Adaptimmune stock plunges after announcing Nasdaq delisting plans

Introduction & Market Context

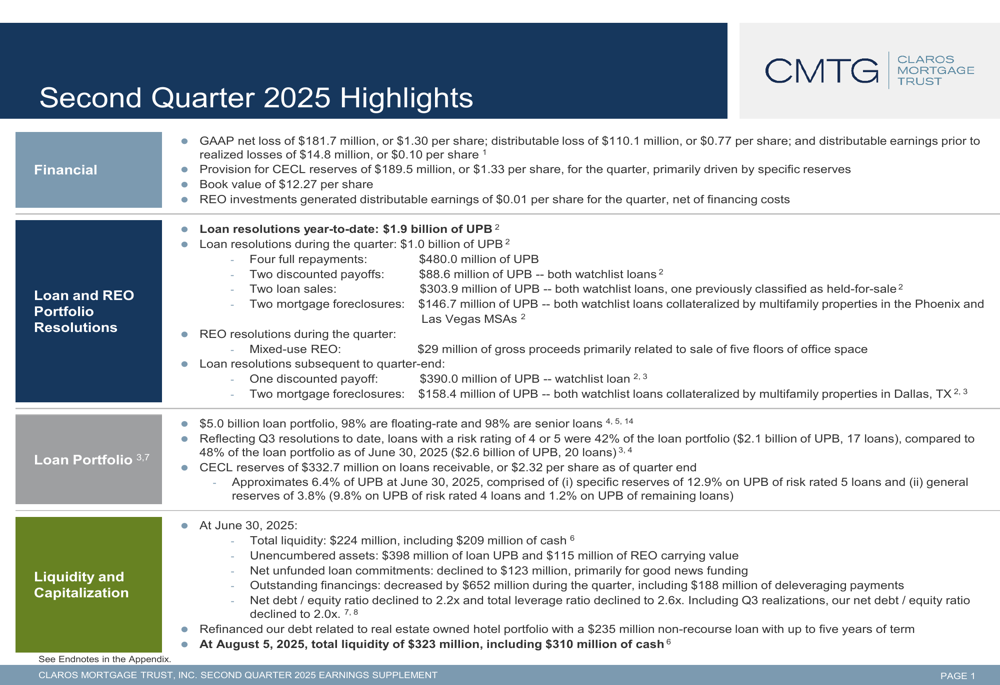

Claros Mortgage Trust Inc (NYSE:CMTG) released its second quarter 2025 earnings presentation on August 6, revealing a significant net loss as the company continues to aggressively resolve troubled loans and build liquidity. The commercial mortgage REIT reported a GAAP net loss of $181.7 million, or $1.30 per share, substantially wider than the previous quarter’s loss of $0.56 per share. The stock closed at $2.86 on August 6, down 1.04% for the day, and has fallen approximately 66% over the past year.

The company’s presentation highlighted its ongoing strategy of deleveraging its portfolio, resolving troubled loans, and strengthening its liquidity position amid continued challenges in commercial real estate markets.

Quarterly Performance Highlights

Claros reported a distributable loss of $110.1 million ($0.77 per share) for Q2 2025, though distributable earnings prior to realized losses were positive at $14.8 million ($0.10 per share). A significant factor in the quarterly loss was a provision for CECL (Current Expected Credit Loss) reserves of $189.5 million, or $1.33 per share, reflecting increased concerns about loan quality.

As shown in the following comprehensive overview of the quarter’s financial performance:

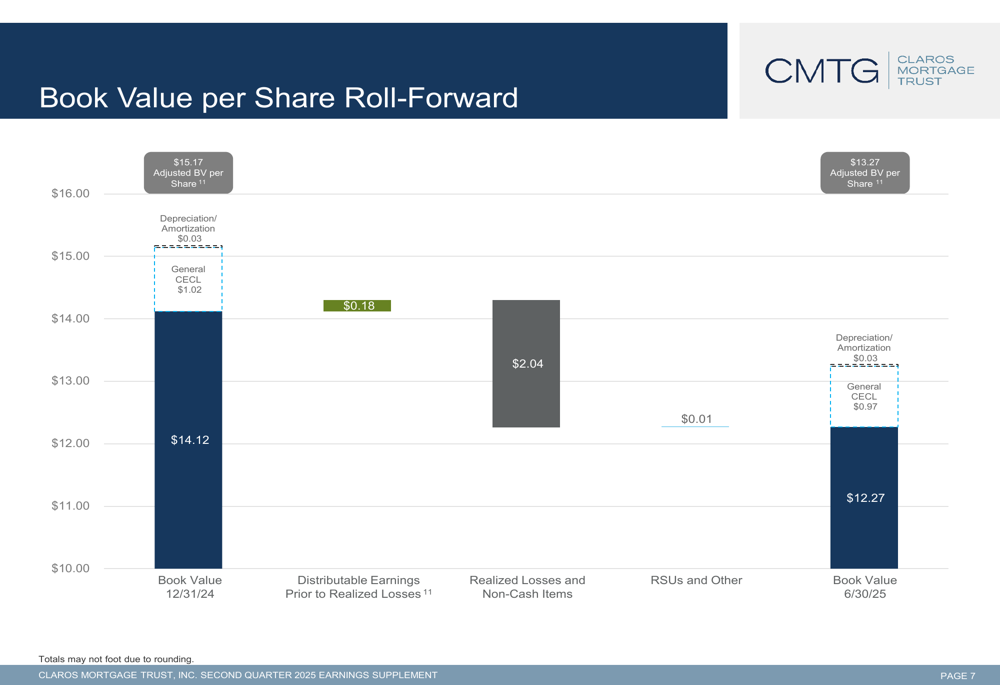

Book value per share declined to $12.27 at quarter-end, down from $14.12 at the end of 2024. The company’s adjusted book value per share, which excludes CECL reserves, stood at $13.27. This decline reflects both realized losses and increased reserves against potential future losses.

The following chart illustrates the changes in book value per share during the first half of 2025:

Loan Portfolio and Risk Management

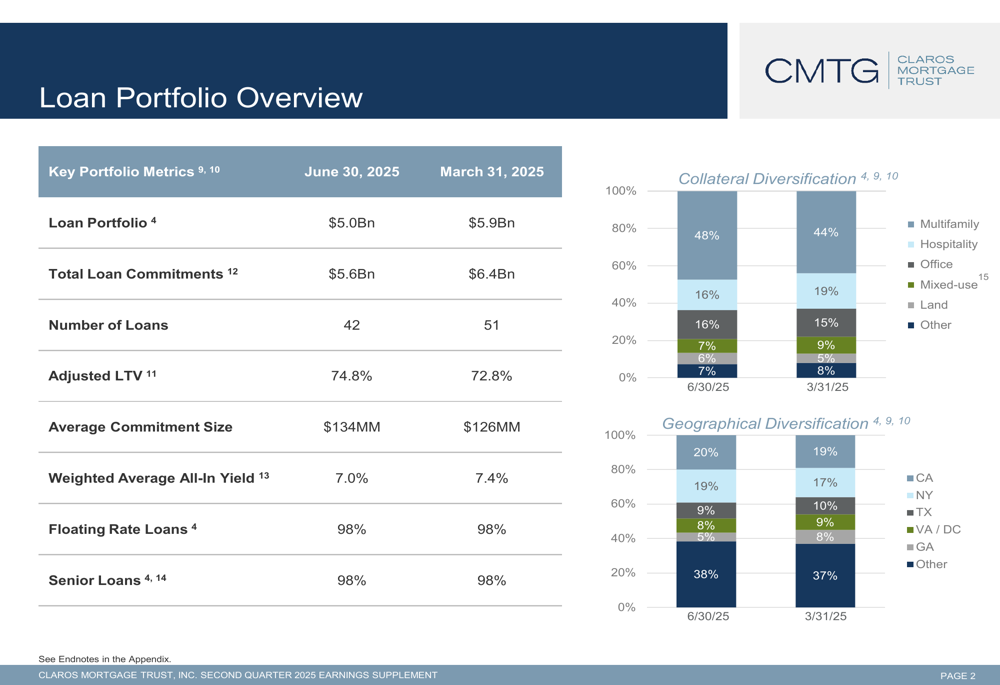

Claros’ loan portfolio decreased to $5.0 billion as of June 30, 2025, down from $5.9 billion at the end of the previous quarter. The portfolio remains predominantly composed of floating-rate (98%) and senior loans (98%), with significant exposure to multifamily (48%) and office (16%) properties.

The following chart provides a detailed breakdown of the loan portfolio by property type and geographic location:

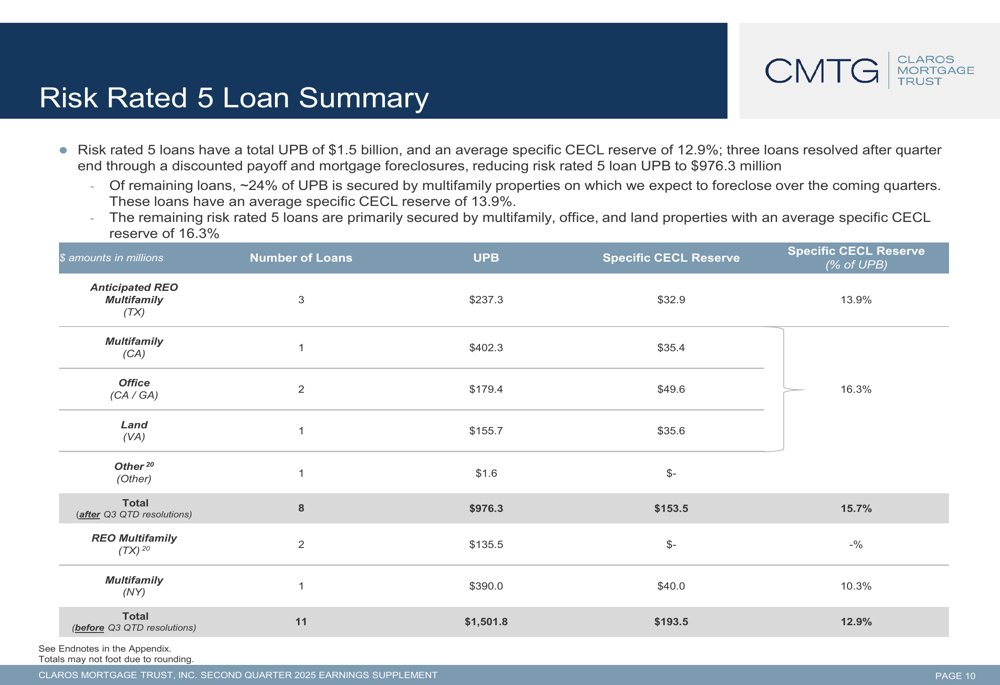

A concerning aspect of the portfolio is the high percentage of troubled loans. As of quarter-end, loans with risk ratings of 4 or 5 represented 42% of the loan portfolio, totaling $2.1 billion across 17 loans. Risk-rated 5 loans, which are the most troubled, had a total unpaid principal balance of $1.5 billion with an average specific CECL reserve of 12.9%.

The company provided detailed information about these high-risk loans:

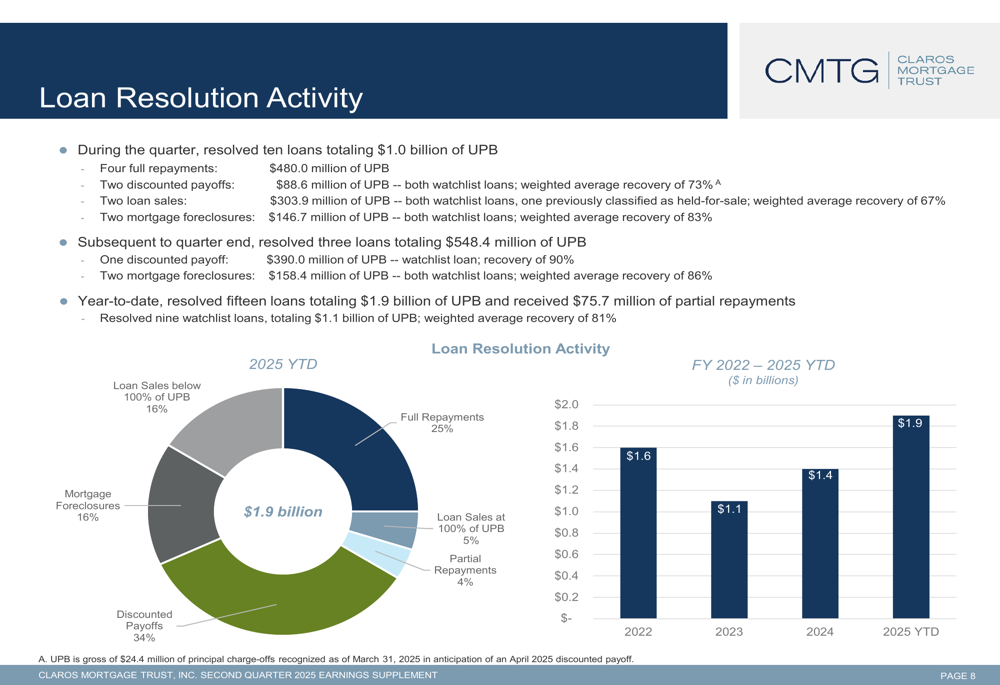

Claros has been actively resolving troubled loans, with $1.0 billion of unpaid principal balance resolved during Q2 through various means, including full repayments, discounted payoffs, loan sales, and foreclosures. Year-to-date, the company has resolved $1.9 billion of loans.

The following chart shows the company’s loan resolution activity:

Liquidity and Capital Position

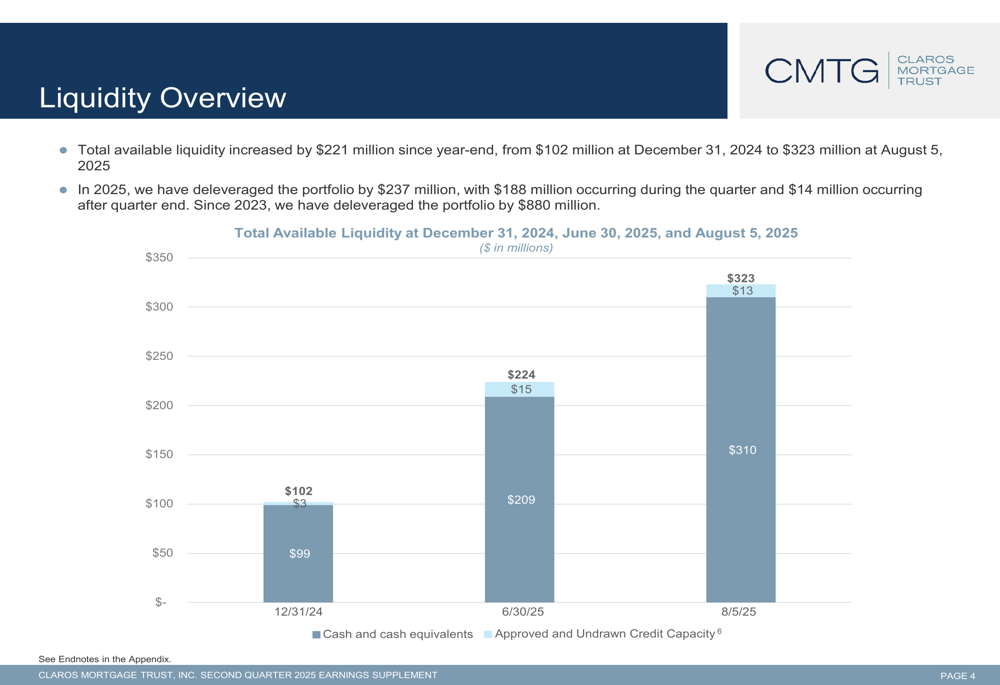

A positive development for Claros has been the significant improvement in its liquidity position. Total (EPA:TTEF) liquidity increased to $224 million as of June 30, 2025, up from $102 million at the end of 2024. By August 5, 2025, liquidity had further improved to $323 million, providing the company with greater financial flexibility.

The following chart illustrates this improving liquidity trend:

The company has also made progress in reducing its leverage. The net debt-to-equity ratio declined to 2.2x from 2.4x at the end of the previous quarter, while the total leverage ratio decreased to 2.6x from 2.8x.

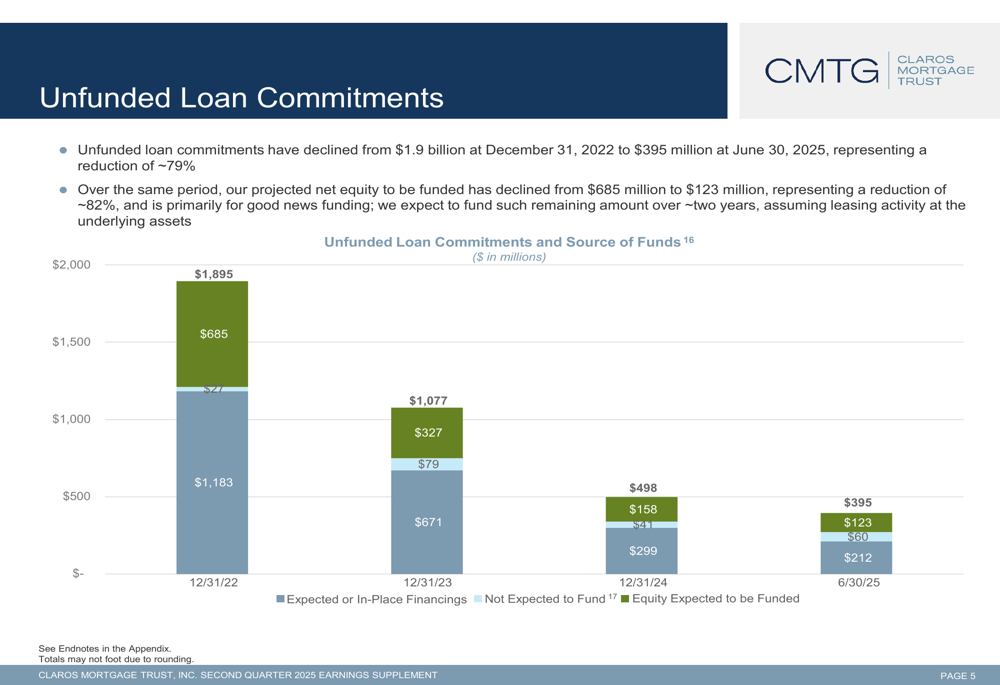

Another positive trend has been the significant reduction in unfunded loan commitments, which have declined by approximately 79% since December 2022, from $1.9 billion to $395 million as of June 30, 2025. This reduction helps mitigate future funding obligations and potential liquidity pressures.

The following chart shows this declining trend in unfunded commitments:

Strategic Initiatives

Claros’ presentation reveals a company focused on defensive strategies rather than growth initiatives. The primary strategic focus appears to be resolving troubled loans, improving liquidity, and reducing leverage.

The company highlighted its success in resolving eight loans through repayment or sales totaling $873 million during the quarter. Additionally, Claros resolved two risk-rated 5 loans with a total unpaid principal balance of $147 million through mortgage foreclosures on multifamily properties.

For its real estate owned (REO) portfolio, Claros noted that its hotel portfolio is experiencing its strongest performance since acquisition. The company refinanced related debt with a $235 million non-recourse loan with up to five years of term. It also completed the sale of a portion of a mixed-use property, generating gross proceeds of $29 million.

Forward-Looking Statements

While the presentation did not provide explicit forward guidance, several trends suggest the company’s direction. Claros appears likely to continue focusing on resolving troubled loans, with particular attention to risk-rated 5 loans secured by multifamily properties, which the company expects to foreclose on in coming quarters.

The improved liquidity position gives Claros greater flexibility to manage its portfolio and potentially take advantage of market opportunities. However, the high percentage of troubled loans (42% of the portfolio) will likely continue to pressure financial performance in the near term.

The significant increase in CECL reserves ($189.5 million in Q2 alone) suggests the company is taking a more conservative approach to valuing its loan portfolio, potentially preparing for additional challenges ahead.

This quarterly presentation represents a continuation of the strategy outlined in the Q1 earnings call, where management indicated they were targeting $2 billion in loan realizations for the year. With $1.9 billion resolved year-to-date, the company appears to be ahead of this target, though at the cost of significant realized losses and declining book value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.