Five things to watch in markets in the week ahead

Canadian National Railway (TSX:CNR) reported its second quarter 2025 results on July 22, delivering modest earnings growth despite revenue challenges and subsequently lowering its full-year outlook due to mounting headwinds from U.S. tariffs and currency pressures.

Quarterly Performance Highlights

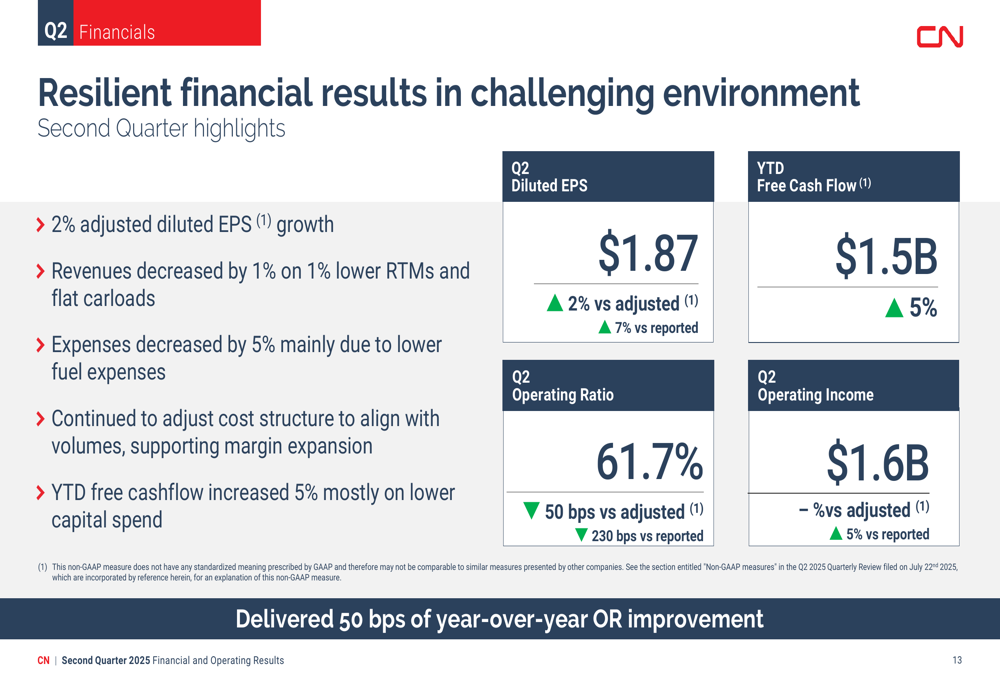

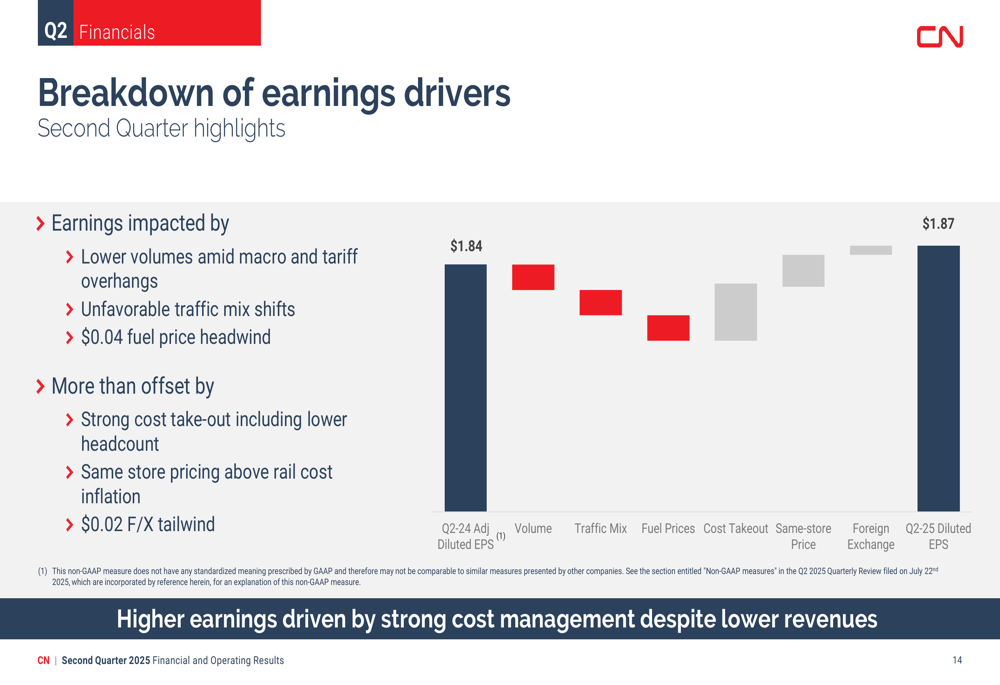

CN Railway achieved adjusted diluted earnings per share of $1.87 in Q2 2025, representing a 2% increase compared to adjusted results from the same period last year, and a 7% improvement over reported figures. The company managed this earnings growth despite a 1% decline in both revenues ($4.3 billion) and revenue ton miles (RTMs).

The railway’s operating ratio—a key efficiency metric where lower is better—improved to 61.7%, a 50 basis point enhancement versus adjusted prior-year results and 230 basis points better than reported figures. Year-to-date free cash flow reached $1.5 billion, up 5% from the previous year.

"Higher earnings were driven by strong cost management despite lower revenues," noted the company in its presentation. Operating expenses decreased by 5%, primarily due to lower fuel expenses, which fell 25% ($138 million) on a constant currency basis. The company continued to adjust its cost structure to align with volumes, supporting margin expansion despite the challenging environment.

Operational Improvements

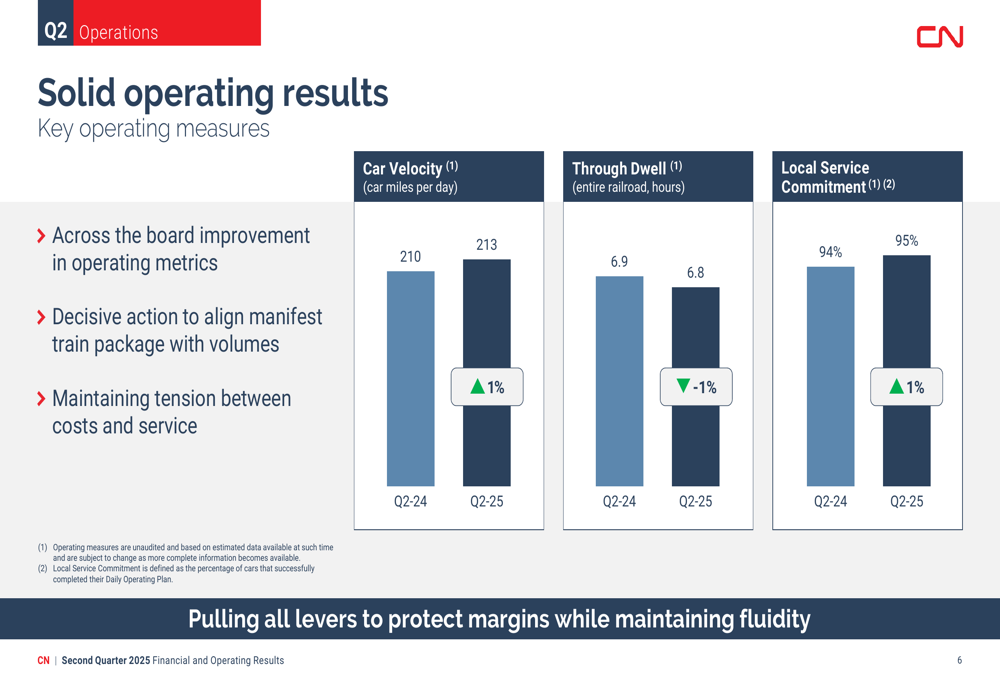

CN Railway reported solid operational metrics for the quarter, with car velocity increasing to 213 car miles per day (up 1%), through dwell time improving to 6.8 hours (down 1%), and local service commitment rising to 95% (up 1%). These improvements demonstrate the company’s focus on operational efficiency amid volume pressures.

The railway highlighted several efficiency initiatives contributing to its performance, including a 4% year-to-date reduction in train delays caused by work blocks, an 11% improvement in gross ton miles per train and engine employee, and a 7% increase in tie installation efficiency.

"Pulling all levers to protect margins while maintaining fluidity," the company stated, emphasizing its approach to balancing service quality with cost management during a period of economic uncertainty.

Segment Performance

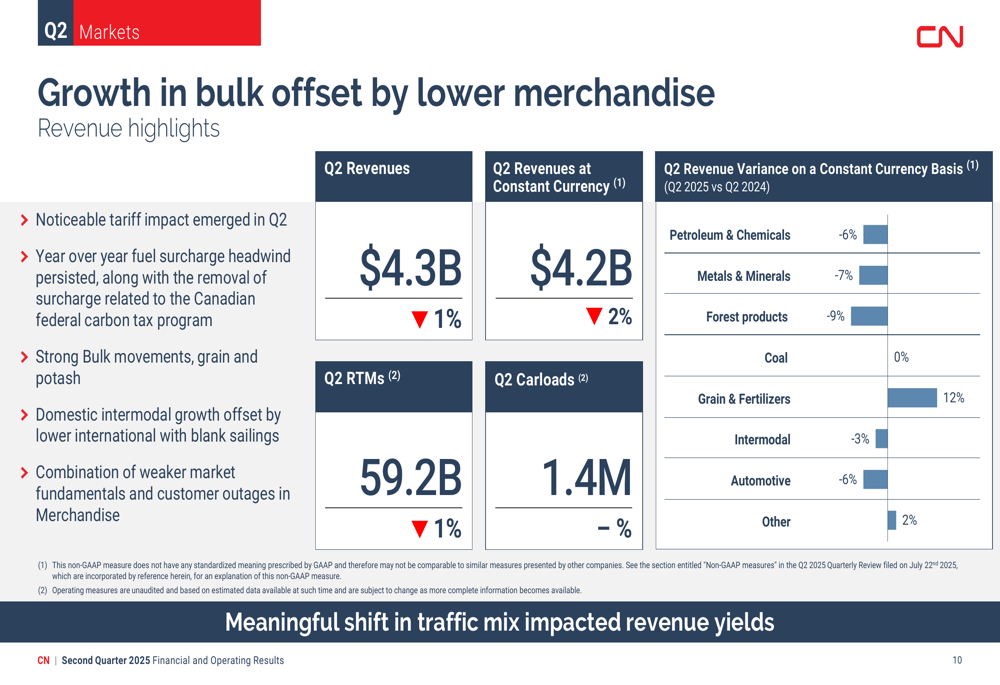

CN Railway’s revenue performance varied significantly across business segments, reflecting shifting economic conditions and trade patterns. Grain and fertilizers stood out as the strongest performer with a 12% revenue increase on a constant currency basis, while forest products experienced the steepest decline at 9%.

Other segments showing weakness included petroleum and chemicals (down 6%), metals and minerals (down 7%), automotive (down 6%), and intermodal (down 3%). Coal revenues remained flat year-over-year, while the "other" category posted a 2% gain.

The company noted a "meaningful shift in traffic mix" that impacted revenue yields during the quarter. This mix shift toward lower-yield bulk commodities and away from higher-yield merchandise segments contributed to the overall revenue decline despite relatively stable volumes.

Revised Outlook & Guidance

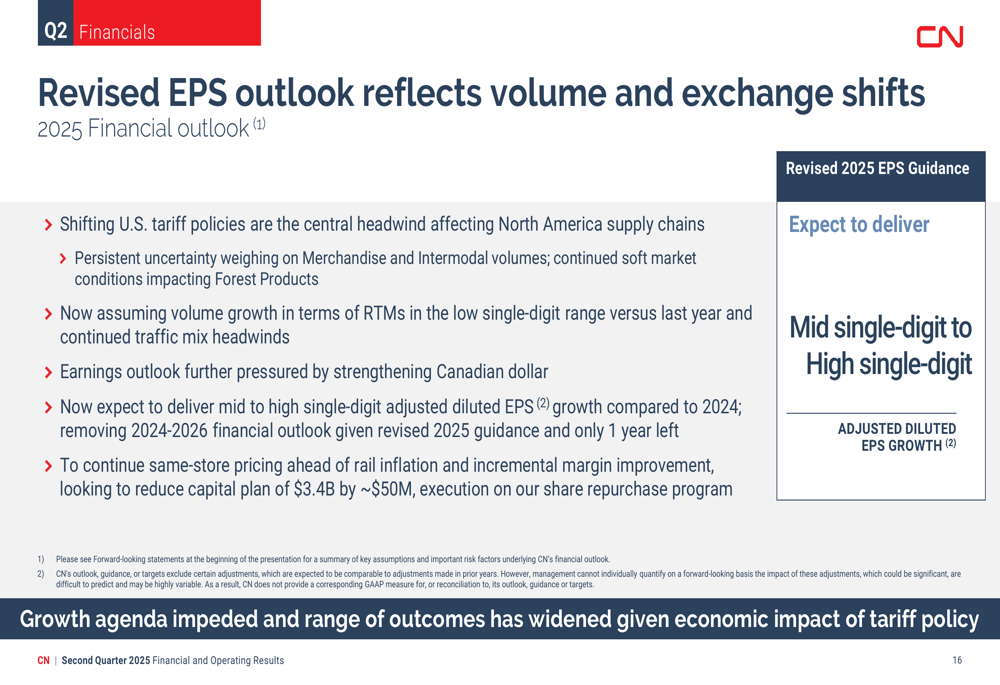

In a significant update, CN Railway revised its full-year outlook downward, citing several emerging headwinds. The company now expects to deliver "mid to high single-digit adjusted diluted EPS growth" for 2025, a reduction from the 10-15% growth guidance provided after Q1 results.

The revised outlook reflects several challenges, including:

1. Shifting U.S. tariff policies creating headwinds across multiple business segments

2. Persistent uncertainty weighing on merchandise and intermodal volumes

3. Continued soft market conditions impacting forest products

4. A strengthening Canadian dollar pressuring earnings

Volume growth expectations were also reduced, with the company now assuming "low single-digit RTM growth" for the year, down from the previous "low to mid-single digit" guidance.

The company provided a detailed segment-by-segment outlook, highlighting particular concerns in forest products ("ongoing weak market fundamentals and impact of US trade measures"), automotive ("impact of tariffs impacting production forecasts and flows"), and international intermodal ("H2 outlook for NA imports has softened due to pull-forward and US tariff impact").

Executive Commentary

Tracy Robinson, President and Chief Executive Officer, emphasized the company’s responsive approach to changing conditions, stating that CN Railway is "reacting with urgency" to the evolving environment. The company is "acting with urgency to align resources with demand" while "staying close to our customers."

"Driving shareholder value creation is our priority," Robinson affirmed, underscoring the company’s commitment to navigating the challenging environment effectively.

Ghislain Houle, Chief Financial Officer, highlighted the company’s resilience, noting that CN Railway "delivered 50 basis points of year-over-year OR improvement" despite the challenging conditions. The focus on cost management and operational efficiency remains central to the company’s strategy for maintaining profitability amid volume pressures.

The stock closed at $141.62 on the day of the presentation, down 0.34%, as investors digested the mixed results and lowered guidance. While the company demonstrated effective cost management and operational improvements, the reduced outlook reflects growing concerns about economic headwinds and trade uncertainties affecting the North American rail sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.