With uncertainty rising, is gold’s bull run far from over?

Introduction & Market Context

Clariane SE (EPA:CLARI) released its H1 2025 results on July 30, showing mixed performance as the company completed its financial restructuring plan six months ahead of schedule. Despite reporting solid organic revenue growth of 4.8%, the company’s stock plunged 13.56% to €4.40 following the announcement, reflecting investor concerns over declining profitability and cash flow generation.

The European care provider, which operates across six countries, achieved significant deleveraging through its €1 billion disposal program but saw its EBITDA decline by 4.1% compared to the same period last year. The company maintained its full-year outlook despite the challenging first half, expecting improved performance in H2 2025.

Financial Performance Highlights

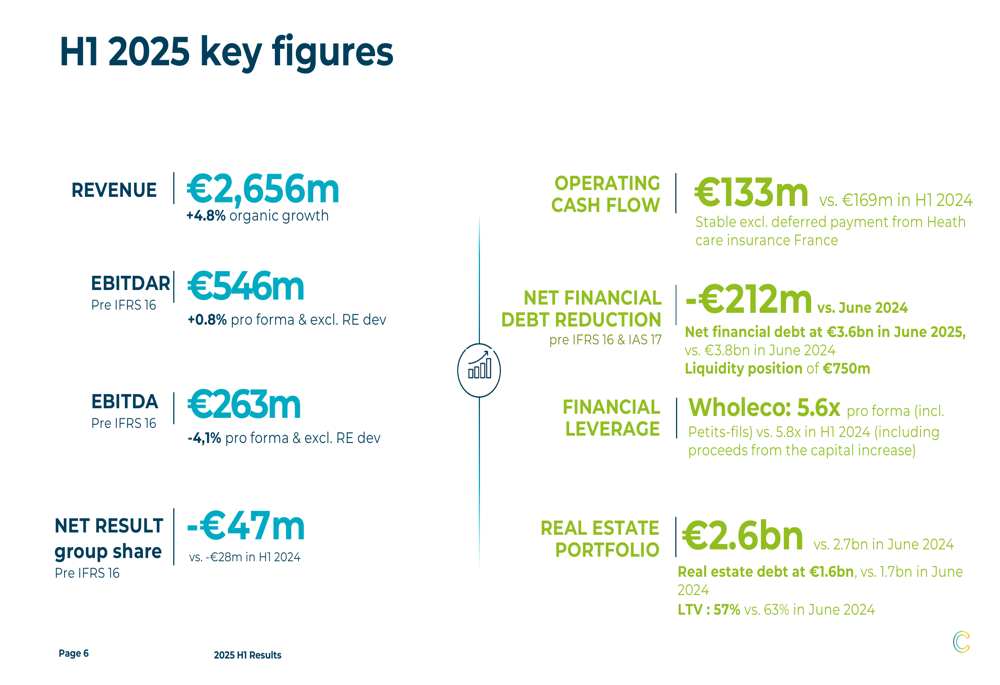

Clariane reported H1 2025 revenue of €2,656 million, representing 4.8% organic growth despite a challenging operating environment. However, profitability metrics showed pressure, with EBITDA declining to €263 million, down 4.1% on a pro forma basis excluding real estate development.

As shown in the following summary of key financial figures:

The company’s net result (group share) deteriorated to -€47 million compared to -€28 million in H1 2024. Operating cash flow also declined to €133 million from €169 million in the prior year period. Management attributed this partly to deferred payments related to the late publication of the 2025 tariff in Specialty Care in France, noting that adjusted for this factor, operating cash flow would have been stable.

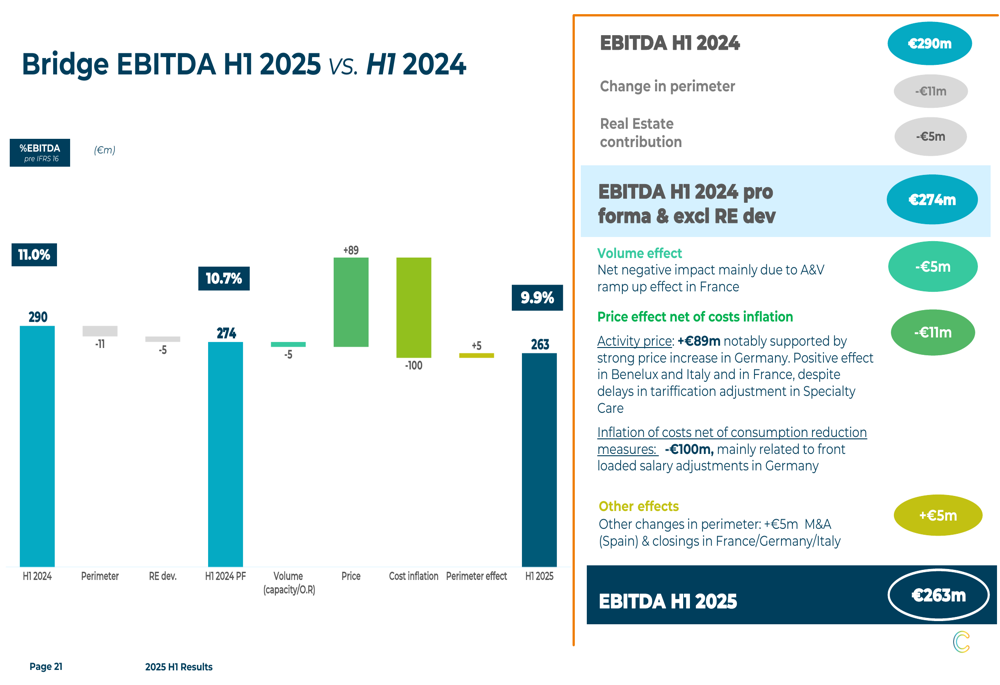

The bridge analysis below illustrates the main factors affecting EBITDA performance:

Strategic Initiatives

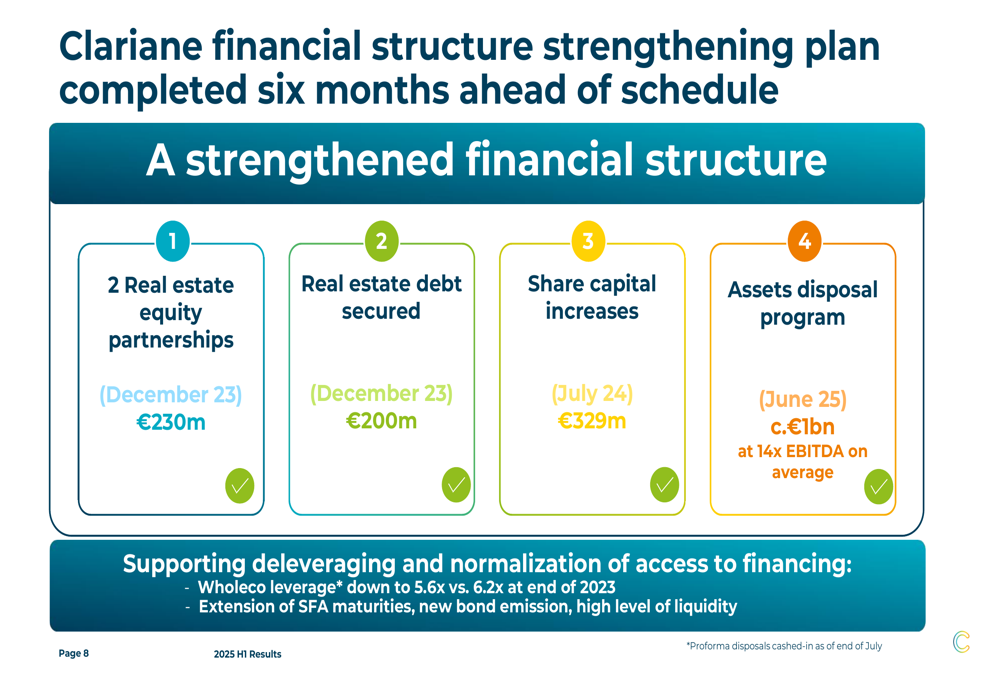

The centerpiece of Clariane’s strategy has been its comprehensive financial structure strengthening plan, which the company completed ahead of schedule. The plan consisted of four key components, including real estate partnerships, secured debt, capital increases, and a significant asset disposal program.

The following chart outlines the key elements of this financial restructuring:

The €1 billion disposal program was executed at an average multiple of 14x EBITDA, with approximately 60% achieved through the sale of operating companies. A notable transaction was the divestiture of Petits-fils, a French home care network, for an enterprise value of €345 million.

The disposal plan has helped reduce Clariane’s debt leverage ratio from 6.2x in December 2023 to 5.6x as of June 2025, with the loan-to-value ratio on real estate assets improving to 57% from 63% a year earlier.

Regional Performance

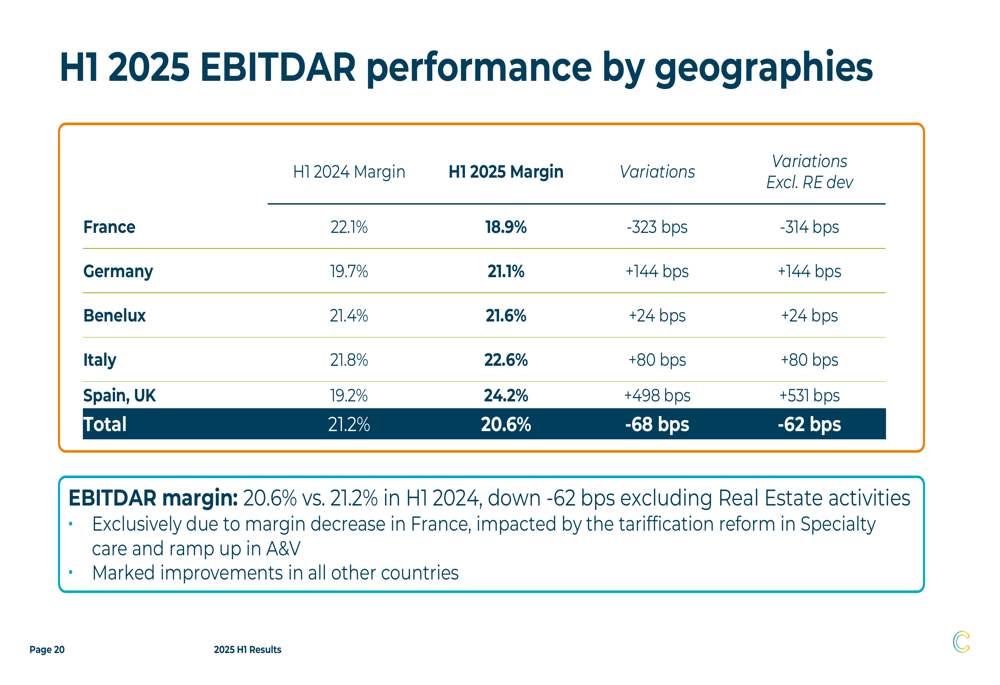

Clariane’s operational performance varied significantly by geography, with France experiencing margin pressure while other regions showed improvement. The company’s long-term care segment, which represents the largest portion of revenue, delivered 5.4% organic growth.

The following table details EBITDAR performance across Clariane’s geographic footprint:

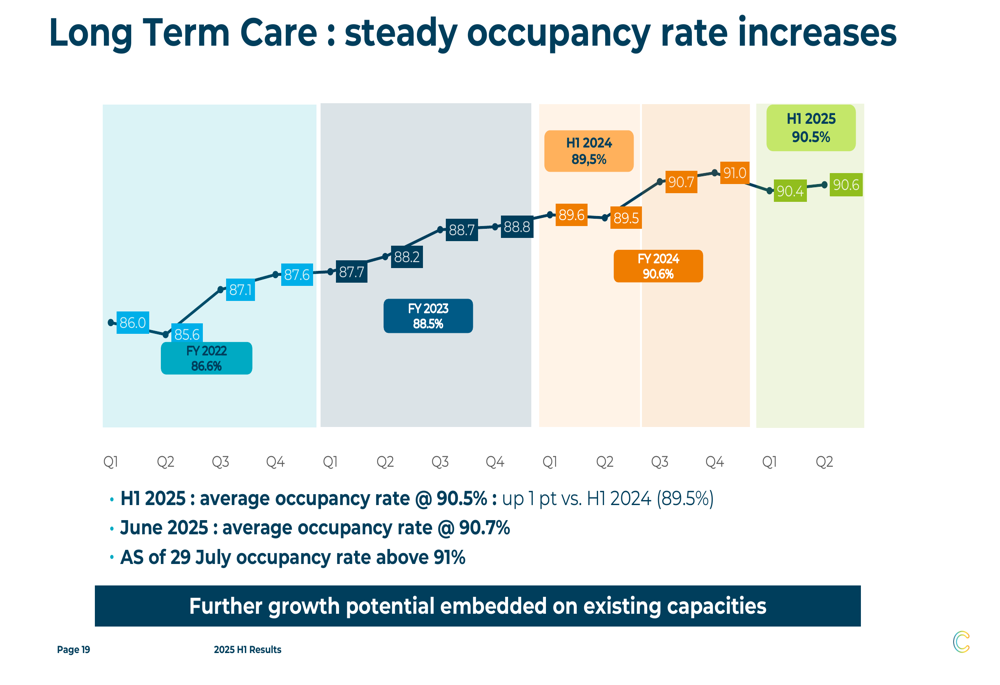

A bright spot in the operational metrics was the steady improvement in occupancy rates, which reached 90.5% in H1 2025, up 1 percentage point from H1 2024. The company reported that occupancy continued to improve, exceeding 91% by late July.

The trend in occupancy rates is illustrated in this chart:

Debt Refinancing and Liquidity

In addition to asset disposals, Clariane has significantly restructured its debt profile. The company successfully issued a €400 million unsecured bond with a 5-year maturity and a 7.875% annual coupon. This issuance attracted substantial investor interest, with an order book exceeding €1.2 billion, representing an oversubscription rate of more than 3 times.

The company also amended and extended its syndicated facility, originally due in May 2026, to a new maturity of May 2029. This includes a €300 million term loan and a €325 million revolving credit facility, along with a new €150 million real estate credit line.

These refinancing activities have extended Clariane’s debt maturity profile and strengthened its liquidity position, which stood at €750 million as of June 30, 2025.

Real Estate Portfolio

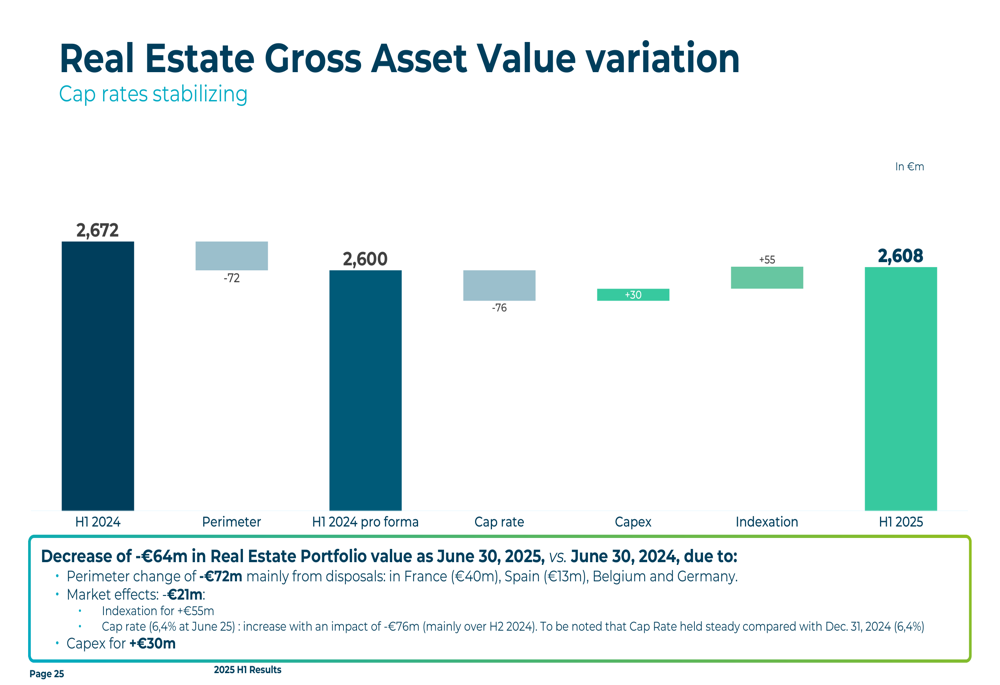

Clariane’s owned real estate portfolio was valued at €2.6 billion as of June 30, 2025, a slight decrease from €2.7 billion a year earlier. The change in value was primarily due to disposals, partially offset by indexation and capital expenditures.

The following chart breaks down the changes in the real estate portfolio value:

Outlook & Forward Guidance

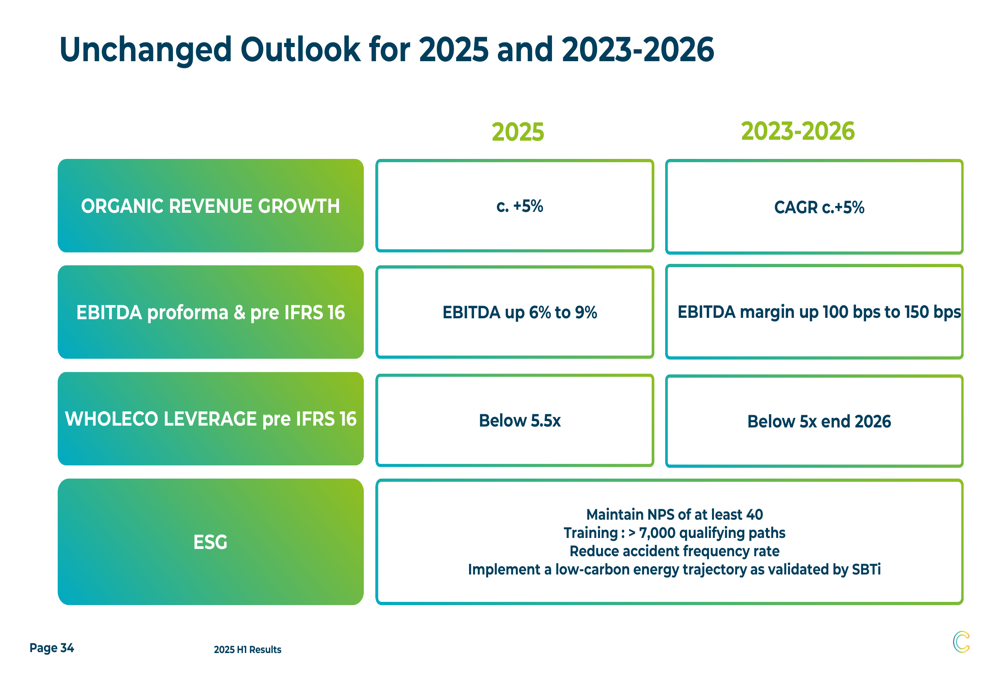

Despite the challenges in H1, Clariane maintained its outlook for 2025 and its medium-term targets for 2023-2026. The company expects approximately 5% organic revenue growth for the full year 2025, with EBITDA growth of 6-9%.

Management anticipates improved performance in H2 2025, driven by:

- Volume increases across all geographies

- Full-year effects of price increases obtained in H1

- Active management of the case mix in Specialty Care in France

- Cost reduction initiatives following the disposal plan

The company’s unchanged outlook is summarized in the following slide:

Conclusion

Clariane’s H1 2025 results present a mixed picture of a company that has successfully executed its financial restructuring strategy but continues to face operational challenges, particularly in its French operations. The significant market reaction suggests investors remain cautious about the company’s ability to deliver on its promised H2 improvement and full-year targets.

While the completion of the €1 billion disposal program ahead of schedule represents a strategic win, the decline in EBITDA and cash flow generation highlights the operational challenges that remain. The company’s ability to leverage its strengthened financial position to drive operational improvements will be critical to restoring investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.