Wall St futures flat amid US-China trade jitters; bank earnings in focus

Caleres Inc (NYSE:CAL) shares plunged over 16% in pre-market trading after the footwear company’s second quarter 2025 presentation revealed continued deterioration in sales and profitability. The presentation, delivered on September 4, 2025, highlighted ongoing challenges from tariffs and weakening consumer demand, despite strategic initiatives including the completed Stuart Weitzman acquisition and cost-cutting measures.

Quarterly Performance Highlights

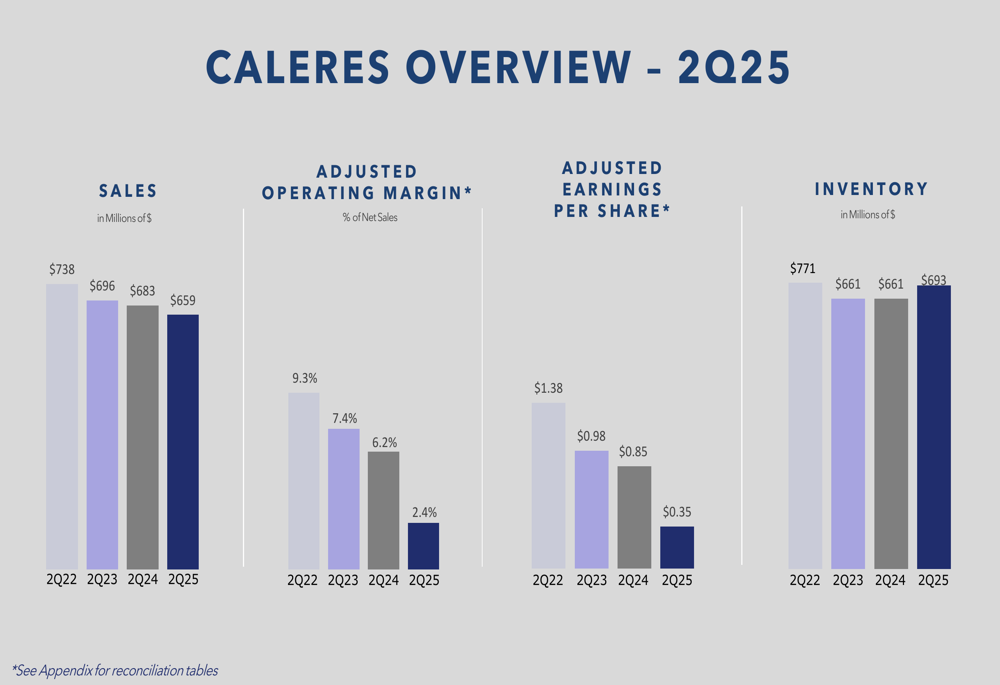

Caleres reported second quarter sales of $659 million, down 3.6% compared to the same period last year. This continues a multi-year downward trend, as quarterly sales have steadily declined from $738 million in Q2 2022. More concerning was the sharp drop in profitability, with adjusted earnings per share falling to $0.35, compared to $0.85 in Q2 2024 and $1.38 in Q2 2022.

As shown in the following comprehensive financial overview, the company has experienced consistent deterioration across key metrics:

Adjusted operating margin contracted significantly to 2.4%, down from 6.2% in the prior-year quarter and 9.3% in Q2 2022. Gross margin declined 210 basis points year-over-year to 43.4%, while inventory levels increased by 5% compared to Q2 2024.

The company’s Q2 at-a-glance summary highlights these challenging metrics:

Segment Performance

Both of Caleres’ main business segments reported declines in the quarter. The Brand Portfolio segment, which includes Sam Edelman, Allen Edmonds, and Naturalizer, posted sales of $276 million, down 3.5% versus the prior year. Management attributed $10 million of this decline to tariff impacts. The segment’s gross margin contracted 240 basis points to 40.3%, while operating margin fell to 3.1%.

Despite these challenges, the Brand Portfolio segment achieved market share gains of 0.5% in Women’s Fashion Footwear and 0.15% in the total market, according to data from Circana:

The Famous Footwear segment, which represents the company’s retail operations, saw sales decline 4.9% year-over-year to $400 million, with comparable store sales down 3.4%. Gross margin for this segment decreased 130 basis points to 43.7%. One bright spot was the kids’ category, which gained 0.3 percentage points of market share within shoe chains and now represents 21% of Famous Footwear’s total business:

Strategic Initiatives

Caleres highlighted several strategic accomplishments aimed at improving performance amid challenging conditions. The company completed its acquisition of Stuart Weitzman, which it described as a "new lead brand" that enhances direct-to-consumer and international capabilities. Management also reported achieving $15 million in annualized structural cost savings and accelerated sourcing migration away from China, reducing China-sourced products to 15% in the back half of 2025.

The presentation emphasized these key strategic initiatives:

"We’re making significant progress on our strategic priorities despite the challenging environment," said Jay Schmidt, CEO, in the previous earnings call. "The Stuart Weitzman acquisition represents an important step in our portfolio diversification and international growth strategy."

Forward-Looking Statements

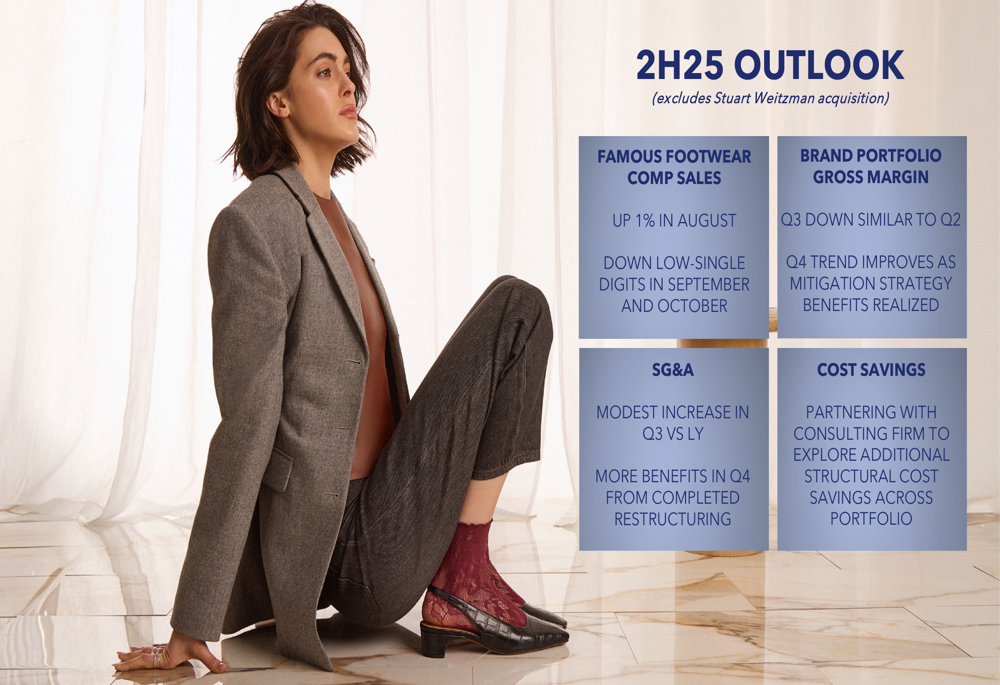

Looking ahead to the second half of 2025, Caleres provided a cautious outlook. The company expects Famous Footwear comparable sales to increase 1% in August but decline in low-single digits during September and October. Brand Portfolio gross margins are projected to decline in Q3 at a similar rate to Q2, with improvement expected in Q4 as mitigation strategies take effect.

Management outlined these expectations for the remainder of the year:

The company is partnering with a consulting firm to identify additional structural cost savings across its portfolio, suggesting further belt-tightening measures may be implemented. SG&A expenses are expected to increase modestly in Q3 compared to last year, with more benefits from restructuring anticipated in Q4.

Market Implications

The market reaction to Caleres’ presentation was decidedly negative, with the stock dropping 16.59% in pre-market trading to $12.47, approaching its 52-week low of $12.09. This follows a challenging first quarter when the company reported an EPS of just $0.22, missing analyst expectations of $0.37.

The continued deterioration in financial performance suggests Caleres is struggling to navigate the challenging retail environment, tariff pressures, and changing consumer preferences. While management has implemented cost-cutting measures and completed the Stuart Weitzman acquisition, investors appear concerned about the company’s ability to reverse declining sales and profitability trends.

The second quarter results represent a significant setback following management’s previous expressions of confidence in their ability to "get back on track" after disappointing Q1 results. With tariff uncertainties continuing to impact the business and consumer demand showing signs of weakness, Caleres faces substantial challenges in stabilizing performance in the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.