Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

CACI International Inc (NYSE:CACI) presented its third-quarter fiscal year 2025 results on April 24, 2025, highlighting strong performance across key metrics and an increasingly favorable budget environment. The company, which specializes in expertise and technology for national security, reported significant growth and raised its full-year guidance amid improving budget visibility and healthy demand signals in its focus areas.

The company’s executives, President and CEO John Mengucci and CFO Jeff MacLauchlan, emphasized CACI’s strategic alignment with administration priorities, particularly in software-defined systems and artificial intelligence applications for defense and intelligence.

Quarterly Performance Highlights

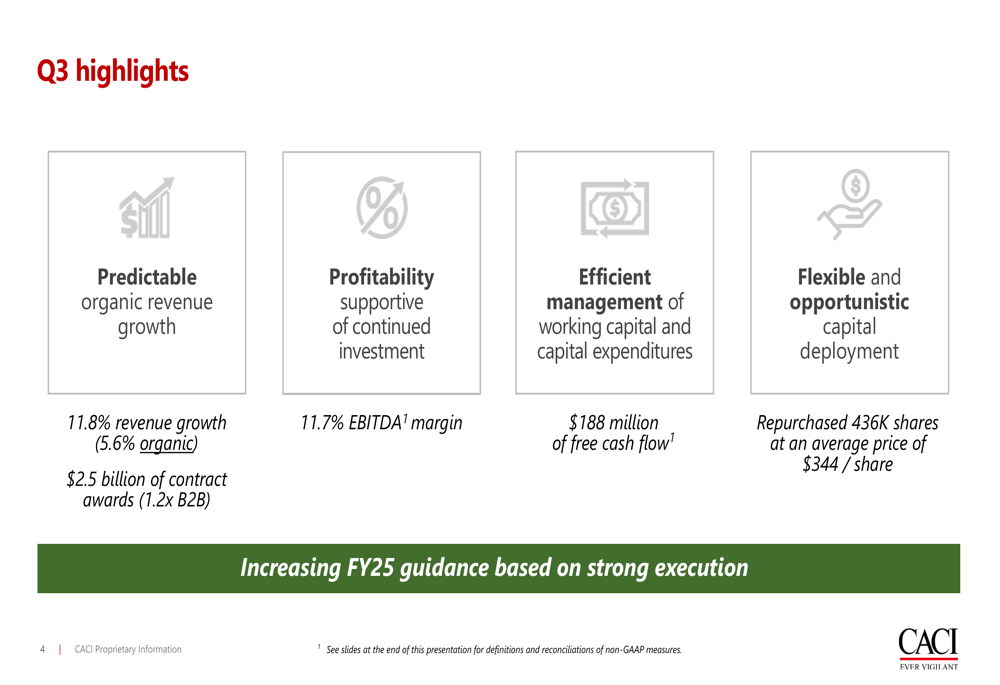

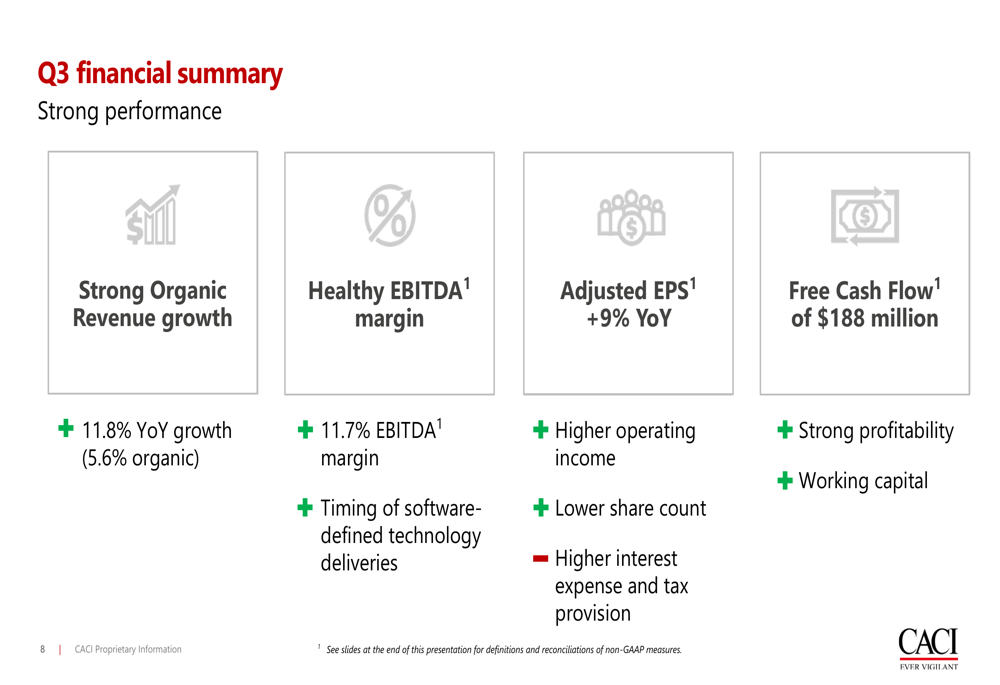

CACI delivered robust financial results in Q3 FY25, with revenue growth of 11.8% year-over-year, including 5.6% organic growth. The company secured $2.5 billion in contract awards, achieving a book-to-bill ratio of 1.2x, indicating strong future revenue potential. EBITDA margin reached 11.7%, supporting continued investments in strategic initiatives.

Free cash flow generation was particularly strong at $188 million, demonstrating efficient management of working capital and capital expenditures. The company also continued its shareholder return program, repurchasing 436,000 shares at an average price of $344 per share during the quarter.

CACI’s adjusted earnings per share increased 9% year-over-year, driven by higher operating income and a lower share count resulting from the company’s ongoing repurchase program. While these positive factors contributed to earnings growth, the company noted that higher interest expenses and tax provisions partially offset these gains.

Detailed Financial Analysis

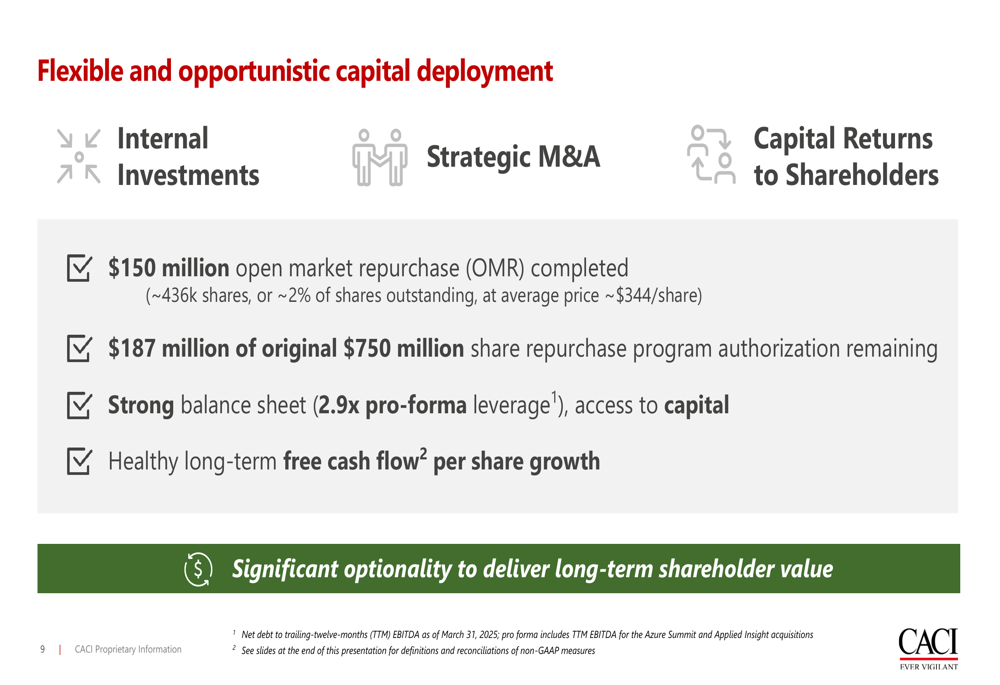

The company’s capital deployment strategy remains flexible and opportunistic, balancing internal investments, strategic M&A, and returns to shareholders. CACI completed a $150 million open market repurchase during the quarter and maintains $187 million of its original $750 million share repurchase authorization.

CACI’s financial position remains solid with a pro-forma leverage ratio of 2.9x, providing significant optionality for future capital allocation decisions. The company emphasized its focus on generating long-term shareholder value through consistent free cash flow per share growth.

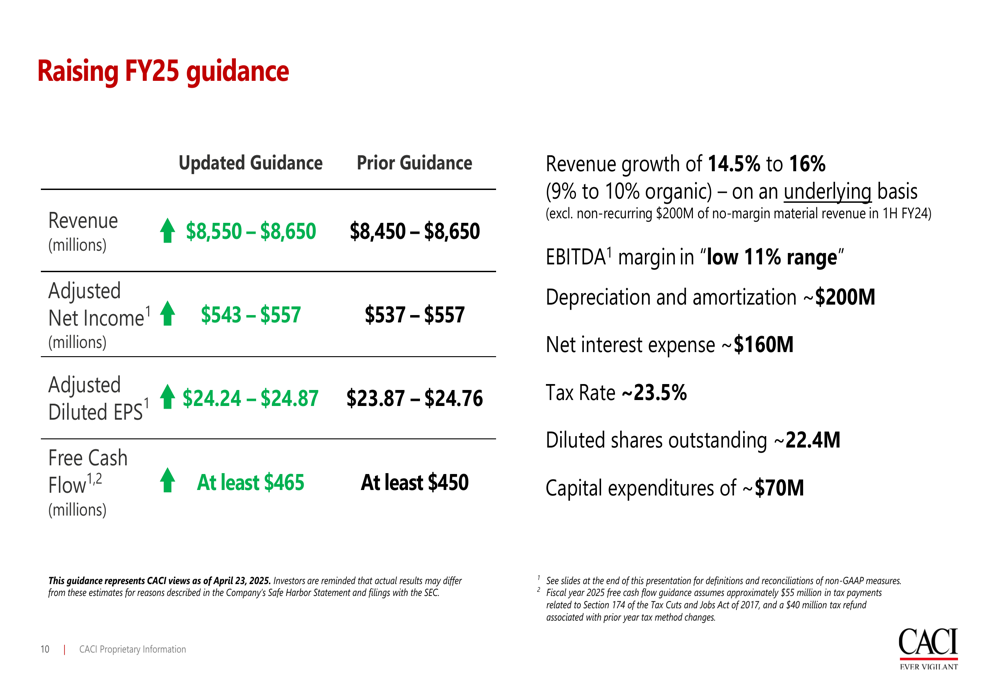

Based on the strong quarterly performance, CACI raised its full-year fiscal 2025 guidance across all key metrics. Revenue is now projected to be $8,550-$8,650 million, representing growth of 14.5-16%, up from the previous guidance of $8,450-$8,650 million. Adjusted net income is expected to be $543-$557 million, with adjusted diluted EPS of $24.24-$24.87, compared to prior guidance of $23.87-$24.76.

The company also increased its free cash flow guidance to at least $465 million, up from the previous estimate of at least $450 million. CACI expects to maintain EBITDA margins in the low 11% range, with approximately $200 million in depreciation and amortization, $160 million in net interest expense, and a tax rate of approximately 23.5%.

Strategic Initiatives

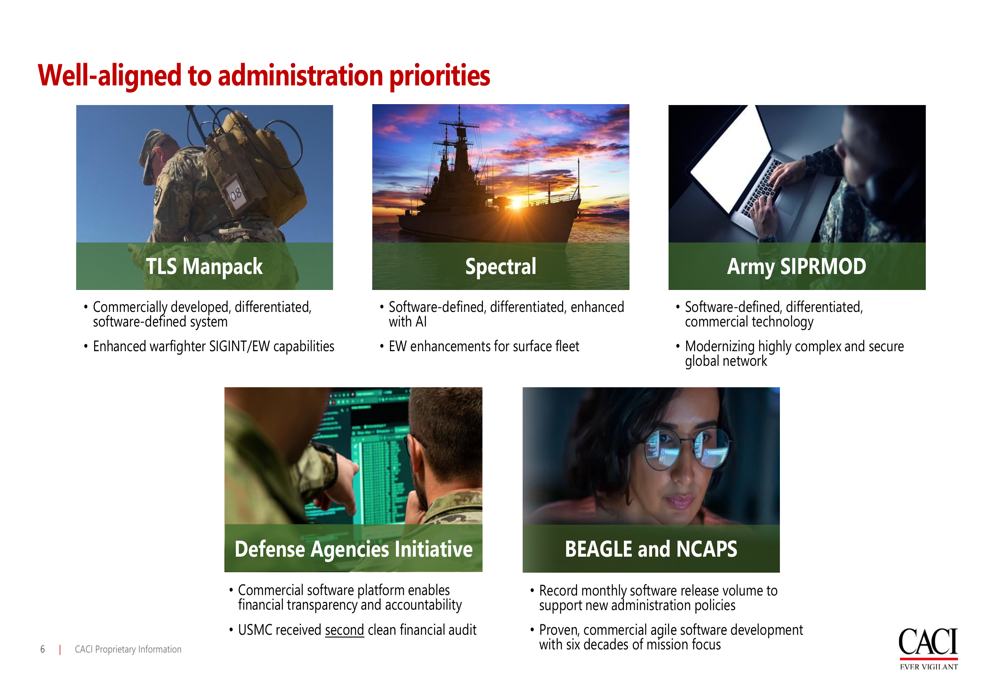

CACI highlighted its strong alignment with current administration priorities, showcasing several key products and services that demonstrate its strategic focus on software-defined systems enhanced with artificial intelligence capabilities.

The company’s portfolio includes the TLS Manpack, a commercially developed, software-defined system with enhanced warfighter SIGINT/EW capabilities; Spectral, a software-defined solution enhanced with AI for electronic warfare on surface fleets; and Army SIPRMOD, which uses software-defined commercial technology to modernize complex global networks.

Additionally, CACI’s Defense Agencies Initiative provides a commercial software platform enabling financial transparency, with the U.S. Marine Corps receiving its second clean financial audit. The company’s BEAGLE and NCAPS offerings feature high software release volumes and agile development methodologies built on decades of mission focus.

Forward-Looking Statements

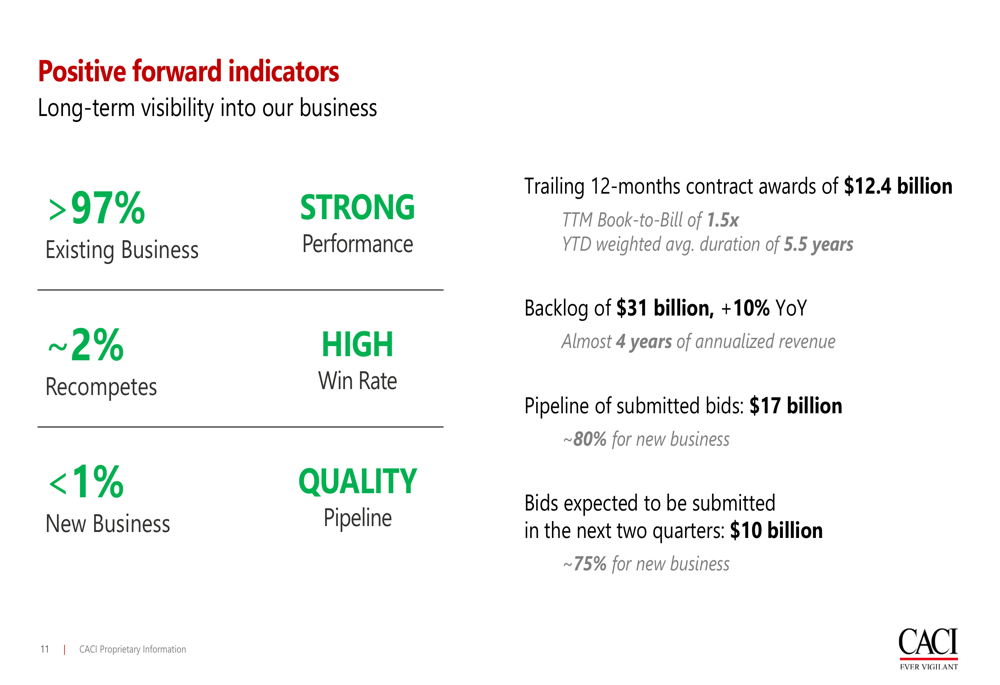

CACI’s forward indicators suggest continued strong performance, with over 97% of projected revenue coming from existing business, approximately 2% from re-competes, and less than 1% from new business. The company reported trailing 12-month contract awards of $12.4 billion and a total backlog of $31 billion, representing a 10% increase year-over-year.

The company’s pipeline remains robust, with $17 billion in submitted bids and an additional $10 billion expected to be submitted in the next two quarters. Management expressed confidence in the company’s three-year financial targets, citing strong execution of its strategy that is well-aligned with administration priorities.

In closing remarks, executives emphasized that CACI’s success is driven by its employees’ talent, innovation, and commitment, positioning the company to drive long-term growth, increase free cash flow per share, and generate sustainable shareholder value in an environment where national security priorities continue to receive bipartisan support.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.