Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

CLIQ Digital AG (ETR:CLIQ) reported a significant decline in revenue for the first quarter of 2025, as the company shifts its focus from growth to profitability while simultaneously announcing a potential delisting from stock exchanges. The digital entertainment company presented these results on May 8, 2025.

The company’s strategic pivot comes amid challenging market conditions for subscription-based digital content providers, with CLIQ implementing comprehensive cost-cutting measures while maintaining its EBITDA margin despite the revenue decline.

Quarterly Performance Highlights

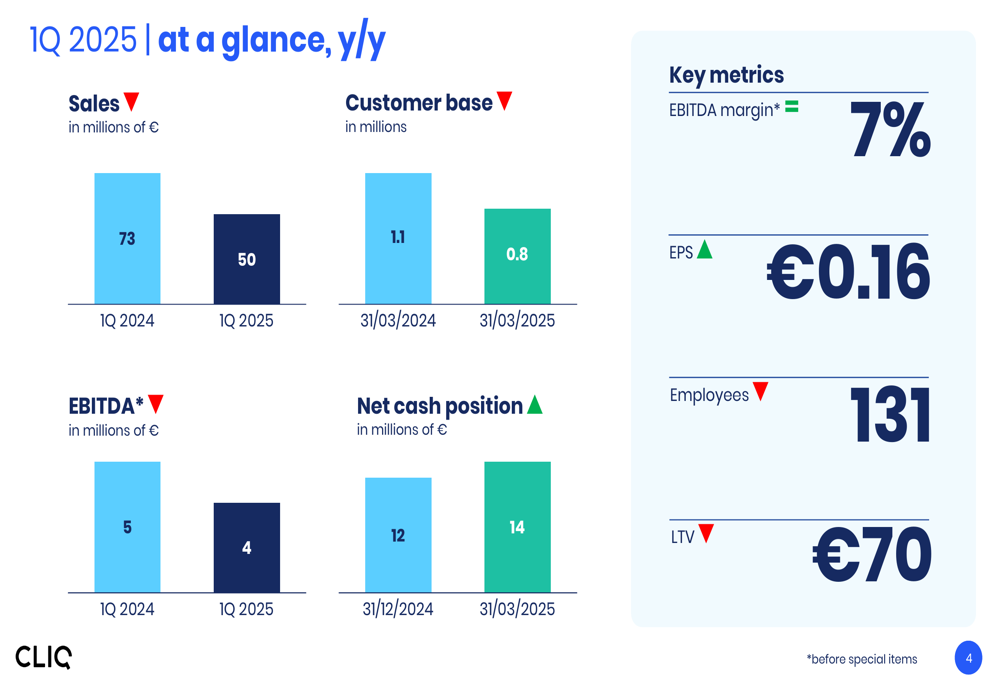

CLIQ Digital’s Q1 2025 results showed substantial year-over-year declines across most key metrics. Sales decreased 32% to €50 million compared to €73 million in Q1 2024. The company’s customer base contracted to 0.8 million, down from 1.1 million as of March 31, 2024.

As shown in the following comprehensive overview of key performance metrics:

EBITDA before special items fell 31% year-over-year to €3.7 million, though the EBITDA margin remained stable at 7.3%. The company reported earnings per share of €0.16 for the quarter. Despite the revenue decline, CLIQ’s net cash position improved to €13.6 million, up from €12 million at the end of 2024.

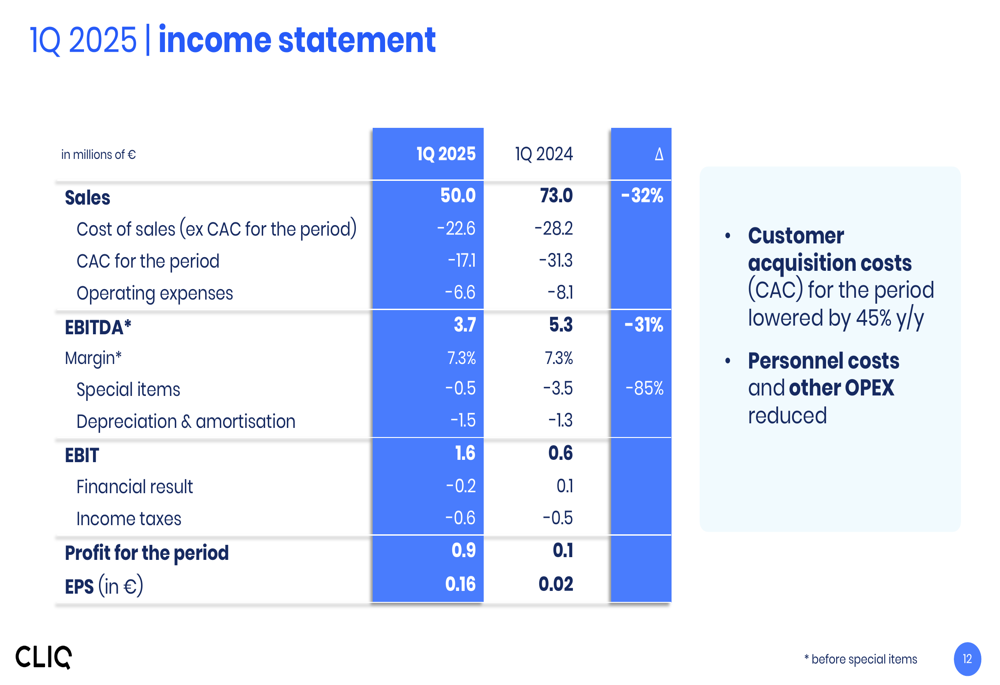

The income statement reveals the full financial picture for the quarter:

Strategic Initiatives

CLIQ Digital has implemented a "Fit For Future" program focused on two key areas: cost efficiencies and productivity gains. The cost efficiency measures include lowered target customer acquisition costs, a strategic review of human resources, reduction of external service providers, and scrutinized SG&A expenses.

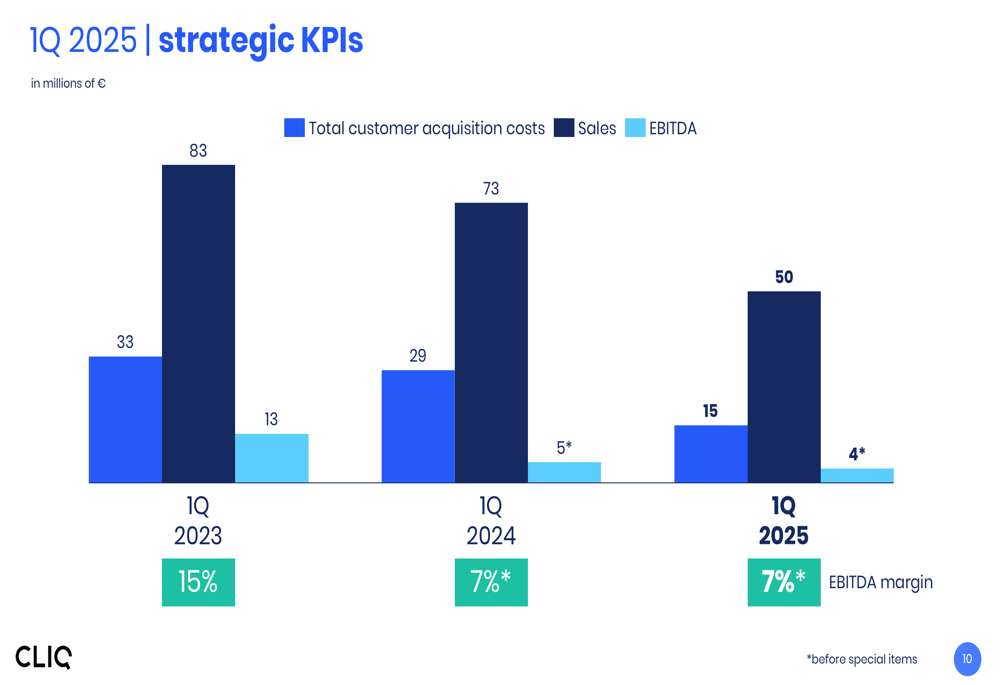

The company’s strategic KPIs over the past three years demonstrate this shift in focus, with customer acquisition costs nearly halved compared to the previous year:

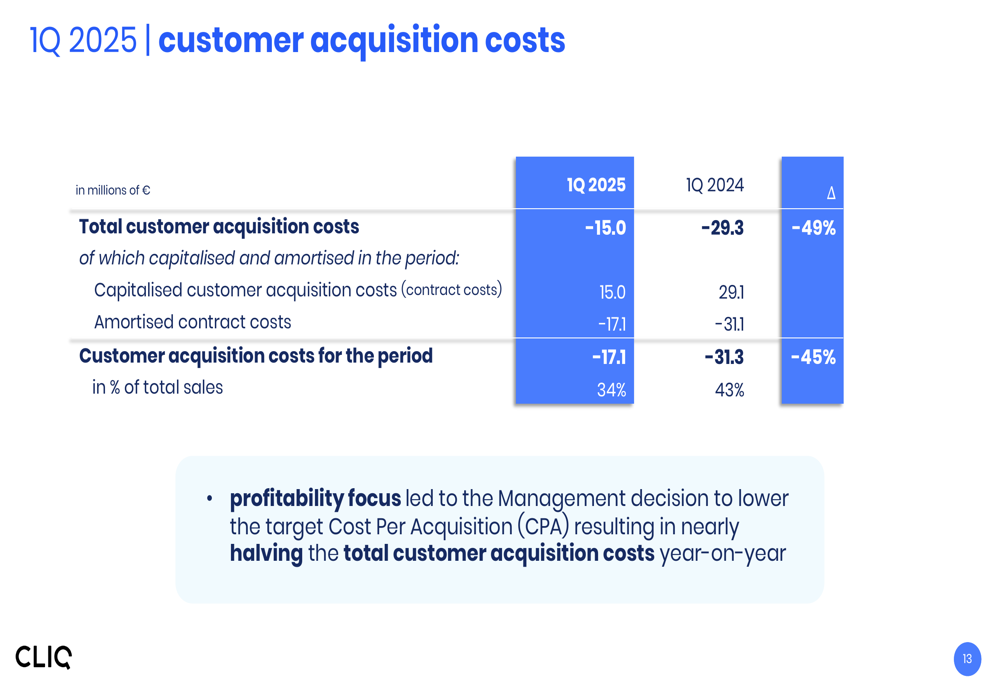

Total (EPA:TTEF) customer acquisition costs fell dramatically to €15 million in Q1 2025, a 49% reduction from €29 million in Q1 2024. This strategic decision to lower the target Cost Per Acquisition (CPA) reflects the company’s prioritization of profitability over growth.

The detailed breakdown of customer acquisition costs shows this significant change in strategy:

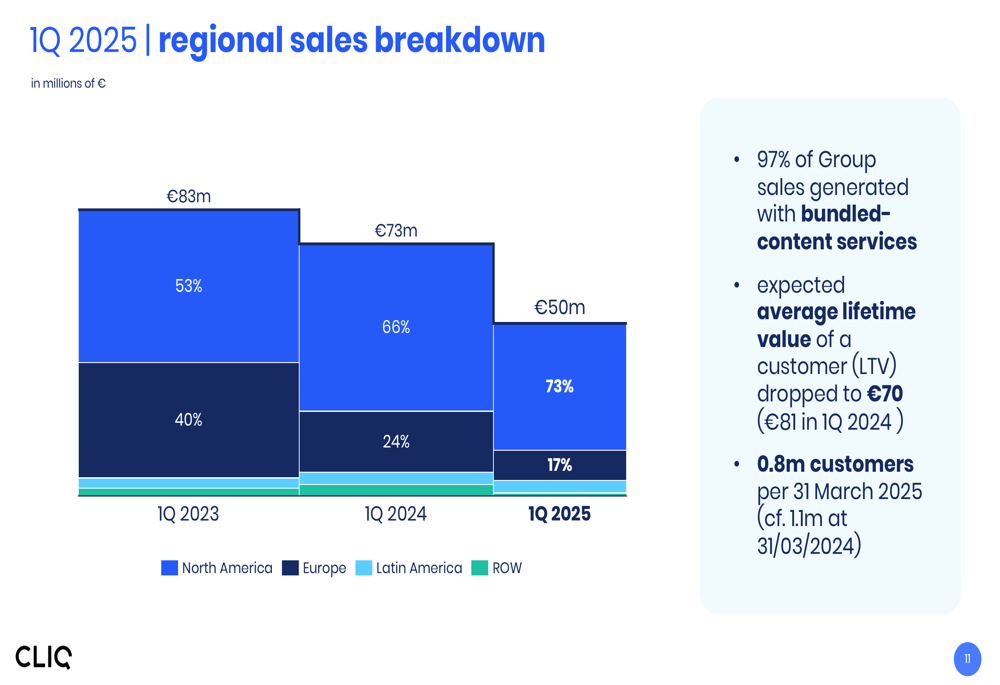

Regional Performance

CLIQ Digital’s geographical sales distribution continues to shift heavily toward North America, which now accounts for 73% of total revenue, up from 66% in Q1 2024 and 53% in Q1 2023. Meanwhile, Europe’s contribution has declined to 17%, down from 24% in Q1 2024 and 40% in Q1 2023.

The regional sales breakdown illustrates this continuing concentration in the North American market:

The company noted that 97% of group sales were generated from bundled-content services. However, the expected average lifetime value of a customer (LTV) dropped to €70 from €81 in Q1 2024, indicating challenges in customer monetization.

Content Strategy

Despite the cost-cutting measures, CLIQ Digital continues to invest in content expansion. The company renewed and extended its pan-territorial licensing agreement with Olympusat for North and Latin America, covering telenovelas and movies for both subscription and advertising-based video-on-demand services.

Additionally, CLIQ secured a major upgrade for its sports vertical in the U.S. through a licensing deal with NAVIO Networks Triple-B Media for 10 linear FAST channels, including coverage of live sports events, recaps, documentaries, and reports across various sports categories.

The company is also exploring new monetization models, including an advertising-based video-on-demand (AVOD) model launched in the U.S., and plans to accept new payment methods such as Apple (NASDAQ:AAPL) Pay and Google (NASDAQ:GOOGL) Pay.

Corporate Structure Changes

In a significant development, CLIQ Digital announced potential changes to its shareholding structure, including a possible delisting from all relevant stock exchanges. This move is supported by the management and supervisory boards if Dylan Media B.V. acquires a significant shareholding.

The proposal includes two potential offers: a Dylan Media Offer (possible partial public tender offer) and a CLIQ Offer (partial public share repurchase offer). The Dylan Media Offer would provide an opportunity for shareholders not wishing to remain invested in a non-listed company to dispose of their shares, though the timing remains unknown.

Forward-Looking Statements

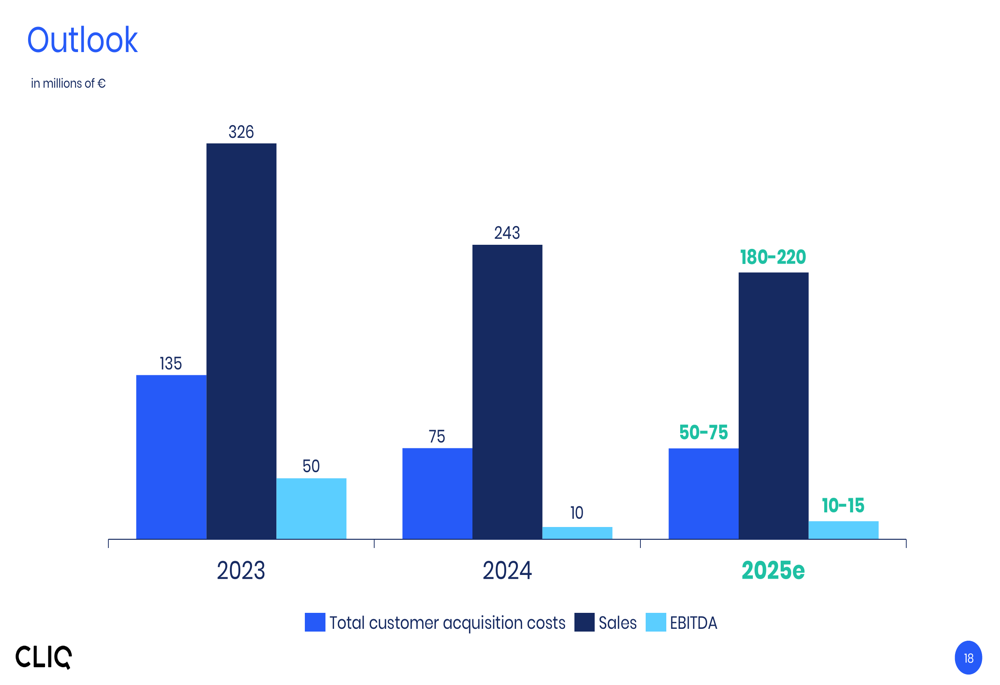

For 2025, CLIQ Digital provided guidance indicating continued challenges ahead. The company expects:

Total customer acquisition costs are projected at €50-75 million, down from €75 million in 2024. Sales are forecast between €180-220 million, compared to €243 million in 2024. EBITDA is expected to be €10-15 million, similar to the €10 million reported in 2024.

This outlook suggests that while the company’s cost-cutting measures may stabilize profitability, revenue growth remains challenging in the near term as CLIQ Digital continues its strategic pivot toward efficiency and sustainable margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.