Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

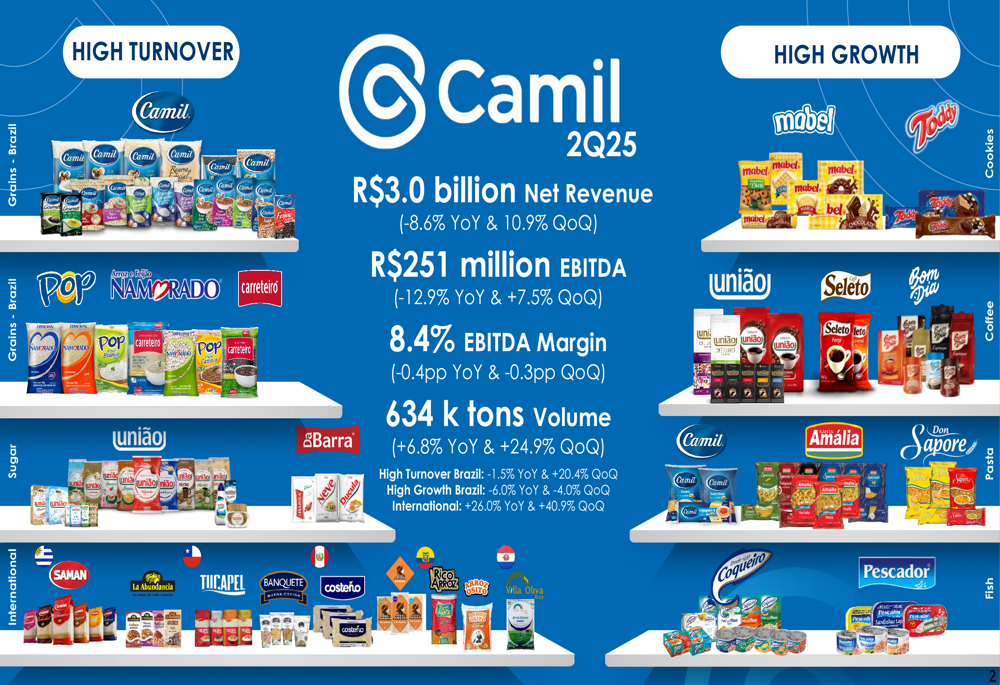

Camil Alimentos SA (BVMF:CAML3) presented its Q2 2025 earnings results on October 10, 2025, revealing a mixed performance characterized by strong volume growth counterbalanced by significant price pressures. The Brazilian food producer reported a net revenue decline of 8.6% year-over-year to R$3.0 billion, while total volume increased 6.8% to 634,000 tons.

The company’s stock closed at R$4.8 on October 9, showing a 2.71% gain, suggesting cautious market optimism ahead of the earnings release. Camil shares have traded between R$3.43 and R$8.7 over the past 52 weeks, indicating considerable volatility in investor sentiment.

Quarterly Performance Highlights

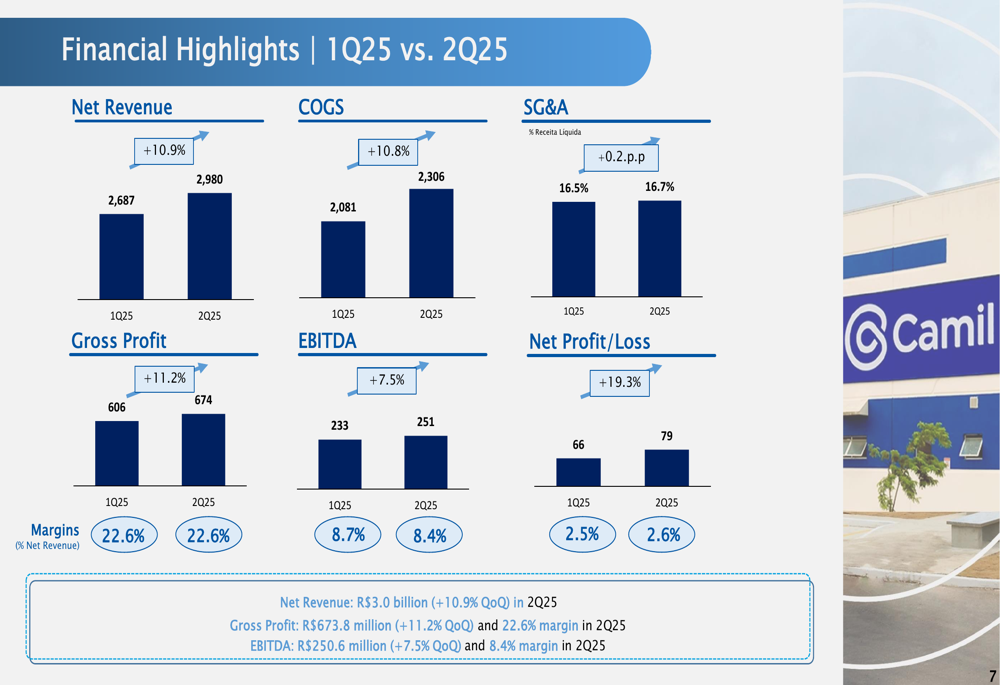

Camil’s second quarter results showed sequential improvement from Q1 2025 but remained below year-ago levels for key profitability metrics. EBITDA fell 12.9% year-over-year to R$251 million but improved 7.5% quarter-over-quarter. Similarly, EBITDA margin contracted to 8.4%, representing a 0.4 percentage point decline from the same period last year.

As shown in the following financial highlights summary:

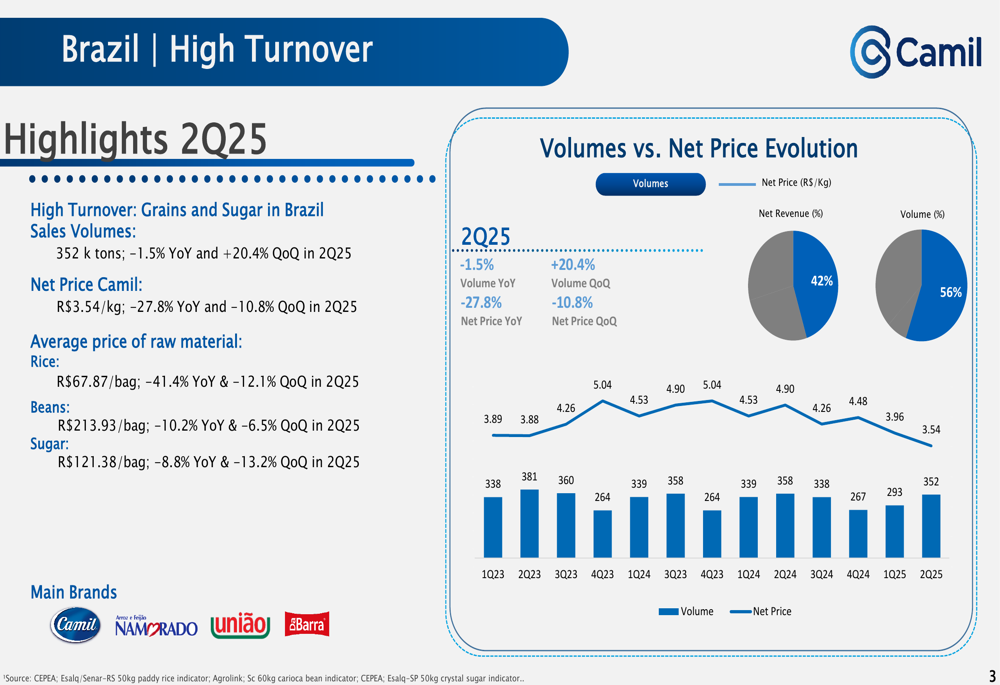

The company’s performance varied significantly across its business segments. High-turnover products in Brazil, which include rice, beans, and sugar, experienced volume declines of 1.5% year-over-year but rebounded 20.4% from the previous quarter. More concerning was the 27.8% year-over-year drop in net prices for these staple products.

The Brazil high-turnover segment details reveal the extent of price pressure:

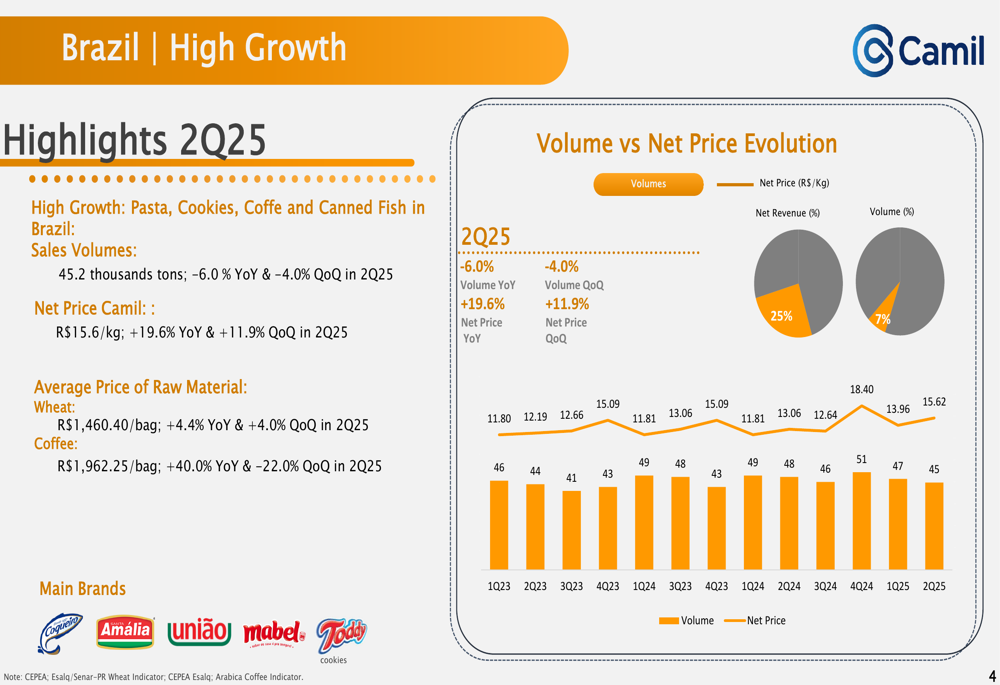

Meanwhile, Camil’s high-growth products in Brazil, which include pasta, cookies, coffee, and canned fish, showed a different pattern with volumes declining 6.0% year-over-year while prices increased 19.6%. This suggests the company is prioritizing margin protection in these premium categories.

The following chart illustrates the high-growth segment dynamics:

Detailed Financial Analysis

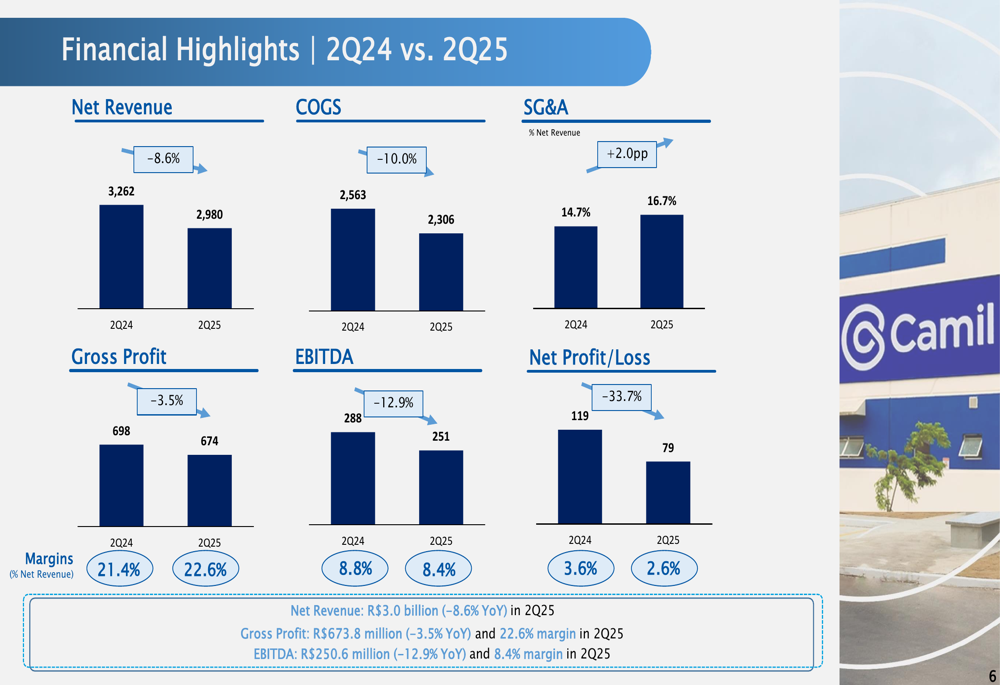

A closer examination of Camil’s financial performance reveals that despite the revenue decline, the company managed to improve its gross margin to 22.6%, up 1.2 percentage points year-over-year. This improvement was driven by effective cost management, as cost of goods sold decreased by 10.0%, outpacing the revenue decline.

However, increased selling, general, and administrative expenses, which rose from 14.7% to 16.7% of revenue, put pressure on overall profitability. Net profit fell 33.7% year-over-year to R$79 million, though it improved 19.3% sequentially from Q1 2025.

The year-over-year financial comparison highlights these trends:

The sequential improvement from Q1 to Q2 2025 provides a more encouraging picture:

Strategic Initiatives

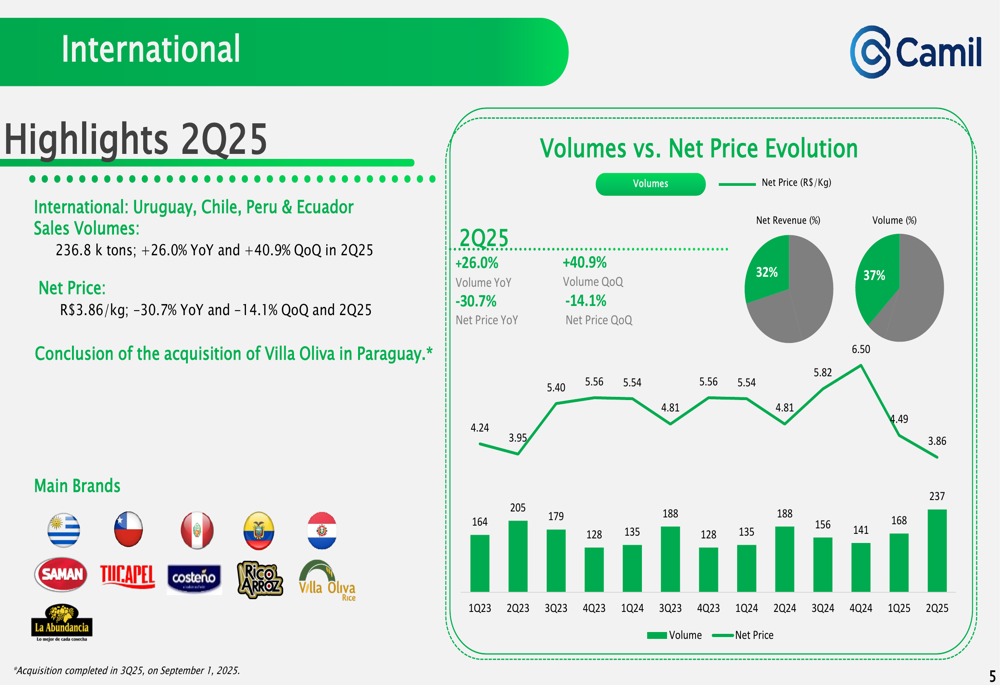

Camil’s international operations emerged as a bright spot in the quarter, with volumes surging 26.0% year-over-year and 40.9% quarter-over-quarter. This growth came despite a 30.7% year-over-year decrease in net prices, reflecting challenging global commodity price environments.

The company completed its acquisition of Villa Oliva in Paraguay on September 1, 2025, expanding its international footprint. This strategic move aligns with Camil’s focus on growth through geographic diversification.

The international performance metrics demonstrate the strength of this segment:

Forward-Looking Statements

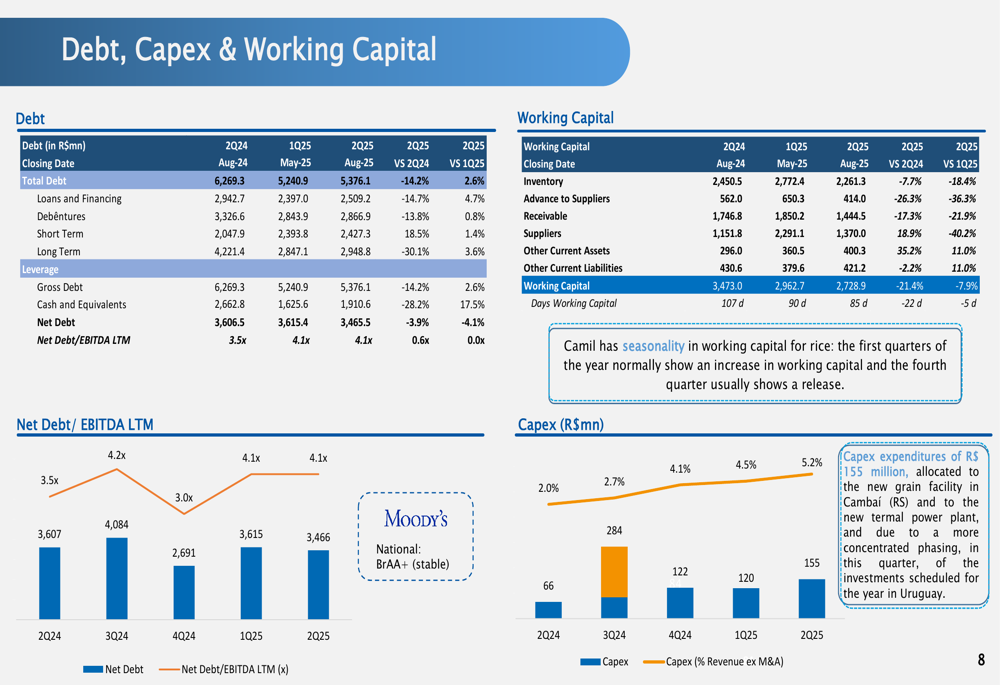

Camil continues to focus on debt management, with a stated goal of reducing its net debt to EBITDA ratio to approximately 2x. As of Q2 2025, this ratio stood at 4x, unchanged from the previous quarter, indicating that debt reduction remains a work in progress.

The company’s working capital management and capital expenditure plans suggest a disciplined approach to financial stewardship during challenging market conditions. Management has emphasized the importance of maintaining strong brands and strategic initiatives to drive growth despite price volatility in key commodity markets.

In the previous quarter’s earnings call, CEO Luciano Quartiero expressed confidence that "with our brands, internal adjustments, and strategic initiatives, we will continue to drive our growth." The Q2 results suggest that while volume growth is materializing, price pressures continue to challenge overall financial performance.

The debt and working capital position provides context for these strategic priorities:

Analyst Perspectives

Market analysts are likely to focus on Camil’s ability to navigate the opposing forces of volume growth and price pressure. The company’s sequential improvement from Q1 2025 suggests potential stabilization, but year-over-year declines in revenue and profits indicate ongoing challenges.

Key questions for investors include whether the strong volume growth in international markets can be maintained while improving price realization, and how quickly Camil can achieve its debt reduction targets. The company’s diversified product portfolio provides some insulation against commodity price volatility, but the significant price declines in high-turnover products remain a concern.

With the stock trading significantly below its 52-week high, Camil’s valuation metrics suggest potential undervaluation if the company can successfully navigate current market challenges and deliver on its strategic initiatives. The completion of the Villa Oliva acquisition represents a tangible step toward the international growth strategy that may help offset domestic market pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.