Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

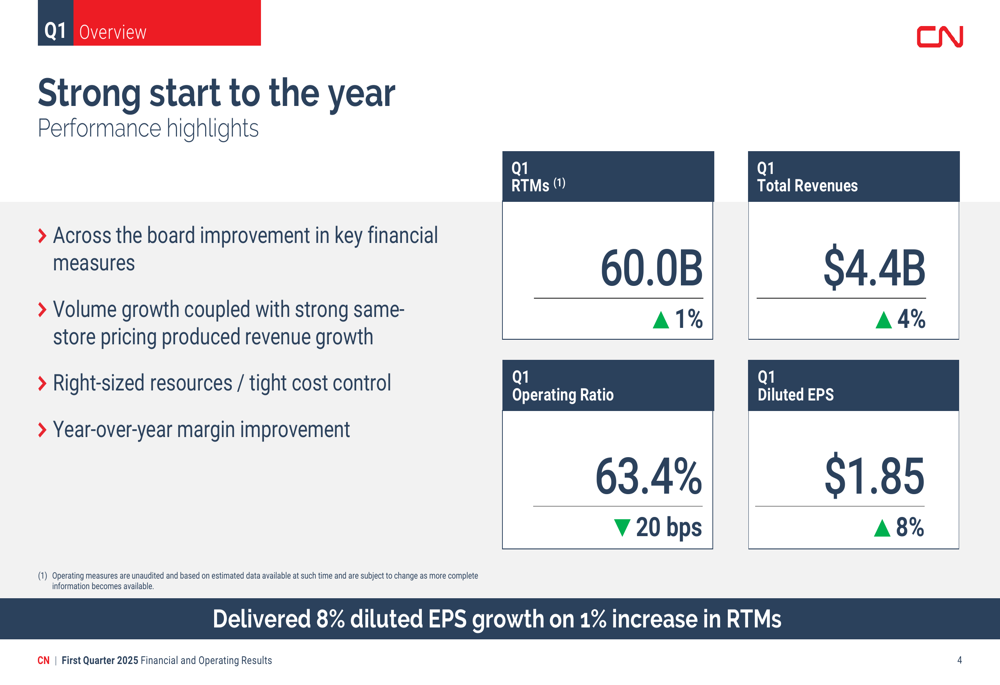

Canadian National Railway (TSX:CNR) Company (TSX:CNR, NYSE:CNI) presented its first quarter 2025 financial results on May 1, 2025, showcasing the company’s ability to deliver growth despite challenging winter conditions and an uncertain economic environment. The railway operator reported a 4% increase in total revenues to $4.4 billion, while diluted earnings per share rose 8% to $1.85, demonstrating CN’s operational resilience and pricing power in the face of modest volume growth.

Tracy Robinson, President and Chief Executive Officer, emphasized that the company had a "strong start to the year" with "across the board improvement in key financial measures." The presentation highlighted CN’s success in right-sizing resources and maintaining tight cost control, which contributed to year-over-year margin improvement.

As shown in the following overview of key performance metrics, CN delivered solid results across multiple financial indicators:

Quarterly Performance Highlights

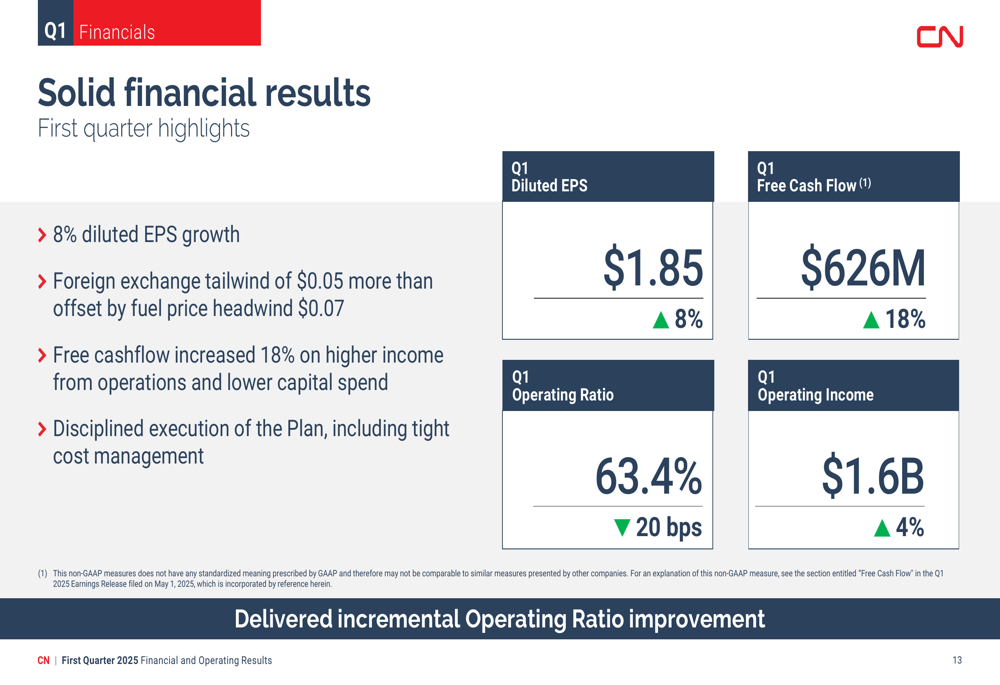

CN Railway’s first quarter results revealed the company’s ability to generate stronger financial returns despite modest volume growth. Revenue ton miles (RTMs) increased by just 1% to 60.0 billion, yet the company delivered an 8% increase in diluted EPS, demonstrating effective cost management and pricing strategies.

The operating ratio—a key efficiency metric where lower is better—improved by 20 basis points to 63.4%. This improvement reflects CN’s continued focus on operational efficiency and cost discipline. Free cash flow showed particularly strong growth, increasing 18% to $626 million, driven by higher income from operations and lower capital expenditures.

The following slide details these key financial metrics, highlighting the company’s solid performance:

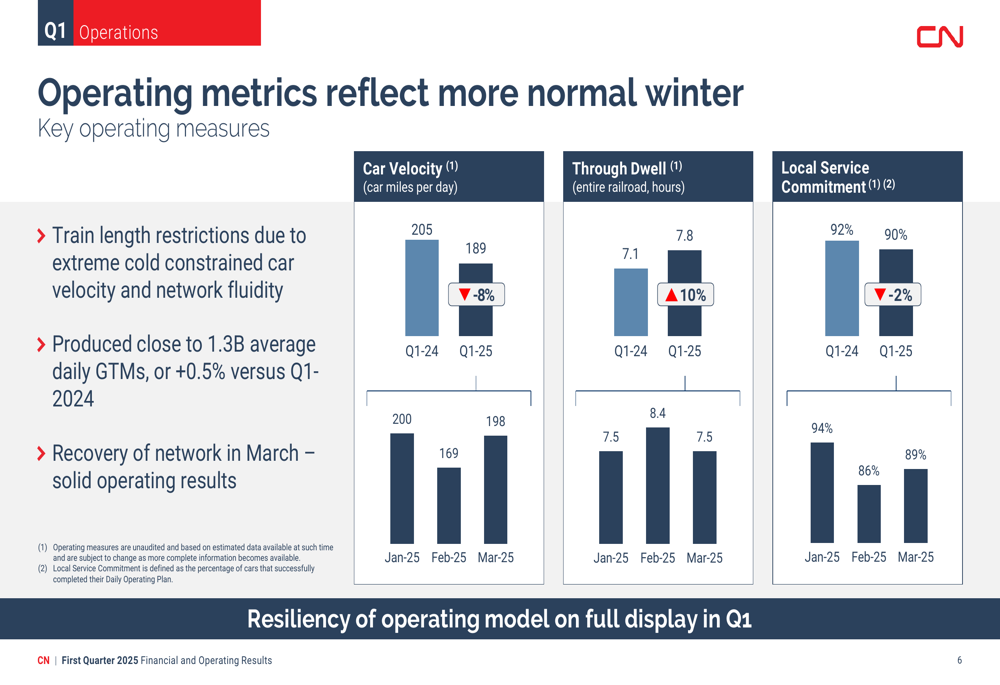

Operational Challenges and Recovery

CN’s operations faced challenges during the first quarter due to winter conditions, which affected network fluidity and constrained car velocity. The company noted that train length restrictions due to extreme cold weather impacted performance metrics, particularly in January and February.

Car velocity decreased 8% year-over-year to 189 car miles per day, while through dwell time increased 10% to 7.8 hours. Local service commitment declined slightly by 2% to 90%. However, the presentation highlighted a notable recovery in March as weather conditions improved, with car velocity rebounding to 198 car miles per day and through dwell improving to 7.5 hours.

The following chart illustrates the operational challenges and subsequent recovery throughout the quarter:

Despite these challenges, CN emphasized the "resiliency of operating model on full display in Q1" and continued to advance key efficiency initiatives. The company reported an 8% improvement in GTMs per T&E employee, an 11% reduction in locomotive failures, and a 12% decrease in train delays caused by work blocks compared to Q1 2024.

The following slide details these efficiency improvements:

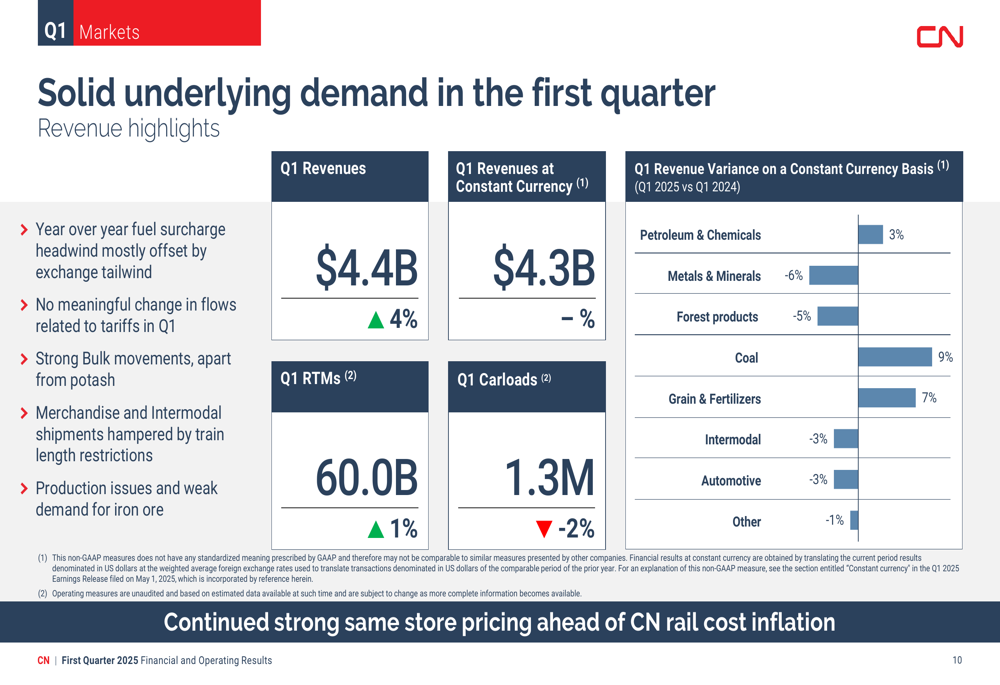

Segment Performance Analysis

CN’s revenue performance varied significantly across business segments during Q1 2025. On a constant currency basis, the strongest performers were Coal (+9%) and Grain & Fertilizers (+7%), while Metals & Minerals (-6%) and Forest Products (-5%) experienced declines.

Chief Commercial Officer Remi G. Lalonde noted that "strong Bulk movements, apart from potash" helped drive revenue growth, while "Merchandise and Intermodal shipments were hampered by train length restrictions." The company also faced challenges from "production issues and weak demand for iron ore" in its Metals & Minerals segment.

The following chart breaks down revenue variance by segment on a constant currency basis:

Looking ahead to the remainder of 2025, CN provided a detailed outlook by segment. The company expects continued strength in chemicals and plastics due to slight growth in industrial production and customer expansions. In the grain segment, CN anticipates difficult comparisons in Q2/Q3 for Canadian grain but strong corn demand and new crush capacity for U.S. grain. The international intermodal business is expected to benefit from CN’s service offering and recovery of volumes lost due to labor disruptions.

The following slide details the company’s segment-specific outlook:

Financial Results and Outlook

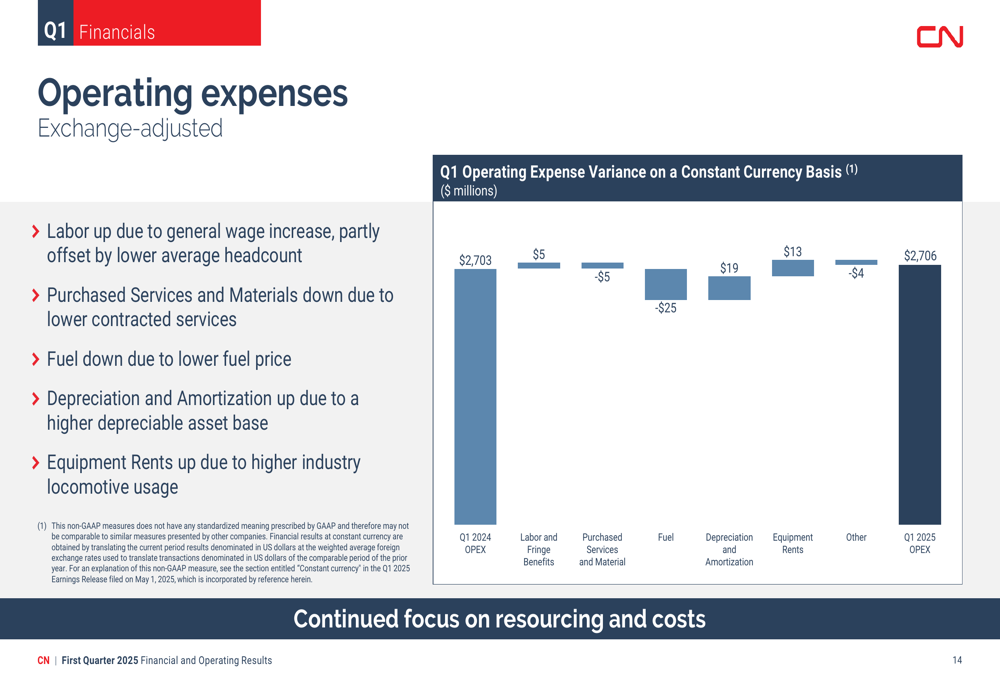

CN’s operating expenses on a constant currency basis remained relatively flat year-over-year at $2.7 billion. Higher labor costs due to wage increases were largely offset by lower fuel prices and contracted services. The company saw increases in depreciation and amortization expenses due to a higher depreciable asset base, as well as higher equipment rents related to increased industry locomotive usage.

The following chart breaks down the changes in operating expenses:

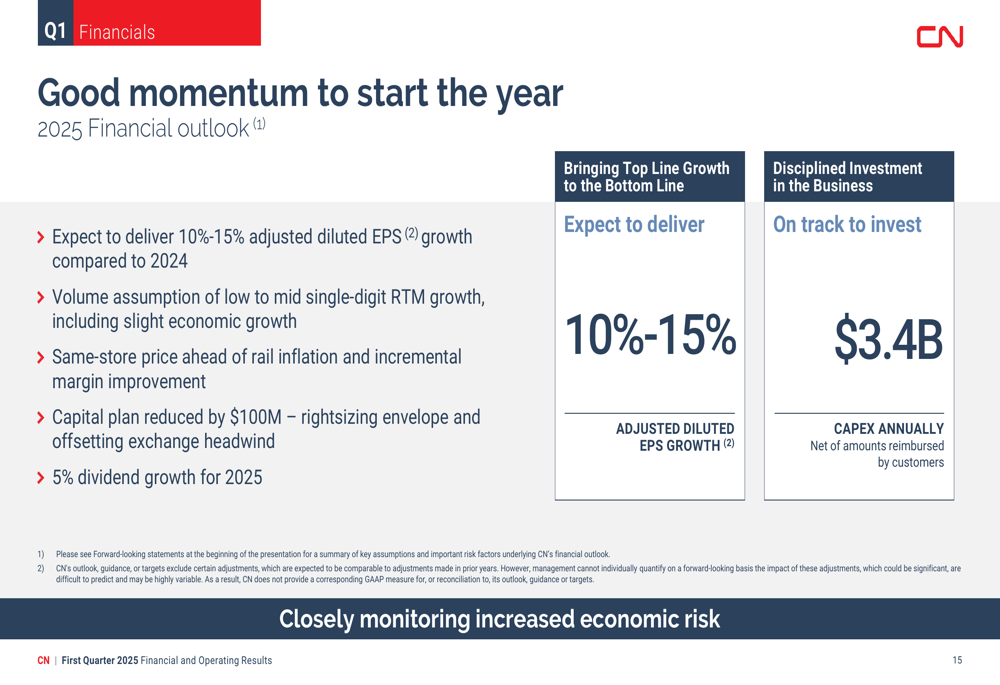

For the full year 2025, CN maintained its positive outlook, expecting to deliver 10%-15% adjusted diluted EPS growth compared to 2024. This forecast is based on low to mid-single-digit RTM growth, pricing ahead of rail inflation, and incremental margin improvement. The company also announced a reduction in its capital plan by $100 million, which it described as "rightsizing envelope and offsetting exchange headwind."

CN reaffirmed its commitment to shareholder returns with a 5% dividend growth for 2025, while noting that it is "closely monitoring increased economic risk."

Forward-Looking Statements

In its closing remarks, CN summarized its Q1 performance and outlook, emphasizing that it had established "good 2025 footing with solid Q1 results." The company reiterated its expectation of low to mid-single-digit RTM growth for the year, with earnings growth expected to accelerate in the second half.

Management highlighted its focus on "staying close to our customers" and "balancing operational and service excellence" as key priorities. The presentation concluded with a commitment to "remain focused on driving shareholder value creation."

Looking further ahead, CN outlined its 2024-2026 financial strategy, targeting high single-digit adjusted diluted EPS growth by "growing faster than the economy and pricing ahead of rail inflation" while delivering "incremental efficiency improvements." The company also reaffirmed its approach to capital allocation, which includes reinvesting in the business, creating shareholder value through dividends and share buybacks, and managing to a 2.5x adjusted debt-to-adjusted EBITDA ratio.

Overall, CN Railway’s Q1 2025 presentation portrayed a company that has successfully navigated seasonal operational challenges while maintaining financial discipline and a positive growth outlook despite economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.