TSX lower as gold rally takes a breather

Introduction & Market Context

Cascades Inc . (TSX:CAS) released its second quarter 2025 financial results on August 7, 2025, showing improved profitability metrics despite ongoing macroeconomic challenges. The packaging and tissue products manufacturer reported adjusted EBITDA of $137 million, representing an 11.5% margin, up from 9.5% in the same quarter last year. The company’s stock closed at $9.02 on August 6, 2025, near its 52-week low of $8.30, reflecting ongoing investor concerns following a disappointing first quarter.

Quarterly Performance Highlights

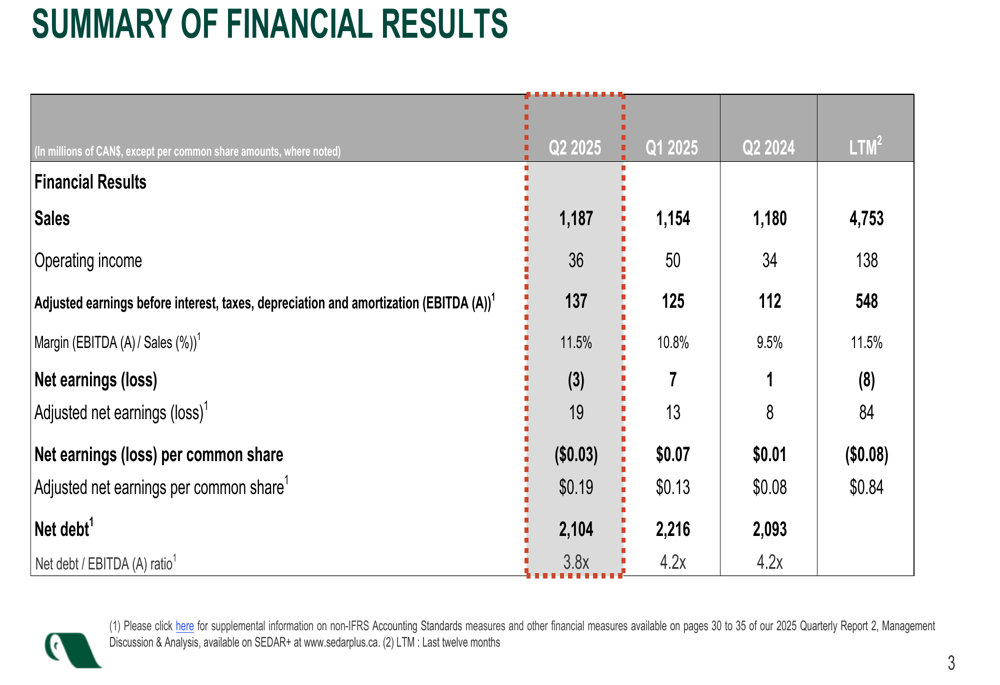

Cascades reported Q2 2025 sales of $1,187 million, slightly higher than both the previous quarter ($1,154 million) and the same period last year ($1,180 million). While operating income decreased sequentially to $36 million from $50 million in Q1, it improved year-over-year from $34 million in Q2 2024.

As shown in the following summary of financial results, the company’s adjusted EBITDA increased to $137 million, representing a 9.6% sequential improvement and a 22.3% year-over-year increase:

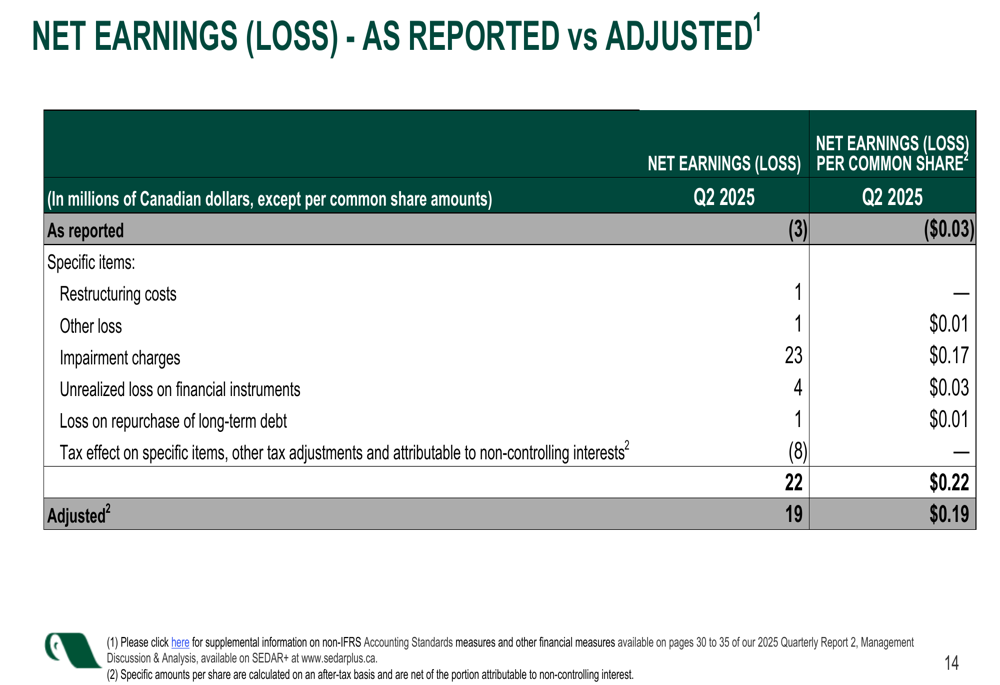

Despite the improved operational performance, Cascades reported a net loss of $3 million ($0.03 per share) compared to net earnings of $7 million in Q1 2025 and $1 million in Q2 2024. However, adjusted net earnings, which exclude specific items, increased to $19 million ($0.19 per share) from $13 million ($0.13 per share) in Q1 2025 and $8 million ($0.08 per share) in Q2 2024.

The following reconciliation illustrates the significant impact of specific items on the company’s reported earnings, particularly the $23 million in impairment charges:

Segment Performance Analysis

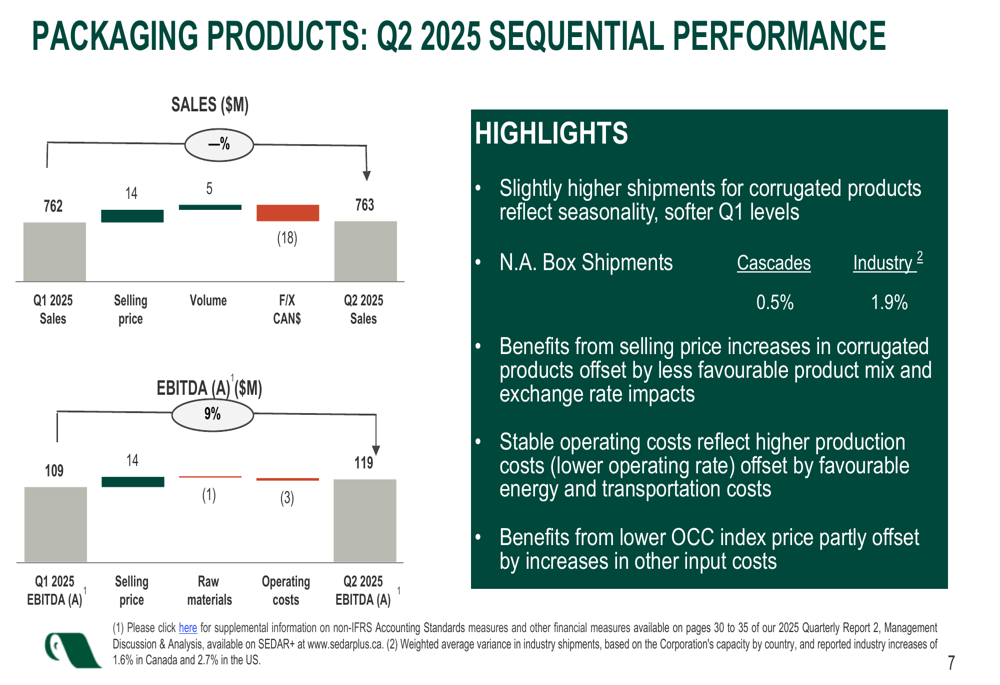

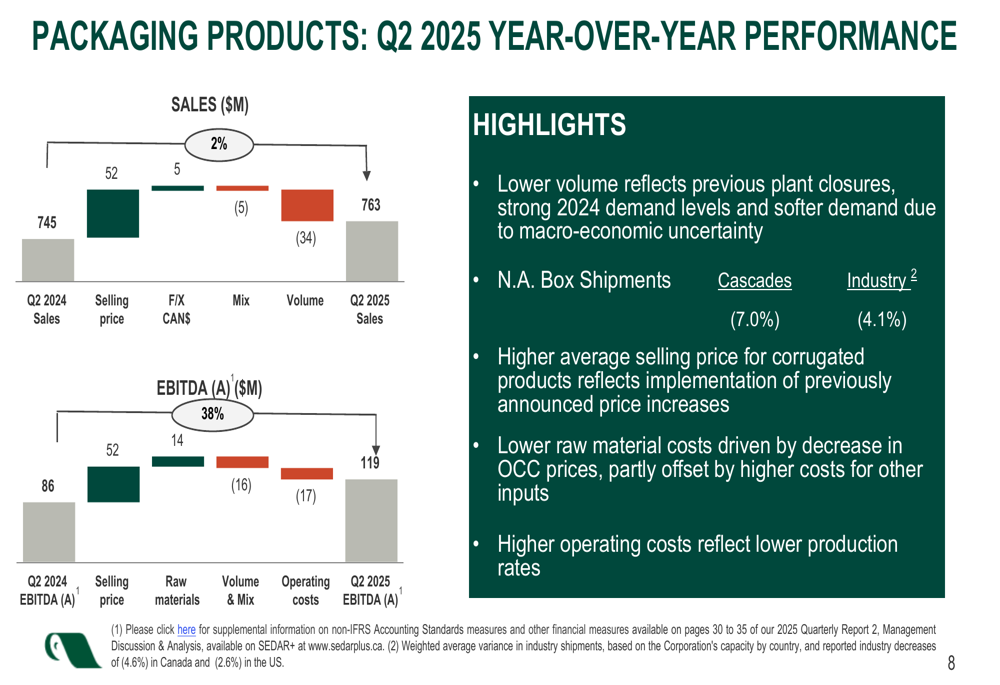

The packaging products segment, which represents the largest portion of Cascades’ business, showed strong performance with EBITDA(A) of $119 million, up from $109 million in Q1 2025 and $86 million in Q2 2024. This improvement came despite relatively flat sales of $763 million.

The following waterfall chart illustrates the key drivers of the sequential improvement in the packaging segment’s EBITDA:

Year-over-year, the packaging segment’s performance was even more impressive, with EBITDA(A) increasing by 38.4% from $86 million in Q2 2024 to $119 million in Q2 2025, driven primarily by higher selling prices and lower raw material costs:

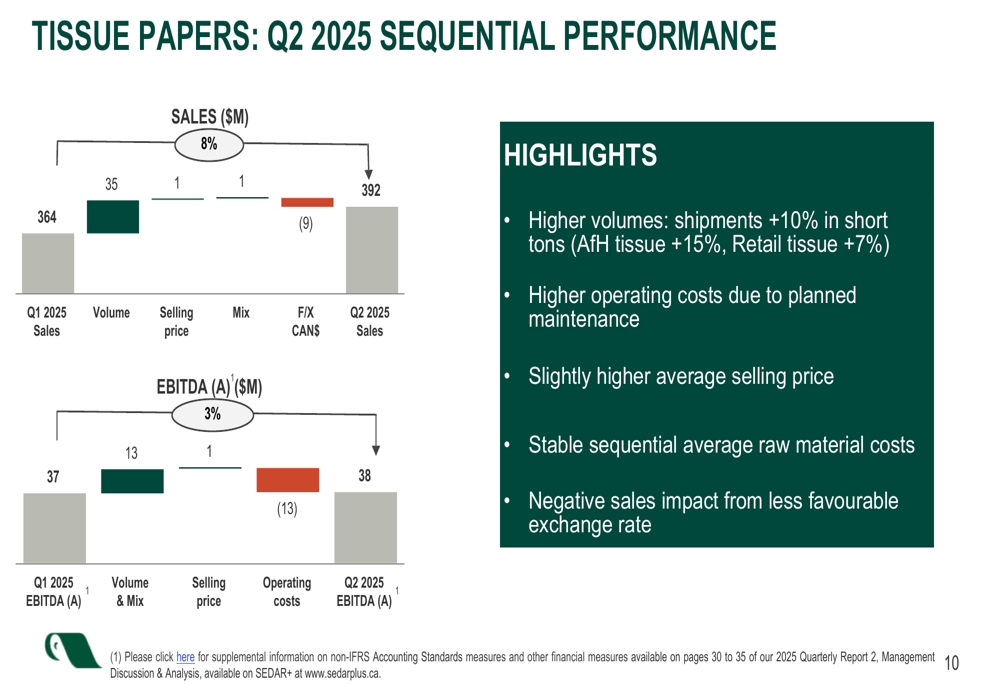

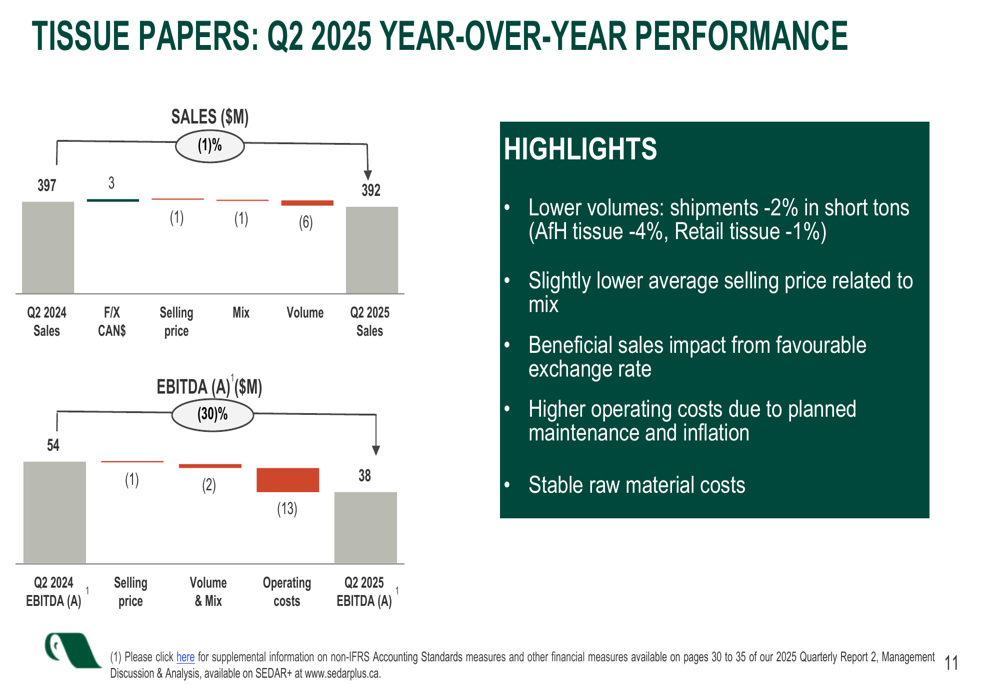

The tissue papers segment showed more modest results, with EBITDA(A) of $38 million, slightly up from $37 million in Q1 2025 but down from $54 million in Q2 2024. Sequential sales increased by 7.7% to $392 million, driven primarily by higher volumes.

As shown in the following chart, the sequential improvement in tissue segment EBITDA was driven by volume and mix, offset by higher operating costs:

Year-over-year, the tissue segment faced challenges, with EBITDA(A) declining by 29.6% from $54 million in Q2 2024 to $38 million in Q2 2025, primarily due to higher operating costs:

Debt Reduction Progress

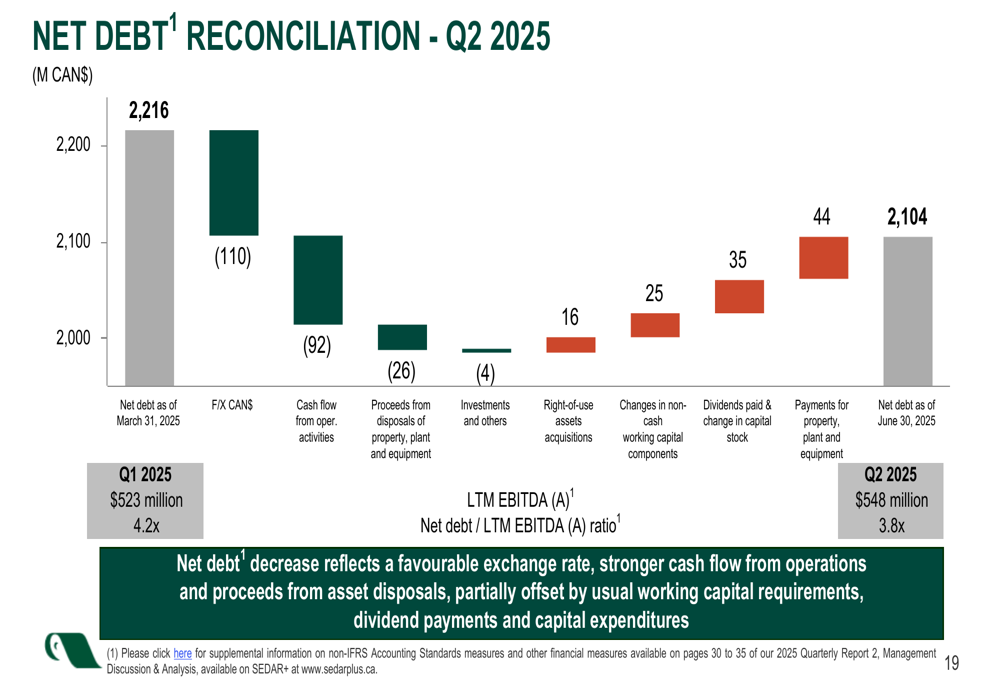

A significant highlight of the quarter was Cascades’ progress in reducing its debt burden. Net debt decreased to $2,104 million from $2,216 million at the end of Q1 2025, while the net debt to EBITDA ratio improved to 3.8x from 4.2x.

The following waterfall chart illustrates the key drivers of the $112 million reduction in net debt during the quarter:

This improvement represents a notable turnaround from the first quarter, when the company reported an increase in net debt of $120 million due to working capital needs, as mentioned in its Q1 2025 earnings call.

Strategic Initiatives & Outlook

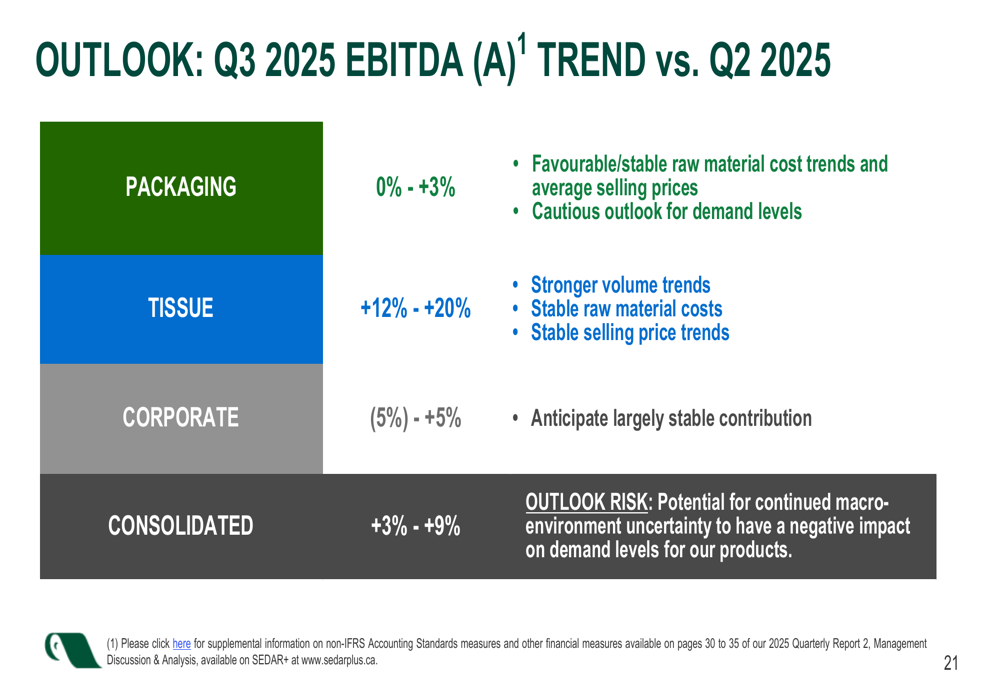

Looking ahead to the third quarter of 2025, Cascades provided a cautiously optimistic outlook, projecting consolidated EBITDA(A) growth of 3% to 9% compared to Q2 2025. The tissue segment is expected to lead this growth with a projected 12% to 20% increase in EBITDA(A), while the packaging segment is forecast to deliver 0% to 3% growth.

As shown in the following outlook summary, the company expects favorable or stable raw material costs and selling prices, while maintaining a cautious stance on demand levels:

Cascades also outlined its strategic priorities for 2025-2026, focusing on strengthening its culture of excellence to drive $100 million in annual run-rate baseline profitability improvements by year-end 2026, aligning its operational and commercial structure, and prioritizing debt reduction in its capital deployment strategy.

While the company continues to face challenges from macroeconomic uncertainty and softer demand, the Q2 2025 results show progress in improving profitability metrics and reducing debt, providing some encouragement after the disappointing first quarter performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.