U.S. stocks rise on Fed cut bets; earnings continue to flow

Introduction & Market Context

CACI International Inc (NYSE:CACI) presented its fourth quarter and full fiscal year 2025 results on August 7, 2025, highlighting strong performance across key metrics and providing an optimistic outlook for fiscal year 2026. The company, which specializes in national security and government services, reported significant growth driven by its strategic focus on software-defined capabilities in critical defense areas.

The presentation comes amid a constructive budget environment for defense contractors, with CACI noting it is well-positioned to address current geopolitical realities and administration priorities. The company expressed comfort operating in a continuing resolution environment, which could affect government funding in the short term.

CACI’s stock closed at $475.29 on August 6, 2025, up 0.8% for the day, and has traded between $318.60 and $588.26 over the past 52 weeks.

FY25 Performance Highlights

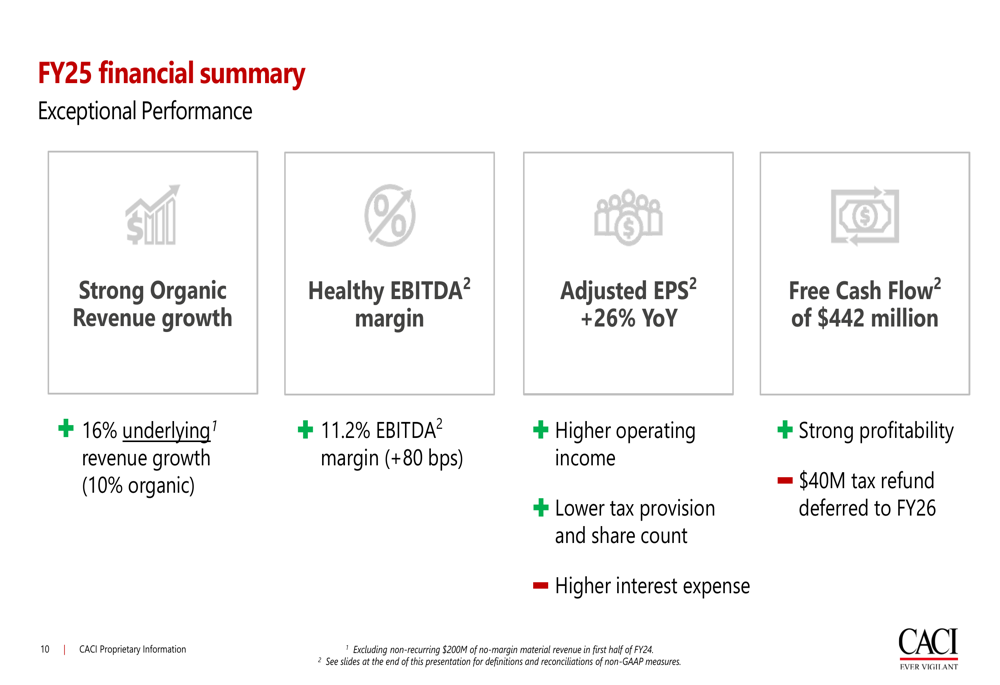

CACI reported exceptional financial performance for fiscal year 2025, with 16% underlying revenue growth (10% organic), excluding non-recurring revenue from the previous year. The company achieved an 11.2% EBITDA margin, representing an 80 basis point improvement year-over-year, while generating $442 million in free cash flow.

As shown in the following summary of FY25 results:

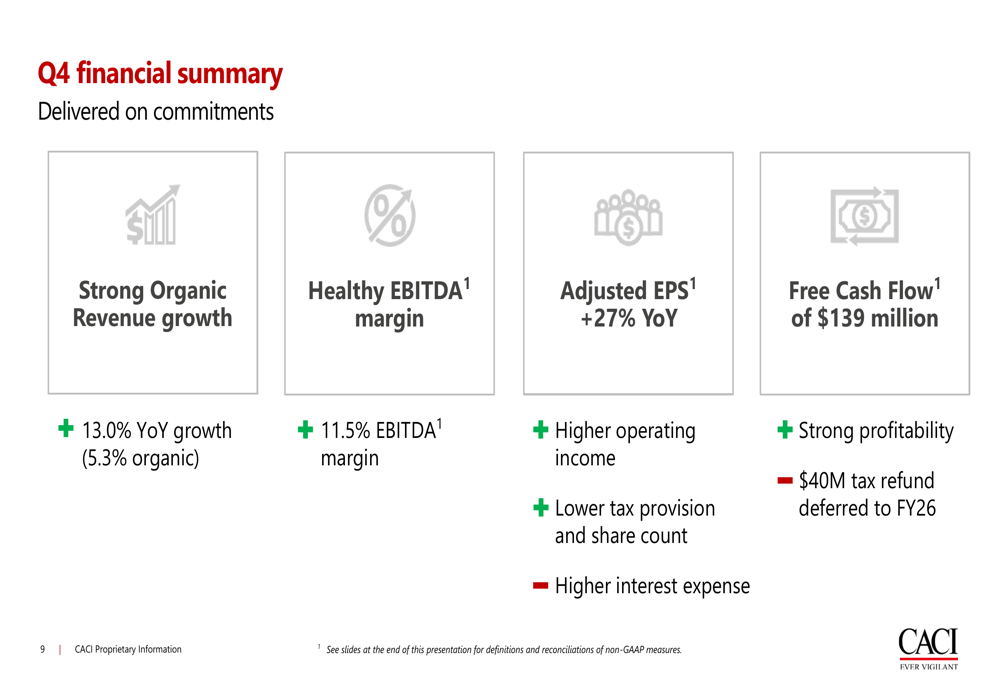

For the fourth quarter specifically, CACI delivered 13.0% year-over-year revenue growth (5.3% organic) and an 11.5% EBITDA margin. Adjusted earnings per share increased by 27% compared to the same quarter last year, with free cash flow of $139 million.

The quarterly performance details are illustrated here:

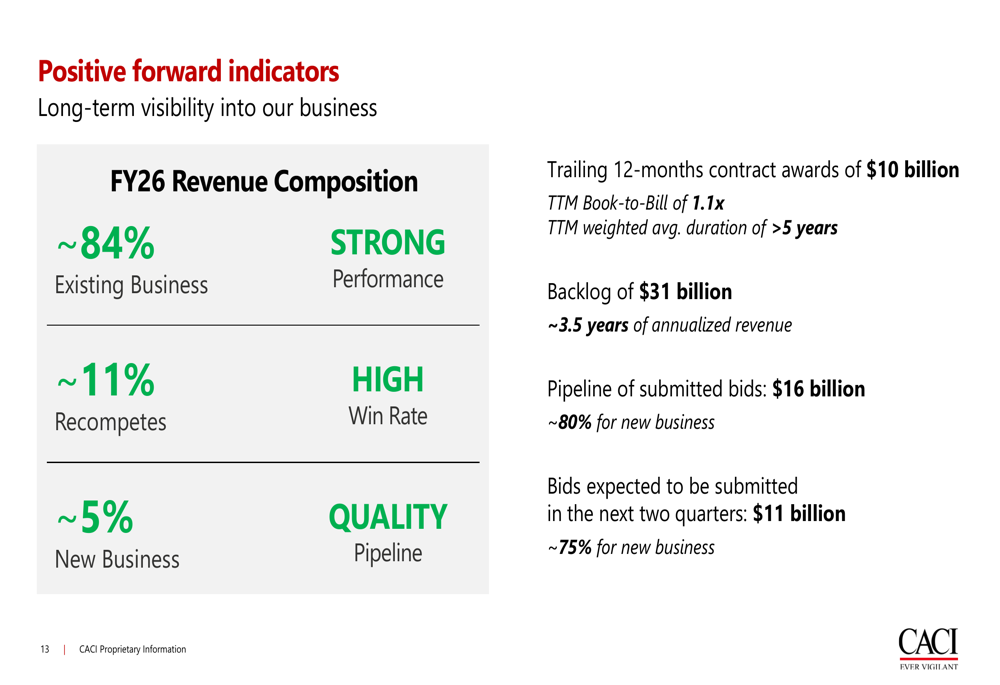

"FY25 success was driven by our strategy, differentiation, and resilience," noted John Mengucci, President and Chief Executive Officer, during the call. The company’s performance was supported by $10 billion in contract awards during the fiscal year, achieving a trailing twelve-month book-to-bill ratio of 1.1x.

Strategic Initiatives & Focus Areas

CACI highlighted three key strategic areas driving its growth: Electromagnetic Spectrum, Counter-UAS (Unmanned Aircraft Systems), and Software (ETR:SOWGn) Modernization. The company emphasized its leadership in commercially-developed software-defined technology, including the TLS Manpack system for Army Brigade Combat Teams.

The strategic focus areas and their market positioning are detailed in this slide:

In the Counter-UAS space, CACI noted increasing demand across defense, border security, and international markets. The company continues to invest ahead of customer needs, leveraging decades of experience and thousands of sensors deployed globally.

For Software Modernization, CACI is positioned to deliver additional efficiencies through legacy system consolidation, employing commercial software development processes including Agile and DevSecOps methodologies. The company highlighted that its NCAPS program is ramping up successfully, meeting all key system availability metrics.

FY26 Guidance & Outlook

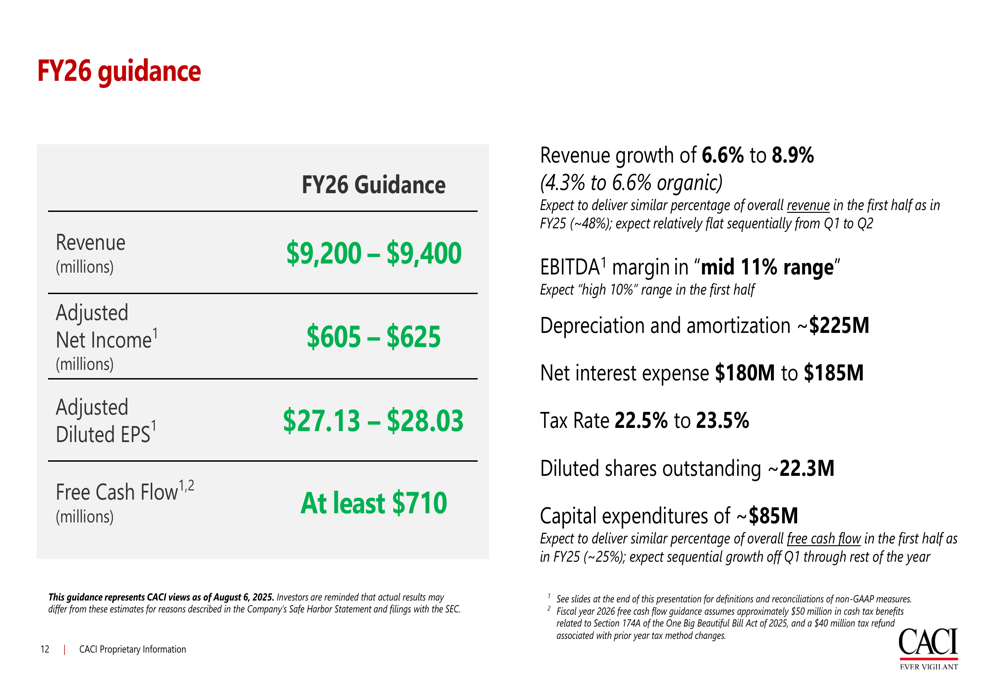

Looking ahead to fiscal year 2026, CACI provided optimistic guidance, projecting revenue between $9.2 billion and $9.4 billion, representing growth of 6.6% to 8.9% (4.3% to 6.6% organic). The company expects adjusted net income of $605-$625 million and adjusted diluted EPS of $27.13-$28.03.

The detailed FY26 guidance is presented here:

Most notably, CACI projects free cash flow of at least $710 million for FY26, representing growth of more than 60% compared to FY25. The company expects EBITDA margin to be in the "mid 11% range," continuing the positive trend from FY25.

CACI’s outlook for FY26 is supported by strong forward indicators, including a backlog of $31 billion (approximately 3.5 years of annualized revenue) and a robust pipeline of submitted bids totaling $16 billion, with approximately 80% for new business.

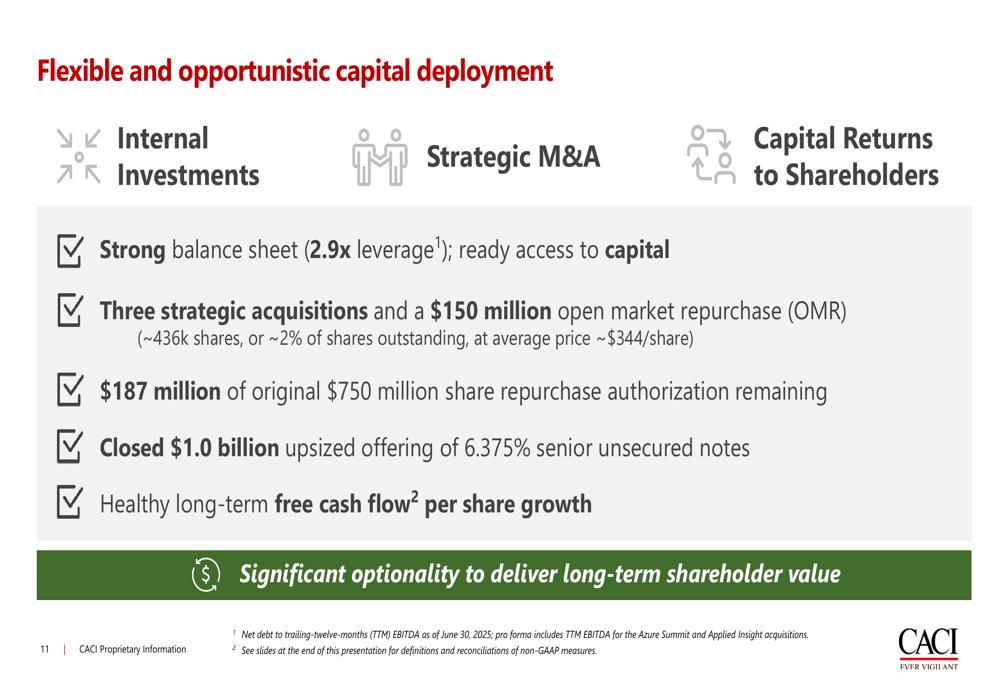

Capital Allocation & Financial Position

CACI maintained a strong balance sheet with 2.9x leverage and demonstrated a flexible capital deployment strategy throughout FY25. The company completed three strategic acquisitions and repurchased approximately 436,000 shares at an average price of $344 per share, representing about 2% of shares outstanding.

The company’s capital deployment approach is illustrated in this slide:

CACI closed a $1.0 billion upsized offering of 6.375% senior unsecured notes during the fiscal year and has $187 million remaining from its original $750 million share repurchase authorization. Management emphasized that this provides "significant optionality to deliver long-term shareholder value."

For FY26, CACI expects capital expenditures of approximately $85 million, a tax rate between 22.5% and 23.5%, and diluted shares outstanding of approximately 22.3 million.

The company also highlighted a favorable resolution of an R&D audit settlement, resulting in a current period benefit of $28 million to net income in FY25, and noted that a $40 million tax refund has been deferred to FY26, which will positively impact cash flow in the coming fiscal year.

Forward-Looking Statements

CACI expressed continued confidence in its three-year financial targets, citing a robust pipeline, business momentum, and a constructive macroeconomic environment. The company emphasized that its success is driven by its employees’ talent, innovation, and commitment.

With approximately 84% of projected FY26 revenue already secured through existing business, CACI appears well-positioned to deliver on its guidance. The company’s focus on software-based capabilities and investments ahead of customer needs continues to be a key differentiator in the competitive defense and national security markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.