Perion Network shares rise 4% on Q3 earnings beat, strong CTV growth

Introduction & Market Context

Capstone Copper Corp (TSX:CS | ASX:CSC) presented its Q2 2025 results on July 31, highlighting record copper production and strong financial performance despite mixed market reaction. The company’s stock closed at $12.71 on October 14, 2025, down 1.81% for the day, though it has shown remarkable strength with a 40.38% year-to-date return according to available market data.

The copper producer operates in what it describes as "top-tier jurisdictions in the Americas," with five producing assets and a clear growth trajectory. The presentation comes amid strong global copper demand and favorable market conditions, with CEO Cashel Meagher noting that "copper is in the spotlight with government signaling its strategic importance."

Quarterly Performance Highlights

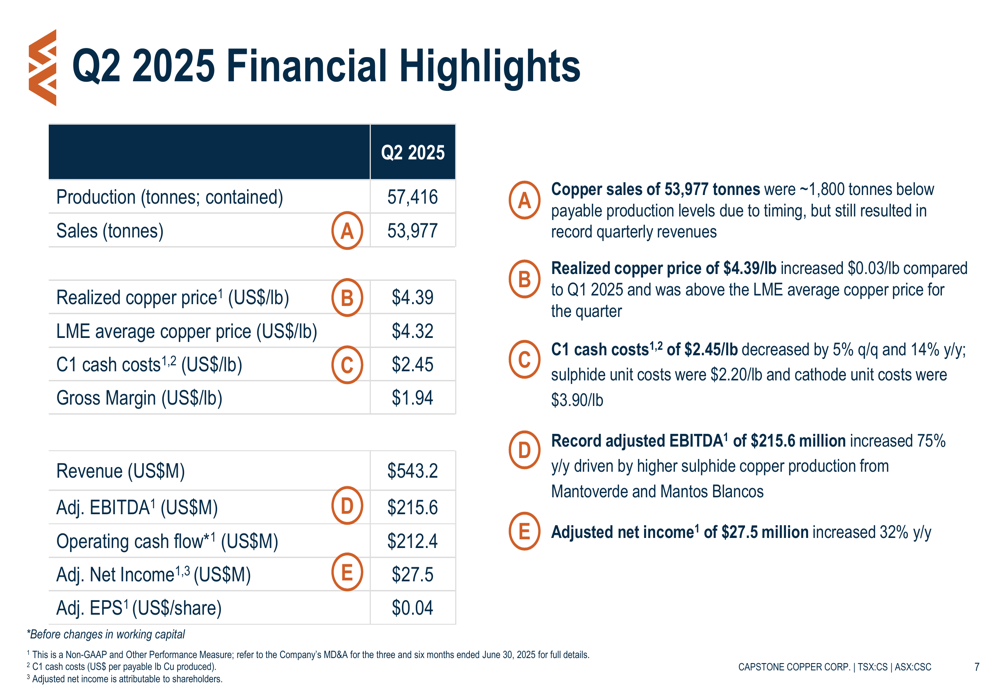

Capstone reported record copper production of 57,416 tonnes in Q2 2025, driving revenue to $543.2 million. The company achieved adjusted EBITDA of $215.6 million, representing a significant 75% year-over-year increase. C1 cash costs decreased to $2.45/lb, down 5% quarter-over-quarter and 14% year-over-year, reflecting operational improvements across most of its mines.

As shown in the following summary of Q2 2025 highlights, the company’s sulphide business outperformed its cathode business in terms of both production volume and cost efficiency:

The financial results demonstrate Capstone’s improving operational efficiency, with gross margin reaching $1.94/lb and adjusted net income of $27.5 million ($0.04 per share). The company’s realized copper price of $4.39/lb exceeded the LME average copper price of $4.32/lb for the quarter.

The detailed financial breakdown reveals record quarterly revenues despite copper sales being slightly below production levels due to timing:

Operational Updates by Mine

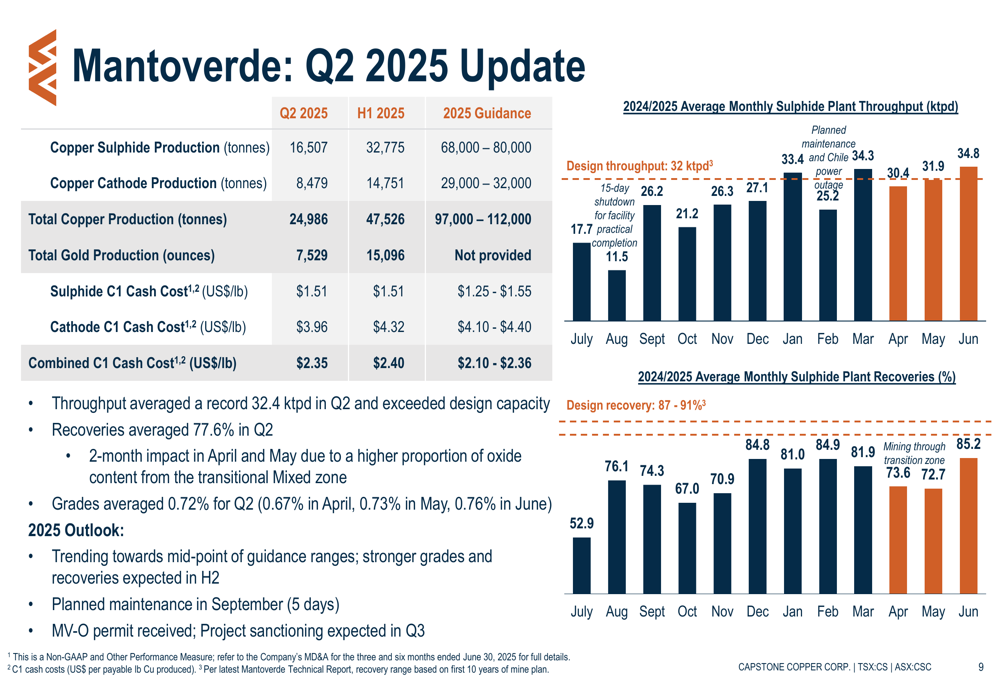

Mantoverde emerged as a standout performer, achieving record throughput averaging 32.4 ktpd in Q2 2025. The operation produced 24,986 tonnes of copper (16,507 tonnes from sulphide and 8,479 tonnes from cathode) with combined C1 cash costs of $2.35/lb. The successful ramp-up of the Mantoverde Development Project, which achieved commercial production in September 2024 and reached design throughput rates in the fourth quarter of operation, has been crucial to Capstone’s overall production growth.

The following chart illustrates Mantoverde’s sulphide plant throughput and recovery improvements:

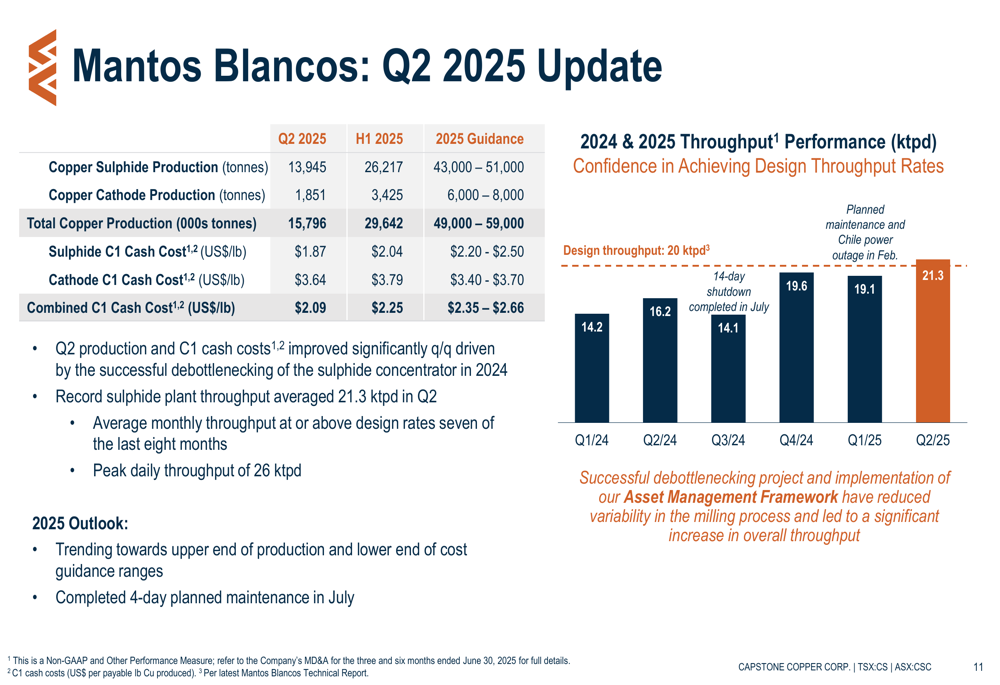

Mantos Blancos also delivered strong results, with total copper production of 15,796 tonnes in Q2 2025 and combined C1 cash costs of $2.09/lb. The operation achieved record sulphide plant throughput averaging 21.3 ktpd and is trending toward the upper end of production guidance and lower end of cost guidance for 2025.

The throughput performance at Mantos Blancos shows consistent improvement:

Pinto Valley faced challenges with production of 10,125 tonnes of copper in Q2 2025 at C1 cash costs of $3.89/lb. Production was impacted by water constraints, though grades and recoveries increased quarter-over-quarter. The operation is implementing an Asset Management Framework to improve performance but is trending toward the lower end of production guidance and upper end of cost guidance for 2025.

Cozamin delivered 6,509 tonnes of copper in Q2 2025 at C1 cash costs of $1.49/lb, with production increasing 6% year-over-year and costs decreasing 16% year-over-year. The operation is trending toward the upper end of production guidance and lower end of cost guidance for 2025.

Growth Strategy and Future Outlook

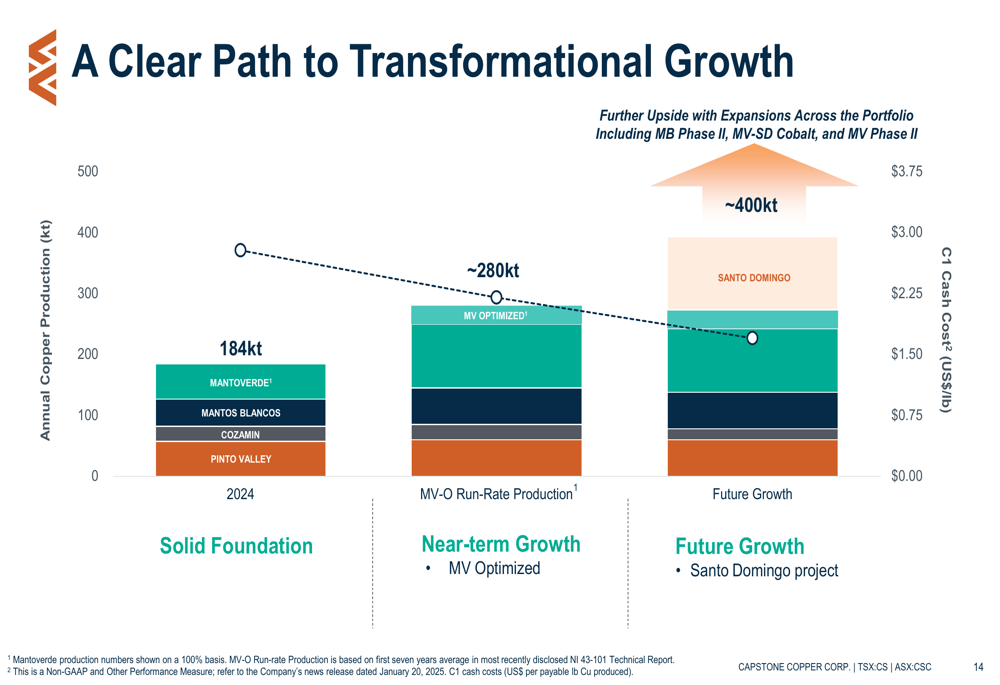

Capstone reaffirmed its 2025 consolidated guidance of 220-255kt copper production and outlined a clear growth trajectory. The company’s path to transformational growth includes increasing production from the current 184kt annual rate to approximately 280kt with the Mantoverde Optimized (MV-O) project, and eventually to around 400kt with the addition of the Santo Domingo project.

This growth path is illustrated in the following chart:

The company reported receiving the MV-O permit and expects project sanctioning in Q3 2025. The Santo Domingo partnership process is also advancing, with announcements expected in the coming quarters. These projects form the cornerstone of Capstone’s strategy to increase production while decreasing unit costs.

Capstone’s positioning in stable jurisdictions across the Americas supports its long-term growth strategy:

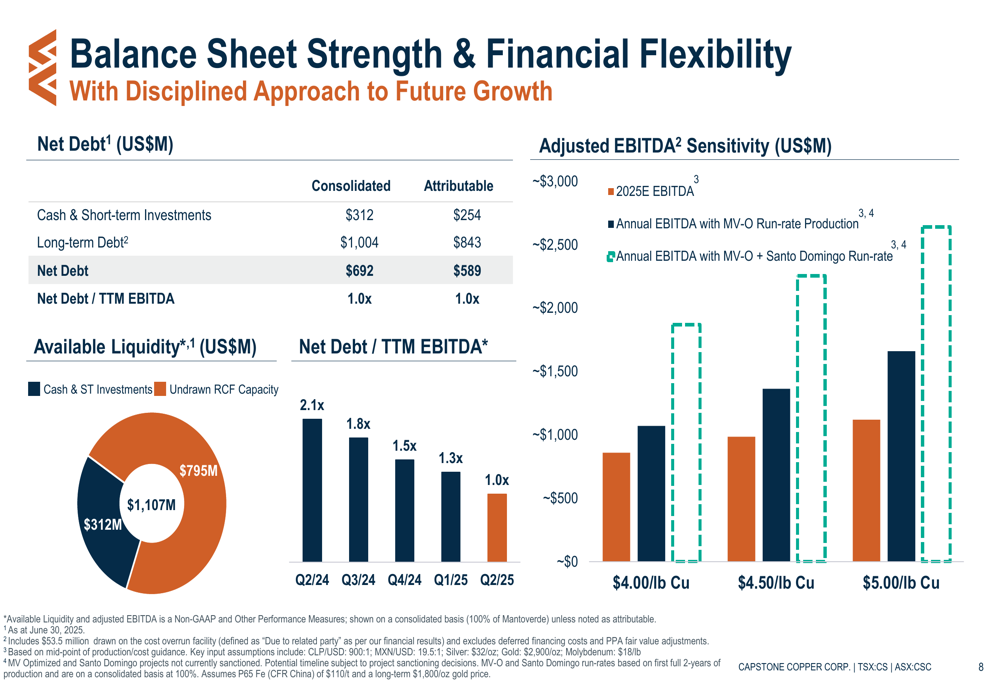

Financial Position and Balance Sheet Strength

Capstone has strengthened its financial position, reporting consolidated net debt of $692 million as of June 30, 2025, representing a Net Debt/TTM EBITDA ratio of 1.0x. The company completed a debt refinancing with repayment of the Mantoverde project finance facility and now has available liquidity of $1,107 million.

The company’s balance sheet flexibility is illustrated in the following summary:

The debt repayment schedule shows minimal near-term obligations, with only $7 million due in 2026 and $17 million in 2027. This provides Capstone with financial flexibility to fund its growth projects while maintaining balance sheet strength.

Forward-Looking Statements

Looking ahead, Capstone’s H2 2025 priorities include MV-O project sanctioning and Santo Domingo partnership process advancement. The company expects higher copper production in the second half of the year, driven primarily by Mantoverde and Pinto Valley.

CEO Cashel Meagher emphasized the company’s strong positioning, stating, "We are positioned extremely well. Our ramp-ups are complete, our production is increasing, and our costs are coming down."

While Capstone faces challenges including water constraints at Pinto Valley and potential market volatility, its diversified asset base, strong balance sheet, and clear growth strategy position it to capitalize on the favorable long-term outlook for copper demand.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.