Buy tech sell-off, Wedbush’s Ives says: ’this is a 1996 moment, not 1999’

Introduction & Market Context

Carrier Global Corporation (NYSE:CARR) presented its second quarter 2025 earnings results on July 29, 2025, highlighting strong performance driven primarily by its commercial HVAC business. The company’s stock was trading at $79.79 in premarket, down slightly by 0.49% following the previous day’s close of $80.18.

The HVAC giant continued to build on its solid first quarter momentum, when it had raised full-year guidance after beating analyst expectations. The Q2 results demonstrate Carrier’s ability to execute its growth strategy despite varying regional performance, with particular strength in the Americas offsetting weakness in China.

Quarterly Performance Highlights

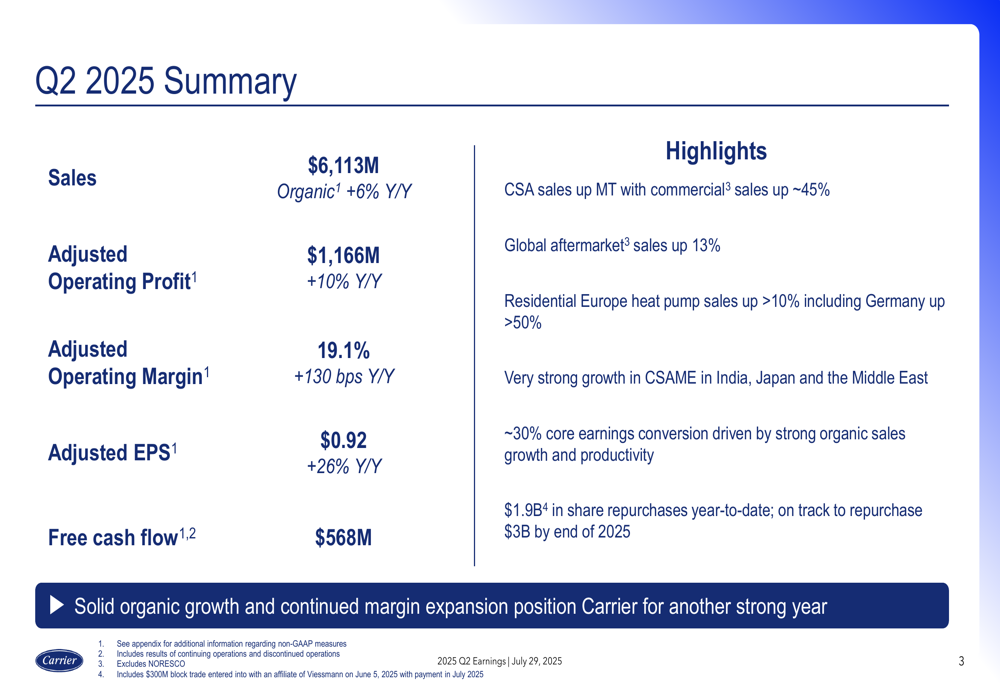

Carrier reported impressive financial results for Q2 2025, with organic sales growth of 6% year-over-year and a substantial 26% increase in adjusted earnings per share.

As shown in the following comprehensive financial summary from the presentation:

Key metrics included sales of $6,113 million, adjusted operating profit of $1,166 million (up 10% year-over-year), and adjusted operating margin of 19.1%, representing a 130 basis point improvement from the prior year. Free cash flow reached $568 million, supporting the company’s aggressive capital return program.

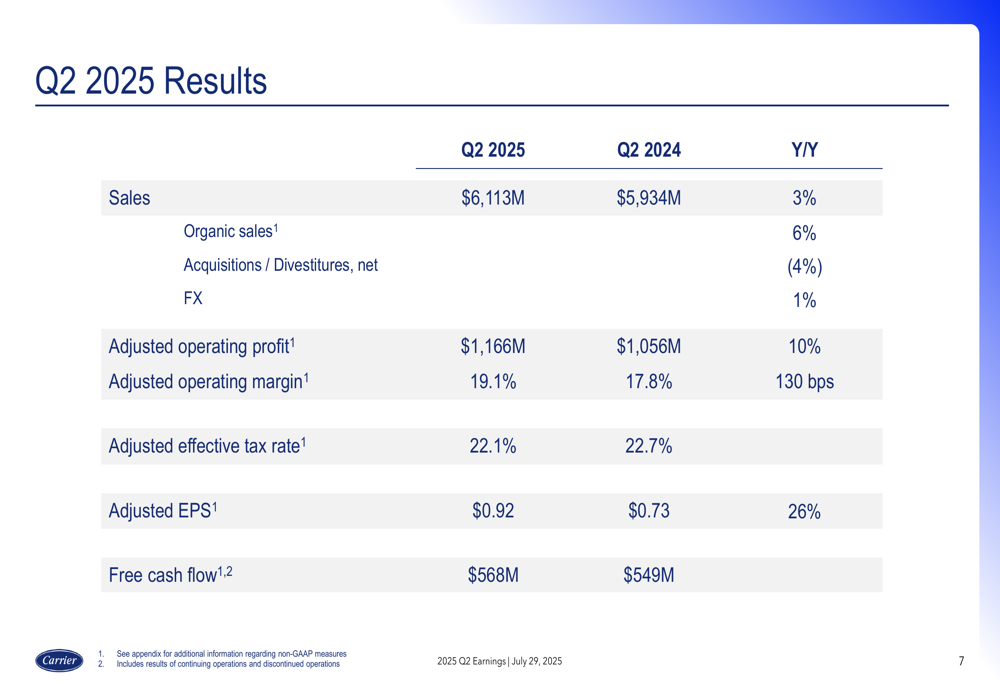

The detailed quarterly results compared to the previous year further illustrate this strong performance:

CEO David Gitlin had previously emphasized the company’s commitment to customer-focused innovation during the Q1 earnings call, stating, "We are laser-focused on our customers and continue to invest in differentiation and solutions to drive sustained outsized growth for years to come." The Q2 results appear to validate this strategy, particularly in the commercial HVAC segment where sales grew approximately 45%.

Segment Analysis

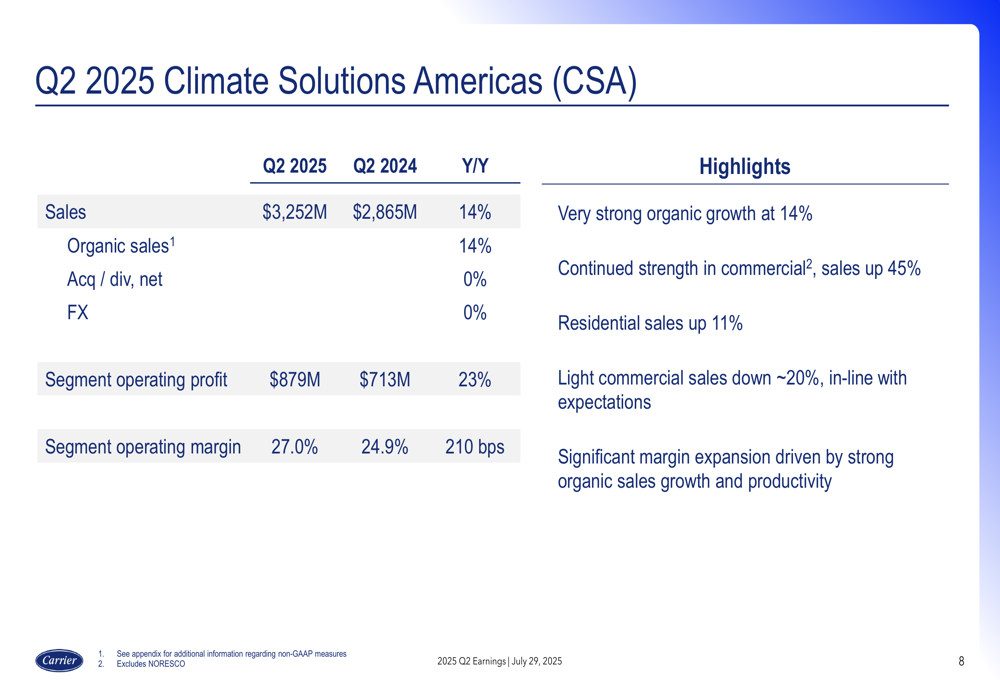

Carrier’s performance varied significantly across its geographic segments, with Climate Solutions Americas (CSA) leading the way while other regions faced challenges.

The CSA segment delivered exceptional results with 14% organic growth and substantial margin expansion:

The segment’s operating margin reached an impressive 27.0%, up 210 basis points year-over-year. Commercial sales surged 45%, while residential sales increased by 11%. However, light commercial sales declined by approximately 20%, which the company indicated was in line with expectations.

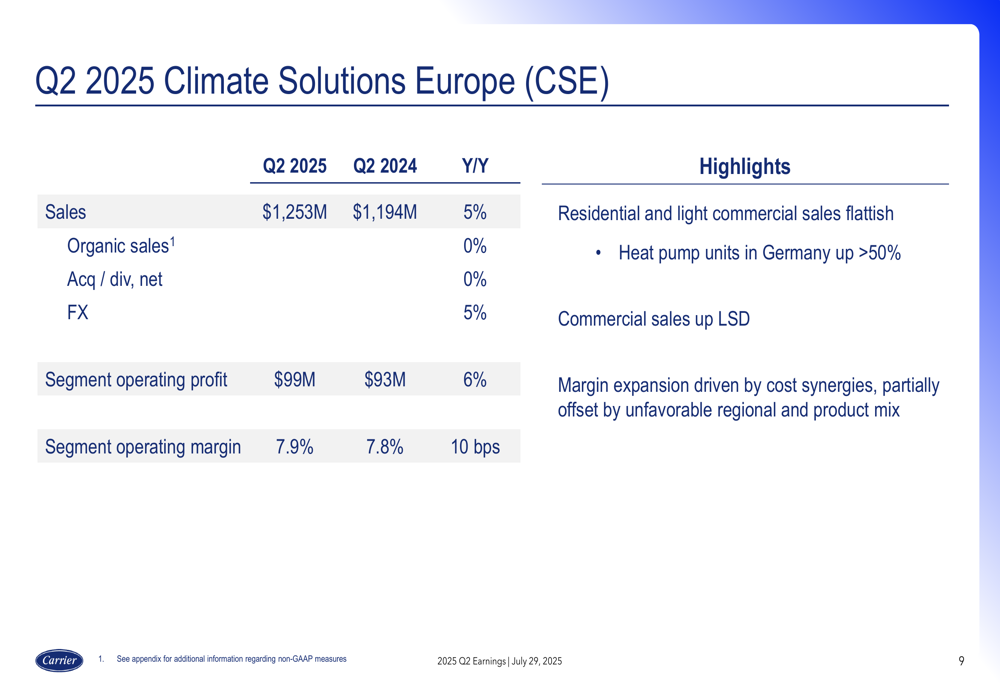

In contrast, Climate Solutions Europe (CSE) reported flat organic sales, with operating margin improving slightly to 7.9%:

A bright spot in Europe was the German heat pump market, where unit sales increased by more than 50%. This growth aligns with Europe’s push toward electrification and decarbonization of heating systems.

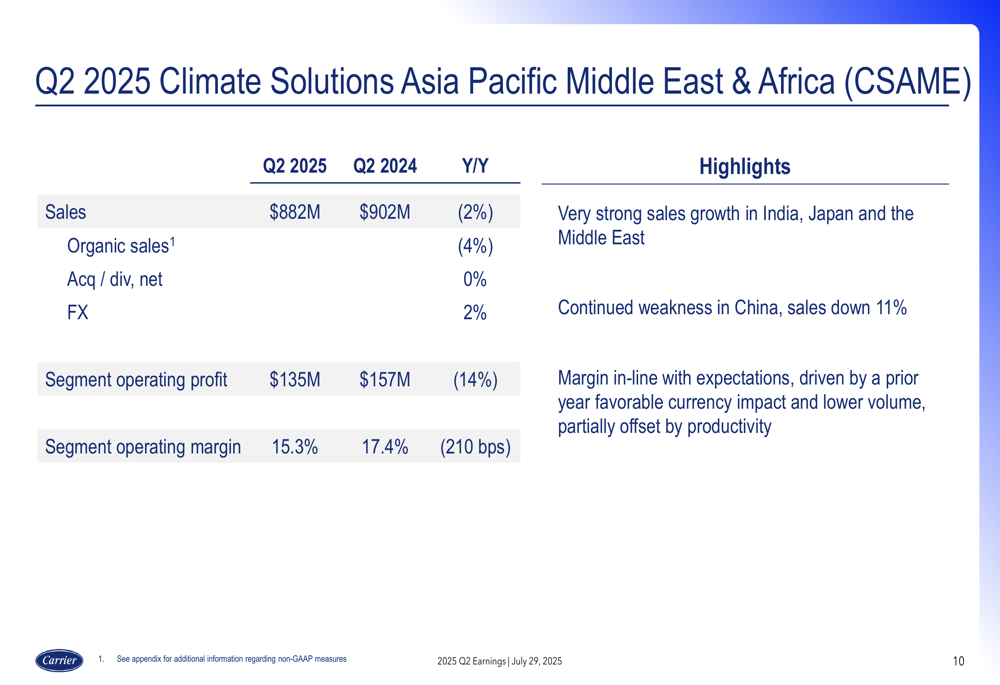

The Asia Pacific, Middle East & Africa (CSAME) segment faced challenges, with organic sales declining 4% and operating margin decreasing by 210 basis points to 15.3%:

The weakness was primarily attributed to China, where sales fell 11%. However, this was partially offset by strong performance in India, Japan, and the Middle East, highlighting the company’s geographic diversification benefits.

Strategic Initiatives

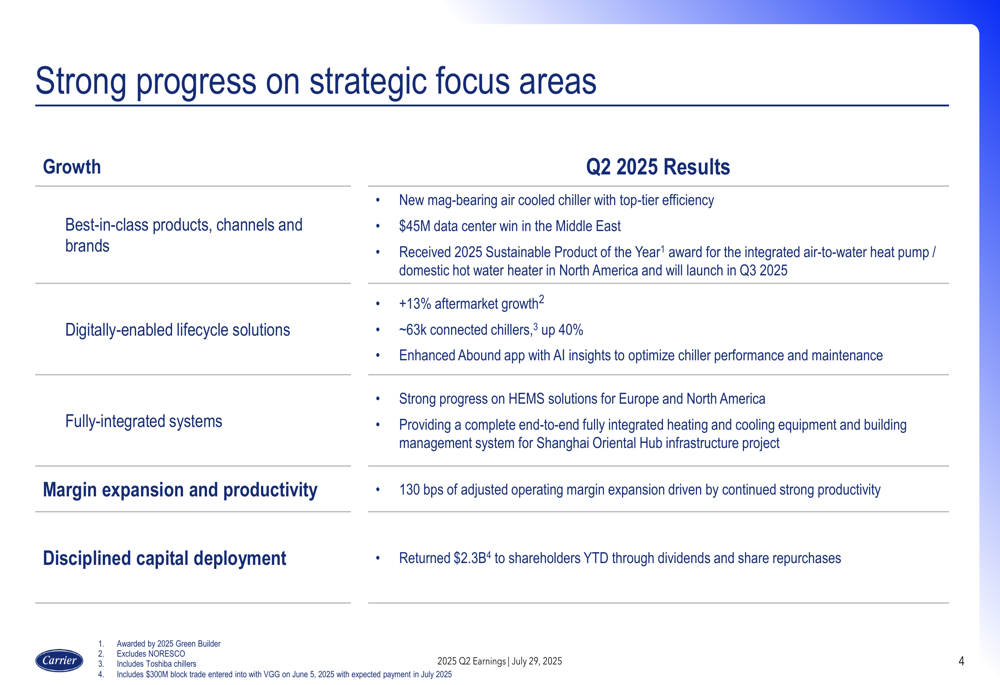

Carrier continued to make progress on its key strategic initiatives during the quarter, focusing on growth, digital solutions, integrated systems, and margin expansion.

The following slide details these achievements:

Notable accomplishments included a $45 million data center win in the Middle East, reflecting the company’s growing presence in this high-growth market. Carrier also enhanced its Abound app with AI insights to optimize chiller performance and maintenance, supporting its digital transformation strategy.

The integration of Viessmann’s residential and light commercial business in Europe appears to be progressing well, with the company reporting:

Carrier noted that it was delivering cost and revenue synergies from the acquisition while experiencing strong growth in air-conditioning sales. The company also reported increasing the number of "Viessmann Systems Profi" partners, which are showing stronger growth rates.

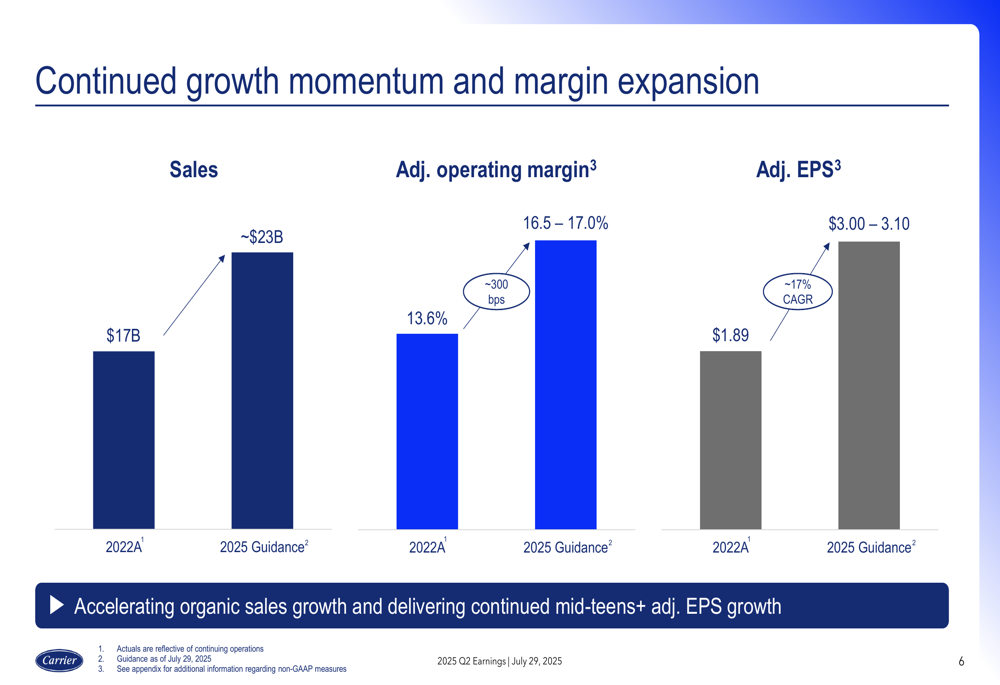

Looking at longer-term trends, Carrier displayed its progress toward 2025 financial targets:

The chart illustrates the company’s growth trajectory from 2022 to 2025, with sales expected to reach approximately $23 billion and adjusted operating margin targeted between 16.5% and 17.0%, representing about 300 basis points of improvement over this period.

Guidance and Outlook

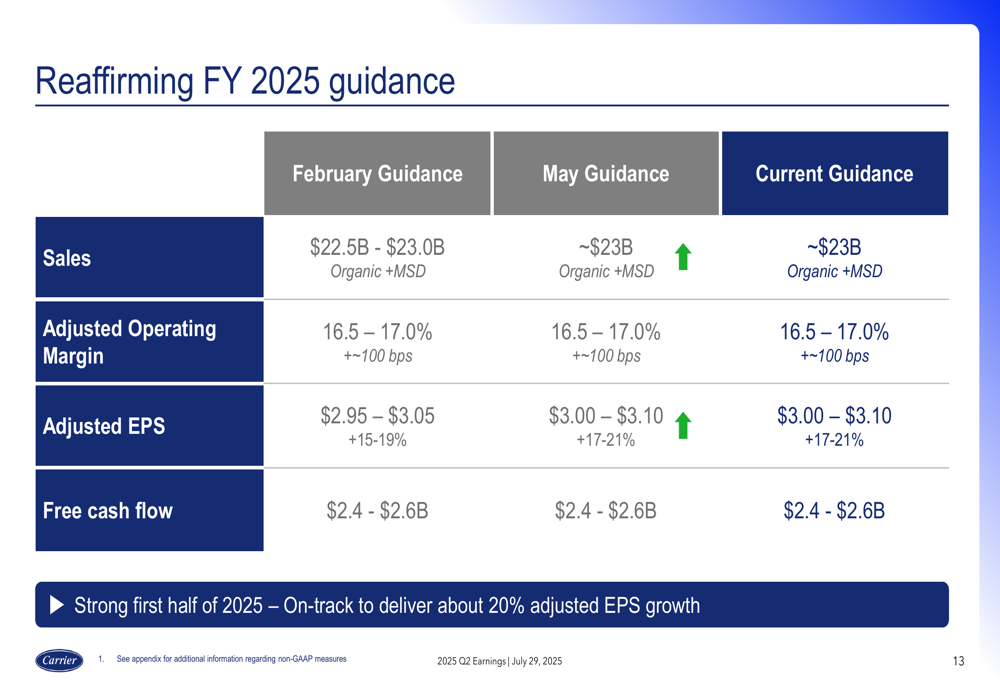

Despite mixed regional performance, Carrier reaffirmed its full-year 2025 guidance across all key metrics:

The company maintained its sales projection of approximately $23 billion with mid-single-digit organic growth, adjusted operating margin of 16.5-17.0% (representing about 100 basis points of expansion), and adjusted EPS of $3.00-$3.10, which implies 17-21% growth year-over-year.

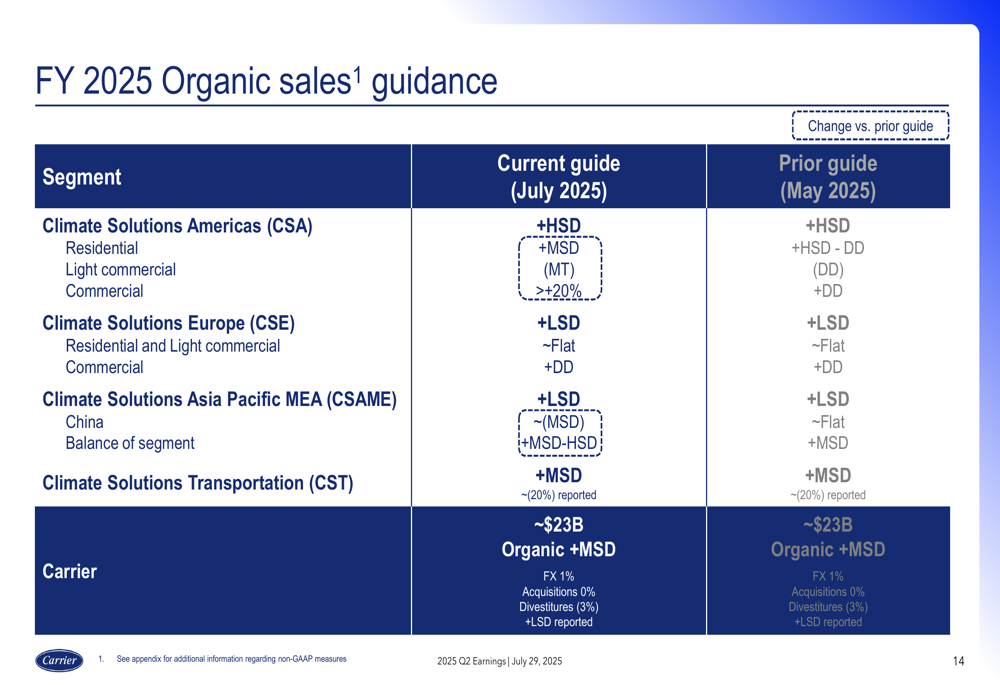

Carrier also provided a more detailed breakdown of its organic sales guidance by segment:

The outlook reflects continued strength in the Americas, with high-single-digit growth expected, while Europe and Asia Pacific are projected to grow at low-single-digit rates. The company maintained its guidance for most segments, with slight adjustments to CSA residential (lowered to mid-single digits from high-single to double digits) and China (lowered to negative mid-single digits from flat).

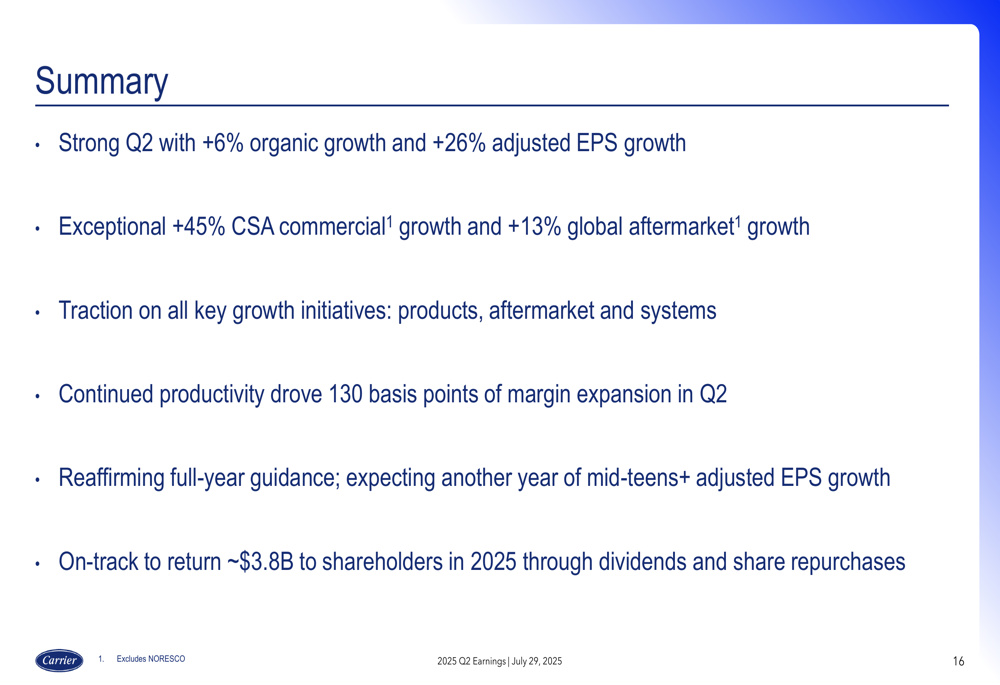

In its summary, Carrier highlighted its key achievements and outlook:

The company emphasized its strong Q2 performance with 6% organic growth and 26% adjusted EPS growth, exceptional commercial growth of 45% in the Americas, and 13% global aftermarket growth. Carrier also noted it was on track to return approximately $3.8 billion to shareholders in 2025 through dividends and share repurchases.

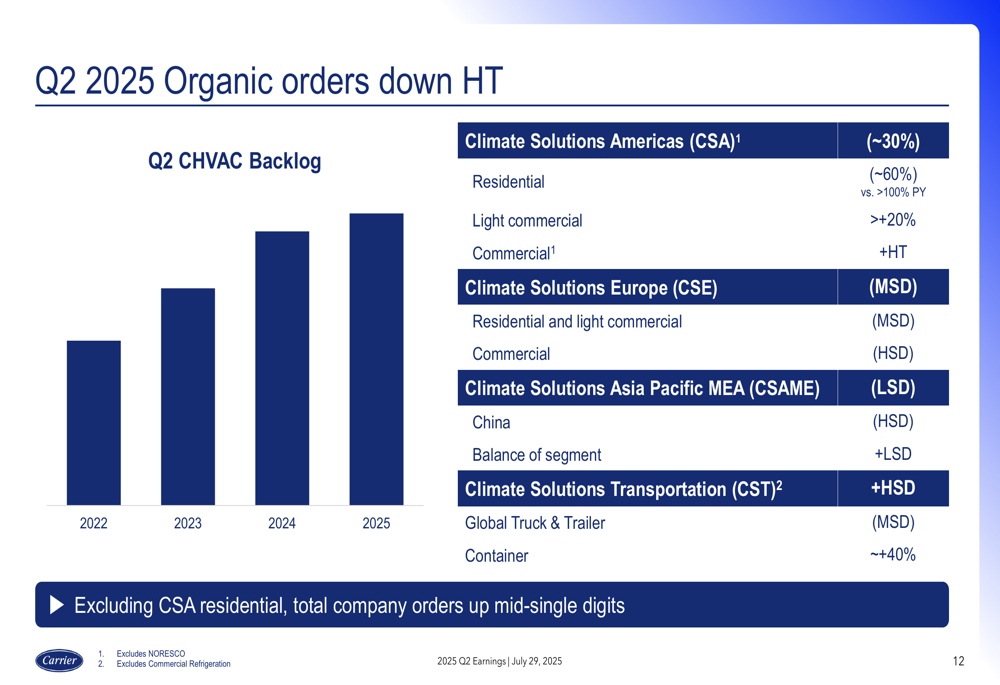

Order trends, however, presented a mixed picture for future quarters:

Overall organic orders were down high teens, primarily due to a 60% decline in CSA residential orders compared to a period of over 100% growth in the prior year. Excluding CSA residential, total company orders were up mid-single digits, suggesting continued momentum in commercial and other segments.

As Carrier moves into the second half of 2025, the company appears well-positioned to achieve its full-year targets, driven by strong commercial HVAC demand, growing aftermarket sales, and continued margin expansion despite regional challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.