HSBC downgrades Bloom Energy after significant rally

Cleveland-Cliffs Inc. (NYSE:CLF) reported a significant loss for the first quarter of 2025, with an adjusted EBITDA loss of $174 million, while outlining an ambitious strategic repositioning plan aimed at generating over $1 billion in combined EBITDA improvements. The company’s stock fell 9.42% in after-hours trading to $7.69 following the May 7 presentation.

Quarterly Performance Highlights

Cleveland-Cliffs reported $4.6 billion in revenue for Q1 2025, with steel shipments of 4.1 million net tons. The company posted a net loss of $483 million for the quarter, compared to a $434 million loss in Q1 2024. Adjusted EBITDA deteriorated significantly from positive $414 million in Q1 2024 to negative $174 million in Q1 2025.

The company attributed the weak performance to several factors, including weaker pricing carried over from Q4 2024 and early 2025, underperformance of non-core assets, and continued challenges in the plate market.

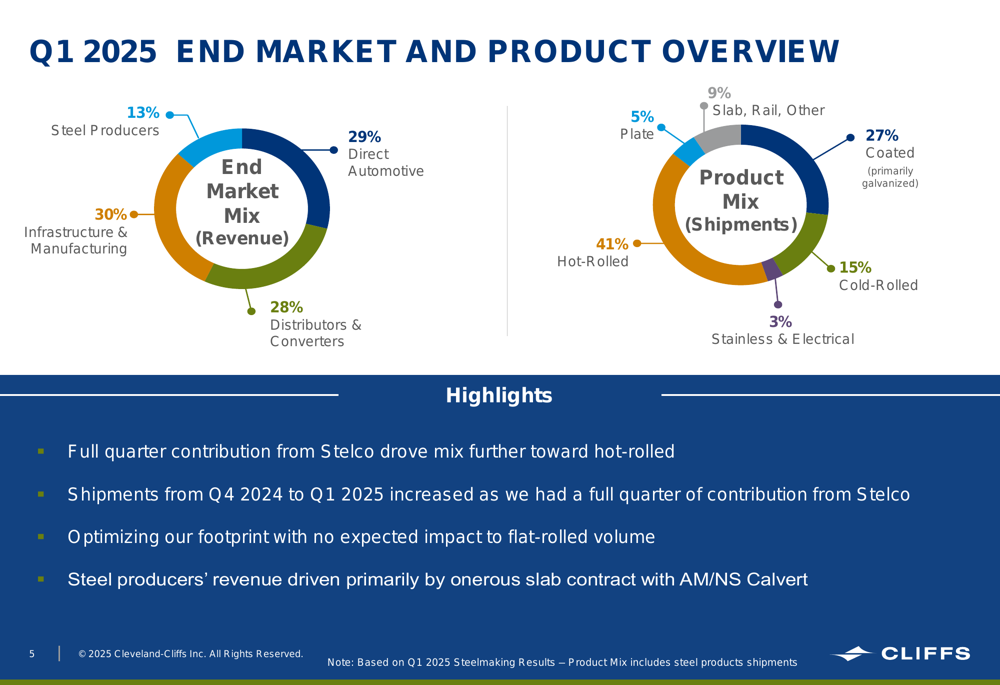

As shown in the following breakdown of Cleveland-Cliffs’ end market and product mix:

The company’s Q1 2025 revenue came primarily from Infrastructure & Manufacturing (30%), Direct Automotive (29%), and Distributors & Converters (28%), with Steel Producers accounting for 13%. On the product side, Hot-Rolled steel dominated shipments at 41%, followed by Coated products at 27%.

Strategic Recovery Plan

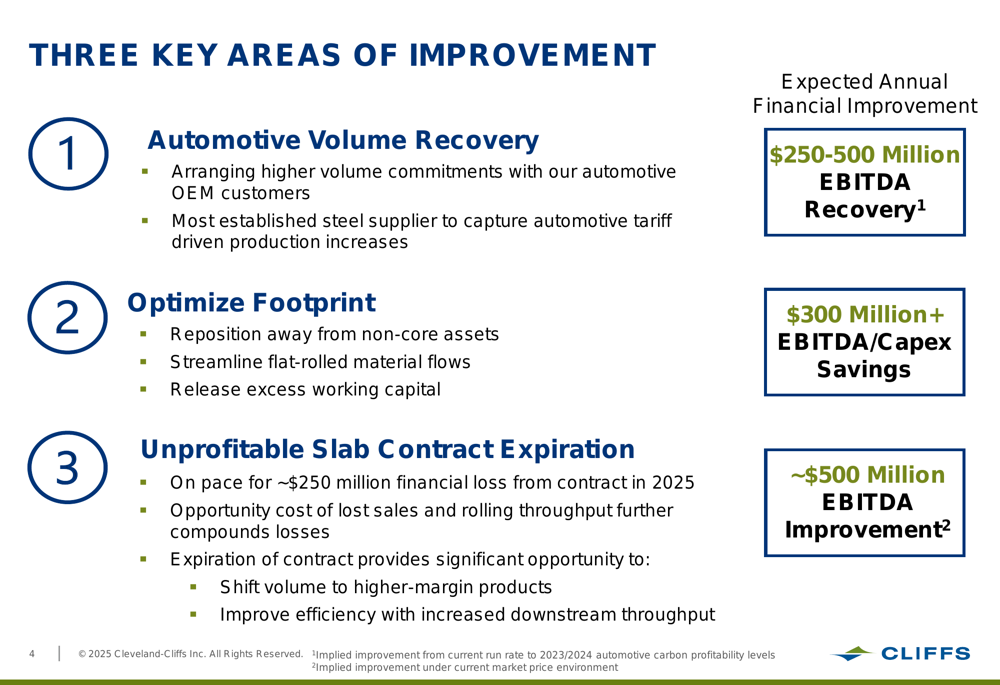

Despite the disappointing quarterly results, Cleveland-Cliffs outlined three key areas of improvement expected to generate substantial financial benefits:

The company’s recovery strategy focuses on automotive volume recovery (expected to generate $250-500 million in EBITDA recovery), footprint optimization (expected to save over $300 million in EBITDA/Capex), and the expiration of an unprofitable slab contract (expected to improve EBITDA by approximately $500 million).

"We expect to see meaningful improvement in Adj. EBITDA from Q1 to Q2," the company stated in its presentation, signaling confidence in its turnaround plan despite current challenges.

Operational Restructuring

A significant component of Cleveland-Cliffs’ strategy involves repositioning away from non-core assets, which is expected to generate substantial annual savings:

The company is implementing targeted operational changes at Riverdale (~$90 million in annual savings), Conshohocken (~$45 million), and Steelton (~$30 million). These facilities have faced challenges including unfavorable cost structures, inefficient logistics, and competition from imports.

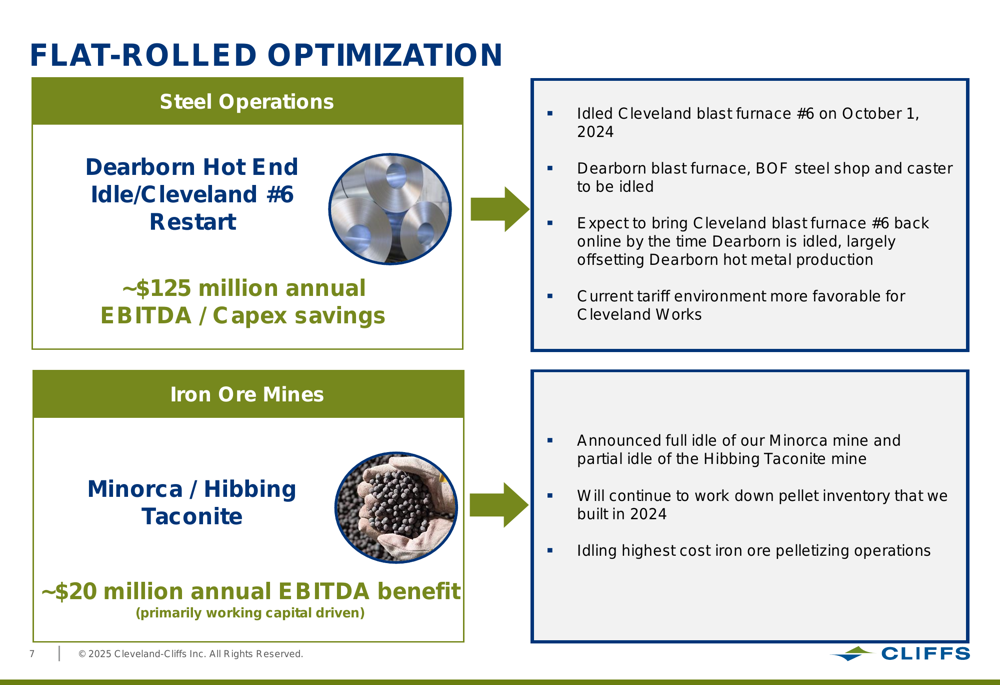

Additionally, Cleveland-Cliffs is optimizing its flat-rolled operations by idling the Dearborn hot end while restarting Cleveland #6 blast furnace, a move expected to save approximately $125 million annually:

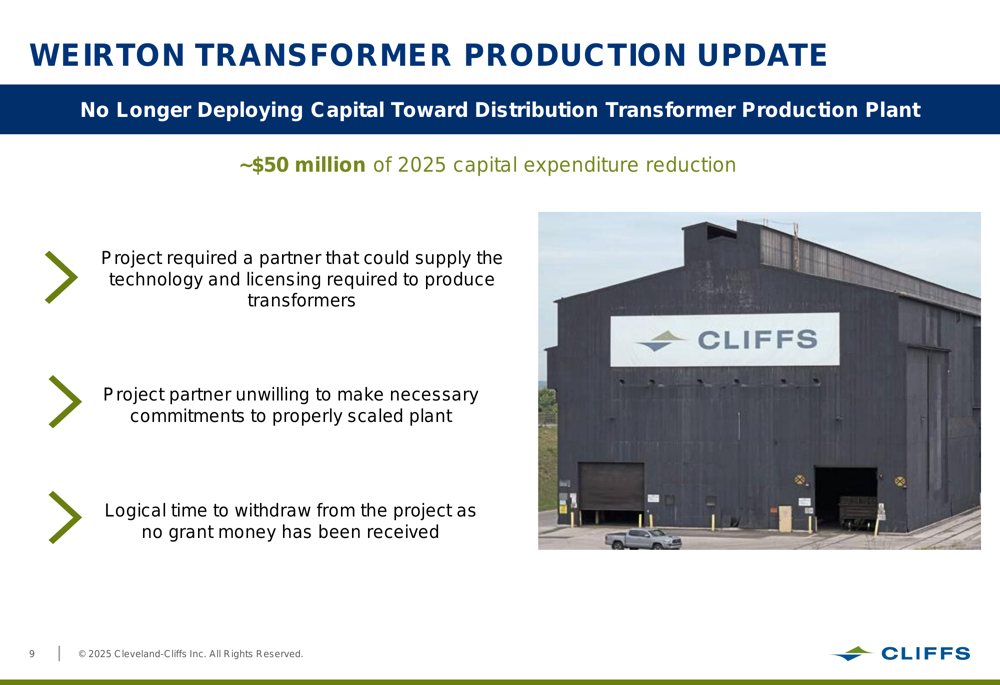

The company has also decided to cancel its planned Weirton transformer production project, resulting in approximately $50 million in capital expenditure reduction for 2025:

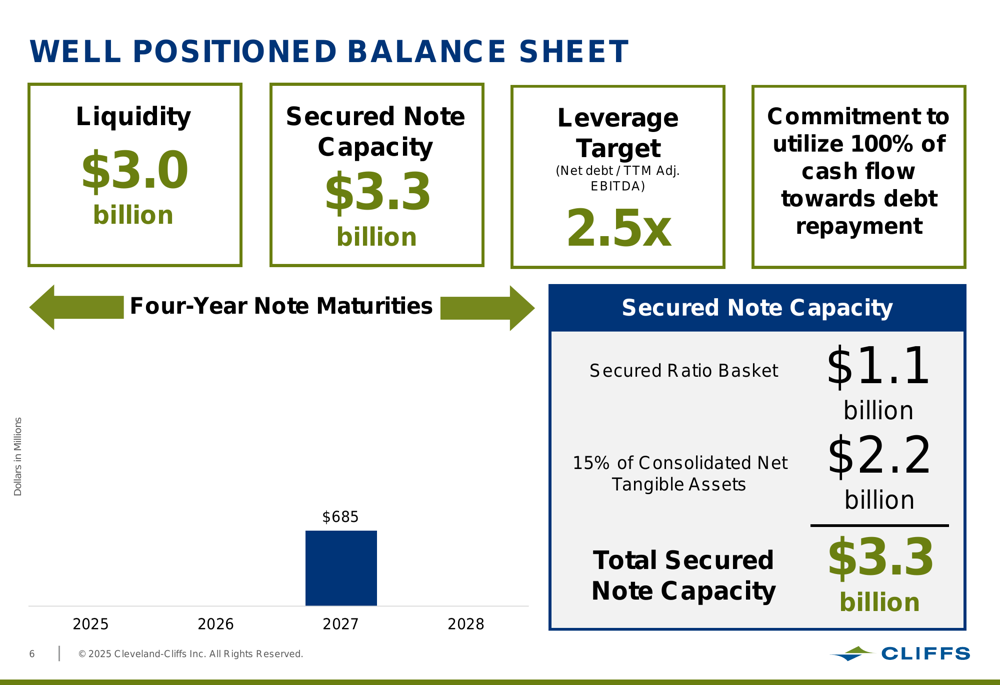

Balance Sheet and Cost Reduction Initiatives

Cleveland-Cliffs emphasized its financial stability with $3.0 billion in liquidity and $3.3 billion in secured note capacity:

The company has committed to utilizing 100% of its cash flow toward debt repayment, with a leverage target (Net debt/TTM Adj. EBITDA) of 2.5x.

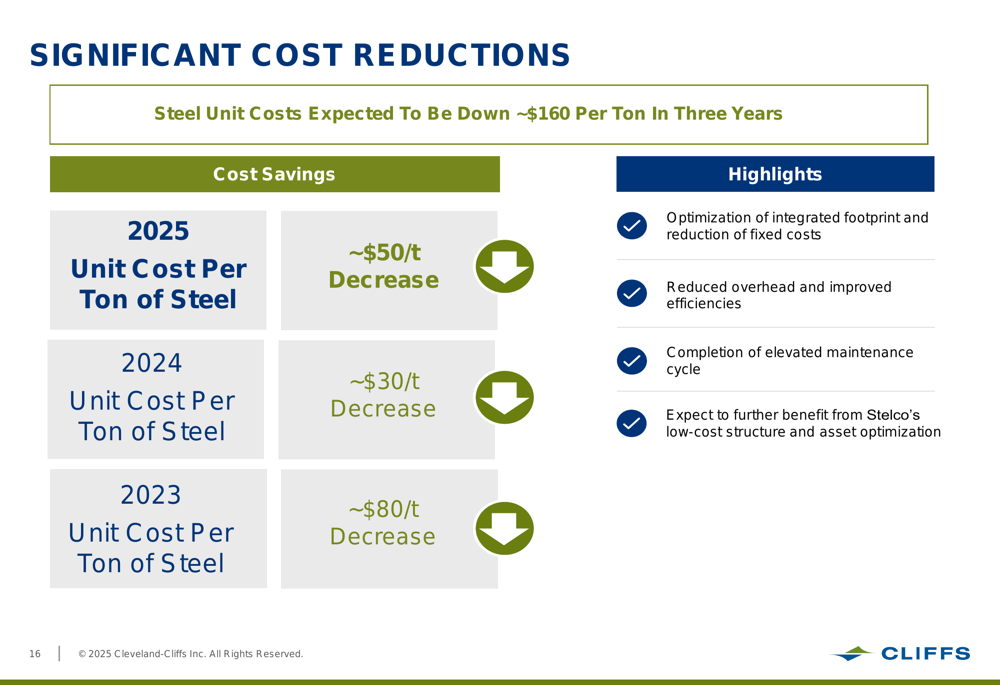

Cleveland-Cliffs is also making significant progress in reducing costs, with steel unit costs expected to decrease by approximately $160 per ton over three years:

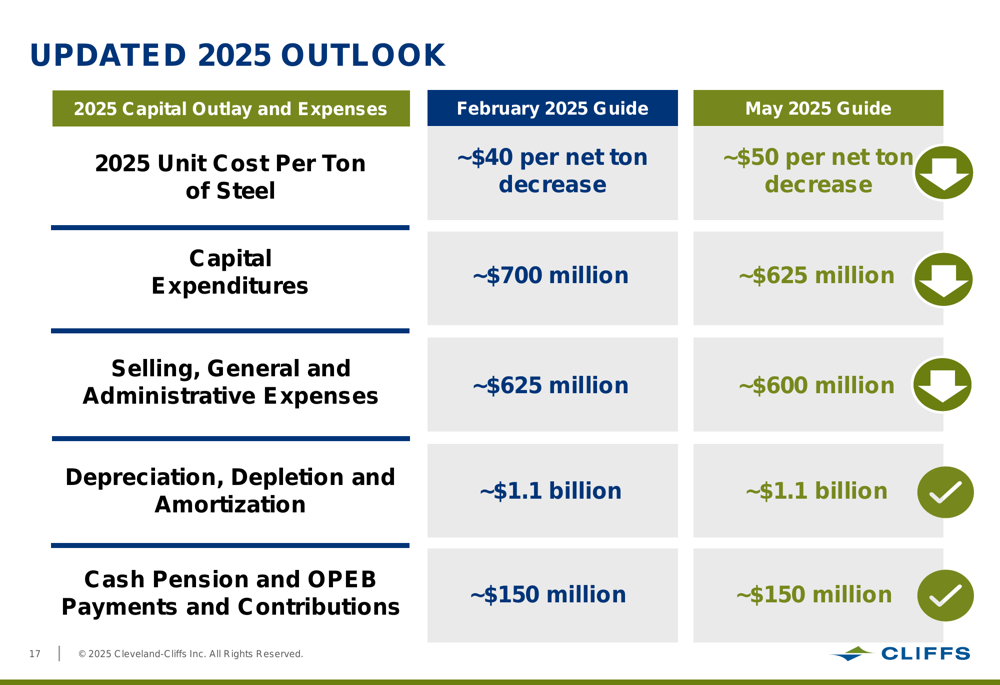

For 2025 specifically, the company has updated its guidance to reflect more aggressive cost-cutting measures:

Capital expenditures have been reduced from the February guidance of ~$700 million to ~$625 million, while SG&A expenses are now expected to be ~$600 million, down from the previous estimate of ~$625 million.

Market Context and Tariff Impact

Cleveland-Cliffs highlighted the ongoing challenge of global steel overproduction, noting that the United States remains the only major steel-producing country that produces less steel than it consumes. The company also addressed the impact of steel tariffs on its Stelco (TSX:STLC) acquisition, which has shifted from serving both Canadian and U.S. markets to focusing entirely on the Canadian market.

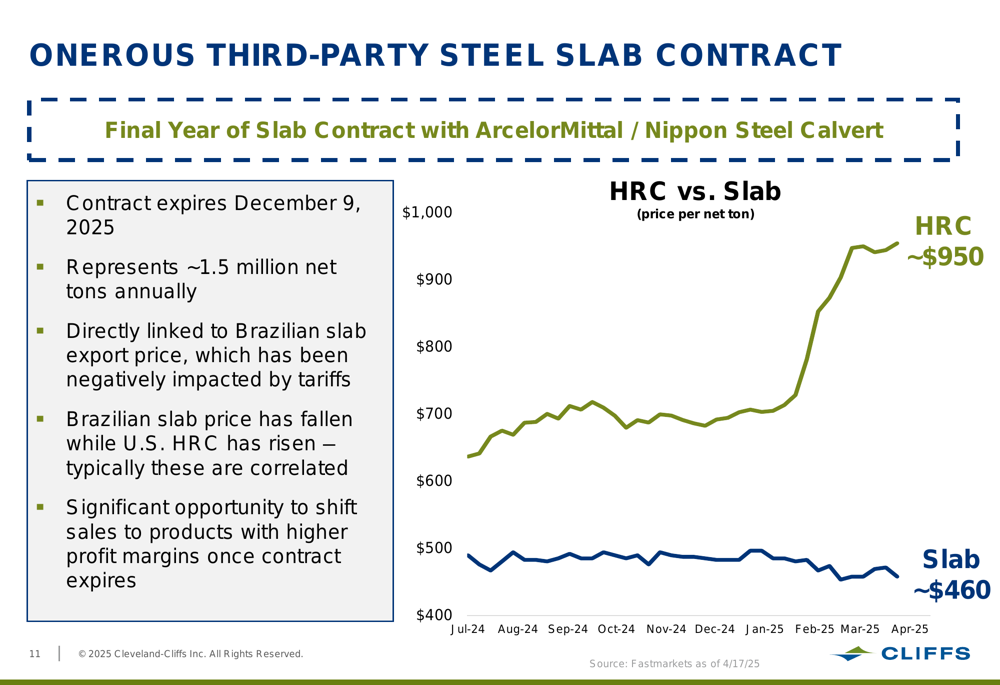

A particularly significant issue for the company has been an onerous slab contract with ArcelorMittal/Nippon Steel Calvert, which expires in December 2025:

The contract, representing approximately 1.5 million net tons annually, has been negatively impacted by tariffs on Brazilian slab exports. Cleveland-Cliffs expects a significant opportunity to shift sales to higher-margin products once the contract expires.

Forward Outlook

Despite current challenges, Cleveland-Cliffs expressed optimism about the remainder of 2025, particularly regarding the potential impact of recent automotive tariffs. On March 26, 2025, President Trump imposed 25% tariffs on imports of automobiles and certain automobile parts, which the company believes will benefit domestic automotive production and, consequently, demand for Cleveland-Cliffs’ steel products.

The company’s updated 2025 outlook reflects confidence in its ability to reduce costs and improve operational efficiency. However, the significant stock decline following the presentation suggests investors remain cautious about the company’s near-term prospects amid continued losses and challenging market conditions.

With its comprehensive strategic repositioning plan, Cleveland-Cliffs is betting on a combination of cost reductions, operational optimizations, and favorable policy developments to return to profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.