Google launches Gemini Enterprise AI platform for workplace automation

Introduction & Market Context

Construcciones y Auxiliar de Ferrocarriles SA (BME:CAF) released its first-half 2025 results on July 28, showing substantial growth in order intake and profitability despite a challenging macroeconomic environment. The Spanish train and bus manufacturer reported a 40% increase in net profit as its zero-emission bus business experienced unprecedented demand.

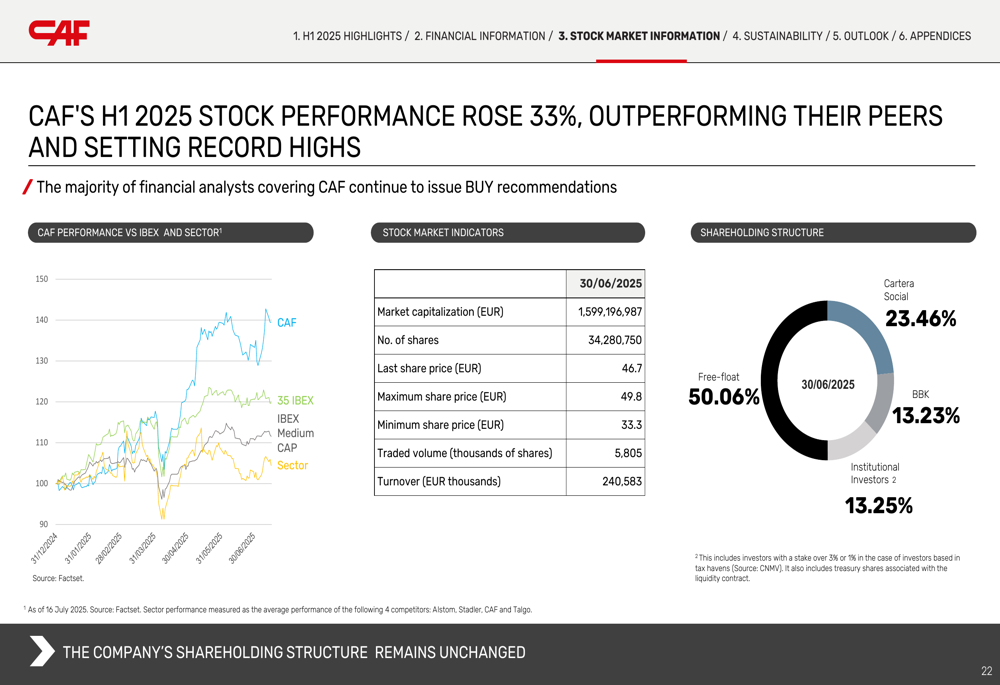

CAF’s stock has performed exceptionally well during the first half of 2025, rising 33% and outperforming industry peers. The company’s share price closed at €54 on the presentation day, near its 52-week high of €55.70, reflecting investor confidence in CAF’s growth strategy and execution.

As shown in the following chart of CAF’s stock performance during H1 2025:

Quarterly Performance Highlights

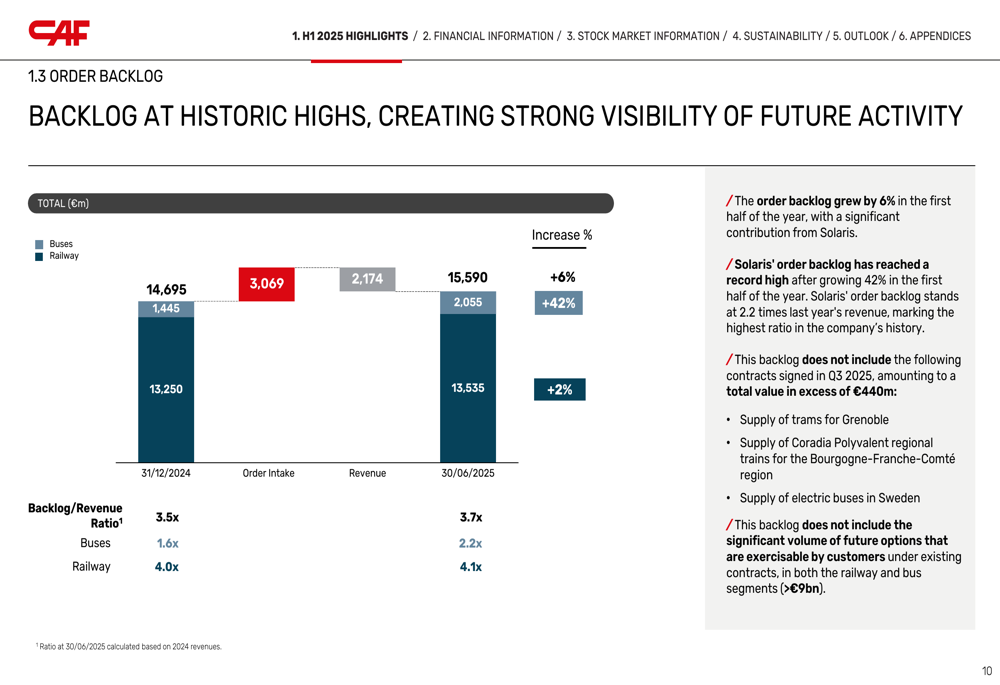

CAF reported strong financial results for H1 2025, with significant improvements across key metrics. Order intake surged 78% year-over-year to €3,069 million, while the backlog grew 6% from December 2024 to reach a historic high of €15,590 million, providing strong visibility for future revenue.

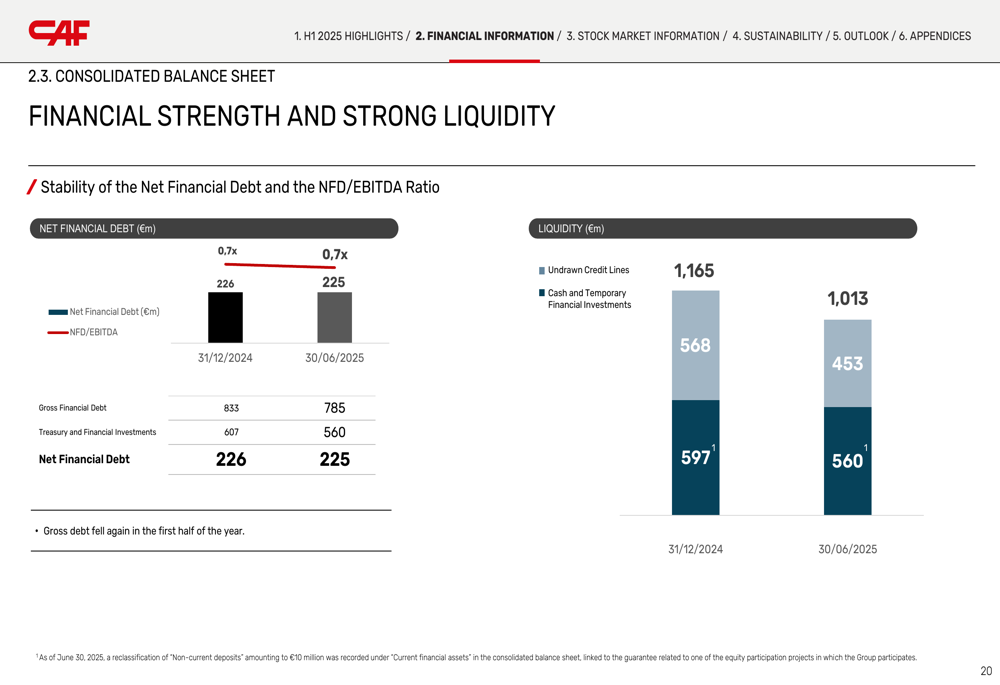

Revenue increased by 4% to €2,174 million, with operating profit (EBIT) rising 12% to €114 million. The EBIT margin expanded by 0.3 percentage points to 5.2%, and net attributable profit jumped 40% to €73 million. The company maintained a solid financial position with a net financial debt to EBITDA ratio of 0.7x.

The following slide summarizes CAF’s key financial figures for H1 2025:

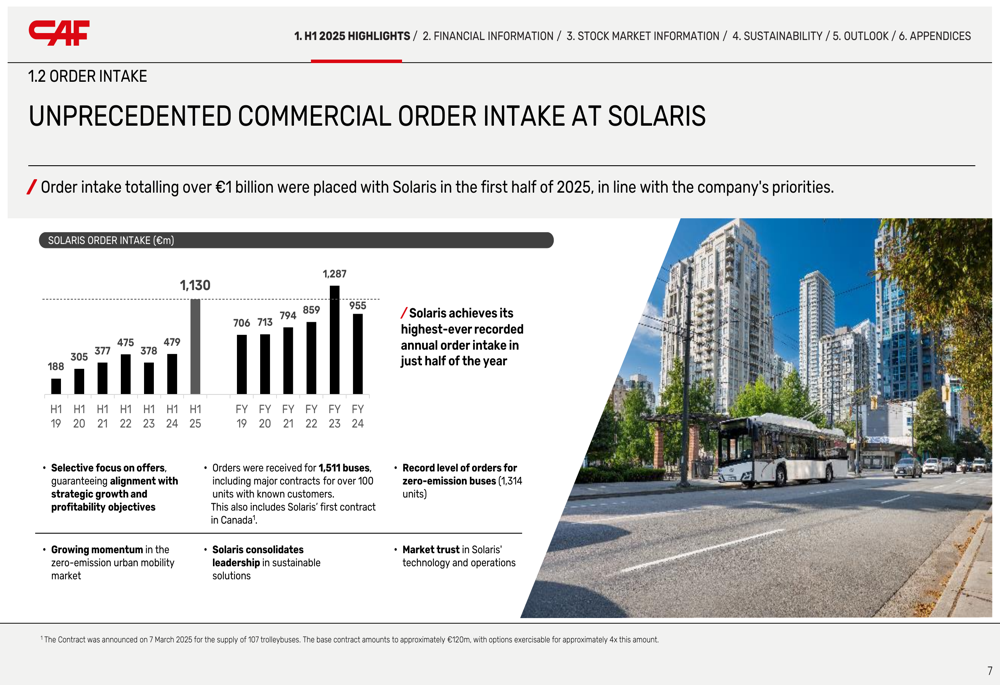

The company’s order intake was particularly strong in the bus segment, where Solaris (CAF’s bus subsidiary) achieved its highest-ever recorded annual order intake in just half a year, exceeding €1 billion. Rail services also performed exceptionally well, with order intake reaching €888 million, representing a book-to-bill ratio of 2.4x.

As illustrated in this chart showing Solaris’ unprecedented order intake:

Detailed Financial Analysis

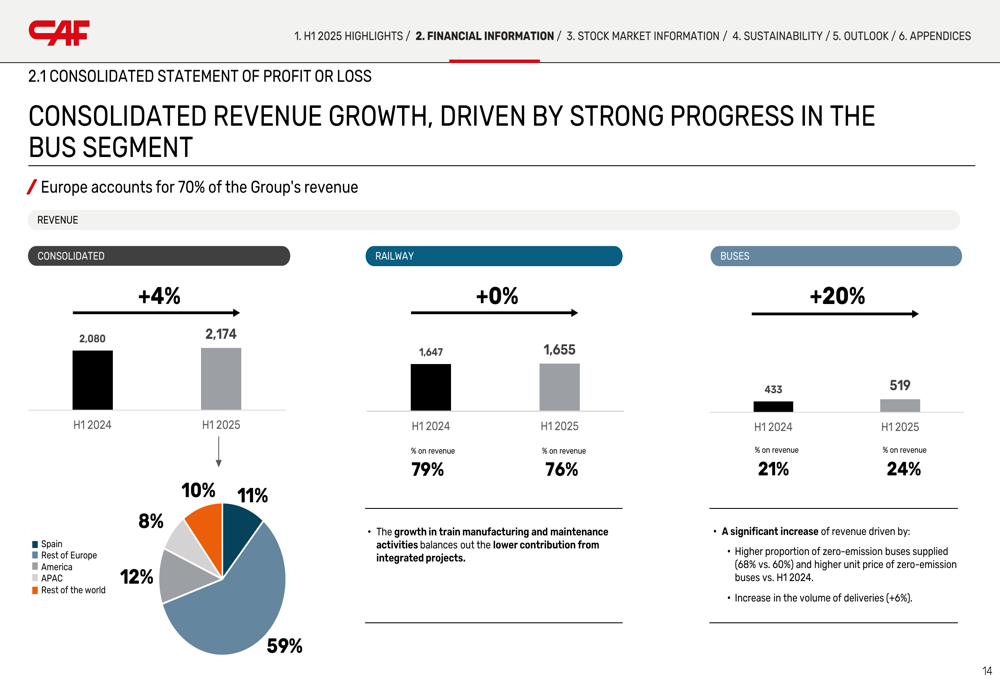

CAF’s consolidated revenue growth of 4% was primarily driven by its bus segment, which grew 20% year-over-year to €519 million. The railway segment remained flat at €1,655 million, with growth in maintenance activities offsetting lower contributions from integrated projects.

The following breakdown shows the consolidated revenue growth by segment:

Within the railway segment, rolling stock revenue increased by 4% to €952 million, while services grew 16% to €365 million. However, integrated solutions and systems revenue declined by 19% to €338 million due to lower contribution from turnkey projects during the period.

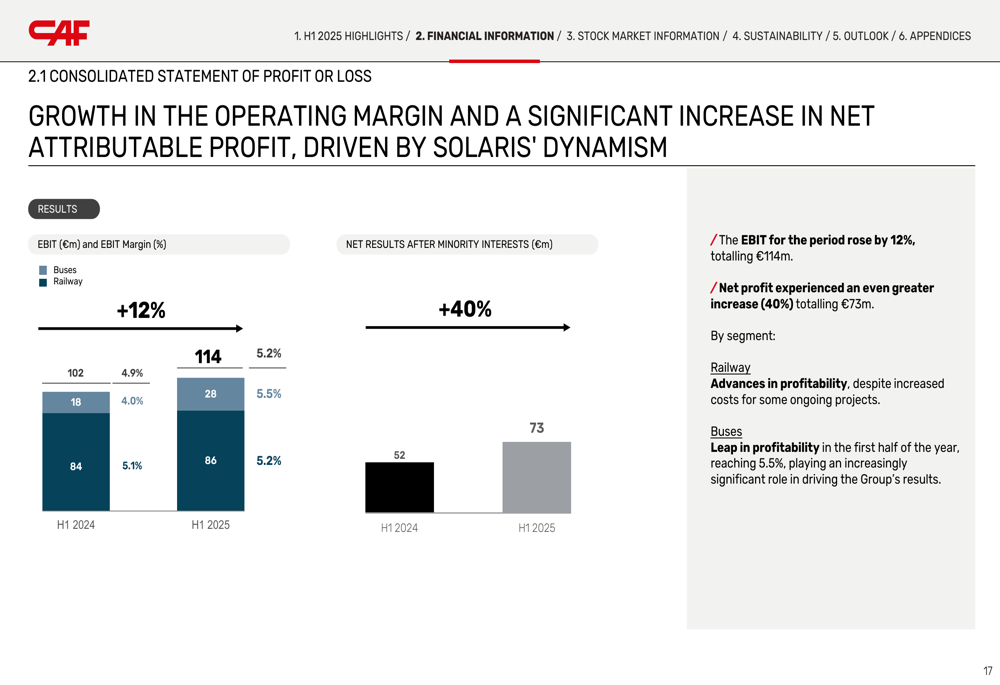

Profitability improved significantly, with EBIT margin expanding to 5.2% despite increased costs. The bus segment showed a remarkable improvement in profitability, reaching a 5.5% margin compared to 4.0% in H1 2024, playing an increasingly significant role in the group’s overall performance.

The following chart illustrates the growth in operating margin:

Cash flow generation was neutral at €0.3 million, primarily due to an increase in working capital. EBITDA of €165 million was offset by working capital changes (-€88 million), CAPEX payments (-€28 million), financial payments (-€11 million), and tax payments (-€37 million).

The company maintained a strong financial position with stable net financial debt of €225 million and available liquidity of €1,165 million, including undrawn credit lines and cash.

As shown in this slide detailing the company’s financial strength:

Strategic Initiatives

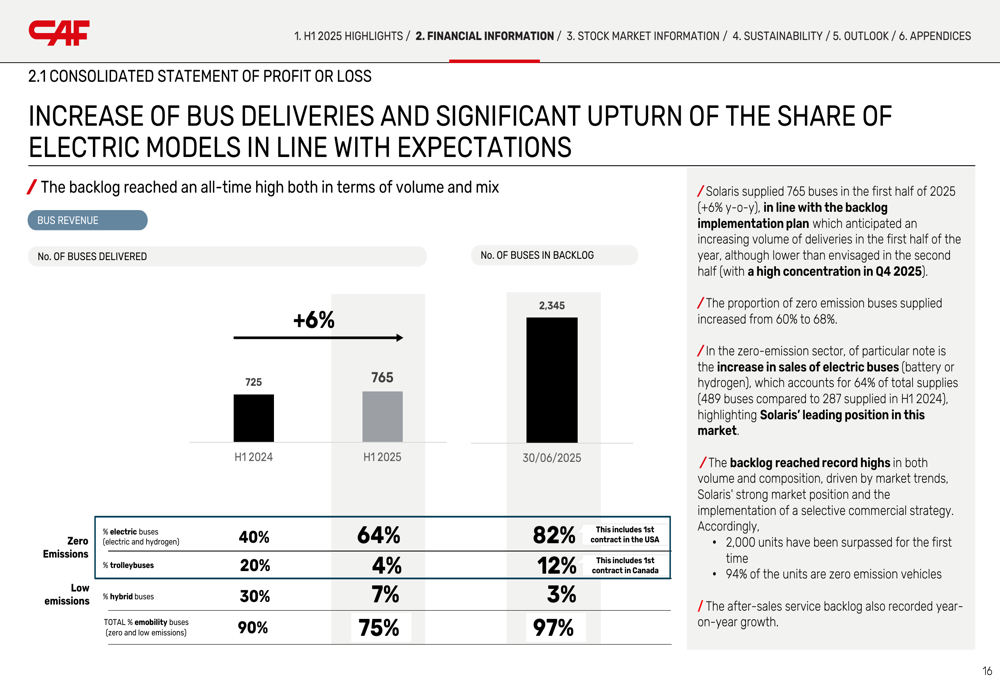

CAF’s strategic focus on zero-emission transportation solutions is yielding significant results, particularly in its bus segment. The company delivered 765 buses in H1 2025, a 6% increase year-over-year, with zero-emission buses (battery or hydrogen) accounting for 64% of total supplies, up from 40% in H1 2024.

The backlog for buses reached an all-time high in terms of volume and mix, with zero-emission buses representing 82% of the backlog as of June 30, 2025, highlighting the company’s successful transition toward sustainable transportation solutions.

The following chart illustrates the increase in bus deliveries and the growing share of electric models:

In the railway segment, CAF is focusing on expanding its services business, which grew 16% in H1 2025. The company currently holds over 150 service contracts across 20 countries, maintaining 11,600 cars with over 4,000 employees dedicated to this segment.

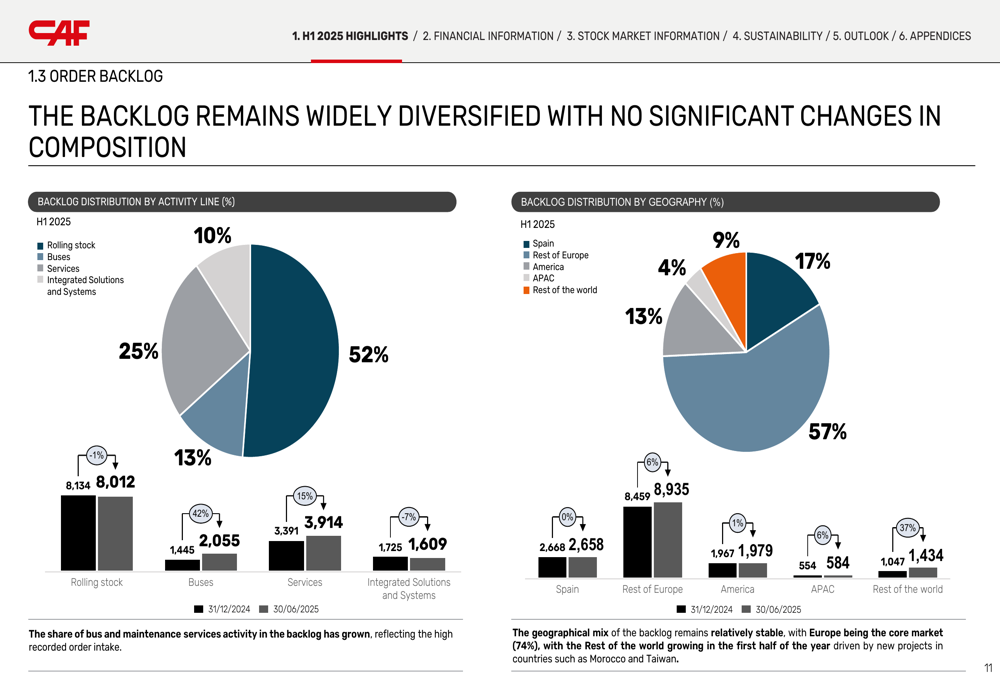

The backlog composition reflects CAF’s strategic priorities, with rolling stock accounting for 52% of the total backlog, followed by services (25%), buses (13%), and integrated solutions and systems (10%). Geographically, Europe remains the core market, representing 66% of the backlog.

As shown in this breakdown of the backlog composition:

Forward-Looking Statements

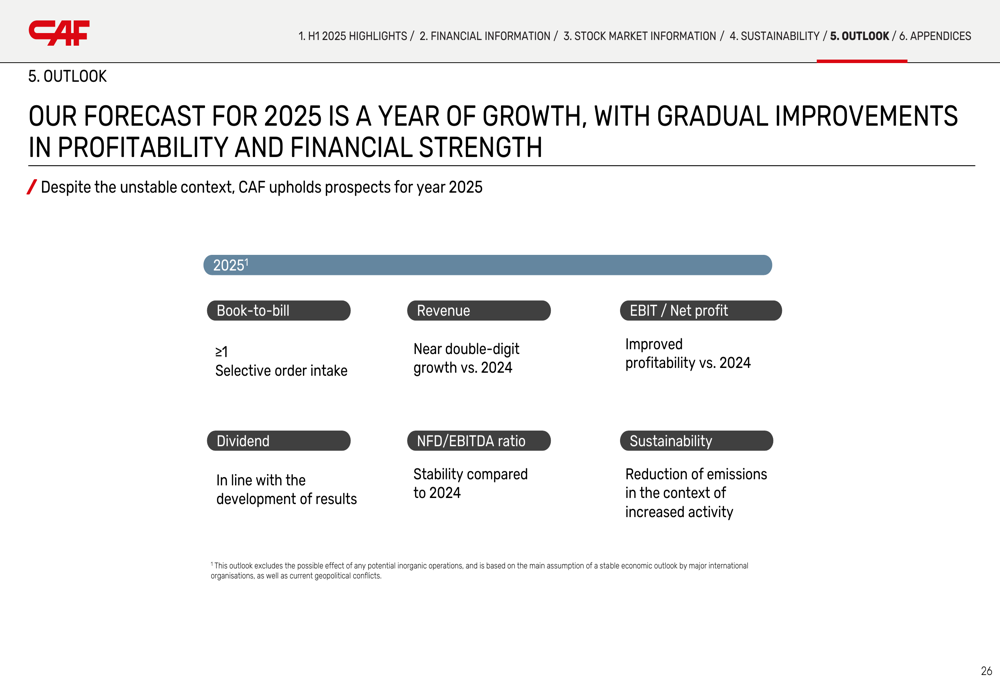

Despite the unstable macroeconomic context, CAF maintained its positive outlook for 2025, forecasting near double-digit revenue growth compared to 2024, improved profitability, and a stable net financial debt to EBITDA ratio.

The company expects to maintain a book-to-bill ratio of at least 1.0 through selective order intake and plans to continue its dividend policy in line with the development of results. CAF also remains committed to reducing emissions despite increased activity levels.

The following slide outlines CAF’s forecast for 2025:

CAF’s record backlog of €15,590 million, representing a backlog-to-revenue ratio of 3.7x for buses and 4.1x for railway, provides strong visibility for future activity. The backlog does not include contracts signed in Q3 2025 (totaling over €440 million) and future options executable by customers (exceeding €9 billion), suggesting potential for further growth.

As illustrated in this chart showing the backlog at historic highs:

With its strong order intake, improving profitability, and strategic focus on sustainable transportation solutions, CAF appears well-positioned to deliver on its growth targets for 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.