S&P 500 falls as ongoing government shutdown, trade jitters weigh

Introduction & Market Context

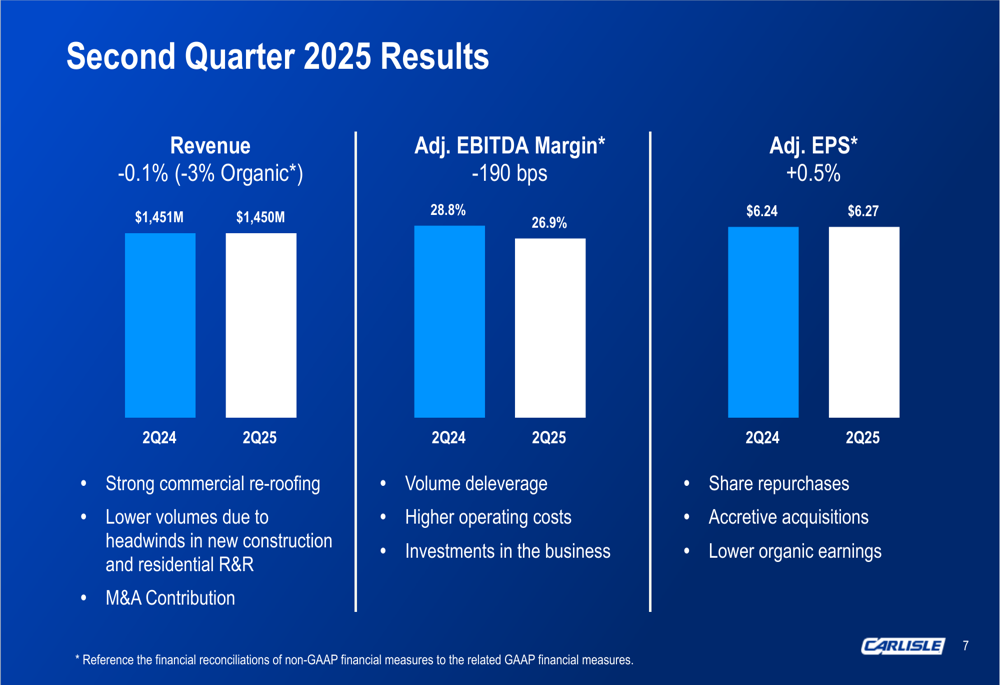

Carlisle Companies (NYSE:CSL) presented its second quarter 2025 results on July 30, showing resilient performance despite challenging market conditions. The building envelope leader reported flat year-over-year revenue of $1.4 billion and a record adjusted EPS of $6.27, slightly up from $6.24 in the prior year. However, these results fell short of analyst expectations, with EPS missing forecasts by 5.86% and revenue coming in 2.68% below expectations.

The market reacted negatively to the earnings miss, with Carlisle’s stock dropping 3.23% in aftermarket trading to close at $422.37, moving away from its 52-week high of $481.26.

As shown in the following overview of Q2 2025 performance, Carlisle maintained its adjusted EBITDA margin above its Vision 2030 target despite market challenges:

Quarterly Performance Highlights

Carlisle’s second quarter results revealed divergent performance across its business segments. The Carlisle Construction Materials (CCM) segment posted a modest 0.6% revenue increase to $1.096 billion, while the Carlisle Weatherproofing Technologies (CWT) segment experienced a 2% revenue decline to $354 million.

The company’s adjusted EBITDA margin contracted by 190 basis points year-over-year to 26.9%, reflecting higher operating costs and continued investments in innovation. Despite these pressures, Carlisle returned $343 million to shareholders through dividends and share repurchases during the quarter.

The following chart illustrates the company’s Q2 2025 financial performance compared to the same period in 2024:

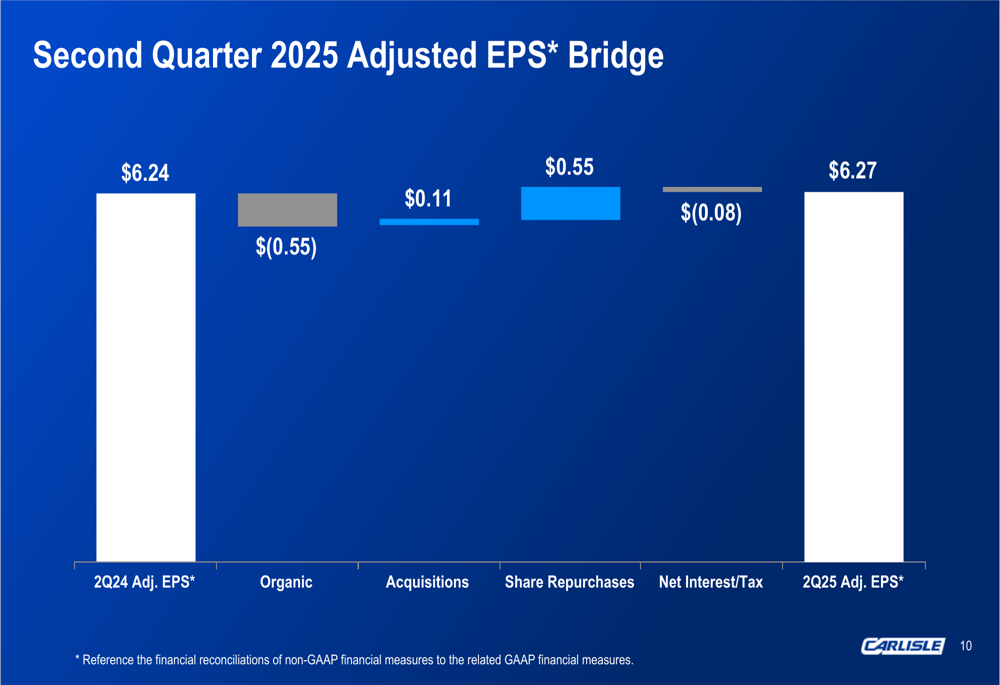

A closer examination of the adjusted EPS bridge reveals how share repurchases and acquisitions helped offset organic earnings decline:

Cash flow performance showed significant improvement, with free cash flow increasing from $156 million in Q2 2024 to $258 million in Q2 2025, putting the company on track to exceed its Vision 2030 target of 15%+ free cash flow margin:

Market Trends & Positioning

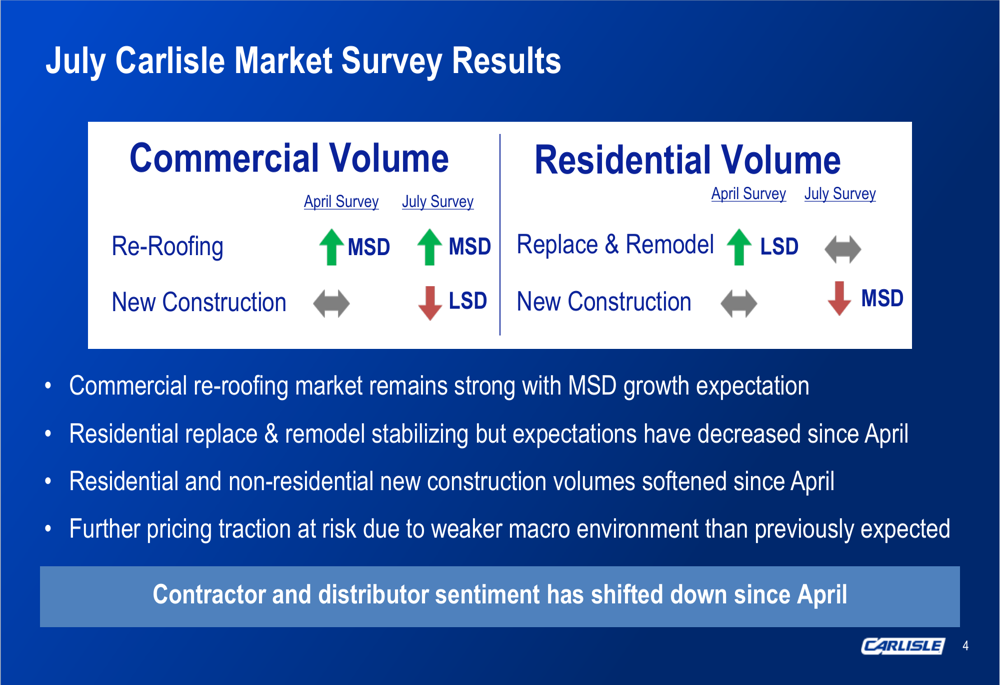

Carlisle’s July market survey revealed contrasting trends across different construction segments. Commercial re-roofing continues to show strength with mid-single-digit growth expectations, while residential replace and remodel markets are stabilizing but at lower levels than previously anticipated. Both residential and non-residential new construction volumes have softened since April.

The survey results also indicate that further pricing traction may be at risk due to a weaker macroeconomic environment, with contractor and distributor sentiment shifting downward since April.

As shown in the following market survey results:

CEO Chris Koch expressed optimism about the company’s performance in the re-roofing market during the earnings call, stating, "We remain optimistic about our strong re-roofing performance balancing the macroeconomic pressures in new construction." However, the company faces challenges including macroeconomic pressures, potential supply chain disruptions, and competitive pressures in the commercial roofing sector.

Strategic Initiatives

Carlisle continues to execute its growth strategy through strategic acquisitions and product innovation. The company recently acquired Bonded Logic, a manufacturer of recycled denim insulation, positioning Carlisle to serve North America’s $14 billion addressable insulation market.

The acquisition aligns with Carlisle’s Vision 2030 strategy and sustainability goals, as Bonded Logic’s products divert post-consumer denim from landfills into energy-efficient insulation:

Innovation remains a key focus area, with several recent product launches aimed at delivering labor savings and energy efficiency. These include Flexible Fast Adhesive, which delivers 60% labor savings, and 12’ InsulBase Flat Polyiso panels, which demonstrated 34% labor savings in time trials:

Forward-Looking Statements

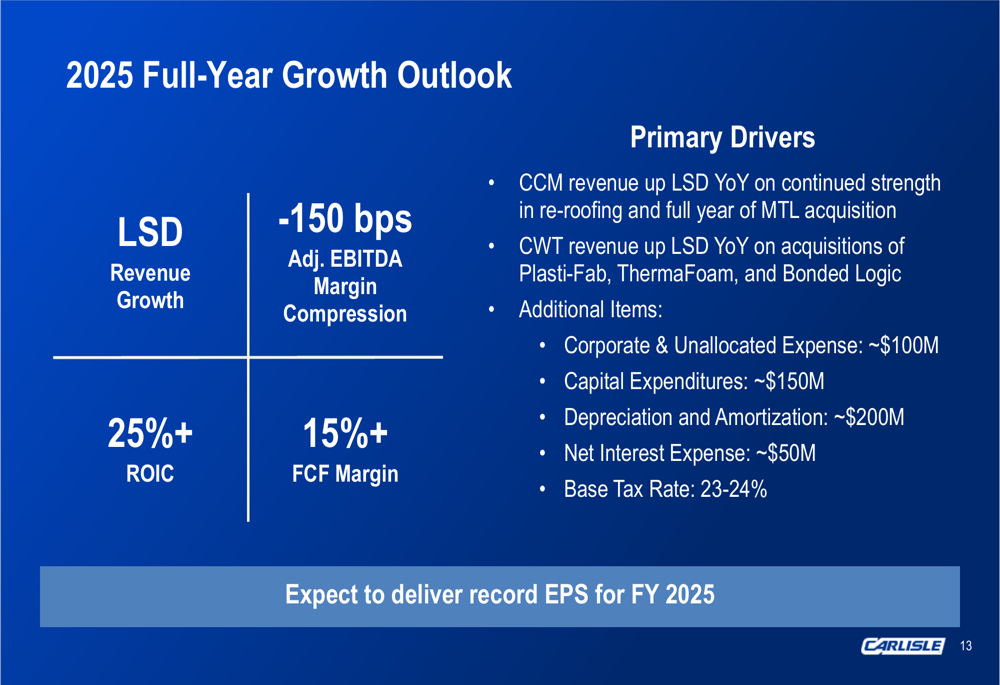

Looking ahead, Carlisle projects low single-digit revenue growth for the full year 2025, with an adjusted EBITDA margin compression of 150 basis points. The company expects to maintain a return on invested capital above 25% and a free cash flow margin exceeding 15%.

The growth outlook is supported by continued strength in commercial re-roofing and the full-year impact of recent acquisitions:

Carlisle remains focused on maintaining market leadership in its core segments while driving margin expansion through operational excellence and pricing discipline. The company’s long-term positioning strategy emphasizes innovation, strategic acquisitions, and efficiency improvements:

Despite the Q2 earnings miss and challenging market conditions, Carlisle expects to deliver record EPS for the full year 2025. However, investors will be watching closely to see if the company can overcome the headwinds in residential and new construction markets while maintaining its pricing power in an increasingly competitive environment.

With a net debt to EBITDA ratio of 1.4x and total liquidity of $1.1 billion, Carlisle maintains a strong balance sheet to execute its growth strategy and capital deployment initiatives, positioning the company to navigate market challenges while pursuing its Vision 2030 goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.