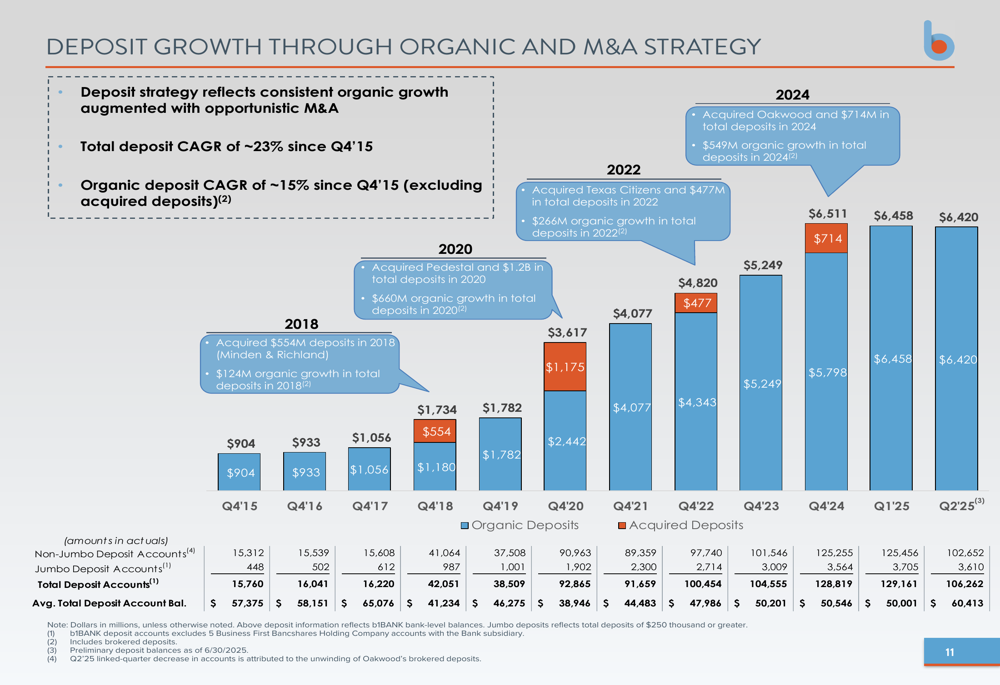

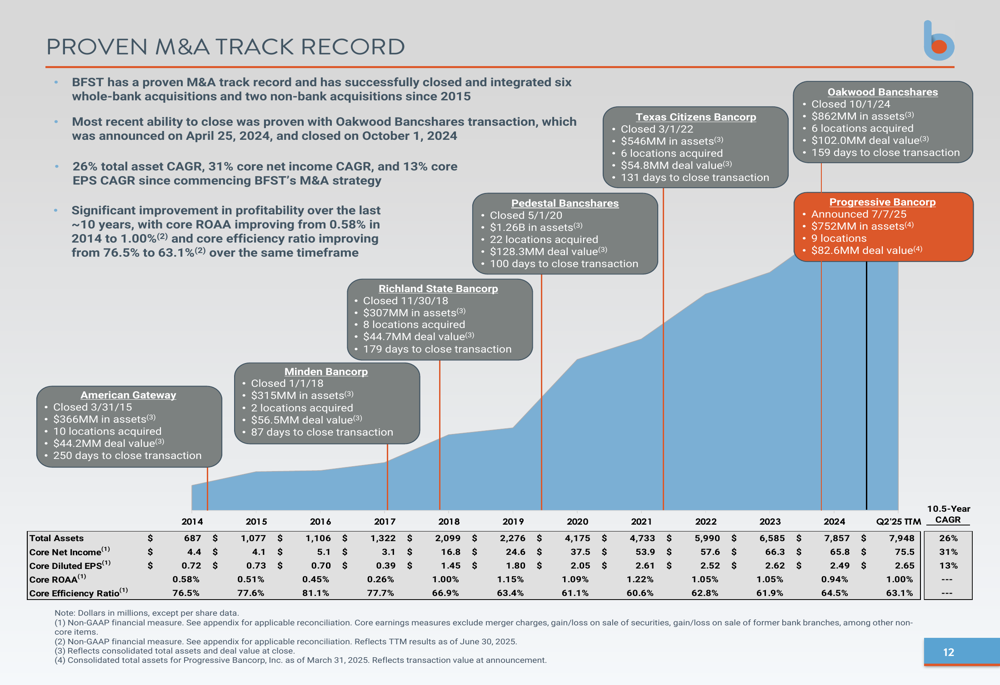

Business First’s growth strategy combines organic expansion with strategic acquisitions. The company has closed and integrated six whole-bank acquisitions and two non-bank acquisitions since 2015, most recently completing the Oakwood Bancshares transaction in October 2024 and announcing the Progressive Bancorp acquisition in July 2025.

This dual approach has yielded impressive results, as illustrated in the following deposit growth chart showing both organic and acquisition-driven expansion:

The company’s acquisition strategy has contributed significantly to its overall growth trajectory, with a 26% total asset CAGR, 31% core net income CAGR, and 13% core EPS CAGR over the past decade. The presentation highlights Business First’s proven M&A track record:

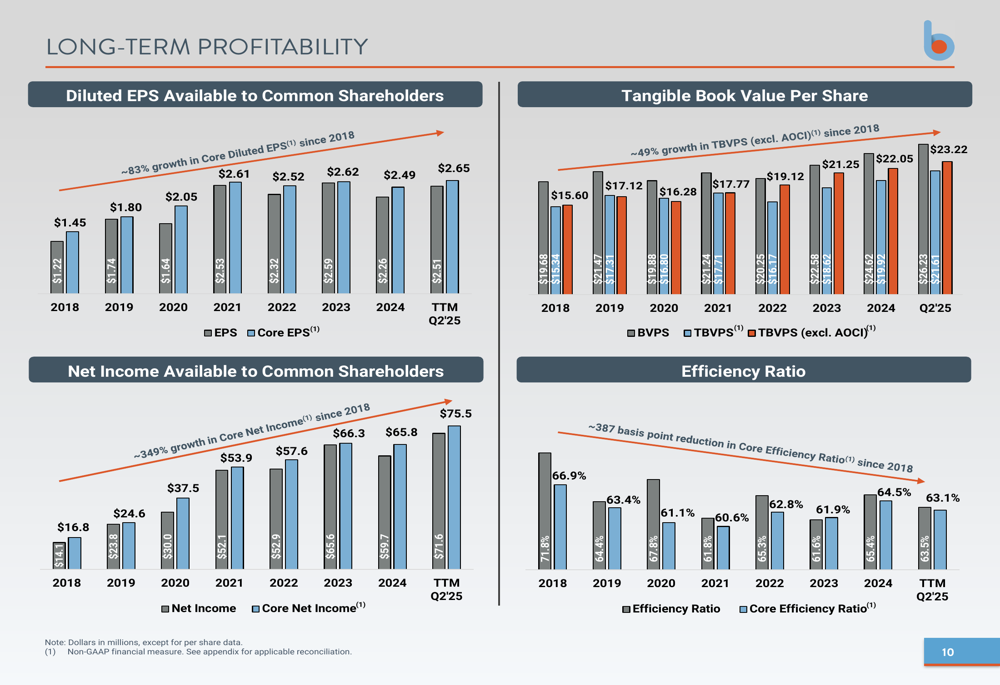

This strategic growth has translated into long-term profitability improvements across multiple metrics, including diluted EPS, tangible book value per share, net income, and efficiency ratio:

Balance Sheet Positioning

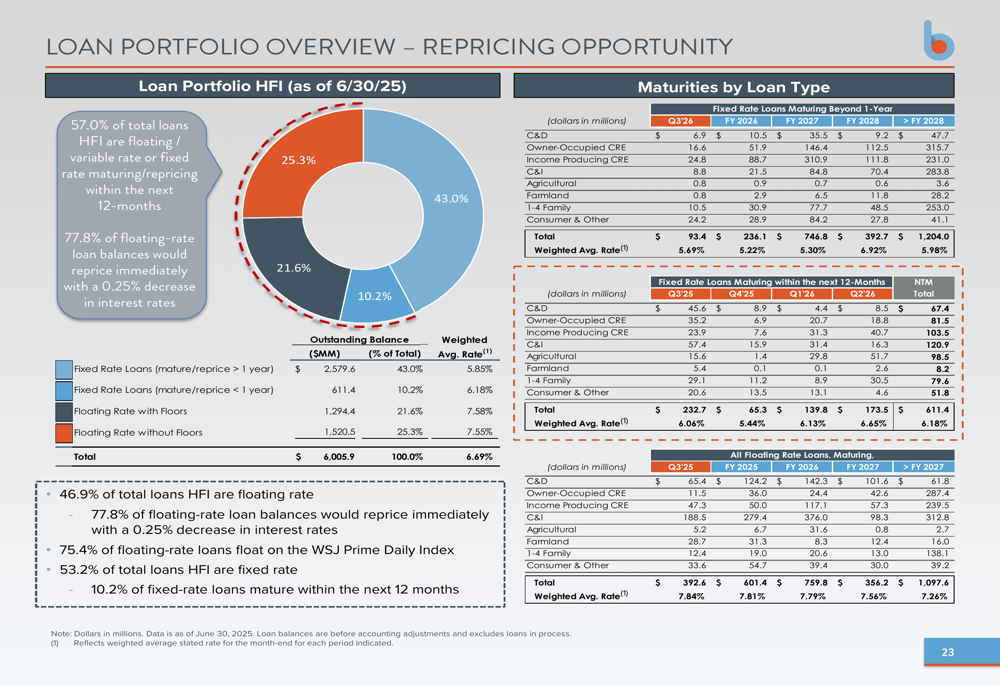

Business First has positioned its balance sheet to benefit from an anticipated easing rate environment. The company disclosed that 57% of its total loans held for investment are either floating/variable rate or fixed rate maturing/repricing within the next 12 months. Additionally, 77.8% of floating-rate loan balances would reprice immediately with a 0.25% decrease in interest rates.

The loan portfolio’s repricing opportunity is illustrated in the following breakdown:

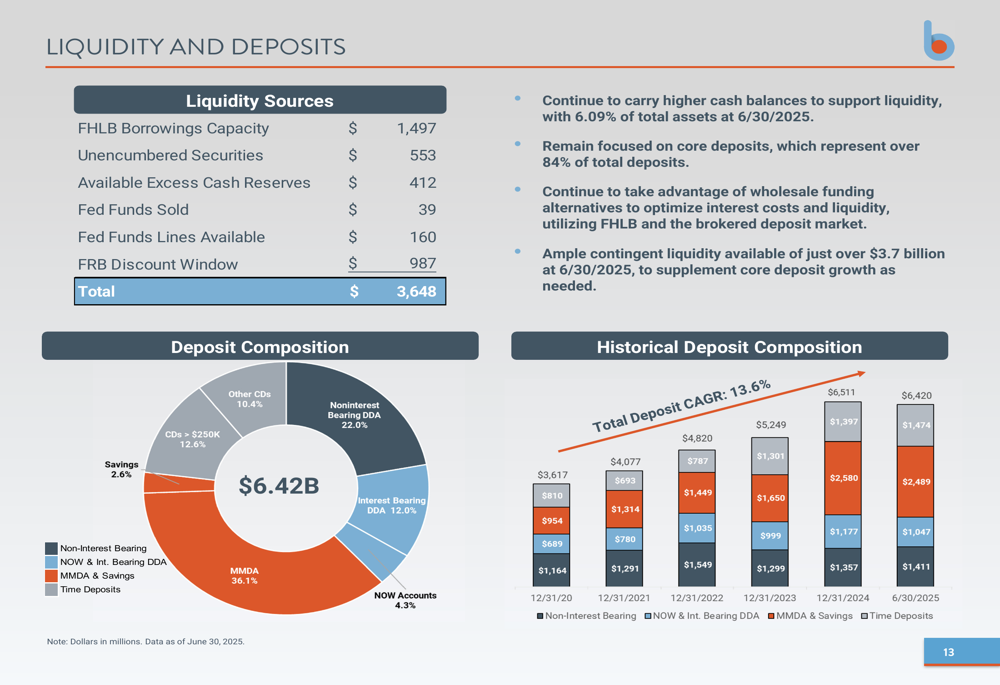

On the deposit side, Business First estimates its deposit beta in an easing rate cycle to be between 45% and 55%, aligning with the guidance provided in the Q1 earnings call. The company maintains ample liquidity with over $3.7 billion in available sources:

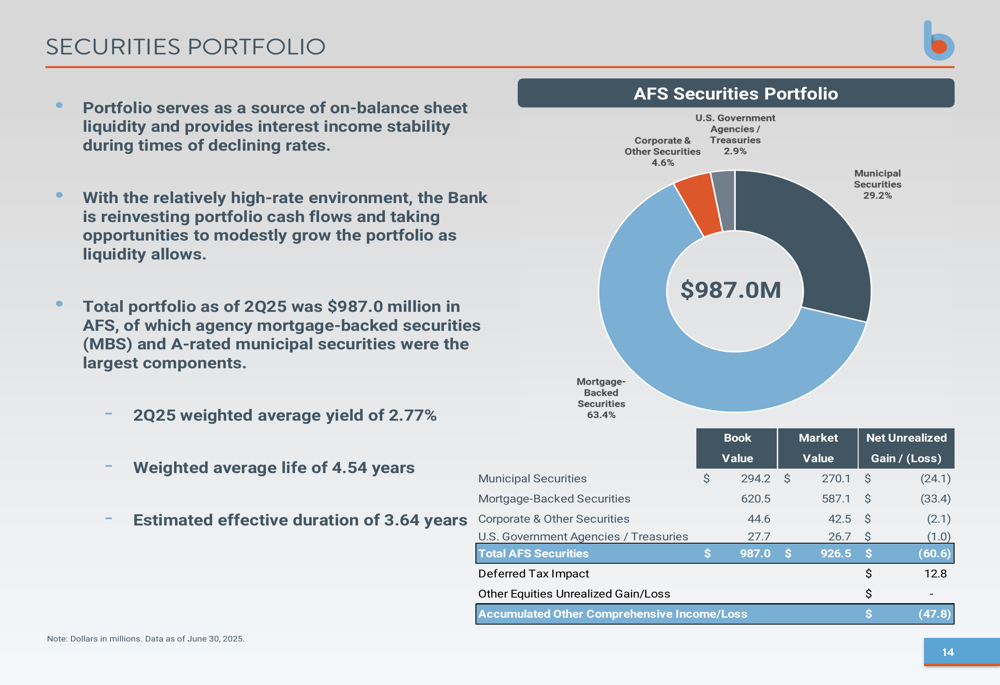

The securities portfolio totals $987.0 million with a weighted average yield of 2.77% and a weighted average life of 4.54 years. The portfolio composition is diversified across municipal securities, mortgage-backed securities, corporate securities, and government agencies:

Forward-Looking Statements

Looking ahead, Business First appears well-positioned for continued growth through both organic expansion and strategic acquisitions. The pending Progressive Bancorp acquisition is expected to further strengthen the company’s market position, particularly in its core Louisiana market where it already holds the #1 deposit market share among Louisiana-headquartered banks.

The company’s credit metrics remain stable, with consistent past due loan trends and nonperforming loans well managed. The allowance for credit losses plus fair value discount on acquired loans provides adequate coverage at 1.19% of total loans.

Business First’s diversified footprint across Louisiana and Texas markets offers protection against regional economic fluctuations, while its expanding noninterest revenue opportunities through its Financial Institutions Group, interest rate swaps, Smith Shellnut Wilson, and Waterstone LSP provide additional income streams beyond traditional banking.

The bank’s positioning for an easing rate environment, with a significant portion of its loan portfolio set to reprice in the coming months, could provide a competitive advantage if the Federal Reserve begins cutting interest rates as anticipated. This aligns with management’s Q1 2025 guidance suggesting that a 25 basis point rate cut could add 1-2 basis points to net interest margin.

As Business First continues to execute its growth strategy, investors will be watching closely to see if the company can maintain its momentum in deposit growth, loan origination, and successful integration of acquisitions while navigating the changing interest rate environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.