Bets on October rate-cut overblown as Fed a ’reluctant dove,’ Macquarie warns

Introduction & Executive Summary

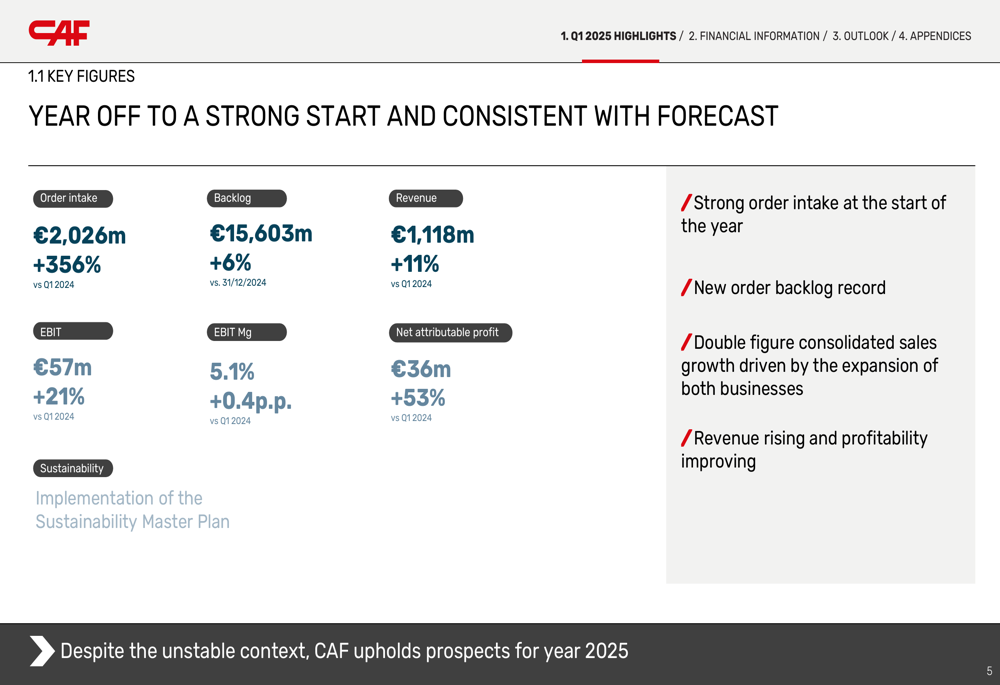

Construcciones y Auxiliar de Ferrocarriles SA (BME:CAF) reported a strong start to 2025, with double-digit growth across key financial metrics and a record order backlog. The Spanish rolling stock manufacturer presented its first-quarter results on May 8, 2025, highlighting a 356% surge in order intake and significant improvements in profitability.

The company’s performance was driven by strong commercial activity in both its railway and bus segments, with notable geographic expansion into new markets including Morocco and Canada. CAF’s shares closed at €43.40 on the day of the presentation, up 0.46%.

As shown in the following comprehensive overview of financial performance:

Quarterly Performance Highlights

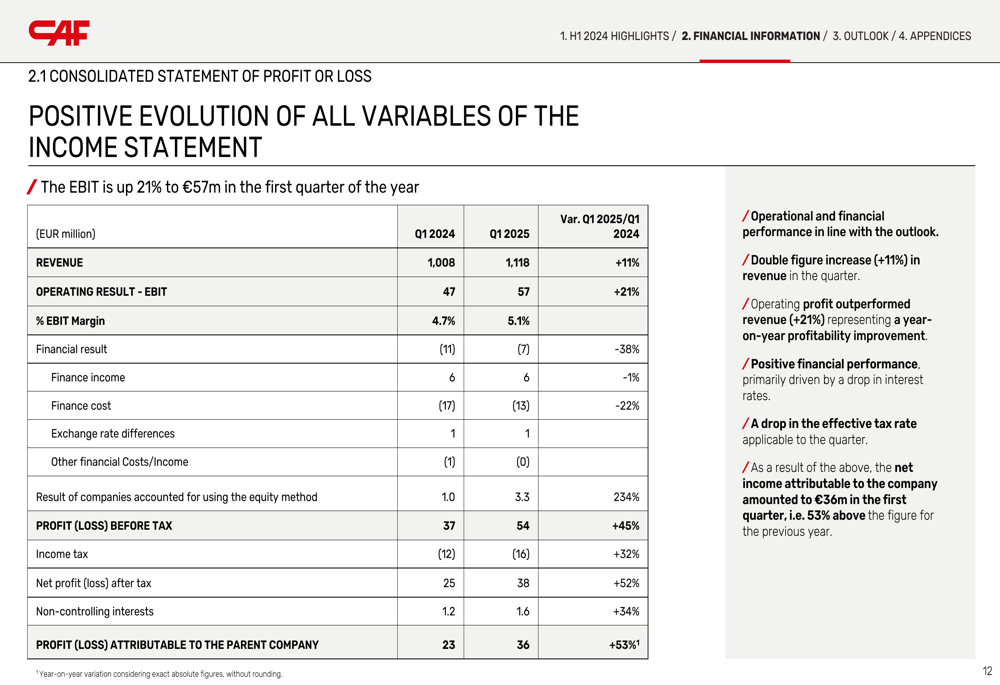

CAF reported consolidated revenue of €1,118 million in Q1 2025, representing an 11% increase compared to the same period last year. The company’s operating profit (EBIT) grew by 21% to €57 million, with the EBIT margin improving by 0.4 percentage points to 5.1%. Net profit attributable to the parent company showed the strongest growth, jumping 53% to €36 million.

The detailed financial results demonstrate positive evolution across all income statement variables:

The company’s financial performance benefited from lower interest rates, with finance costs decreasing by 22% compared to Q1 2024. This contributed to a 45% increase in profit before tax, reaching €54 million.

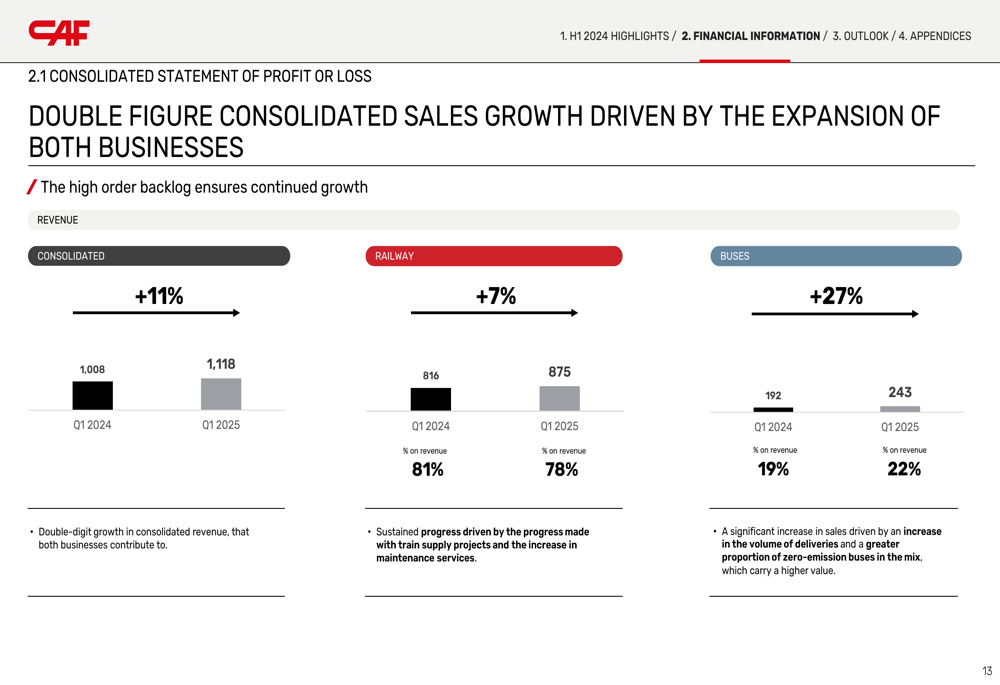

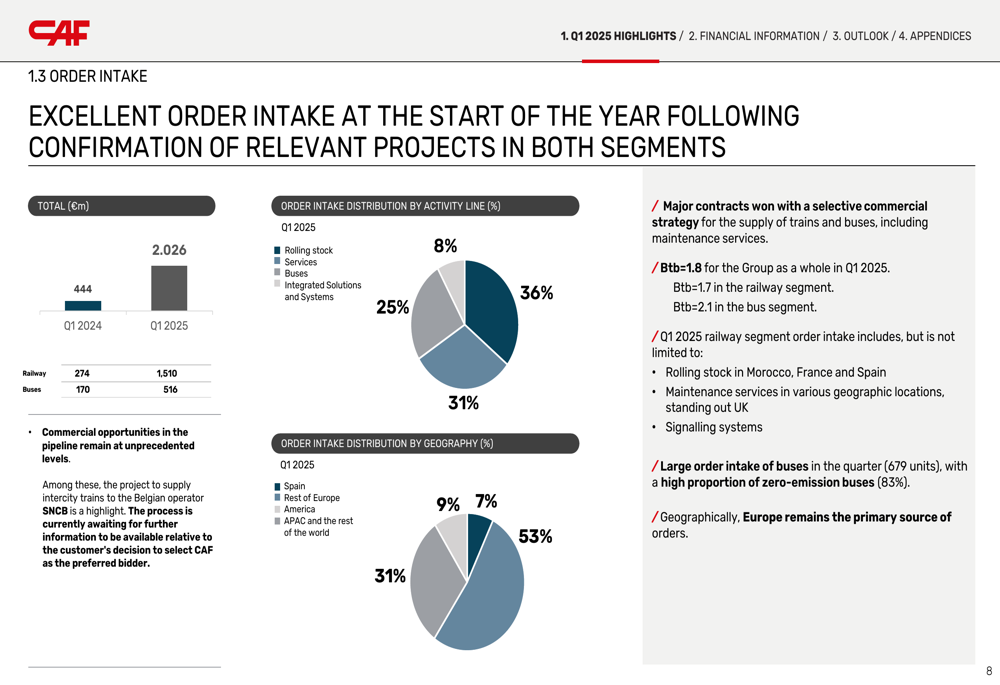

Revenue growth was driven by both business segments, with railways continuing to represent the majority of sales at 78% of total revenue. However, the bus segment showed stronger growth momentum:

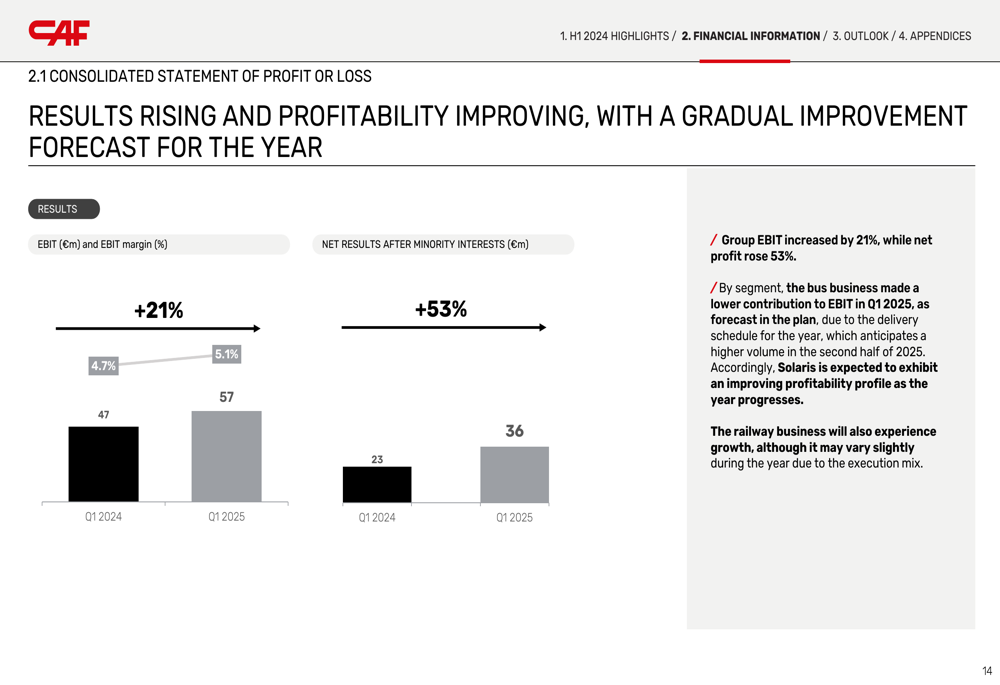

Profitability metrics continued their upward trajectory, with the company forecasting gradual improvement throughout the year:

Order Intake and Backlog

The most impressive aspect of CAF’s Q1 performance was the extraordinary growth in order intake, which reached €2,026 million, representing a 356% increase compared to Q1 2024. This commercial success was achieved through what the company described as a "selective commercial strategy" for both trains and buses.

The order intake was well-diversified across business lines and geographies, with Europe remaining the primary source of orders at 53% of the total:

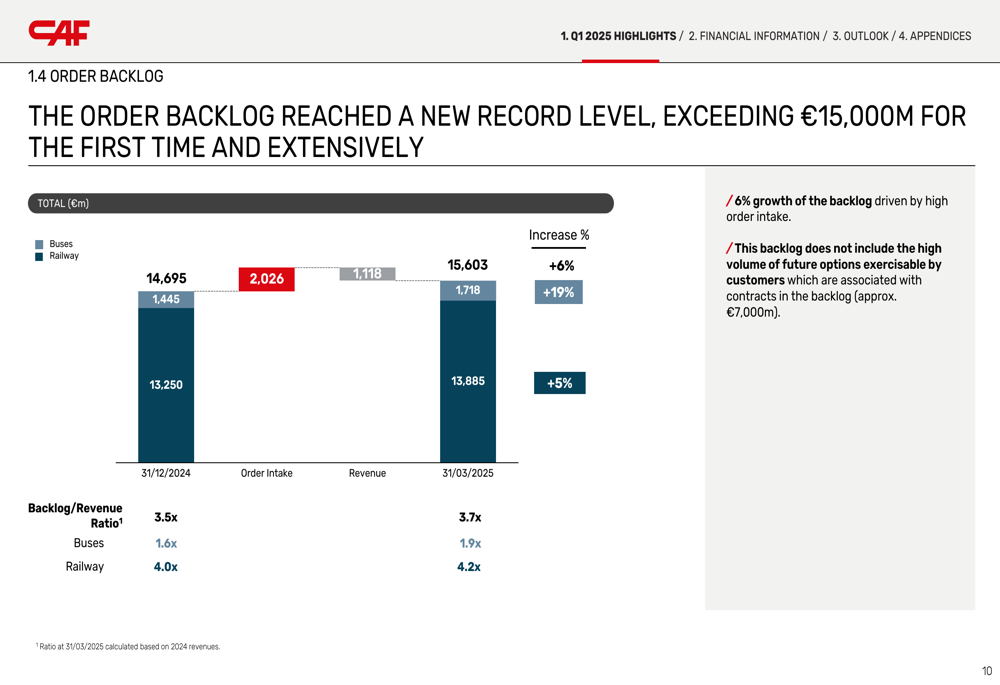

This strong commercial activity pushed CAF’s order backlog to a new record level, exceeding €15 billion for the first time. The total backlog reached €15,603 million, a 6% increase from December 31, 2024, providing substantial visibility for future revenue:

The backlog-to-revenue ratio improved to 3.7x from 3.5x, with the railway segment at 4.2x and the bus segment at 1.9x. Notably, the company indicated that the backlog figure does not include approximately €7 billion in future options that could be exercised by customers.

Geographic Expansion

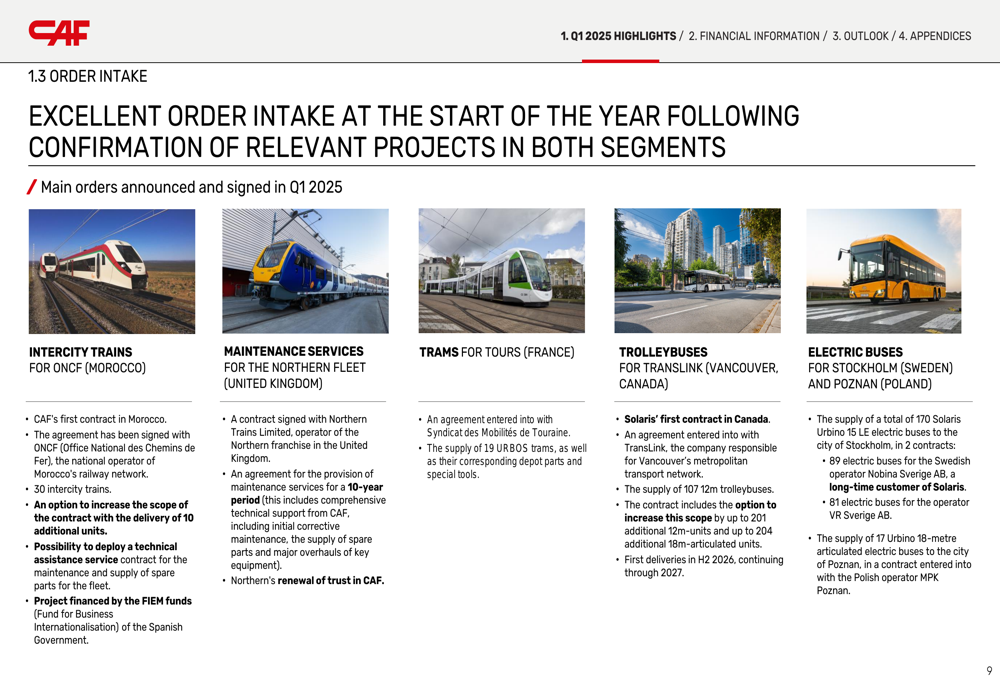

CAF highlighted several significant contract wins during the quarter, including strategic entry into new markets. The company secured its first contract in Morocco for 30 intercity trains for ONCF, with an option to increase to 40 units.

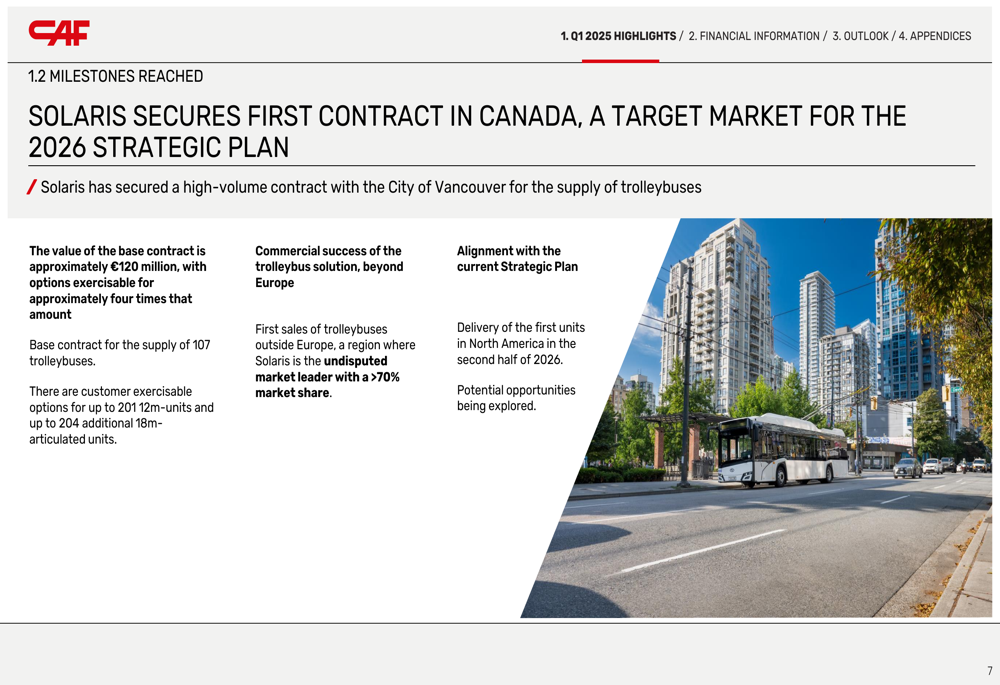

In another milestone, CAF’s bus subsidiary Solaris secured its first contract in Canada, a target market in the company’s 2026 Strategic Plan. The contract with the City of Vancouver is for the supply of trolleybuses:

The base contract, valued at approximately €120 million, includes 107 trolleybuses with options for up to 405 additional units that could multiply the contract value by approximately four times. Solaris claims to be the undisputed market leader in trolleybuses with over 70% market share.

Other significant orders announced during the quarter included:

US Market Exposure

In light of recent tariff concerns, CAF addressed its exposure to the United States market, emphasizing that it represents a relatively small portion of its business. According to the company, approximately 6% of its backlog is related to the US, and less than 1% of direct purchases for non-US projects originate from the country.

The company noted that it complies with the "Buy American Act" through its industrial plant in Elmira, New York, and a portion of its supply chain in the US. CAF also highlighted that it has contractual protection mechanisms in place for changes in law and exchange rate hedging for ongoing projects.

Despite these challenges, CAF reaffirmed that the US remains a core market in its strategy, with plans for continued local industrial implementation. In the bus segment, the company is progressing with its current protected exports strategy while evaluating the decision to localize production.

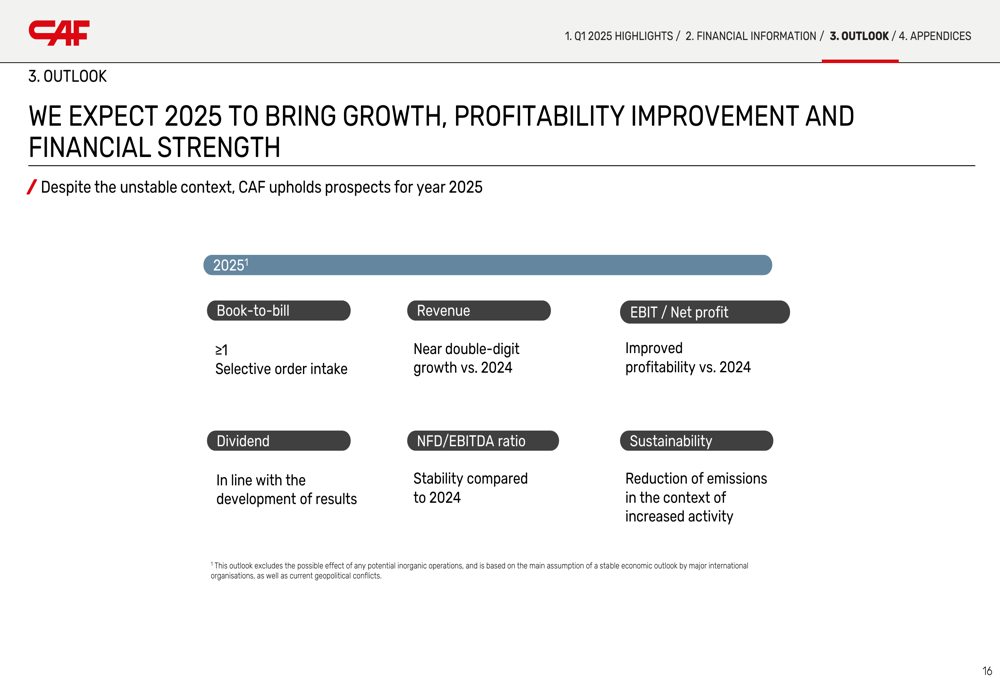

2025 Outlook

Looking ahead, CAF maintained its positive outlook for 2025 despite acknowledging an unstable context. The company expects to achieve near double-digit revenue growth compared to 2024, with improved profitability for both EBIT and net profit:

The company aims to maintain a book-to-bill ratio of at least 1.0 through selective order intake and expects stability in its net financial debt to EBITDA ratio compared to 2024. CAF also plans to align its dividend policy with the development of results and continue reducing emissions despite increased activity levels.

With a record backlog, strong order intake, and improving profitability, CAF appears well-positioned to deliver on its 2025 outlook, continuing the positive momentum demonstrated in the first quarter of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.