Street Calls of the Week

Introduction & Market Context

Chevron Corporation (NYSE:CVX) released its second quarter 2025 earnings presentation on August 1, highlighting record production levels that partially offset the impact of lower oil prices. The company’s stock showed positive momentum in premarket trading, up 0.57% to $152.50, despite reporting lower earnings compared to both the previous quarter and the same period last year.

The energy giant navigated a challenging price environment with Brent crude averaging $68 per barrel in Q2, down from $76 in Q1 2025 and $85 in Q2 2024. This price decline was a significant factor in the company’s year-over-year earnings decrease, though Chevron emphasized its operational achievements and strategic positioning following the Hess acquisition.

Quarterly Performance Highlights

Chevron reported earnings of $2.5 billion ($1.45 per diluted share) for Q2 2025, down from $3.5 billion in Q1 2025 and $4.4 billion in Q2 2024. Adjusted earnings, which exclude special items, came in at $3.1 billion ($1.77 per share).

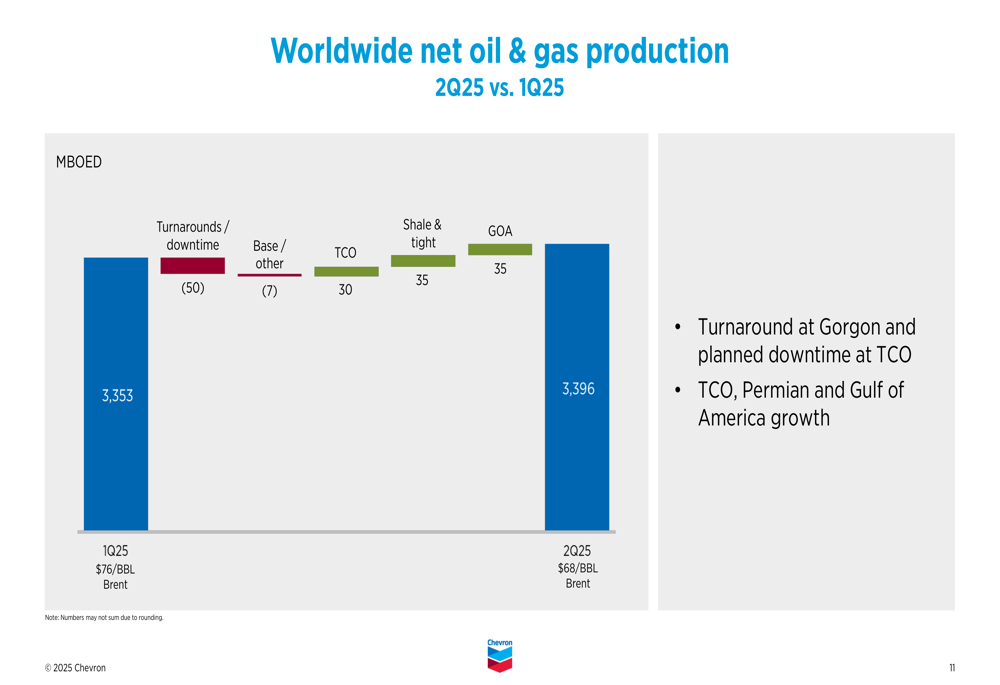

Despite the earnings decline, Chevron achieved record U.S. and worldwide production, reaching 3,396 thousand barrels of oil equivalent per day (MBOED) in Q2, up from 3,353 MBOED in Q1 2025. This production growth was driven by several key assets, including a significant milestone in the Permian Basin.

As shown in the following chart of worldwide net oil and gas production:

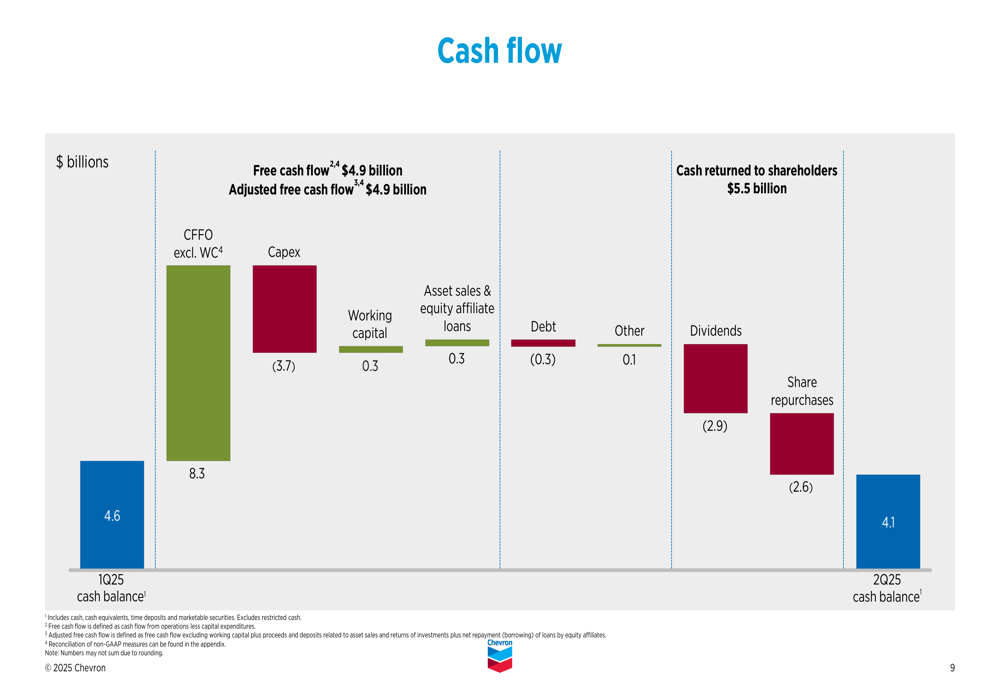

The company generated $8.6 billion in cash flow from operations ($8.3 billion excluding working capital) and returned $5.5 billion to shareholders through dividends ($2.9 billion) and share repurchases ($2.6 billion).

The following cash flow breakdown illustrates how Chevron allocated its resources during the quarter:

Strategic Initiatives and Growth Outlook

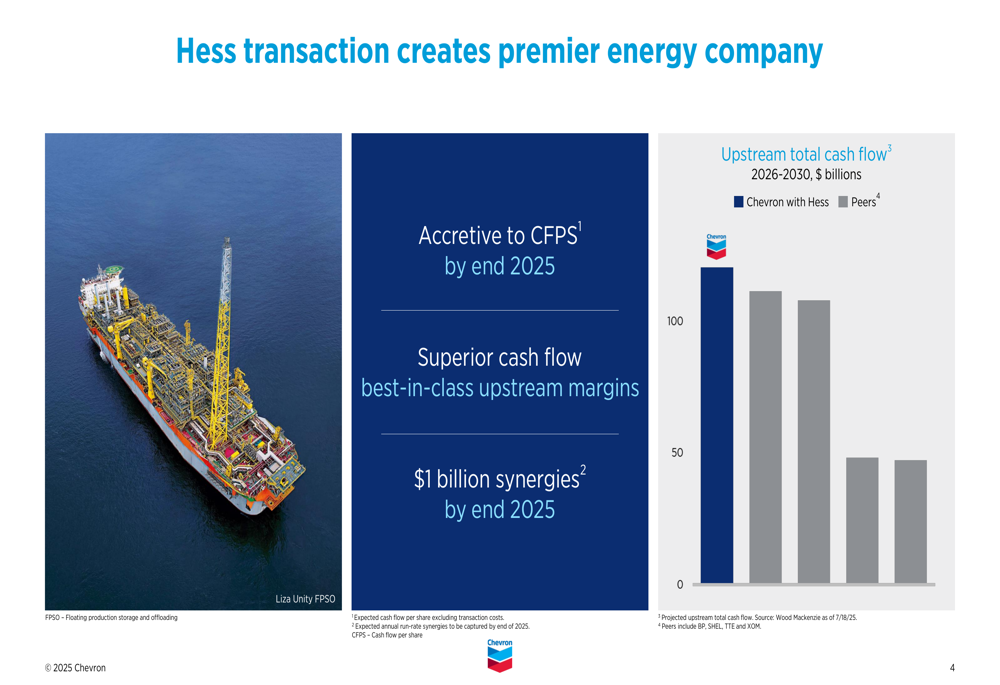

The most significant strategic development in Q2 was the completion of Chevron’s acquisition of Hess Corporation (NYSE:HES), which the company expects to be accretive to cash flow per share by the end of 2025. Management projects $1 billion in synergies by year-end and positions the combined entity as having superior cash flow with best-in-class upstream margins.

The company’s presentation highlighted the projected upstream total cash flow advantage over peers:

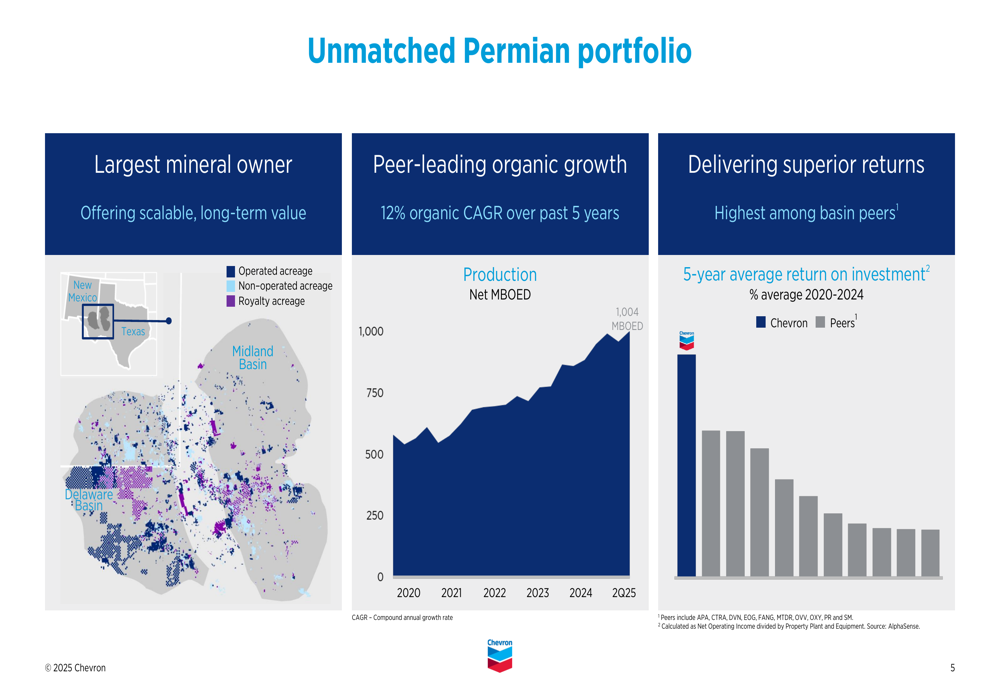

Chevron also celebrated reaching 1 million barrels of oil equivalent per day (MMBOED) in the Permian Basin, reinforcing its position as the largest mineral owner in the region with peer-leading organic growth and superior returns.

The company’s Permian portfolio details are illustrated in this comprehensive slide:

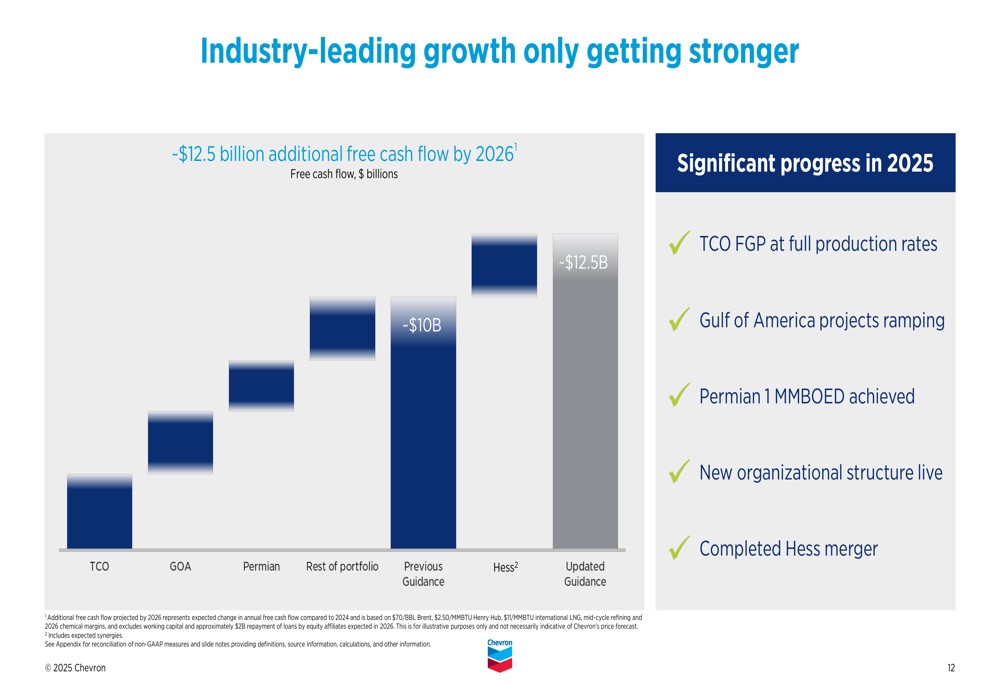

Looking ahead, Chevron projects approximately $12.5 billion in additional free cash flow by 2026 compared to 2024 levels, driven by several growth initiatives including TCO reaching full production rates, Gulf of America projects ramping up, and the Permian Basin achievement.

The components of this projected growth are broken down in the following chart:

Detailed Financial Analysis

Chevron’s Q2 2025 financial performance reflects the impact of lower oil prices offset by production increases. The company maintained a strong balance sheet with debt and net debt ratios of 16.8% and 14.8%, respectively.

Return on capital employed (ROCE) was 6.2% for the quarter, with adjusted ROCE at 7.5%. Total (EPA:TTEF) capital expenditures were $3.7 billion, with organic capex at $3.5 billion.

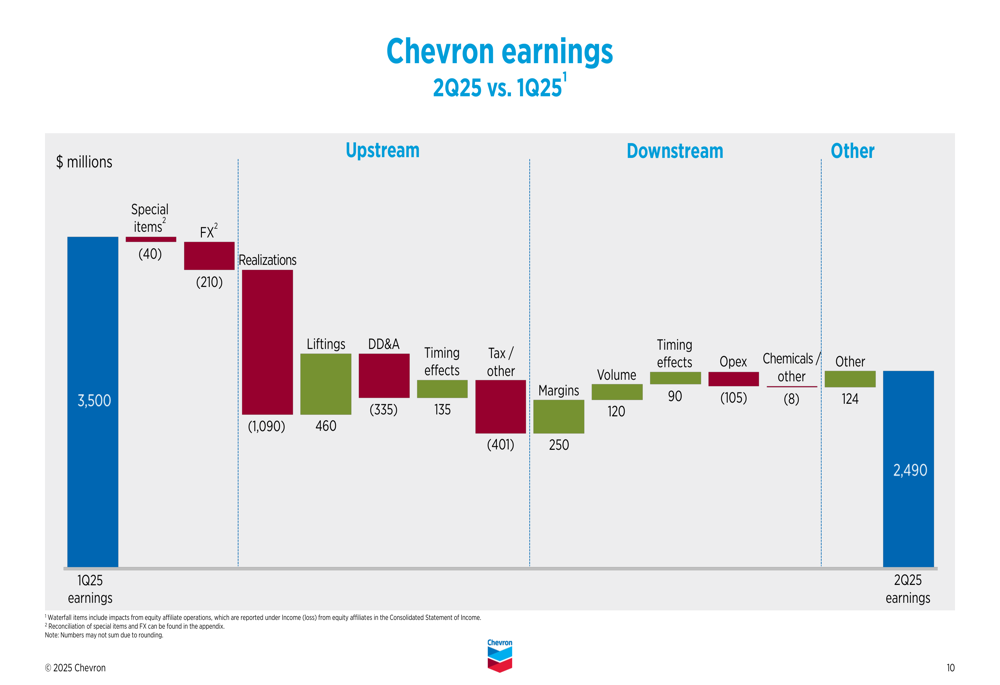

The following waterfall chart breaks down the factors contributing to the earnings change from Q1 to Q2 2025:

In the upstream segment, lower realizations (prices) were the primary driver of reduced earnings, partially offset by higher production volumes. Downstream earnings improved quarter-over-quarter, benefiting from higher refining margins and stronger throughput at U.S. West Coast facilities.

Forward-Looking Statements

For the third quarter of 2025, Chevron provided guidance including expected turnarounds and downtime of approximately 60 MBOED and associated earnings impact of $(200)-(250) million. The company projects share repurchases of $2.5-3.0 billion for Q3, consistent with Q2 levels.

Regarding the Hess integration, Chevron expects production from Hess assets to be 450-500 MBOED in the second half of 2025, with capital expenditures of $2.0-2.5 billion for these assets.

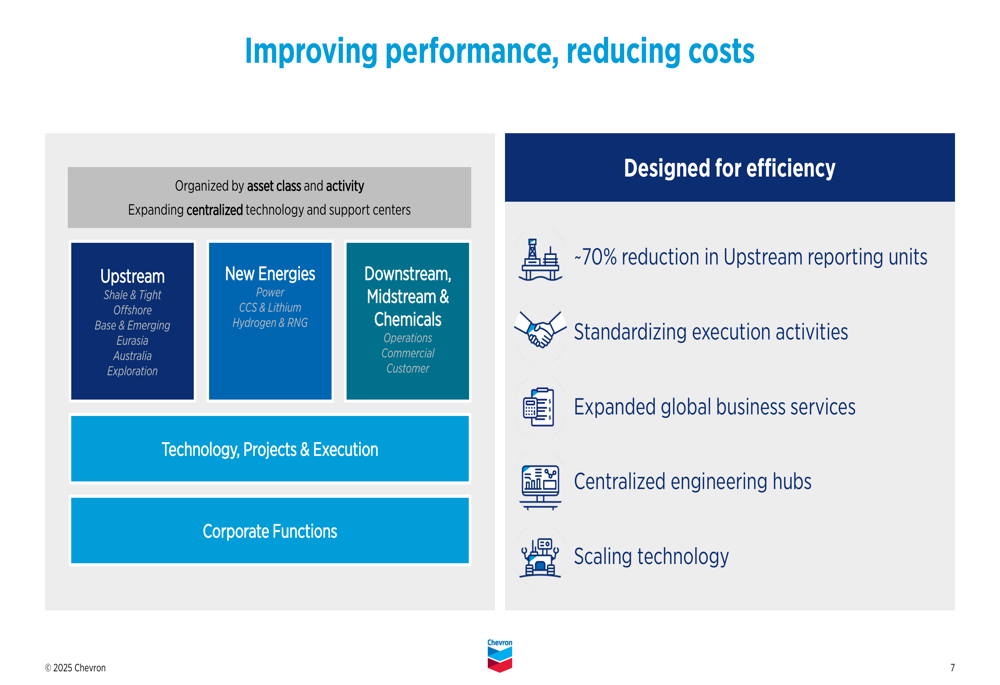

The company highlighted its efforts to improve performance and reduce costs through organizational restructuring, with approximately 70% reduction in upstream reporting units and expanded centralized technology and support centers:

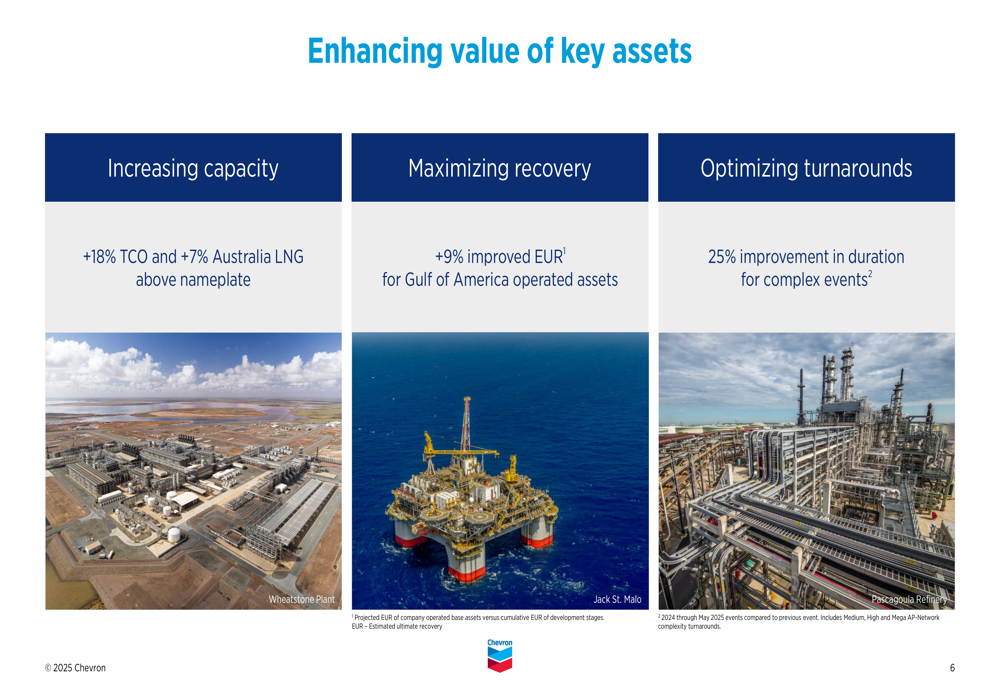

Chevron continues to enhance the value of key assets by increasing capacity, maximizing recovery, and optimizing turnarounds, as illustrated in this slide:

While the quarter’s earnings reflect the challenges of a lower price environment, Chevron’s presentation emphasized its long-term positioning, operational achievements, and financial discipline as it integrates the Hess acquisition and advances its growth strategy across its global portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.