TSX lower as gold rally takes a breather

Introduction & Market Context

ConocoPhillips (NYSE:COP) reported second-quarter 2025 results on August 7, showing a sequential decline in earnings primarily driven by lower commodity prices, while production volumes exceeded guidance. The company’s stock traded up 0.96% in premarket to $94.00 following the presentation, suggesting investors were focusing on operational achievements and forward guidance rather than the earnings decline.

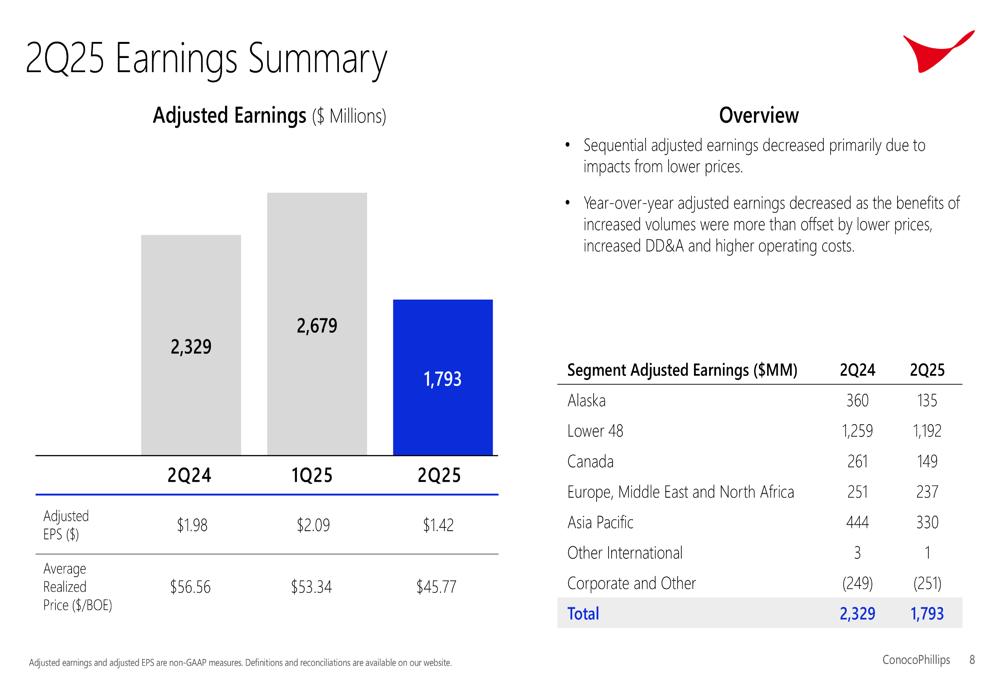

The oil and gas producer reported adjusted earnings per share of $1.42 for Q2 2025, down from $2.09 in the previous quarter and $1.98 in the same quarter last year, as lower realized prices offset production gains.

Quarterly Performance Highlights

ConocoPhillips delivered second-quarter production of 2,391 thousand barrels of oil equivalent per day (MBOED), exceeding the company’s guidance range of 2,340-2,380 MBOED. Despite this operational success, financial metrics showed pressure from market conditions.

As shown in the following quarterly earnings summary:

Adjusted earnings fell to $1.793 billion in Q2 2025 from $2.679 billion in Q1 2025 and $2.329 billion in Q2 2024. The company’s average realized price dropped to $45.77 per barrel of oil equivalent (BOE) in Q2 2025, compared to $53.34 in Q1 2025 and $56.56 in Q2 2024.

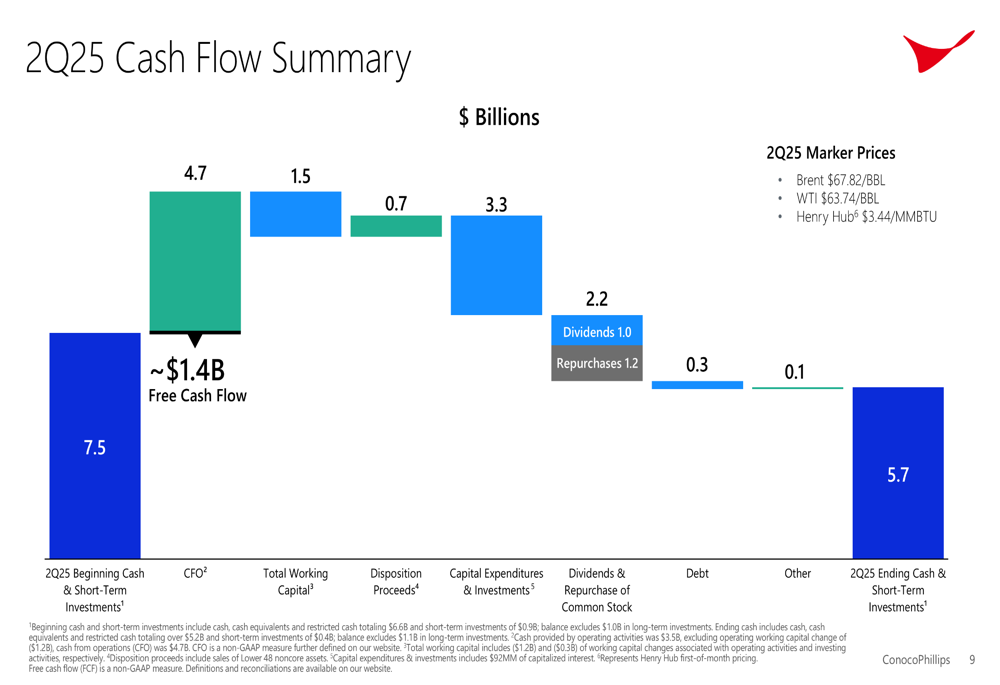

Cash flow from operations reached $4.7 billion, generating free cash flow of $1.4 billion after capital expenditures. The company ended the quarter with $5.7 billion in cash and short-term investments.

The following cash flow summary illustrates the company’s financial movements during Q2:

ConocoPhillips maintained its commitment to shareholder returns, distributing $2.2 billion through $1.0 billion in dividends and $1.2 billion in share repurchases during the quarter. The company remains on track to distribute approximately 45% of full-year cash flow from operations to shareholders.

Marathon Oil (NYSE:MRO) Integration Success

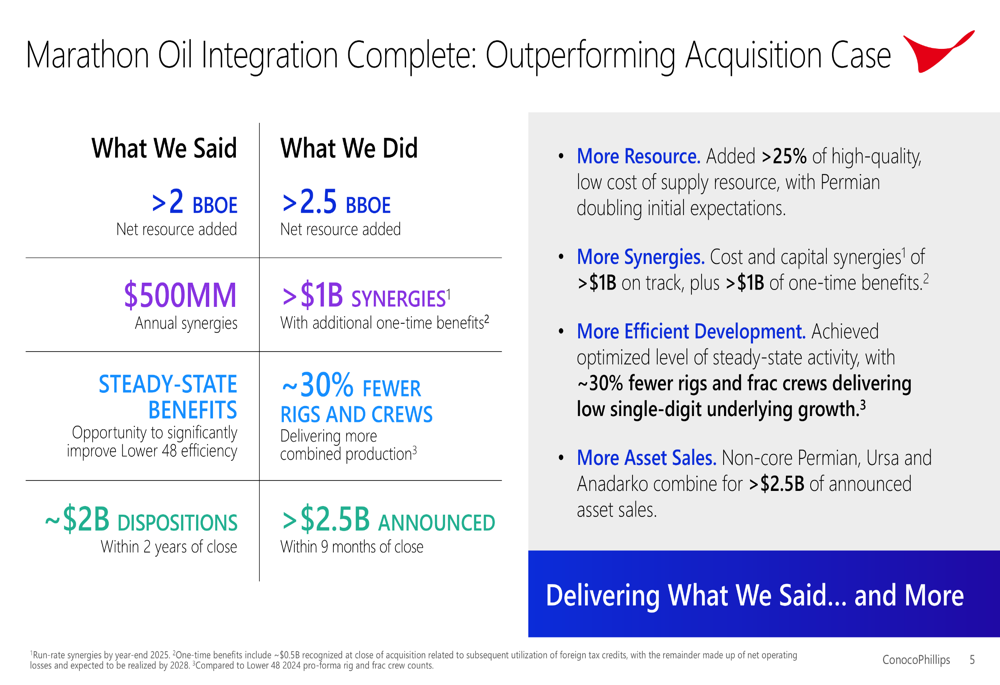

A significant highlight of the presentation was the completed integration of Marathon Oil, which has exceeded initial expectations across multiple metrics. The acquisition has added more than 2.5 billion barrels of oil equivalent (BBOE) to ConocoPhillips’ resource base, surpassing the initial target of 2 BBOE.

As detailed in the integration summary:

The company has achieved more than $1 billion in synergies, double the $500 million initially projected, plus more than $1 billion in one-time benefits. Operational efficiency has improved dramatically, with approximately 30% fewer rigs and frac crews delivering more combined production than before the merger.

"We’re delivering results while driving continuous improvement," the company noted in its presentation, highlighting how the Marathon integration has strengthened its portfolio, particularly in the Permian Basin where resource additions doubled initial expectations.

Portfolio Optimization

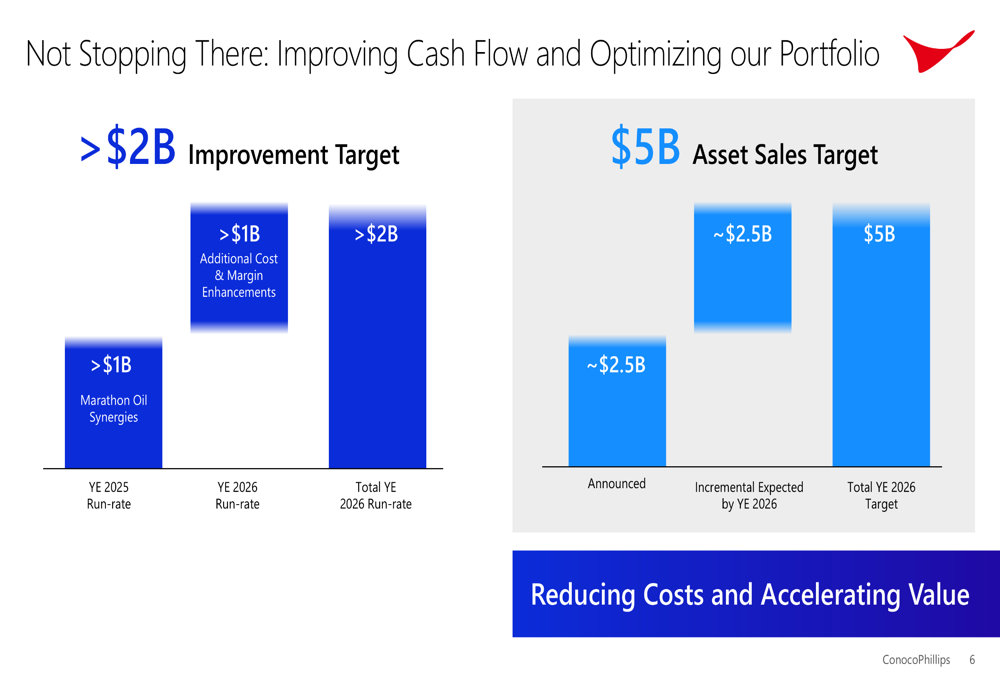

ConocoPhillips is actively optimizing its portfolio through both cost reductions and strategic asset sales. The company has announced more than $2.5 billion in asset sales within nine months of closing the Marathon acquisition, ahead of the initial two-year timeline for $2 billion in dispositions.

The portfolio optimization strategy is illustrated in this chart:

The company has now raised its total asset sale target to $5 billion by year-end 2026, with the recently announced agreement to sell Anadarko Basin assets for $1.3 billion contributing to this goal. These non-core divestitures allow ConocoPhillips to focus on its highest-return opportunities.

Beyond asset sales, the company is targeting more than $2 billion in improvements by year-end 2026, including more than $1 billion from Marathon Oil synergies and an additional $1 billion from cost reductions and margin enhancements.

Forward-Looking Statements

Despite the quarterly earnings decline, ConocoPhillips maintained its full-year production guidance midpoint, even after accounting for the Anadarko Basin asset sale. Capital and cost guidance also remained unchanged.

The company expects stronger free cash flow in the second half of 2025, driven by contributions from its Australia Pacific LNG (APLNG) project, tax benefits, and lower capital spending.

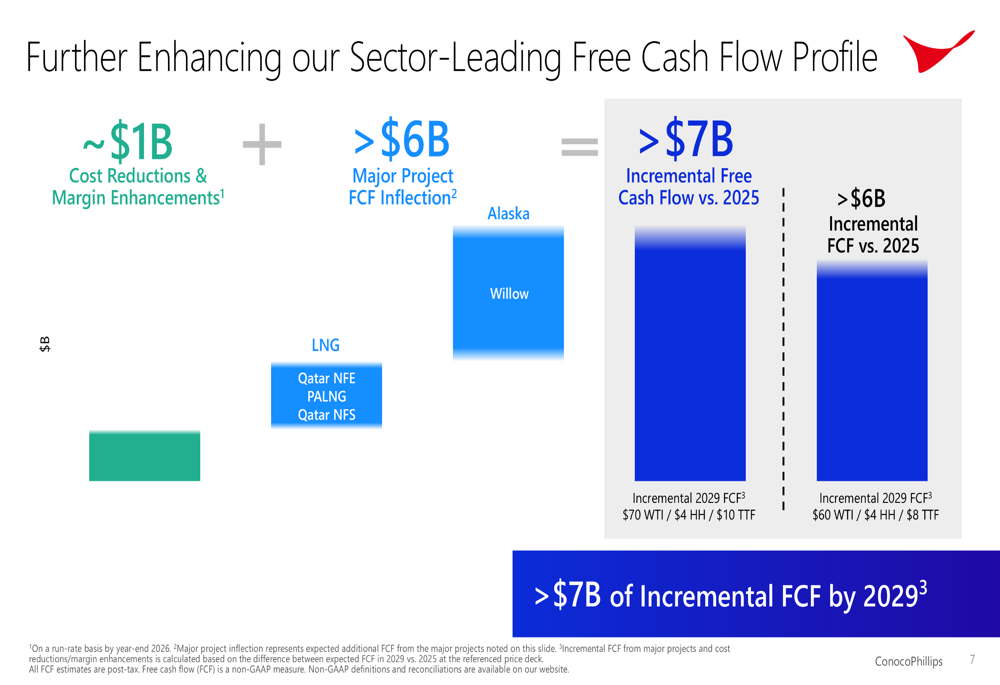

Looking further ahead, ConocoPhillips projects a significant improvement in its free cash flow profile:

By 2029, the company expects to generate more than $7 billion in incremental free cash flow compared to 2025 levels, assuming $70 WTI oil prices. This growth will be driven by cost reductions, margin enhancements, and major project contributions from Alaska (Willow) and LNG projects (Qatar NFE, PALNG, and Qatar NFS).

Commodity Price Realizations

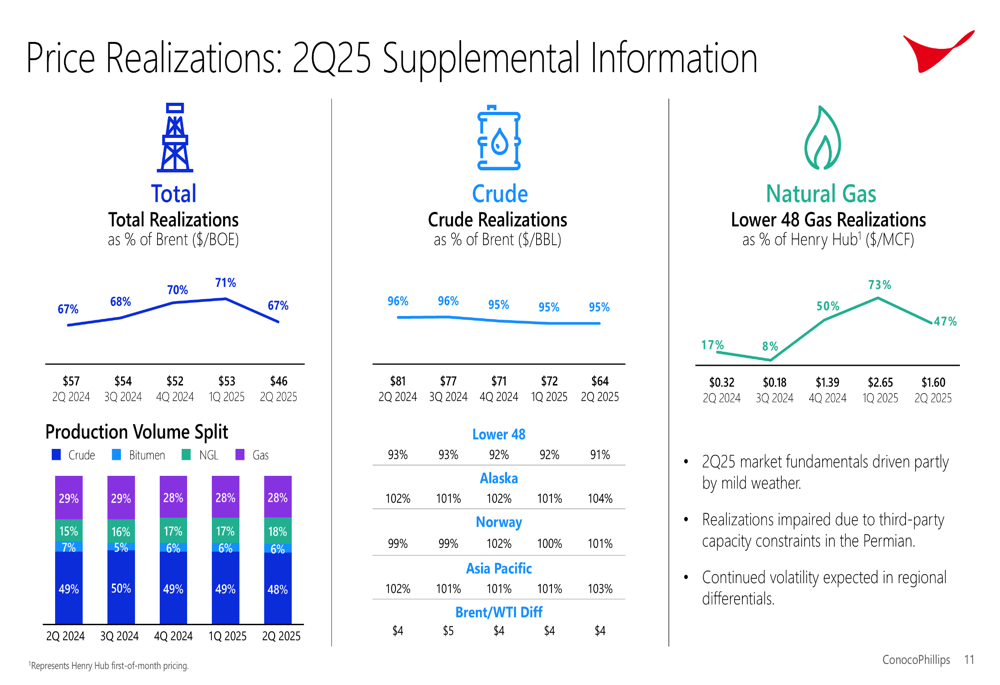

The second quarter’s financial performance was significantly impacted by lower commodity price realizations across the portfolio. Total (EPA:TTEF) realizations as a percentage of Brent crude fell to 67% in Q2 2025 from 71% in Q1 2025.

The following chart details the company’s price realizations:

Natural gas realizations in the Lower 48 were particularly weak at 47% of Henry Hub prices ($1.60/MCF), down from 73% in the previous quarter. The company attributed this decline to mild weather conditions and third-party capacity constraints in the Permian Basin, noting that "continued volatility expected in regional differentials" would likely persist.

Despite these near-term challenges with commodity prices, ConocoPhillips emphasized its long-term competitive advantages, including what it describes as "unmatched Lower 48 inventory depth and quality" and "differentiated longer-cycle investments in LNG and Alaska" that position the company for sustainable growth and returns through market cycles.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.