5 big analyst AI moves: Nvidia, AMD upgraded; ASML seen on €1,000 path

Introduction & Market Context

Darling Ingredients Inc (NYSE:DAR) released its Q2 2025 financial results on July 24, 2025, revealing a mixed performance with sequential improvement from Q1 but significant year-over-year challenges. The company’s shares fell 5.02% in premarket trading to $35.01, reflecting investor concerns despite some positive developments in certain business segments.

The quarterly results showed modest revenue growth of 1.8% year-over-year, but net income plummeted 83.9% compared to the same period last year. This continues a challenging 2025 for the company, which reported a loss in Q1, though Q2 marks a return to profitability.

Quarterly Performance Highlights

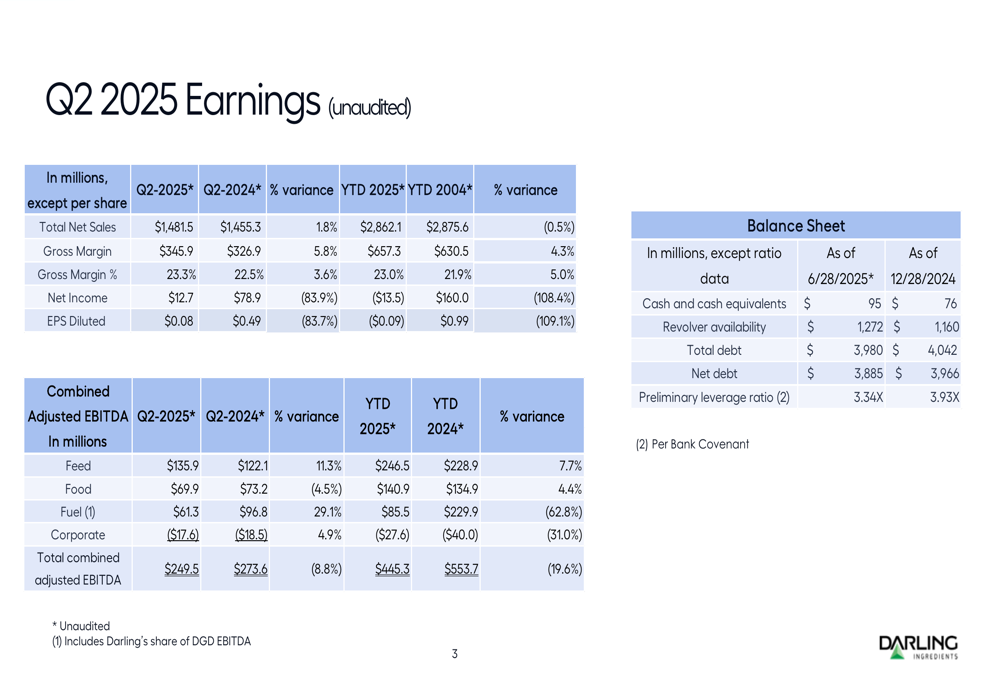

Darling Ingredients reported Q2 2025 net sales of $1,481.5 million, up 1.8% from $1,455.3 million in Q2 2024. Despite the revenue increase, net income fell dramatically to $12.7 million from $78.9 million in the prior-year period, resulting in diluted earnings per share of $0.08 compared to $0.49 in Q2 2024.

As shown in the following comprehensive financial results table, the company did achieve gross margin improvement, reaching 23.3% compared to 22.5% in the same quarter last year:

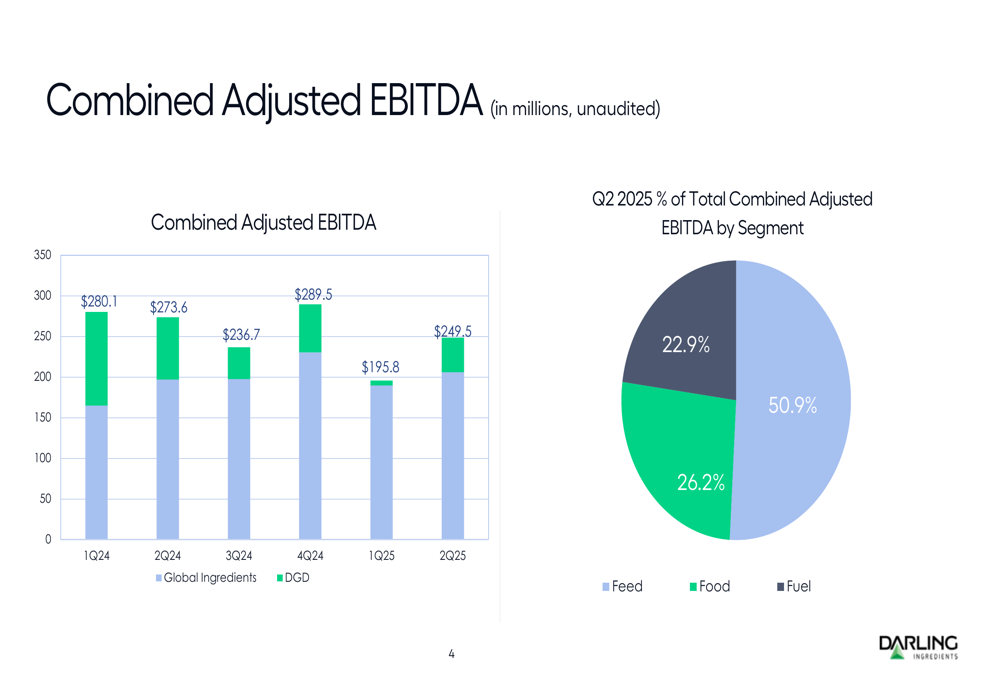

Combined adjusted EBITDA for Q2 2025 was $249.5 million, representing an 8.8% decrease from $273.6 million in Q2 2024. However, this marks a significant sequential improvement from the $195.8 million reported in Q1 2025, suggesting some stabilization in the business.

The following chart illustrates the quarterly progression of combined adjusted EBITDA, showing the recovery in Q2 2025 after a challenging start to the year:

Segment Analysis

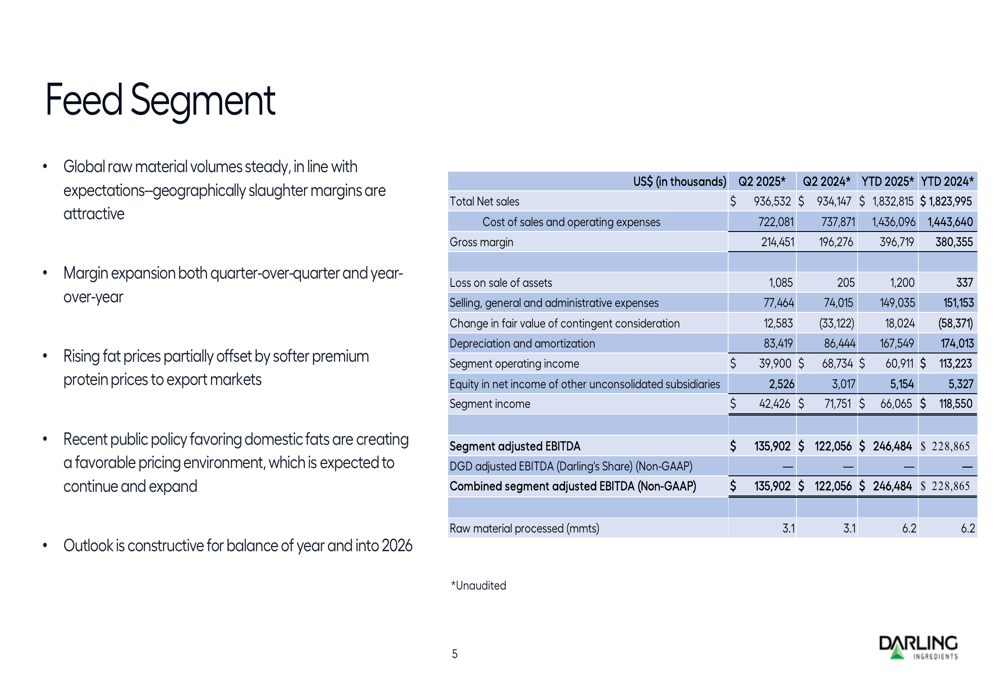

The Feed segment emerged as the bright spot in Darling’s portfolio, with segment adjusted EBITDA increasing 11.3% to $135.9 million compared to $122.1 million in Q2 2024. This segment now represents over 50% of the company’s total combined adjusted EBITDA, as shown in the segment breakdown chart above.

Key drivers for the Feed segment included steady raw material volumes and margin expansion, with rising fat prices partially offsetting softer premium protein prices. Management noted a favorable pricing environment due to recent public policy developments.

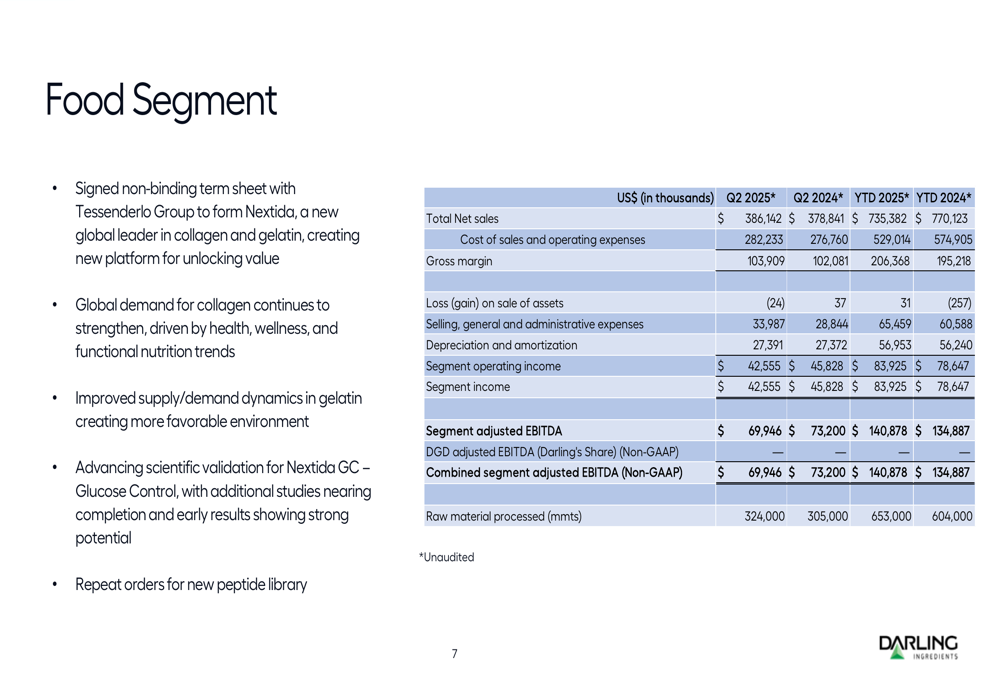

The Food segment delivered mixed results with adjusted EBITDA of $69.9 million, down 4.5% from $73.2 million in Q2 2024. Despite the slight decline, the company highlighted several positive developments, including strengthening global demand for collagen and improved supply/demand dynamics in gelatin.

A notable strategic initiative in this segment was the signing of a non-binding term sheet with Tessenderlo Group to form Nextida, potentially strengthening Darling’s position in the collagen market.

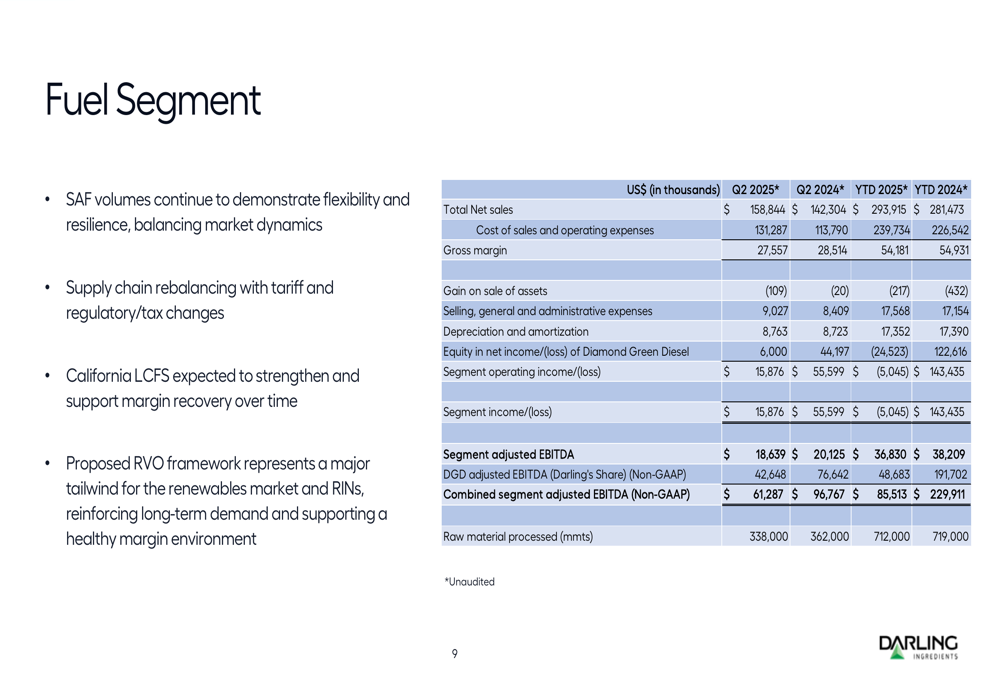

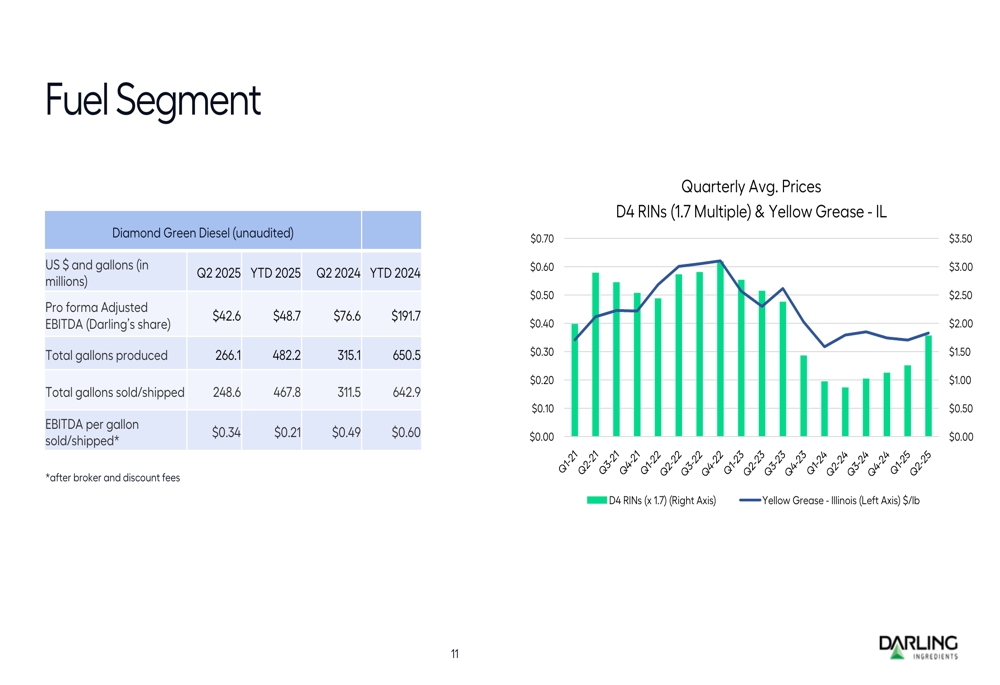

The Fuel segment faced the most significant challenges, with combined segment adjusted EBITDA declining 29.1% to $61.3 million from $96.8 million in Q2 2024. This segment has been particularly impacted by market conditions affecting Diamond Green Diesel (DGD), Darling’s joint venture.

Diamond Green Diesel’s performance metrics showed significant year-over-year declines, with Darling’s share of pro forma adjusted EBITDA falling to $42.6 million from $76.6 million in Q2 2024. Total (EPA:TTEF) gallons produced decreased to 266.1 million from 315.1 million, while EBITDA per gallon sold dropped to $0.34 from $0.49.

Balance Sheet and Financial Position

Despite earnings challenges, Darling made progress in strengthening its balance sheet. As of June 28, 2025, the company reported:

- Cash and cash equivalents of $95 million, up from $76 million at the end of 2024

- Total debt of $3,980 million, down from $4,042 million

- Net debt of $3,885 million, improved from $3,966 million

- Preliminary leverage ratio of 3.34X, significantly better than 3.93X at year-end 2024

This debt reduction continues the trend noted in the Q1 earnings report, which mentioned $146.2 million in debt paid down during that quarter.

Forward-Looking Statements

Management expressed optimism about several market developments that could positively impact future performance:

1. California’s Low Carbon Fuel Standard (LCFS) is expected to strengthen and support margin recovery in the Fuel segment

2. The proposed Renewable Volume Obligation (RVO) framework represents a potential tailwind for renewable fuel markets

3. Global demand for collagen continues to strengthen, supporting the Food segment

4. Sustainable Aviation Fuel (SAF) volumes demonstrate flexibility and resilience despite current market challenges

The company’s outlook for the Feed segment remains constructive for the balance of the year and into 2026, driven by favorable pricing trends.

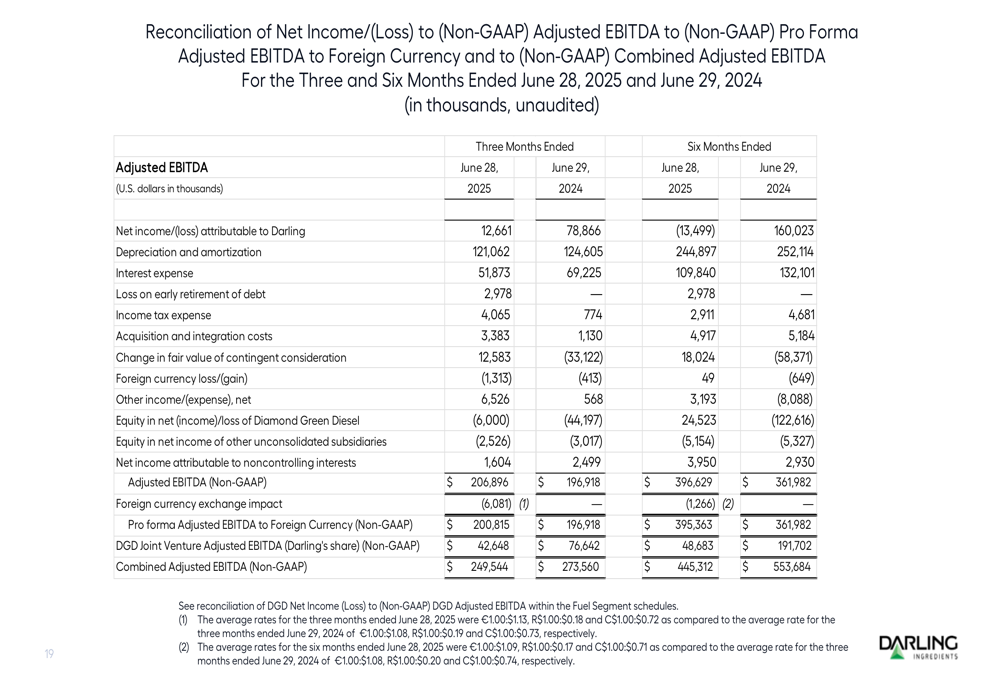

Adjusted EBITDA Reconciliation

The following reconciliation table provides insight into how Darling calculates its adjusted EBITDA figures, which are central to how the company presents its financial performance:

The reconciliation highlights the significant gap between reported net income and adjusted EBITDA metrics, with numerous adjustments including depreciation and amortization, income taxes, and interest expense.

In conclusion, Darling Ingredients’ Q2 2025 results present a mixed picture with sequential improvement from Q1 but continued year-over-year challenges. The Feed segment’s strong performance partially offset weaknesses in the Fuel segment, while balance sheet improvements demonstrate management’s focus on financial stability amid volatile market conditions. Investors will be watching closely to see if the sequential improvement continues in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.