Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Cirrus Logic (NASDAQ:CRUS) presented its Investor Relations Update on August 5, 2025, highlighting the company’s financial performance for Q1 FY26 and providing guidance for Q2 FY26. The Austin, Texas-based semiconductor company, which specializes in analog and mixed-signal integrated circuits, reported continued momentum in its core audio business while making significant strides in diversifying its product portfolio.

The presentation comes after Cirrus Logic reported strong Q4 FY25 results in its previous earnings release, where it beat analyst expectations with earnings per share of $1.67 against the forecasted $1.18. The company’s stock has been trading in a 52-week range of $75.83 to $147.46, with the current price around $105.58, reflecting investor confidence in its growth strategy.

Quarterly Performance Highlights

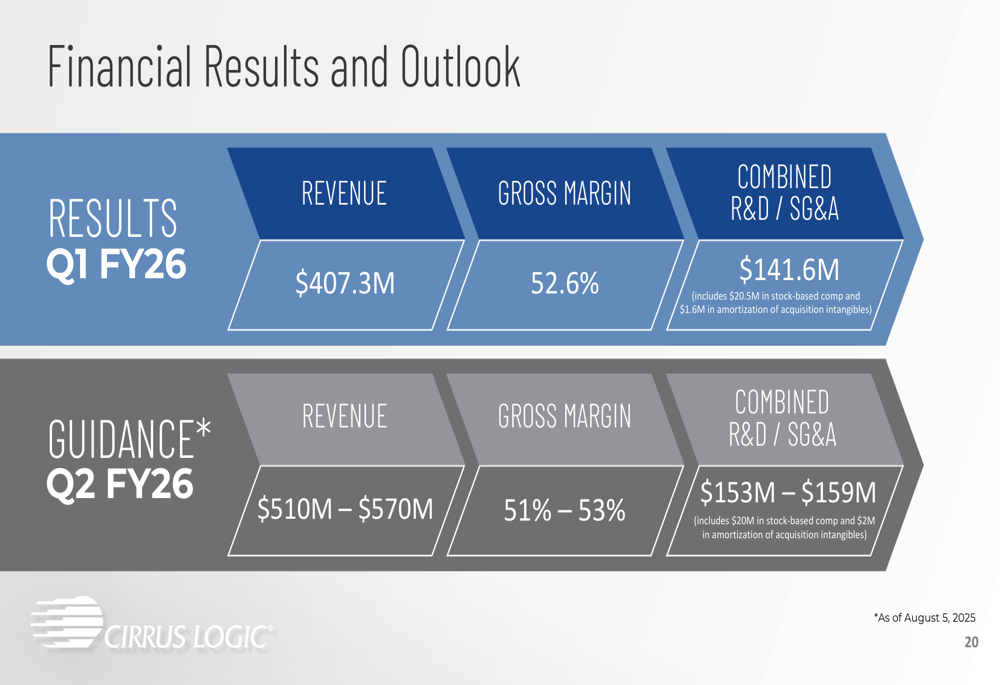

Cirrus Logic reported Q1 FY26 revenue of $407.3 million, exceeding the company’s previous guidance range of $330-390 million. The gross margin came in at a healthy 52.6%, while combined R&D and SG&A expenses totaled $141.6 million, including $20.5 million in stock-based compensation and $1.6 million in amortization of acquisition intangibles.

For the upcoming Q2 FY26, Cirrus Logic provided optimistic guidance, projecting revenue between $510 million and $570 million, with gross margin expected to remain strong at 51-53%.

As shown in the following financial results and outlook:

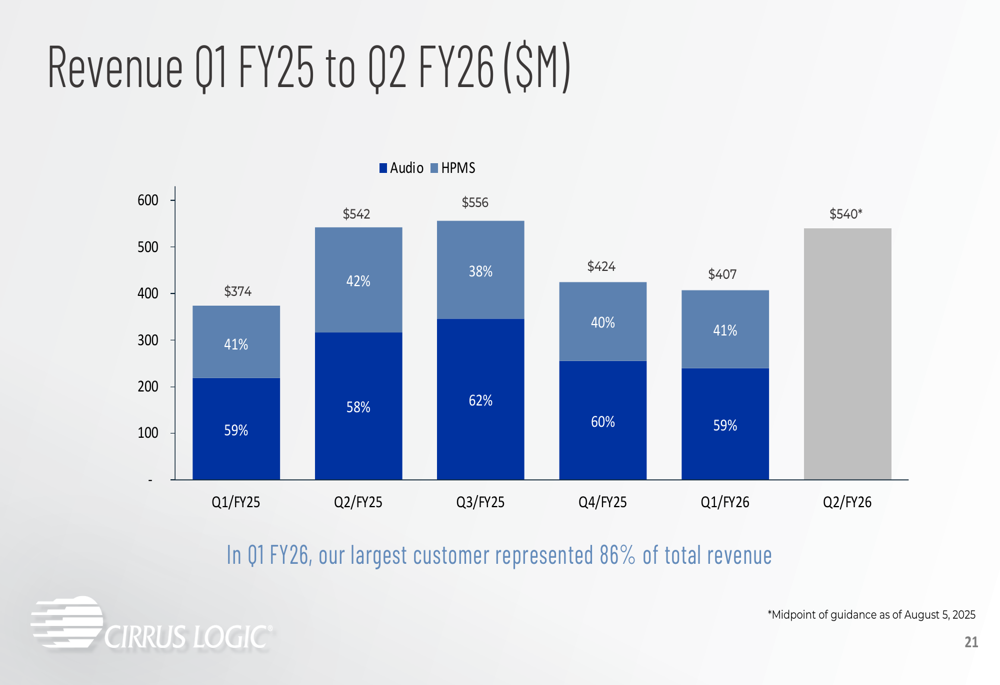

The company’s revenue breakdown reveals that audio products continue to be the largest segment, representing 59% of total revenue in Q1 FY26, while High-Performance Mixed-Signal (HPMS) products accounted for 41%. This ratio has remained relatively stable over the past year, indicating consistent performance across product categories.

The revenue trend over the past six quarters shows seasonal fluctuations typical in the semiconductor industry, with stronger performance in the second and third quarters of each fiscal year:

Notably, Cirrus Logic disclosed that its largest customer represented 86% of total revenue in Q1 FY26, highlighting the company’s significant customer concentration risk. This customer is widely understood to be Apple Inc. (NASDAQ:AAPL), though not explicitly named in the presentation.

Strategic Initiatives

A central theme of the presentation was Cirrus Logic’s strategy to expand its addressable market and reduce customer concentration through product diversification. The company is leveraging its core strengths in audio and mixed-signal processing to enter new markets and applications.

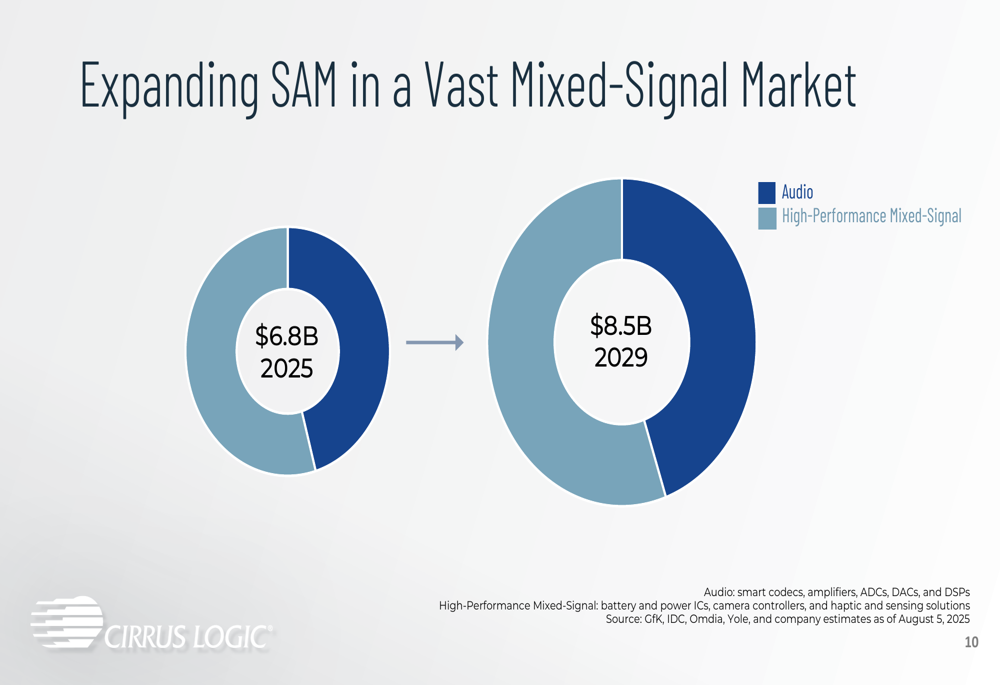

The presentation highlighted the company’s expanding Served Addressable Market (SAM), which is projected to grow from $6.8 billion in 2025 to $8.5 billion by 2029, representing a significant growth opportunity:

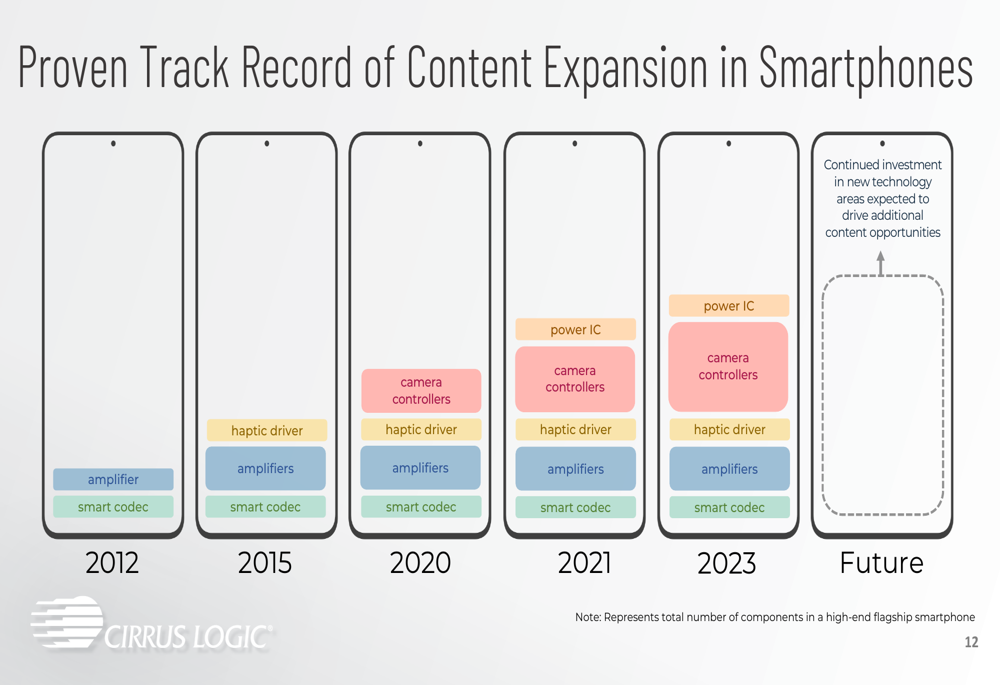

Cirrus Logic’s growth strategy focuses on three key pillars: maintaining leadership in smartphone audio, increasing HPMS content in smartphones, and leveraging audio and HPMS strengths to expand into new applications and markets. The company has demonstrated a consistent track record of increasing component content in smartphones over time:

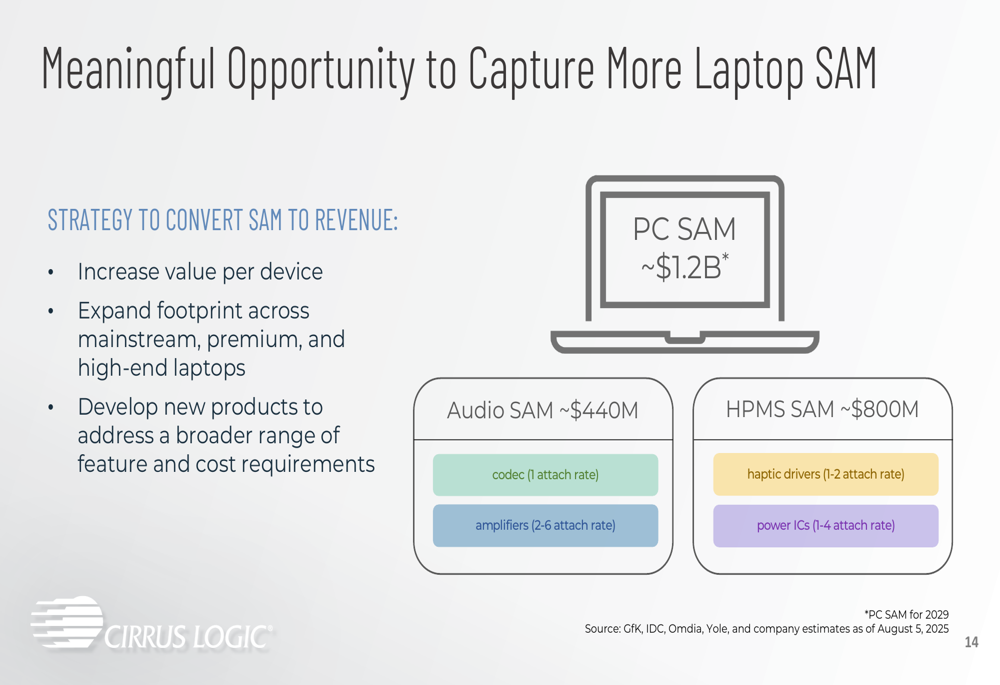

Beyond smartphones, Cirrus Logic is targeting substantial opportunities in the laptop market, with a projected SAM of approximately $1.2 billion by 2029. The company’s strategy includes increasing value per device, expanding its footprint across laptop segments, and developing new products to address various feature and cost requirements:

Detailed Financial Analysis

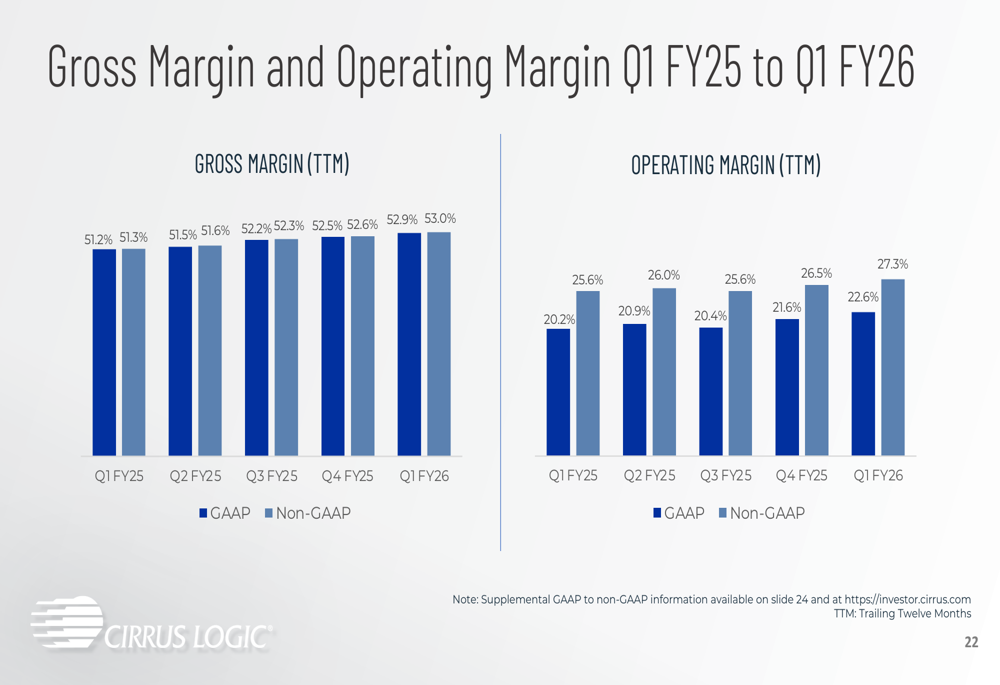

Cirrus Logic’s financial performance shows strength across multiple metrics. The company’s gross margin and operating margin have been trending upward on both GAAP and non-GAAP bases:

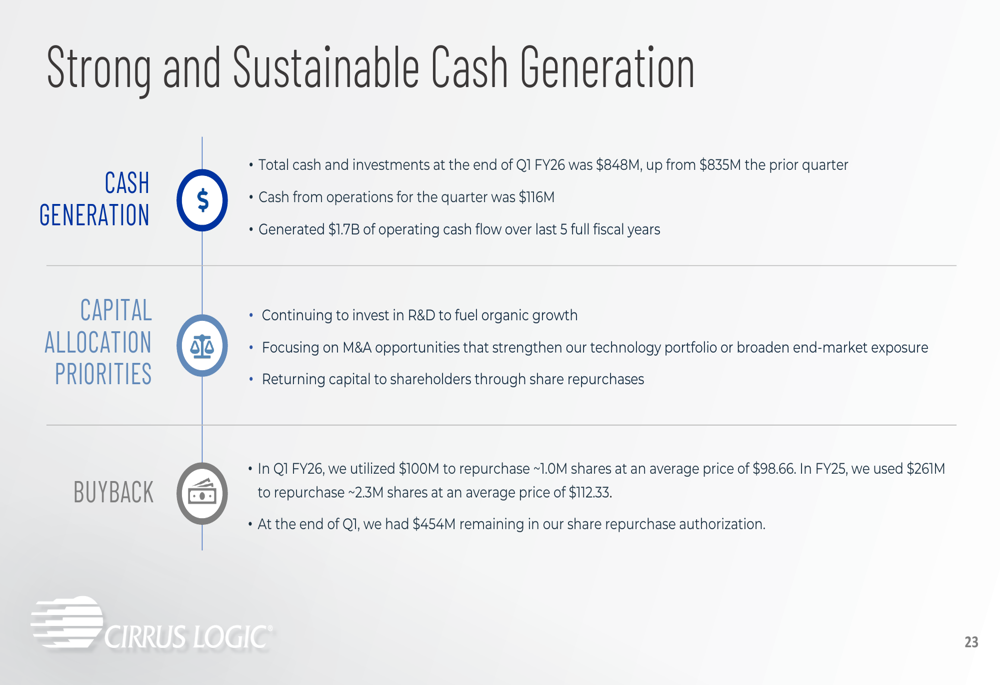

Cash generation remains a significant strength for Cirrus Logic. The company reported total cash and investments of $848 million at the end of Q1 FY26, up from $835 million in the previous quarter. Cash from operations for the quarter was robust at $116 million, continuing the trend that has generated $1.7 billion in operating cash flow over the past five fiscal years.

The company has been actively returning capital to shareholders through share repurchases. In Q1 FY26, Cirrus Logic used $100 million to repurchase approximately 1 million shares at an average price of $98.66. This follows $261 million used in FY25 to repurchase 2.3 million shares at an average price of $112.33. As of the end of Q1 FY26, $454 million remained in the share repurchase authorization.

Forward-Looking Statements

Looking ahead, Cirrus Logic is positioning itself for continued growth through product diversification and market expansion. The company is investing significantly in high-performance mixed-signal technologies, with over two-thirds of its new patent filings in calendar year 2024 related to this area.

The company’s capital allocation priorities remain focused on investing in R&D to fuel organic growth, pursuing strategic M&A opportunities, and returning capital to shareholders through share repurchases.

While Cirrus Logic faces challenges, including high customer concentration and competitive pressures in the semiconductor industry, its strong financial position, technological capabilities, and expansion strategy provide a solid foundation for future growth. The company’s ability to generate substantial cash flow while investing in new technologies and markets will be critical to its long-term success in reducing dependency on its largest customer and capturing opportunities in emerging markets like laptops, wearables, and automotive applications.

As the company continues to execute on its diversification strategy, investors will be watching closely to see if Cirrus Logic can translate its expanding addressable market into sustainable revenue growth and reduced customer concentration in the coming quarters and years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.