Street Calls of the Week

Introduction & Market Context

Crayon Group Holding ASA (OB:CRAYN) presented its Q1 2025 quarterly results on May 21, 2025, highlighting solid growth in international markets while navigating a softer performance in its Nordic home region. The company, a global provider of IT services specializing in software and cloud solutions, reported overall growth amid its ongoing integration with SoftwareOne.

The presentation, delivered by CEO Melissa Mulholland and CFO Brede Huser, emphasized Crayon’s strengthening position in Microsoft (NASDAQ:MSFT)’s evolving Cloud Solution Provider (CSP) ecosystem, where the tech giant is prioritizing higher-quality partners. This strategic positioning appears to be creating growth opportunities for established players like Crayon.

Quarterly Performance Highlights

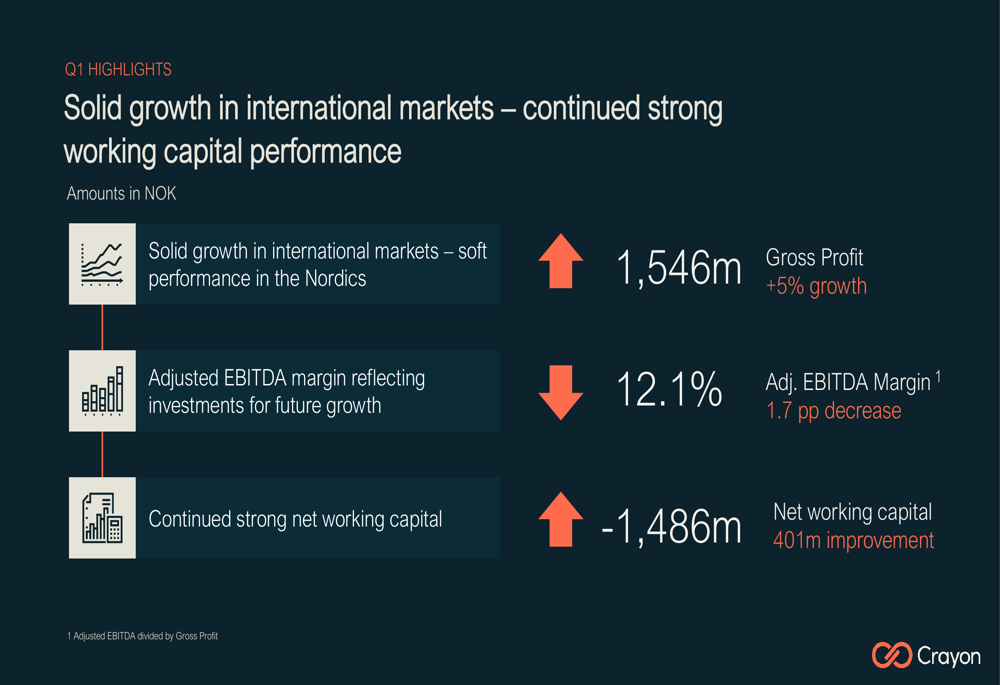

Crayon reported a gross profit of 1,546 million NOK for Q1 2025, representing a 5% year-over-year increase. However, the adjusted EBITDA margin decreased by 1.7 percentage points to 12.1%, which the company attributed to investments for future growth.

As shown in the following key performance indicators chart:

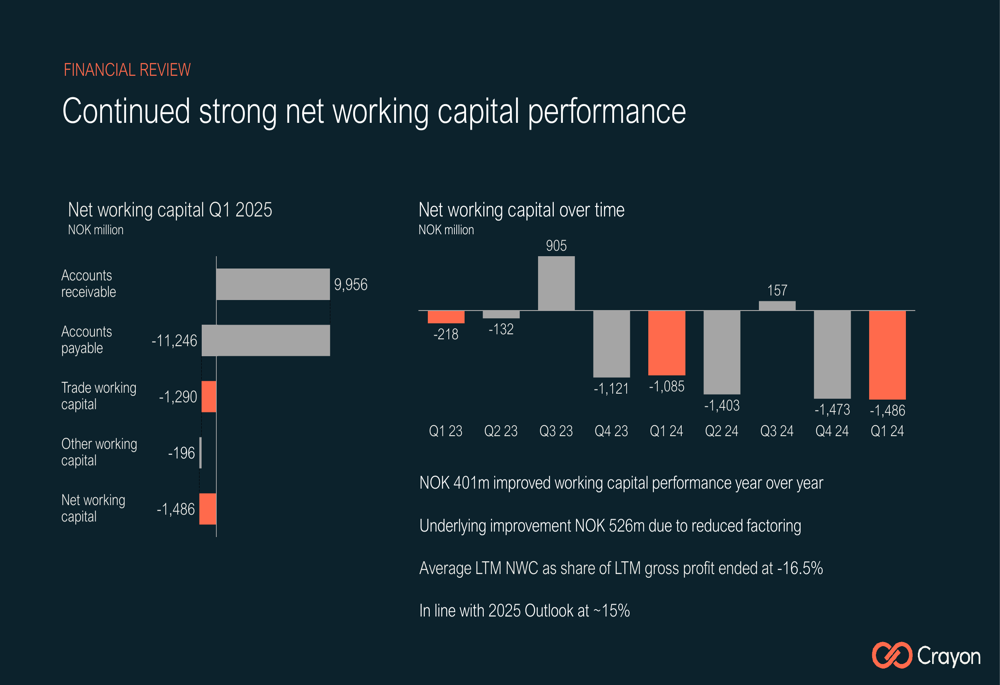

The company’s net working capital position improved significantly to -1,486 million NOK, representing a 401 million NOK improvement year-over-year. This strong working capital performance has been a consistent bright spot for Crayon, helping to maintain a robust financial position despite margin pressures.

Regional and Business Segment Analysis

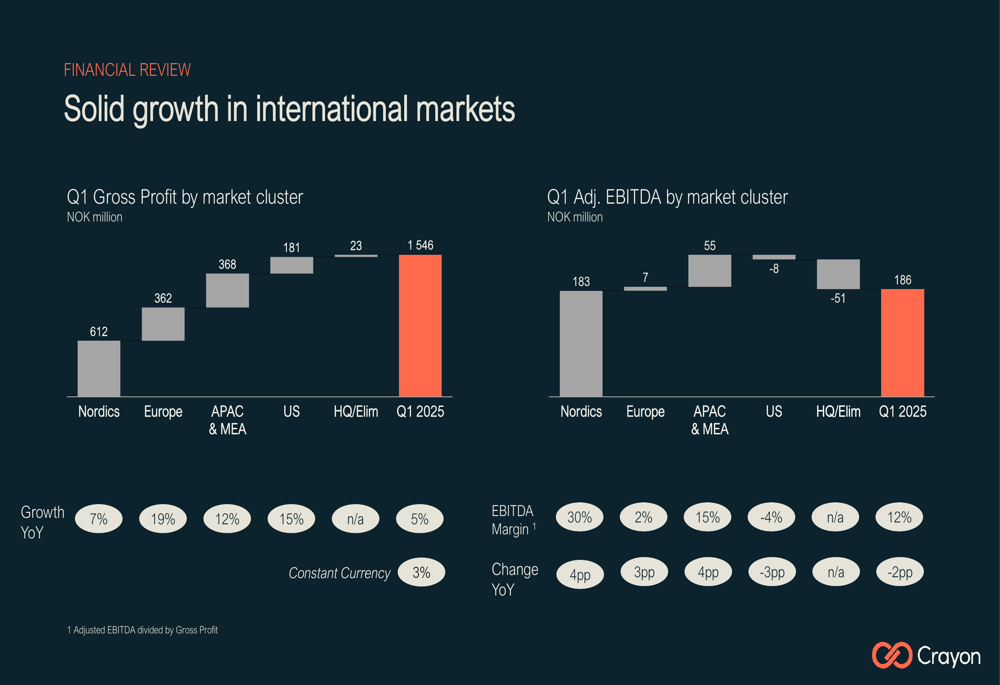

Crayon’s international markets demonstrated impressive growth, offsetting softer performance in the Nordic region. Europe led the way with 19% growth, followed by the US (15%) and APAC & MEA (12%), while the Nordic region posted a more modest 7% increase.

The following chart illustrates the regional breakdown of gross profit and adjusted EBITDA:

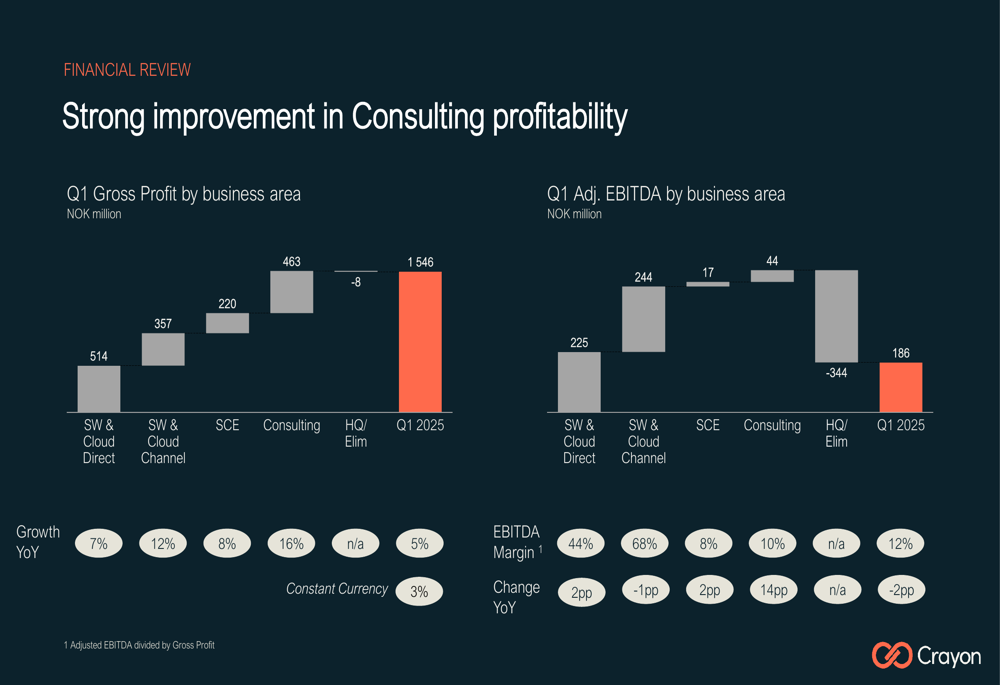

From a business segment perspective, Consulting showed particularly strong improvement in profitability, growing 16% year-over-year with a 10% EBITDA margin, up from -1% in Q1 2024. Software (ETR:SOWGn) & Cloud Channel services grew 12% with an impressive 68% EBITDA margin, while Software & Cloud Direct services increased 7% with a 44% EBITDA margin.

The business segment performance breakdown reveals the strength of Crayon’s diverse portfolio:

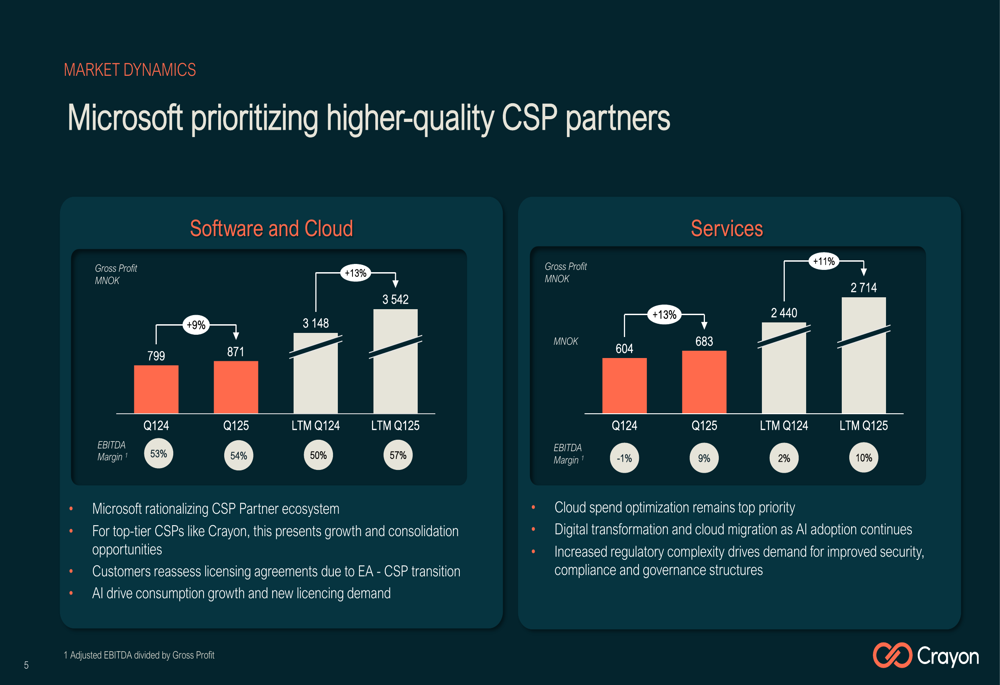

The company highlighted market dynamics favoring its position, particularly Microsoft’s rationalization of its CSP partner ecosystem and the ongoing EA-CSP transition, which is prompting customers to reassess their licensing agreements. Additionally, AI adoption is driving consumption growth across Crayon’s markets.

As illustrated in the market dynamics overview:

Financial Position and Working Capital

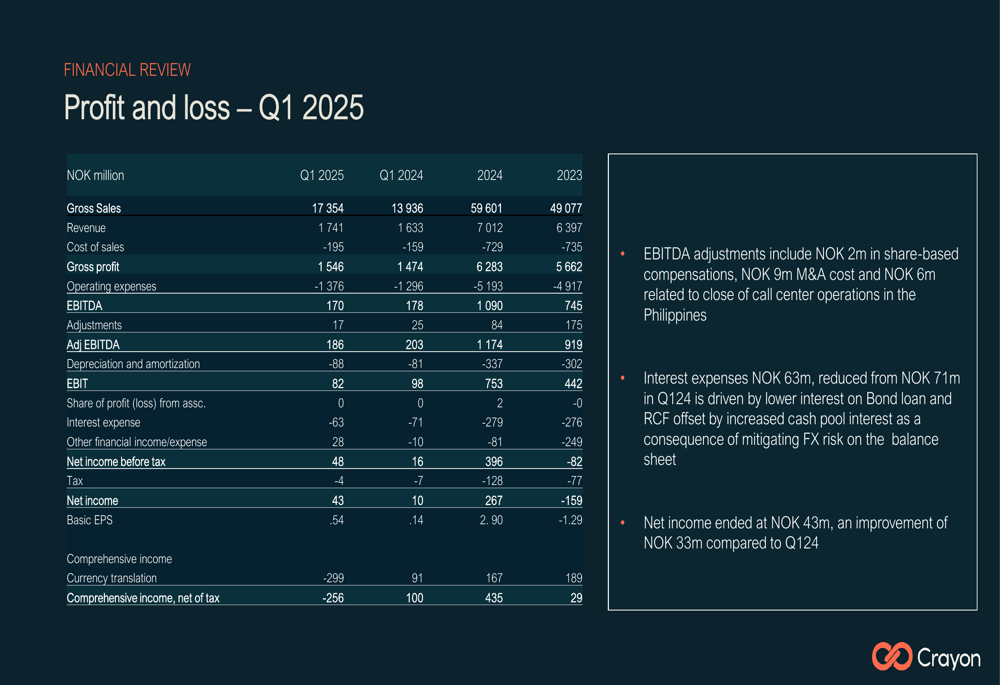

Crayon maintained a strong financial position in Q1 2025, with net income reaching 43 million NOK, an improvement of 33 million NOK compared to Q1 2024. The company’s balance sheet showed total assets of 19,179 million NOK, with shareholders’ equity of 2,701 million NOK.

The company’s working capital management continues to be exemplary, as shown in the following chart:

The average last twelve months (LTM) net working capital as a share of LTM gross profit ended at -16.5%, which aligns with the company’s 2025 outlook of approximately -15%. The underlying improvement in working capital was 526 million NOK when accounting for reduced factoring, which decreased to 122 million NOK from 247 million NOK in Q1 2024.

Crayon’s profit and loss statement reveals the detailed financial performance:

The company’s net debt to EBITDA ratio improved to 0.4x, down from 1.2x, reflecting a strengthened balance sheet. Both the revolving credit facility and overdraft facility remained undrawn by quarter end, contributing to a substantial liquidity reserve of 3,348 million NOK.

Strategic Initiatives and Future Outlook

A key strategic development for Crayon is its combination with SoftwareOne, creating what the company describes as "a stronger, global platform." Integration preparations are reportedly progressing well, with a focus on day-one readiness.

The company showcased its capabilities in data and AI solutions through a case study of a Singapore media conglomerate, highlighting how Crayon is helping automate media classification and metadata generation:

This project, valued at SGD $3.3 million in new AWS annual recurring revenue, demonstrates Crayon’s ability to deliver complex cloud-based AI and generative AI solutions in the media sector.

Looking ahead, Crayon emphasized that its key strengths and customer commitment will remain central as it accelerates growth, expands capabilities, and creates long-term value as part of the SoftwareOne organization. The integration is expected to enhance the company’s competitive position in the global software and cloud solutions market.

Crayon shares (OB:CRAYN) closed at 136.4 NOK on May 20, 2025, up 3.65% ahead of the earnings presentation, and have traded between 100.9 NOK and 144.4 NOK over the past 52 weeks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.