Bill Gross warns on gold momentum as regional bank stocks tumble

Cooper Standard (NYSE:CPS) shares jumped over 17% in premarket trading after the company’s Q2 2025 earnings presentation revealed significant margin improvements despite relatively flat sales. The automotive supplier reported continued progress in its operational efficiency initiatives and maintained its positive outlook for the full year despite market uncertainties.

Quarterly Performance Highlights

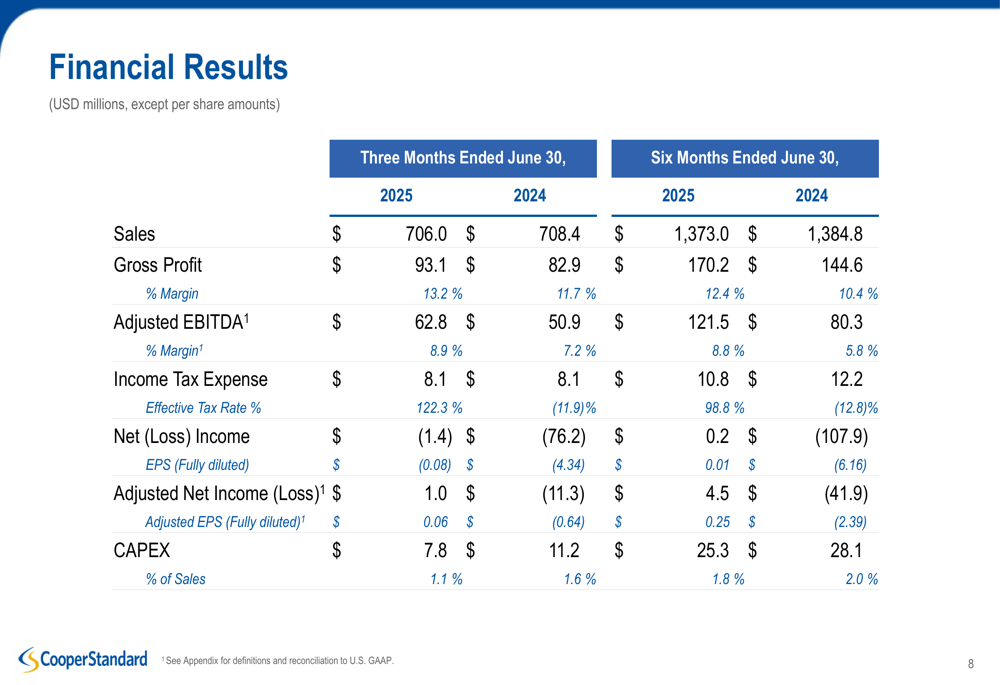

Cooper Standard reported Q2 2025 sales of $706.0 million, slightly down from $708.4 million in the same period last year. However, the company achieved substantial improvements in profitability metrics, with adjusted EBITDA increasing to $62.8 million from $50.9 million in Q2 2024, representing an adjusted EBITDA margin of 8.9% compared to 7.2% in the prior year.

The company’s net loss narrowed dramatically to $1.4 million, a significant improvement from the $76.2 million loss reported in Q2 2024. For the first half of 2025, Cooper Standard achieved a slight net income of $0.2 million, compared to a loss of $107.9 million in the first half of 2024.

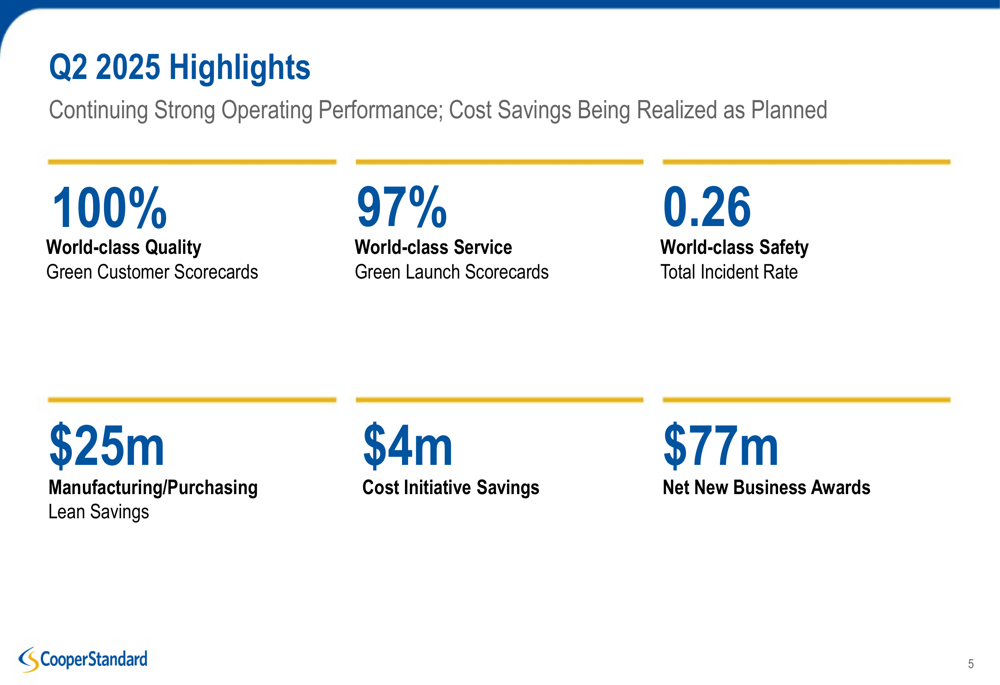

As shown in the following highlights from the presentation, the company maintained strong operational performance across key metrics:

The company’s focus on operational excellence has earned it recognition from major automotive manufacturers, reinforcing its position as a preferred supplier in the industry.

Detailed Financial Analysis

Cooper Standard’s Q2 2025 results demonstrate the impact of its cost-saving initiatives and operational improvements. While sales remained relatively flat year-over-year, the company achieved significant gains in profitability through manufacturing and purchasing efficiencies.

The following table details the company’s financial performance for both the quarter and year-to-date periods:

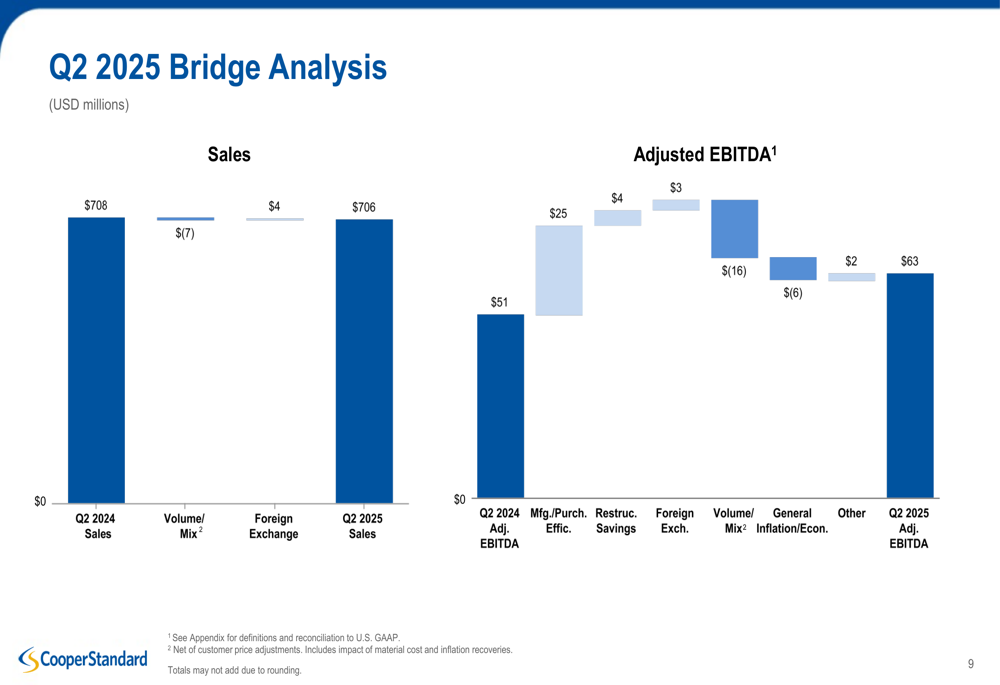

A bridge analysis of the Q2 results reveals that manufacturing and purchasing efficiencies contributed $25 million to adjusted EBITDA, while restructuring savings added another $4 million. These gains were partially offset by negative volume/mix effects of $16 million and general inflation impacts of $6 million.

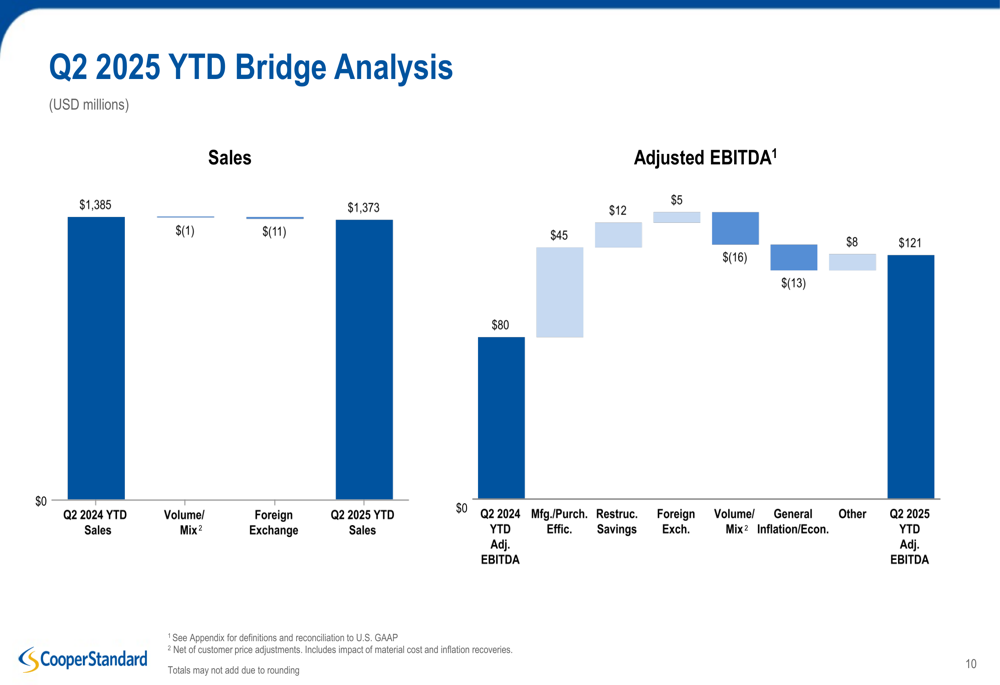

The year-to-date bridge analysis shows even stronger contributions from efficiency initiatives, with manufacturing and purchasing improvements adding $45 million to adjusted EBITDA and restructuring savings contributing $12 million.

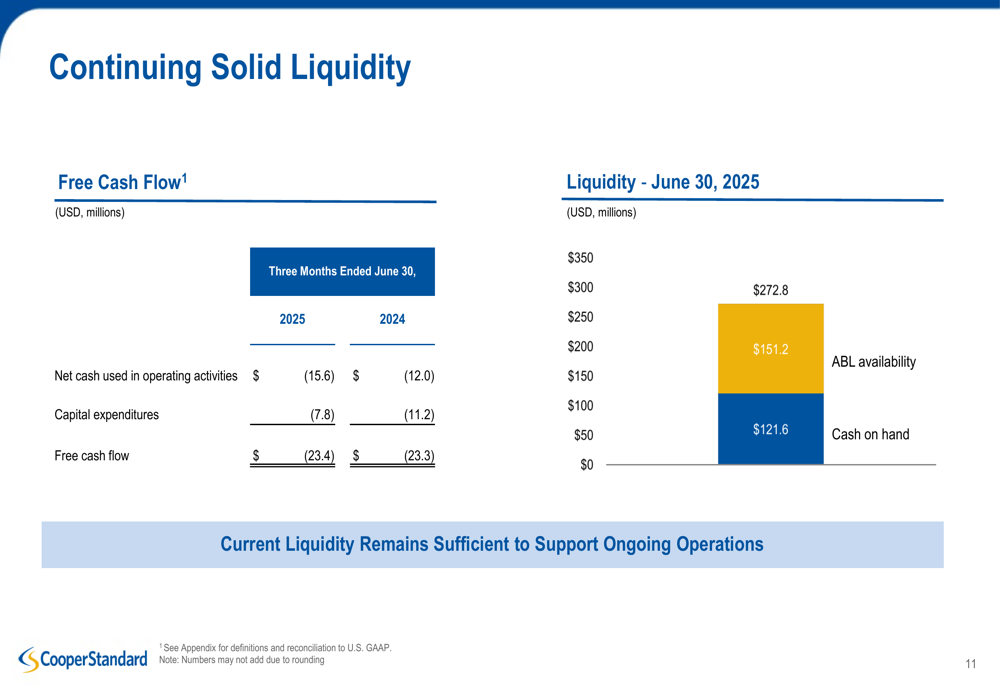

Despite the improved operating performance, Cooper Standard reported negative free cash flow of $23.4 million for Q2 2025, similar to the $23.3 million negative free cash flow in the same period last year. However, the company maintains a solid liquidity position with $272.8 million in total liquidity as of June 30, 2025.

Strategic Initiatives

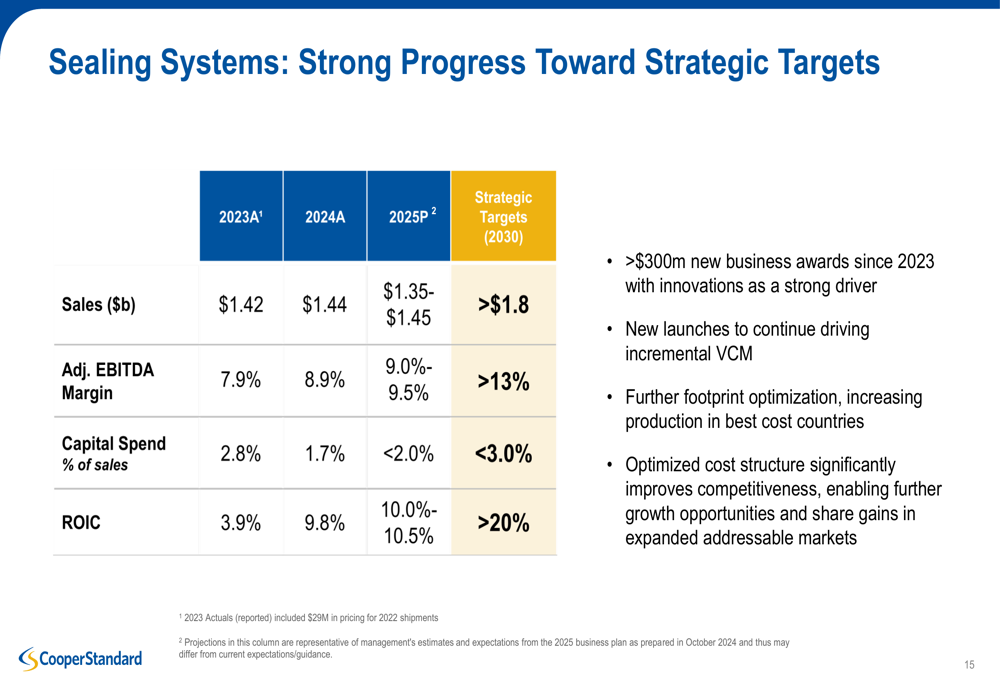

Cooper Standard continues to make progress toward its strategic goals in both of its main business segments. The company’s Sealing Systems segment is on track to achieve its 2025 projected adjusted EBITDA margin of 9.0-9.5%, up from 8.9% in 2024. The segment has secured over $300 million in new business awards since 2023 and continues to optimize its footprint and cost structure.

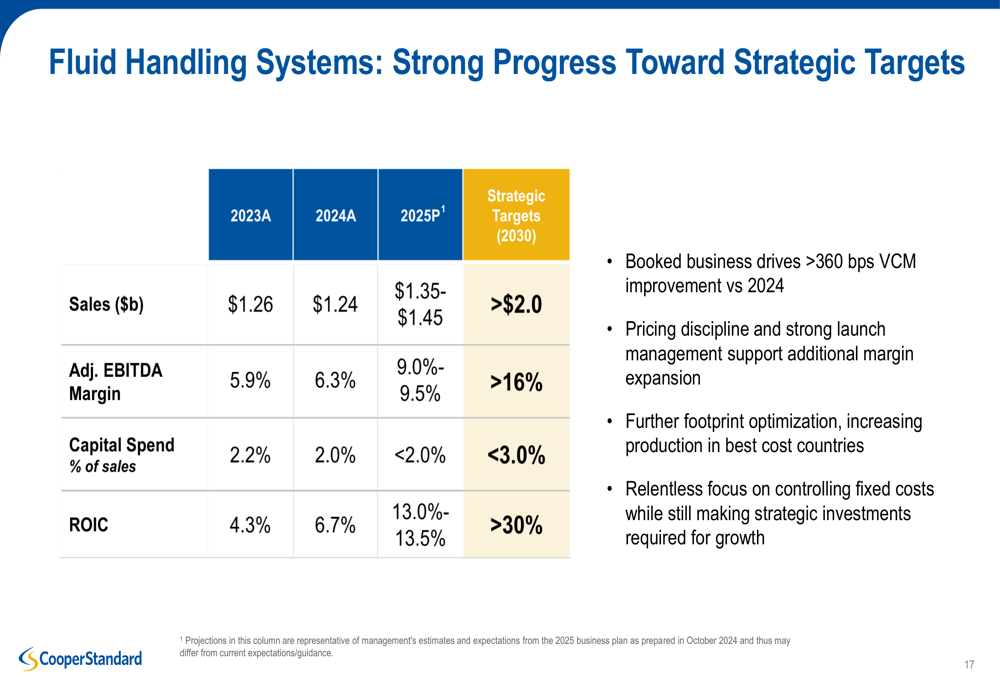

The Fluid Handling Systems segment is showing even more dramatic improvement, with projected adjusted EBITDA margin of 9.0-9.5% for 2025, up from 6.3% in 2024. The segment is benefiting from pricing discipline, strong launch management, and continued focus on controlling fixed costs.

Cooper Standard is strategically positioning itself to capitalize on the growing hybrid vehicle market, which presents significant content-per-vehicle opportunities. The company is also leveraging digital transformation and AI to optimize asset utilization and drive further operational improvements.

Forward-Looking Statements

Despite uncertainties around trade policy and potential tariff impacts, Cooper Standard maintains its positive outlook for 2025. The company expressed confidence in its ability to manage tariff-related challenges and expects to mitigate or recover associated costs from customers.

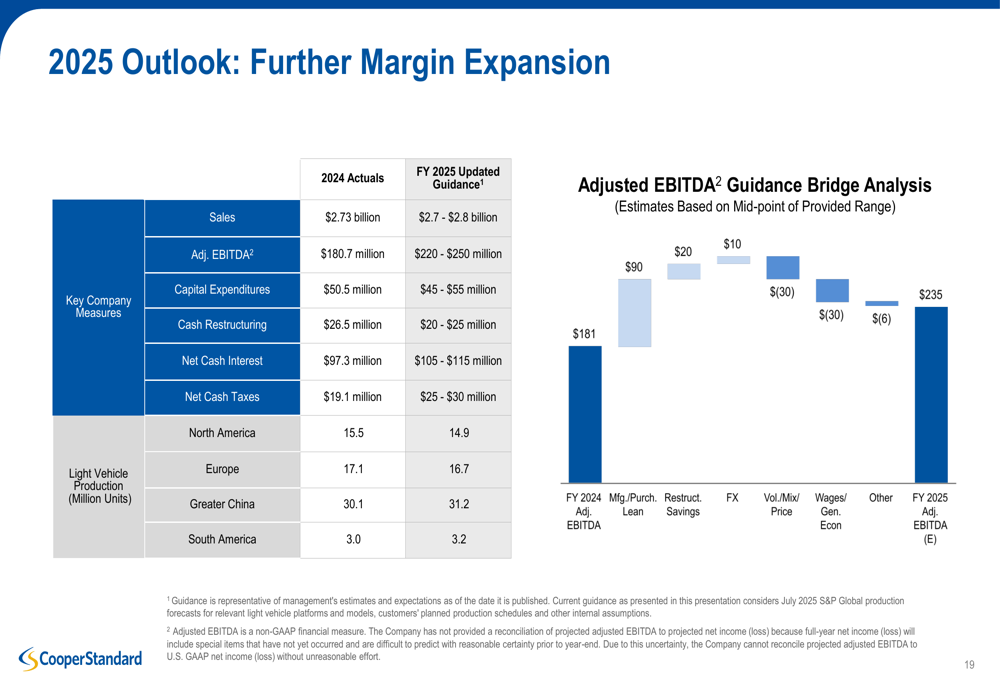

For the full year 2025, Cooper Standard maintained its guidance of $2.7-2.8 billion in sales and adjusted EBITDA of $220-250 million, representing significant improvement from the $180.7 million reported in 2024.

The company’s guidance reflects continued confidence in its ability to drive margin expansion through manufacturing and purchasing efficiencies, despite headwinds from volume/mix effects and general economic pressures.

This positive outlook aligns with the company’s performance in Q1 2025, when it reported a net income of $1.6 million, a turnaround from a $31.7 million loss in Q1 2024. The continued focus on lean initiatives and restructuring efforts appears to be yielding sustainable results, supporting the company’s long-term strategic targets of achieving double-digit EBITDA margins and strong returns on invested capital.

The market’s positive reaction, with shares up 17.43% in premarket trading to $28.30, suggests investors are encouraged by Cooper Standard’s continued progress in improving profitability despite challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.