Street Calls of the Week

Introduction & Market Context

CLIQ Digital AG (ETR:CLIQ) presented its Q2 and first-half 2025 results on August 7, 2025, revealing a company navigating significant challenges in the payment ecosystem while focusing on profitability and cash preservation. The digital entertainment provider has withdrawn its full-year 2025 outlook due to disruptions in the payment ecosystem driven by card schemes and acquirers, with financial impacts currently unquantifiable.

The company’s stock, which has been trading near its 52-week low of €17.80, saw a modest 1.25% increase following the presentation, suggesting cautious investor response to the mixed results.

Quarterly Performance Highlights

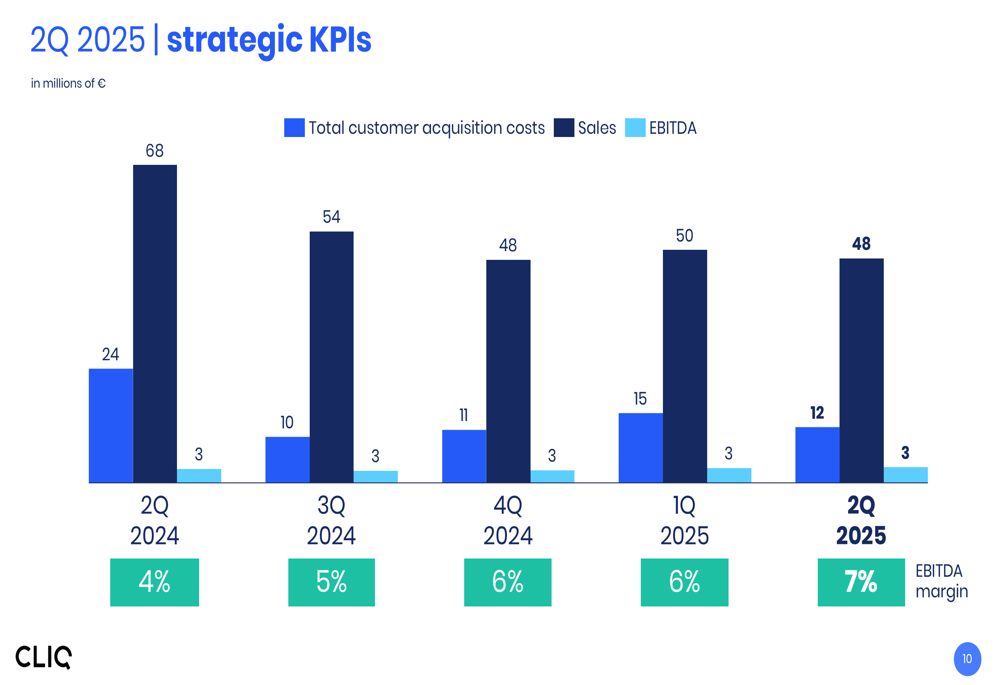

CLIQ Digital reported Q2 2025 sales of €48.1 million, a 4% decrease from €50.0 million in Q1 2025. Despite this decline, EBITDA increased by 5% to €3.3 million, with the EBITDA margin improving to 6.9% from 6.3% in the previous quarter.

As shown in the following chart of quarterly performance metrics:

The company has maintained relatively stable EBITDA of around €3 million over the past five quarters while significantly reducing customer acquisition costs from €24 million in Q2 2024 to €12 million in Q2 2025. This strategic shift has helped improve EBITDA margins from 4% to 7% year-over-year.

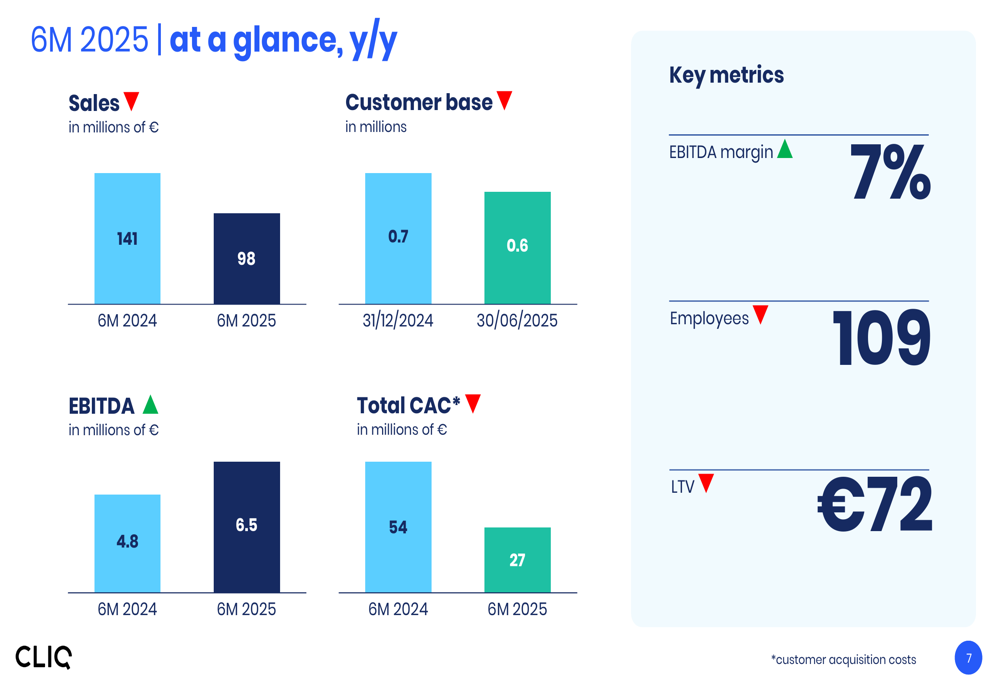

For the first half of 2025, CLIQ Digital’s key metrics compared to the same period in 2024 show a mixed picture:

Sales decreased by 30% year-over-year to €98 million, while the customer base contracted from 0.7 million to 0.6 million. However, EBITDA increased to €6.5 million from €4.8 million, reflecting the company’s focus on profitability over growth.

Detailed Financial Analysis

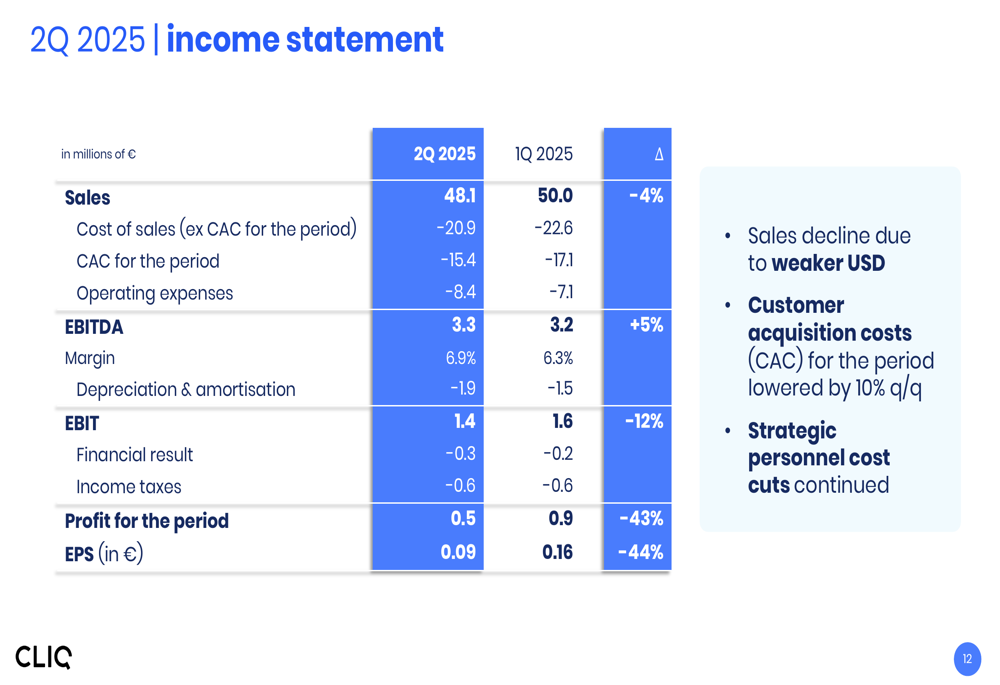

CLIQ Digital’s Q2 2025 income statement reveals the company’s strategic shift toward profitability:

While sales declined by 4% quarter-over-quarter, the company managed to reduce cost of sales and customer acquisition costs, resulting in a 5% increase in EBITDA. However, profit for the period decreased by 43% to €0.5 million, and earnings per share fell by 44% to €0.09, primarily due to higher operating expenses.

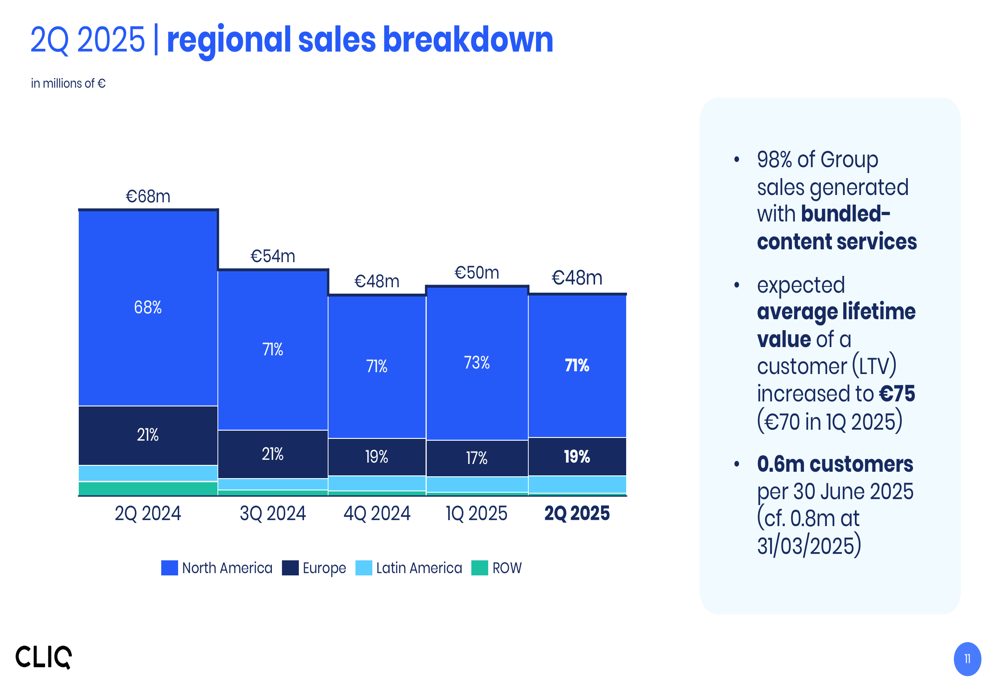

The company’s regional sales breakdown shows continued dominance in North America, which accounted for 71% of Q2 2025 sales:

Europe contributed 19% and Latin America 10% of total sales. The company noted that 98% of group sales were generated from bundled-content services, and the expected average lifetime value of a customer increased to €75 from €70 in Q1 2025.

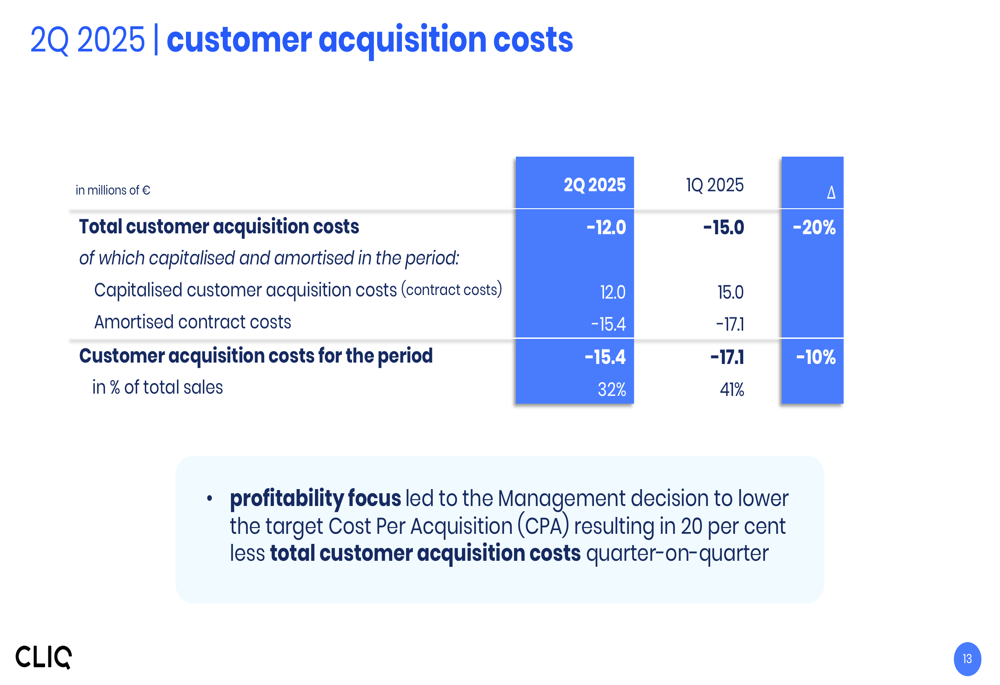

CLIQ Digital has significantly reduced its customer acquisition costs as part of its profitability focus:

Total (EPA:TTEF) customer acquisition costs decreased by 20% quarter-over-quarter to €12.0 million, representing 32% of total sales compared to 41% in Q1 2025. This reduction reflects management’s decision to lower the target Cost Per Acquisition (CPA) to improve profitability.

Cash Position & Balance Sheet

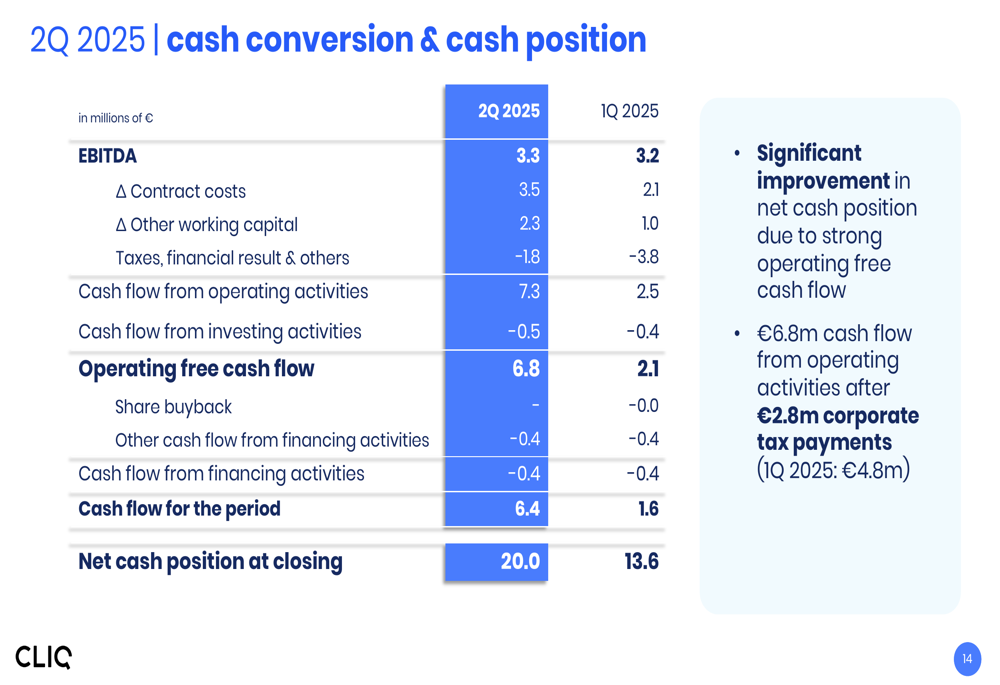

One of the bright spots in CLIQ Digital’s presentation was its improved cash position and strong cash conversion:

The company generated €7.3 million in cash flow from operating activities in Q2 2025, a significant improvement from €2.5 million in Q1 2025. This resulted in an operating free cash flow of €6.8 million and increased the net cash position to €20.0 million as of June 30, 2025, up from €13.6 million at the end of Q1.

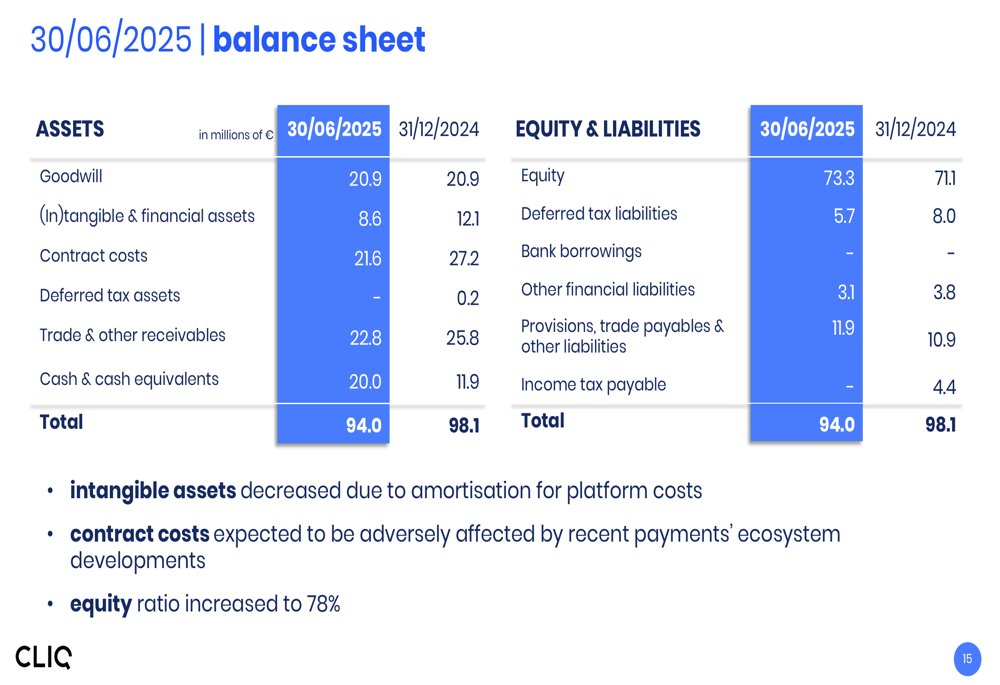

The balance sheet as of June 30, 2025, shows a solid financial position with an equity ratio of 78%:

Total assets decreased slightly to €94.0 million from €98.1 million at the end of 2024, primarily due to lower contract costs and intangible assets. The company has no bank borrowings and maintains a strong liquidity position.

Strategic Initiatives & Outlook

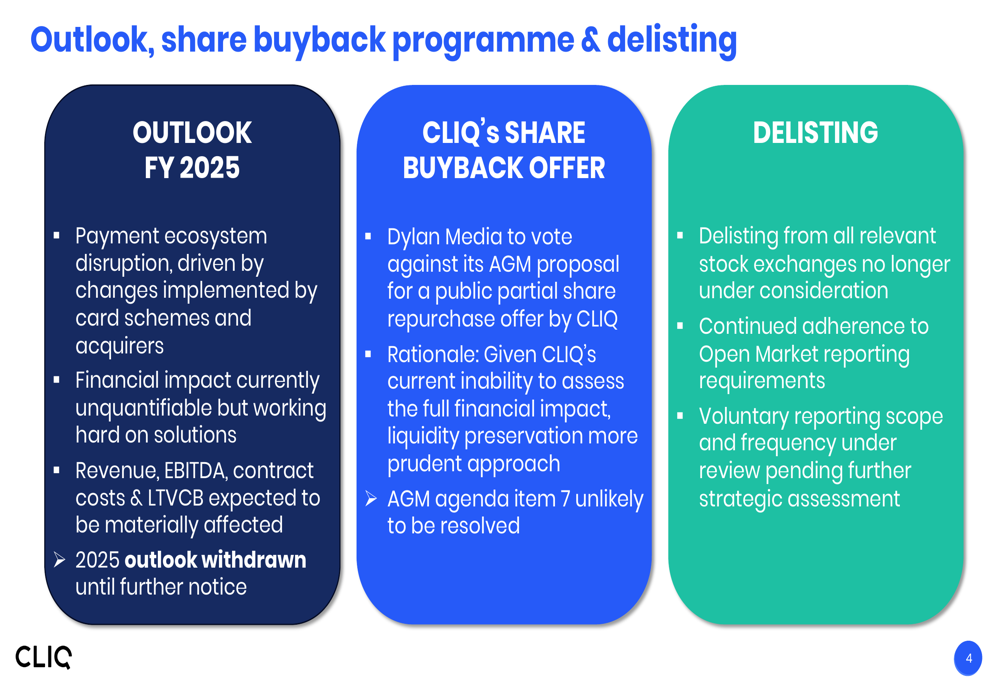

CLIQ Digital has withdrawn its 2025 outlook due to payment ecosystem disruption, which is expected to materially affect revenue, EBITDA, contract costs, and lifetime value of customer base (LTVCB). The company provided the following update on its strategic initiatives:

The company has decided against proceeding with a share buyback program, with Dylan Media (which owns approximately 41% of CLIQ Digital along with management) voting against the AGM proposal. This decision is based on the need to preserve liquidity given the uncertainty around the financial impact of the payment ecosystem disruption.

Additionally, CLIQ Digital has abandoned plans for delisting from stock exchanges, stating it will continue to adhere to Open Market reporting requirements while reviewing the scope and frequency of voluntary reporting.

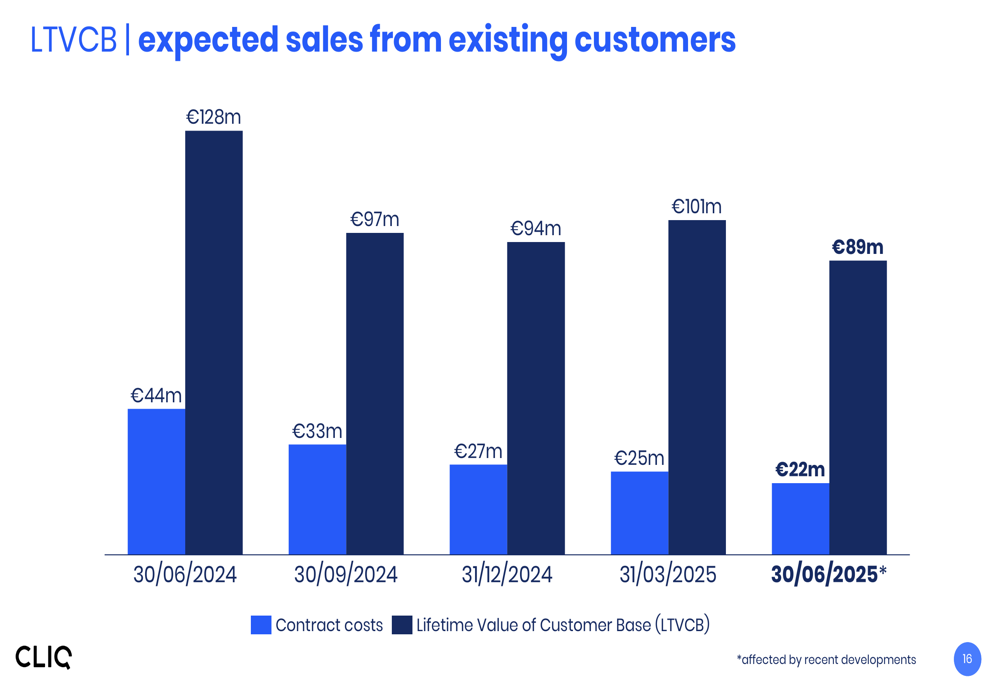

The expected sales from existing customers (LTVCB) has been affected by recent developments in the payment ecosystem:

The LTVCB decreased to €89 million as of June 30, 2025, from €101 million at the end of Q1 2025, while contract costs decreased to €22 million from €25 million.

Forward-Looking Statements

While CLIQ Digital has withdrawn its specific financial guidance for 2025, the company’s presentation suggests a continued focus on profitability and cash preservation amid market challenges. The payment ecosystem disruption poses significant uncertainties, but the company’s improved cash position and reduced cost structure may provide some buffer against these headwinds.

The decision to maintain stock exchange listing indicates a commitment to market transparency, which could help maintain investor confidence despite the challenging outlook. However, investors should note that the company’s ability to generate revenue and maintain its customer base may be materially affected by the ongoing payment ecosystem disruption.

CLIQ Digital’s strategic shift from growth to profitability appears to be yielding results in terms of improved margins and cash flow, but the sustainability of this approach amid market disruptions remains to be seen.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.