NextEra Energy stock rises after Google power deal report

Introduction & Market Context

Cellnex Telecom (BME:CLNX) SA (BME:CLNX) presented its H1 2025 results on August 1, showcasing a recovery from its disappointing Q1 performance. The European telecom infrastructure giant reported solid organic growth across key metrics, helping to stabilize investor sentiment after shares had dipped following Q1 results that missed forecasts.

The company’s stock closed at €31.00 on July 31, down 1.18% ahead of the results presentation, and remains closer to its 52-week low of €28.39 than its high of €37.31. This performance reflects ongoing market concerns despite the improved results presented in the H1 slides.

Quarterly Performance Highlights

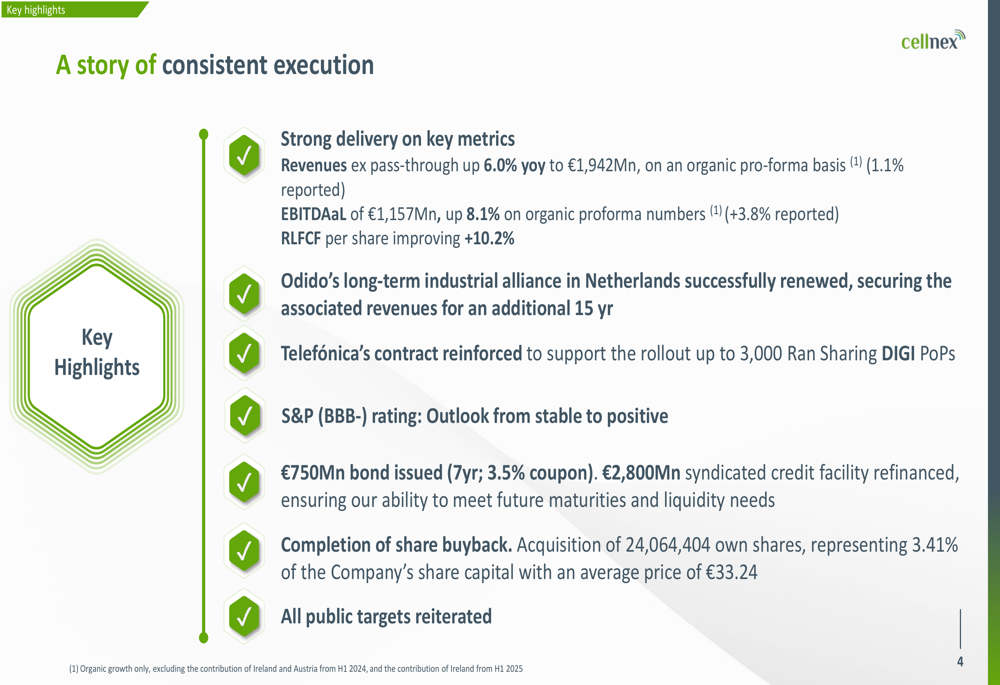

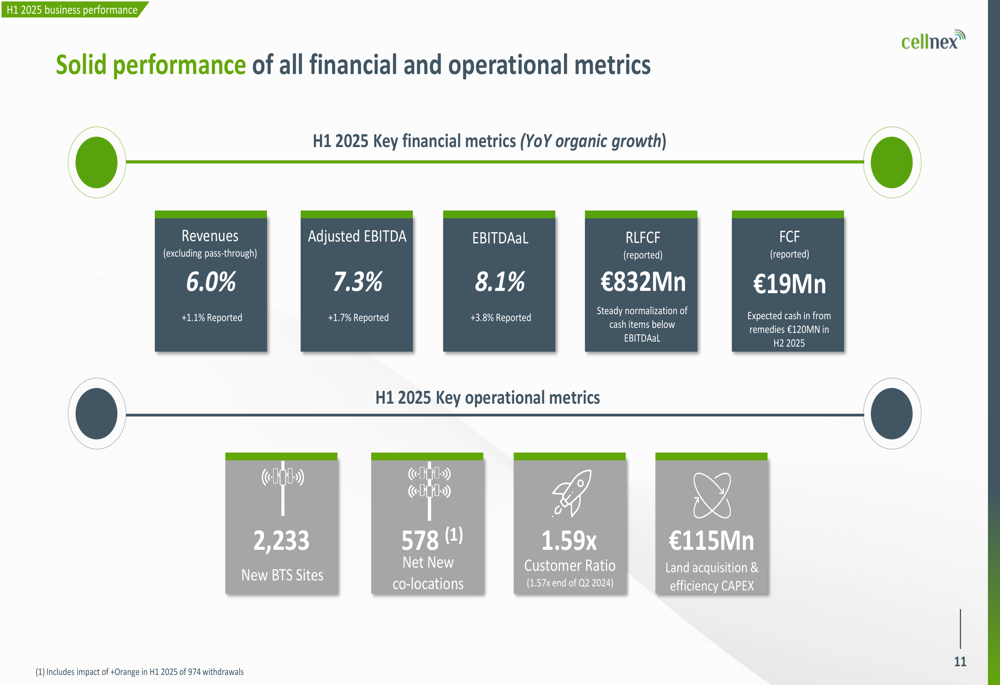

Cellnex reported strong delivery on key financial metrics for H1 2025, with revenues excluding pass-through costs increasing by 6.0% year-over-year to €1,942 million on an organic pro-forma basis. This represents a significant improvement from Q1 performance, when the company missed revenue forecasts by $116 million.

EBITDAaL (EBITDA after leases) reached €1,157 million, up 8.1% on organic pro-forma numbers, while RLFCF (Recurring Levered Free Cash Flow) per share improved by 10.2% compared to the same period last year.

As shown in the following key highlights from the presentation:

The company also highlighted solid operational metrics, including the deployment of 2,233 new BTS (Build-to-Suit) sites and 578 net new co-locations. The customer ratio stands at 1.59x, demonstrating Cellnex’s ability to attract multiple tenants to its infrastructure.

These operational achievements are illustrated in the following slide:

Strategic Initiatives

A significant portion of the presentation focused on Cellnex’s strategic contract renewals and new agreements, which strengthen the company’s long-term business outlook and revenue visibility.

The company successfully renewed its long-term industrial alliance with Odido in the Netherlands for an additional 15 years with CPI-linked terms. Additionally, Cellnex reinforced its contract with Telefónica to support the rollout of up to 3,000 RAN Sharing DIGI Points of Presence (PoPs), along with the deployment of 110 additional physical PoPs.

These strategic agreements are detailed in the following slide:

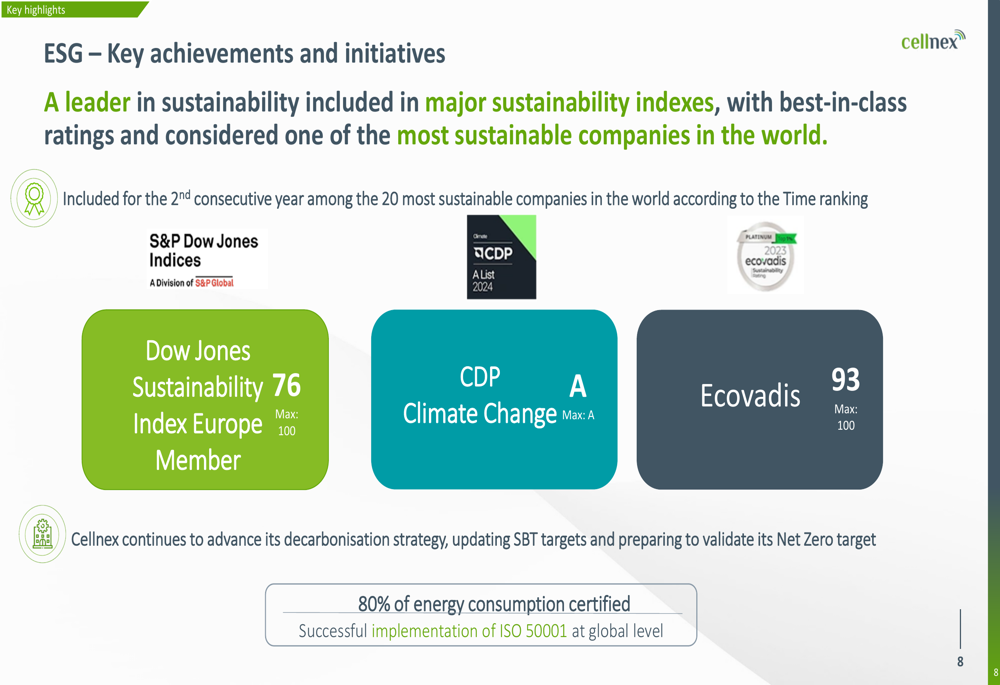

Cellnex also highlighted its ESG achievements, positioning itself as a leader in sustainability. The company has been included in major sustainability indexes with best-in-class ratings and is considered one of the most sustainable companies globally according to Time magazine’s ranking. Notably, 80% of Cellnex’s energy consumption is certified, and the company has successfully implemented ISO 50001 at a global level.

The company’s sustainability credentials are showcased here:

Detailed Financial Analysis

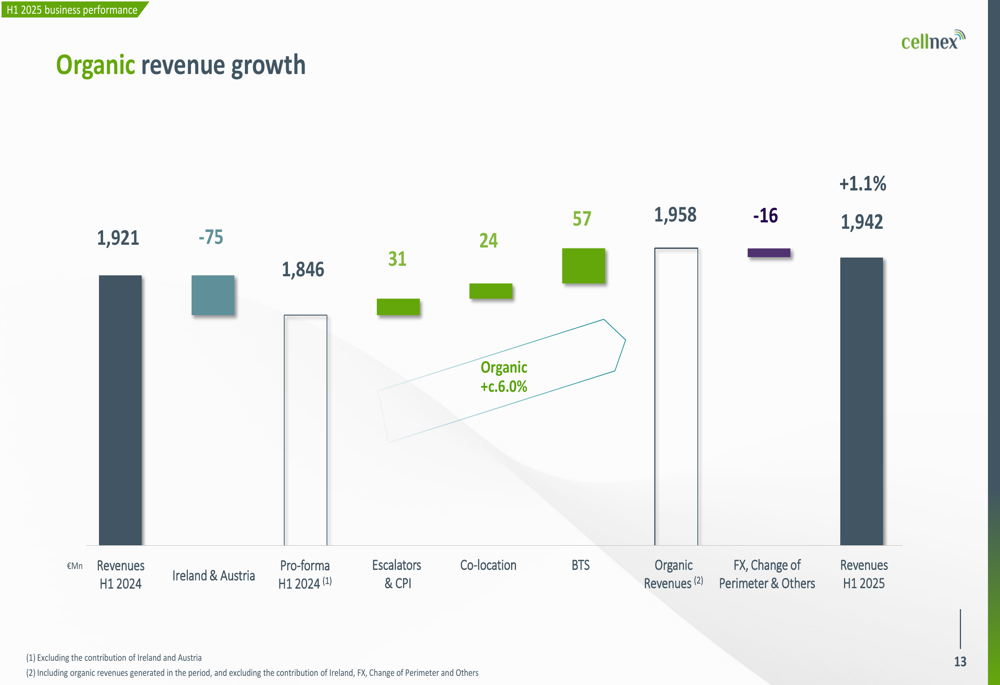

The presentation provided a detailed breakdown of Cellnex’s organic revenue growth, illustrating how various factors contributed to the overall performance. Despite the divestment of operations in Ireland and Austria, which reduced revenues by €75 million, the company achieved organic growth through escalators and CPI adjustments (€31 million), co-location (€24 million), and BTS deployments (€57 million).

This waterfall chart clearly shows the components of revenue growth:

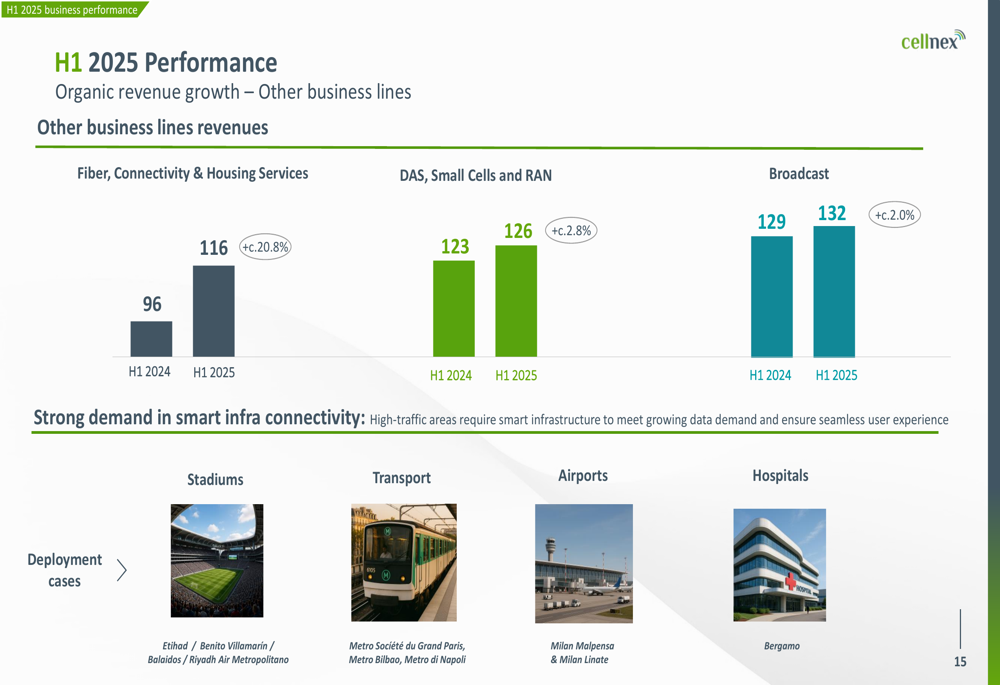

Beyond its core towers business, Cellnex reported impressive growth in other business lines. Fiber, Connectivity & Housing Services grew by approximately 20.8%, while DAS, Small Cells and RAN increased by 2.8%, and Broadcast by 2.0%. This diversification strategy helps reduce dependence on the traditional towers business and opens new growth avenues.

The growth in these alternative business lines is illustrated here:

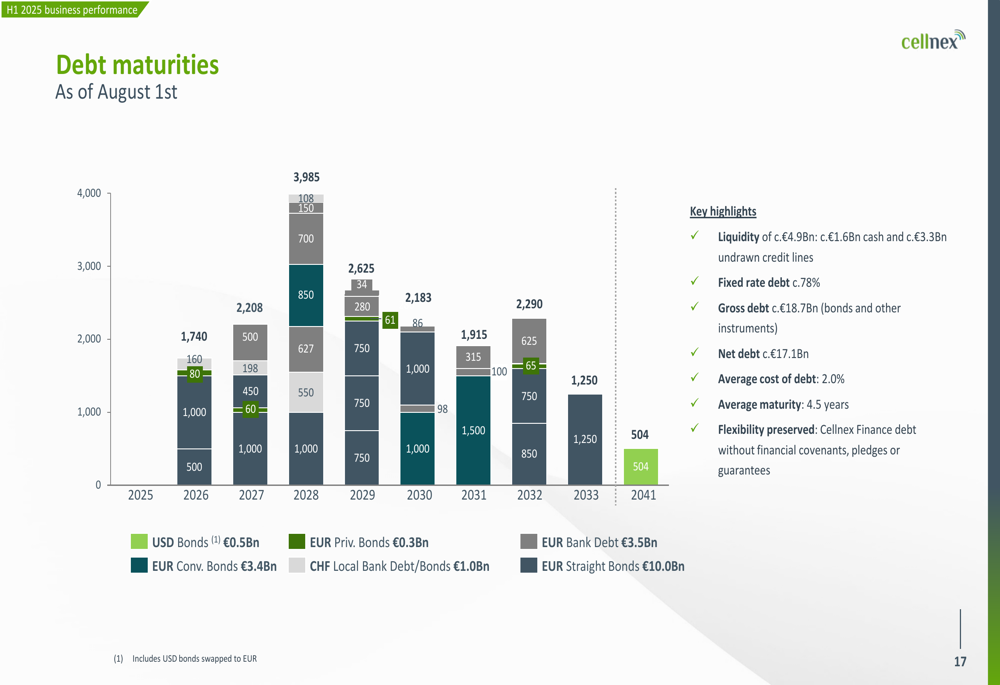

The company also demonstrated strong financial discipline in managing its debt profile. Cellnex maintained a liquidity position of approximately €4.9 billion, comprising €1.6 billion in cash and €3.3 billion in undrawn credit lines. The average cost of debt stands at 2.0% with an average maturity of 4.5 years. Notably, S&P improved its outlook on Cellnex’s BBB- rating from stable to positive, reflecting the company’s strengthening financial position.

The debt maturity profile is shown in the following slide:

Forward-Looking Statements

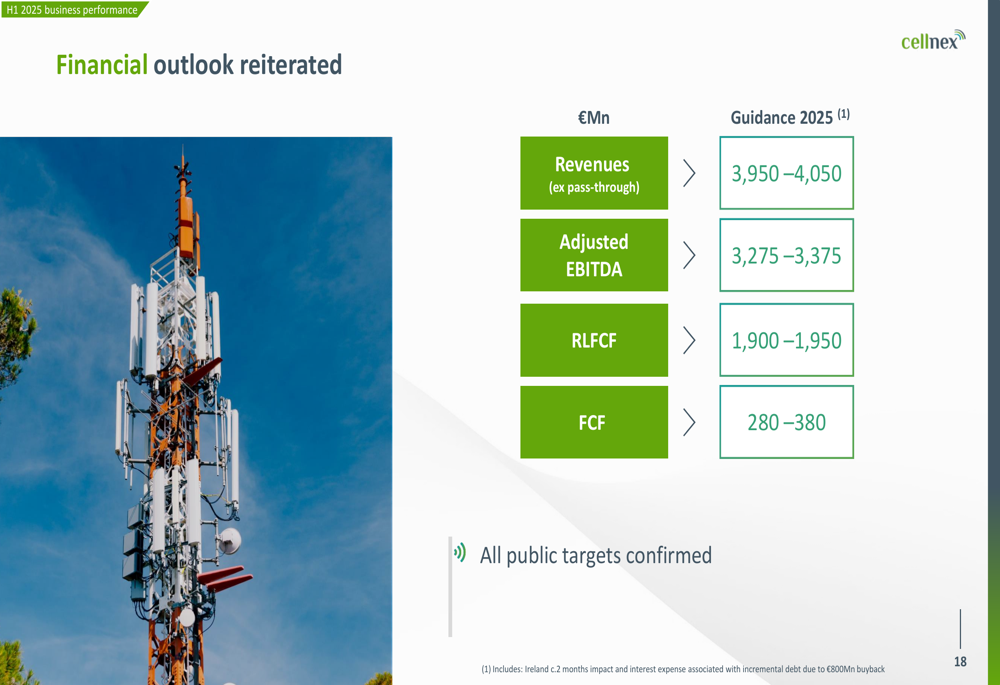

Despite missing Q1 2025 forecasts earlier in the year, Cellnex has reiterated its financial outlook for the full year 2025. The company continues to target revenues (excluding pass-through) of €3,950-4,050 million, adjusted EBITDA of €3,275-3,375 million, RLFCF of €1,900-1,950 million, and FCF of €280-380 million.

This confirmed guidance suggests management’s confidence in continued strong performance through the second half of 2025, as illustrated in this slide:

Conclusion

Cellnex’s H1 2025 presentation demonstrates a company recovering from early-year challenges, with strong organic growth across key metrics and strategic contract renewals that enhance long-term revenue visibility. The improved S&P outlook and solid operational performance indicate that the company is successfully executing its business strategy despite the competitive European telecom infrastructure market.

However, investors should note the disconnect between the Q1 earnings miss and the positive H1 results, suggesting a significantly stronger Q2 performance. As Cellnex continues to diversify its business lines and optimize its cost structure, its ability to consistently meet financial targets will be crucial for rebuilding investor confidence and improving stock performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.