S&P 500 falls as ongoing government shutdown, trade jitters weigh

Introduction & Market Context

Civeo Corporation (NYSE:CVEO), a leading provider of hospitality services for resource industries, presented its third quarter 2024 results and strategic outlook on October 30, 2024. The company, which operates primarily in Canada and Australia, reported mixed performance with its Australian operations showing robust growth while Canadian operations continued to decline. Trading at $23.20 as of September 12, 2025, Civeo’s stock has experienced volatility over the past year, with a 52-week range of $18.01 to $28.92.

Executive Summary

Civeo reported third quarter 2024 revenues of $176.3 million and adjusted EBITDA of $18.8 million, in line with management expectations. The company maintained its full-year 2024 guidance, projecting revenues between $675-$700 million and adjusted EBITDA of $83-$88 million. With a net leverage ratio of just 0.3x as of September 30, 2024, Civeo continues to prioritize shareholder returns through its quarterly dividend of $0.25 per share and ongoing share repurchases.

As shown in the following snapshot of Civeo’s business:

The company’s revenue mix has shifted significantly toward Australia, which now represents 58% of total revenue and 74% of adjusted EBITDA for the last twelve months ended September 30, 2024. This geographic rebalancing reflects Civeo’s strategic pivot toward the growing Australian market, particularly in integrated services.

Quarterly Performance Highlights

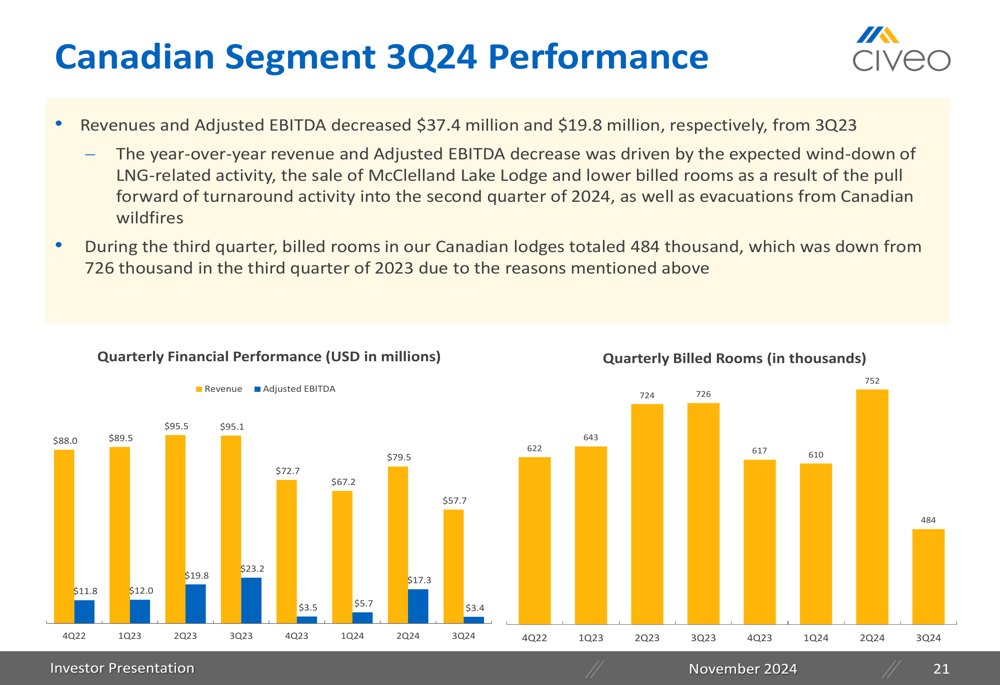

Civeo’s third quarter results revealed contrasting performance between its two primary markets. The Canadian segment experienced significant declines, with revenues and adjusted EBITDA decreasing by $37.4 million and $19.8 million, respectively, compared to Q3 2023. This downturn was primarily attributed to the wind-down of LNG activity, the sale of McClelland Lake Lodge, and lower billed rooms, which fell to 484,000 from 726,000 in the prior year period.

The following chart illustrates the Canadian segment’s declining performance:

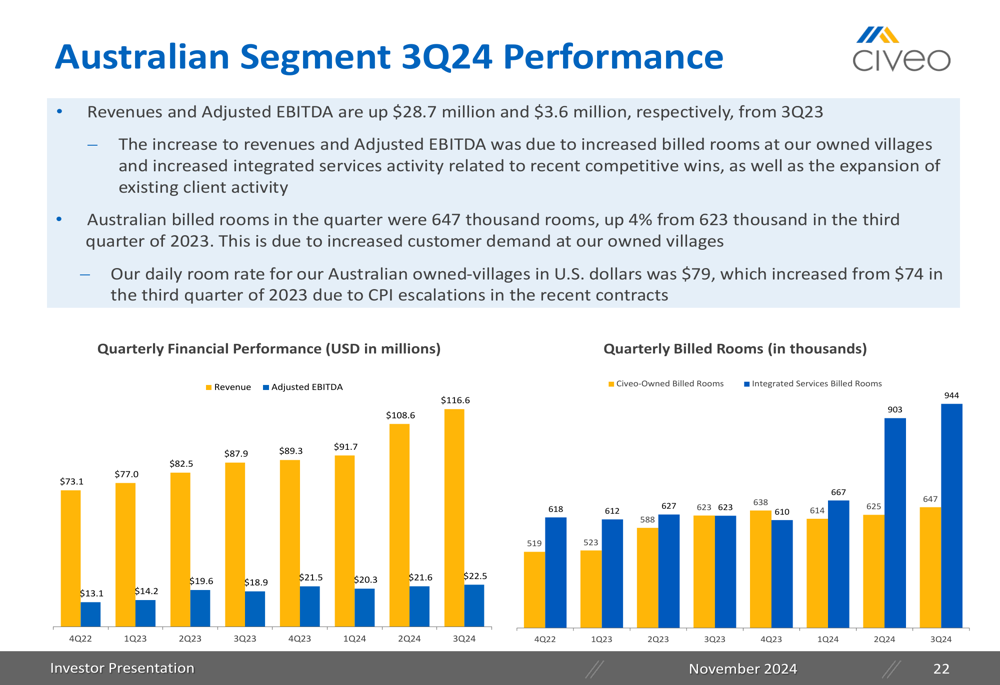

In contrast, the Australian segment demonstrated strong growth, with revenues increasing by $28.7 million and adjusted EBITDA rising by $3.6 million compared to Q3 2023. This improvement was driven by increased billed rooms, which grew 4% to 647,000, and expanded integrated services activity. The daily room rate for Australian owned-villages also improved to $79, up from $74 in the same period last year.

The Australian segment’s performance is detailed in this chart:

Strategic Initiatives

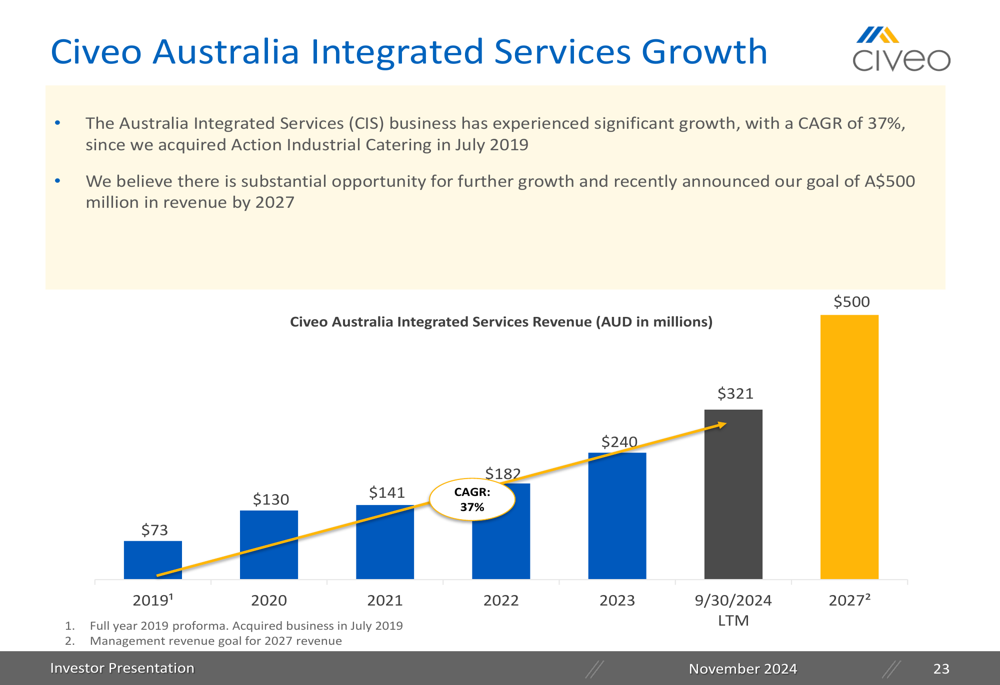

Civeo’s strategic focus has clearly shifted toward expanding its Australian operations, particularly in integrated services. Since acquiring Action Industrial Catering in July 2019, this business has grown at a compound annual growth rate of 37%, reaching A$321 million in the last twelve months ended September 30, 2024. The company has set an ambitious target of A$500 million in Australian revenue by 2027.

The following chart demonstrates this impressive growth trajectory:

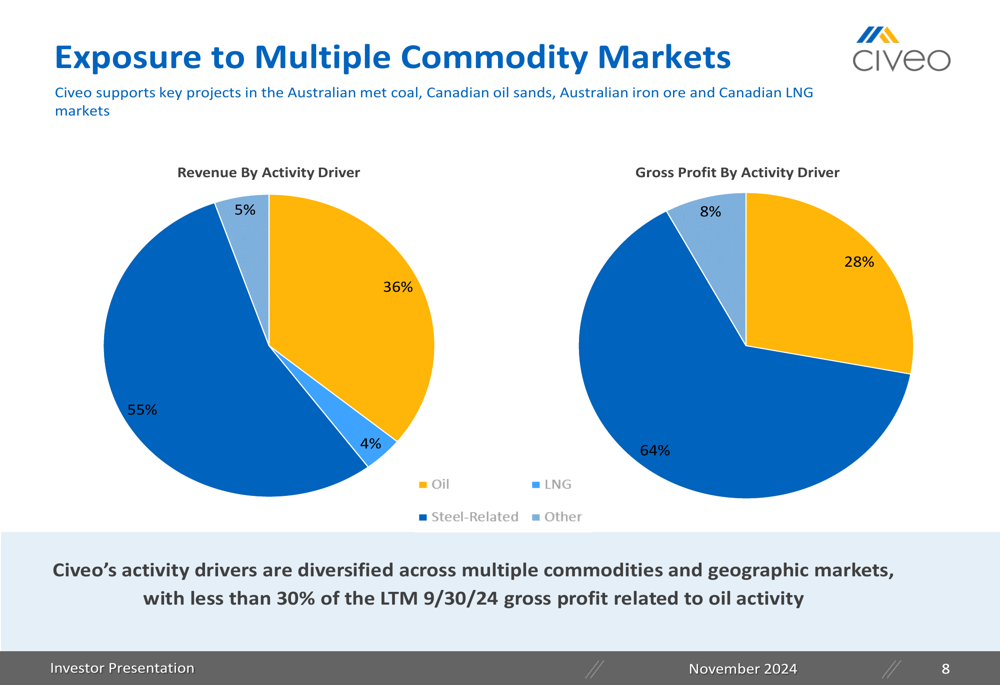

Civeo’s business model benefits from diversification across multiple commodity markets, reducing its exposure to any single sector. As illustrated in the revenue breakdown, the company derives 55% of revenue from steel-related activities, 36% from LNG, 5% from oil, and 4% from other sources. This diversification provides stability to cash flows despite volatility in individual commodity markets.

Financial Position and Capital Allocation

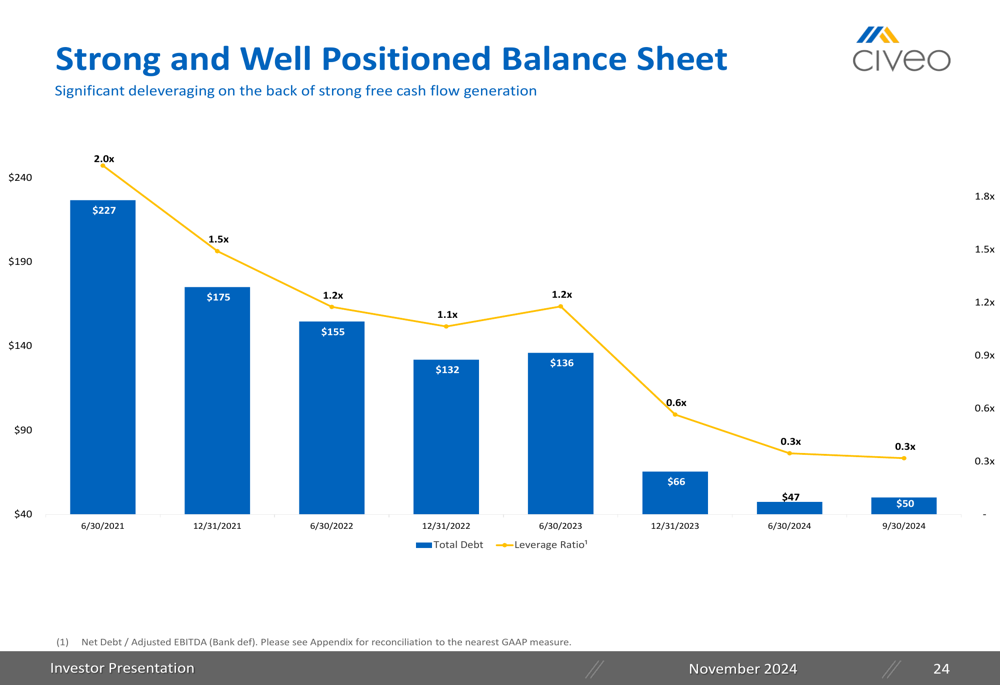

Civeo has maintained a strong balance sheet, with consistent deleveraging over the past three years. The net leverage ratio has declined from 2.0x in June 2021 to just 0.3x as of September 30, 2024, providing significant financial flexibility for future growth initiatives and shareholder returns.

The company’s deleveraging progress is shown here:

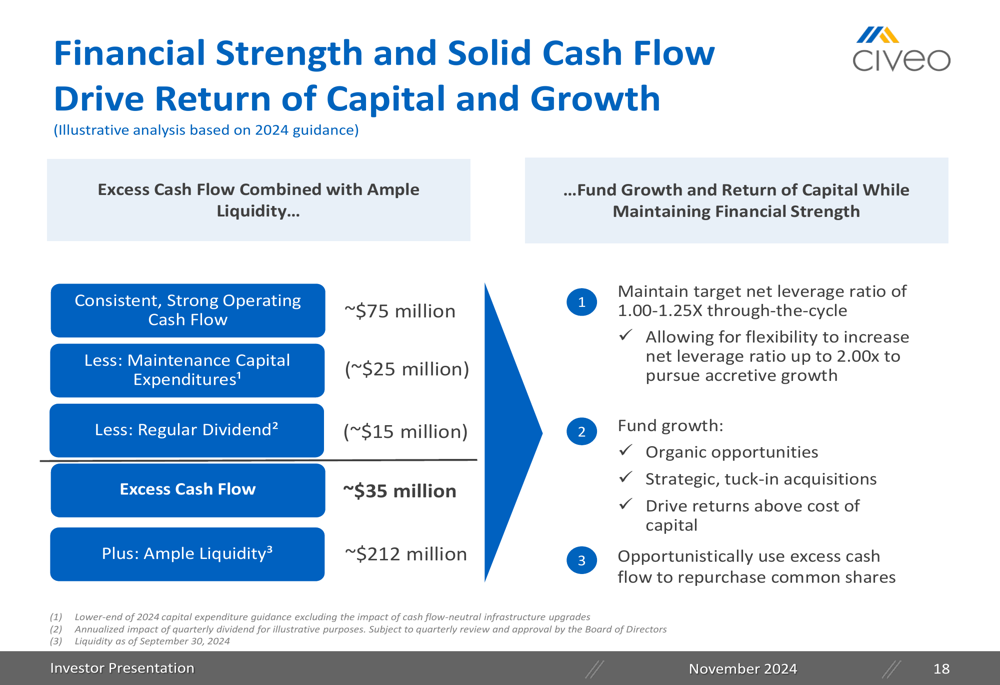

This strong financial position supports Civeo’s capital allocation strategy, which balances growth investments, particularly in Australia, with shareholder returns through dividends and share repurchases. The company expects to generate approximately $75 million in operating cash flow annually, with about $35 million in excess cash flow after accounting for maintenance capital expenditures and dividend payments.

Civeo’s capital allocation framework is detailed below:

During the third quarter, the company repurchased 515,000 common shares for approximately $14.2 million, continuing its commitment to returning capital to shareholders. Civeo has repurchased the equivalent of 3.2 million shares, or 19.1% of fully diluted outstanding shares, for approximately $85 million over time.

Forward-Looking Statements

Looking ahead, Civeo has maintained its full-year 2024 guidance, projecting revenues of $675-$700 million, adjusted EBITDA of $83-$88 million, capital expenditures of $30-$35 million, and free cash flow of $50-$60 million. The company expects to maintain its target net leverage ratio of 1.00-1.25x through the cycle while continuing to fund growth opportunities and return capital to shareholders.

However, investors should note that Civeo’s financial position appears to have deteriorated significantly after this presentation. According to a recent earnings article covering Q2 2025 results, the company reported a net loss of $0.25 per share, missing forecasts of $0.08 EPS. Net debt reportedly increased, with management targeting "a year-ending leverage ratio of approximately two times" – a substantial increase from the 0.3x reported in this presentation. This suggests potential challenges in maintaining the strong financial position highlighted in the Q3 2024 presentation.

Civeo’s strategic focus on growing its Australian operations while managing the decline in Canadian activities appears prudent given the contrasting performance of these segments. The company’s diversified exposure across multiple commodities and geographies provides some resilience, though investors should monitor the apparent increase in leverage and potential challenges in the Canadian market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.