Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Day One Biopharmaceuticals (NASDAQ:DAWN) presented its first quarter 2025 financial results on May 6, highlighting continued growth for its flagship product OJEMDA™ (tovorafenib) amid challenging market conditions. The company’s stock has faced pressure recently, trading near its 52-week low at $6.99 in after-hours trading, representing a 6.95% decline on the day of the presentation.

The biopharmaceutical company, focused on developing targeted therapies for pediatric cancers, maintained its commercial momentum with OJEMDA while working to establish the treatment as a standard of care for BRAF-altered pediatric low-grade glioma (pLGG).

Quarterly Performance Highlights

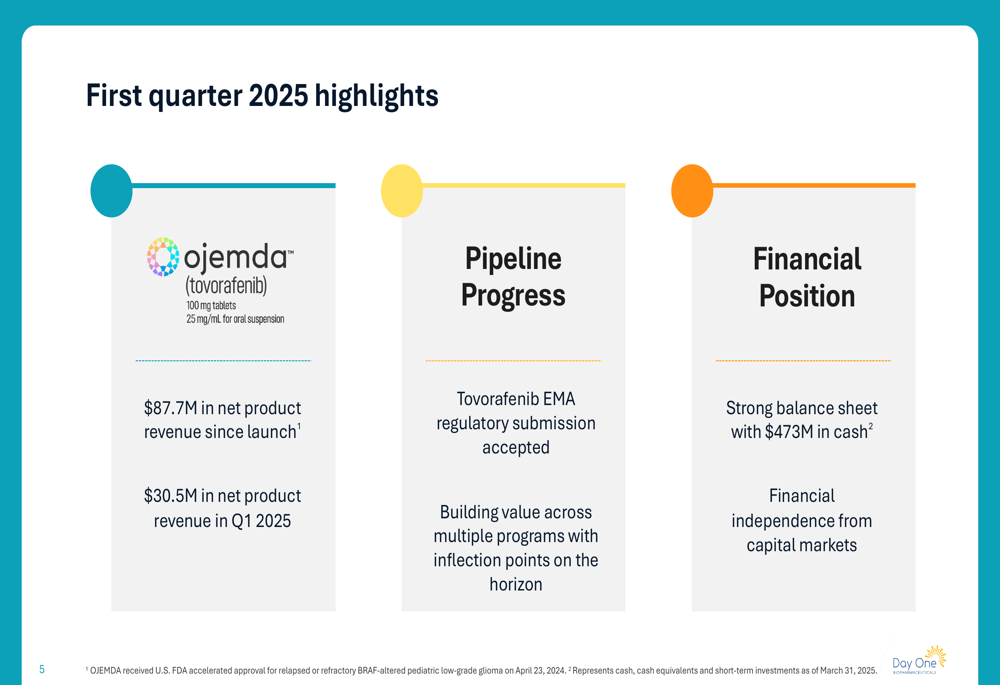

Day One reported several key achievements for Q1 2025, including continued revenue growth for OJEMDA and important regulatory progress.

As shown in the following comprehensive overview of the quarter’s highlights:

The company generated $30.5 million in net product revenue from OJEMDA in Q1 2025, bringing the total revenue since launch to $87.7 million. Additionally, Day One highlighted the acceptance of its Tovorafenib EMA regulatory submission and maintained a strong financial position with $473 million in cash, providing financial independence from capital markets.

OJEMDA Commercial Performance

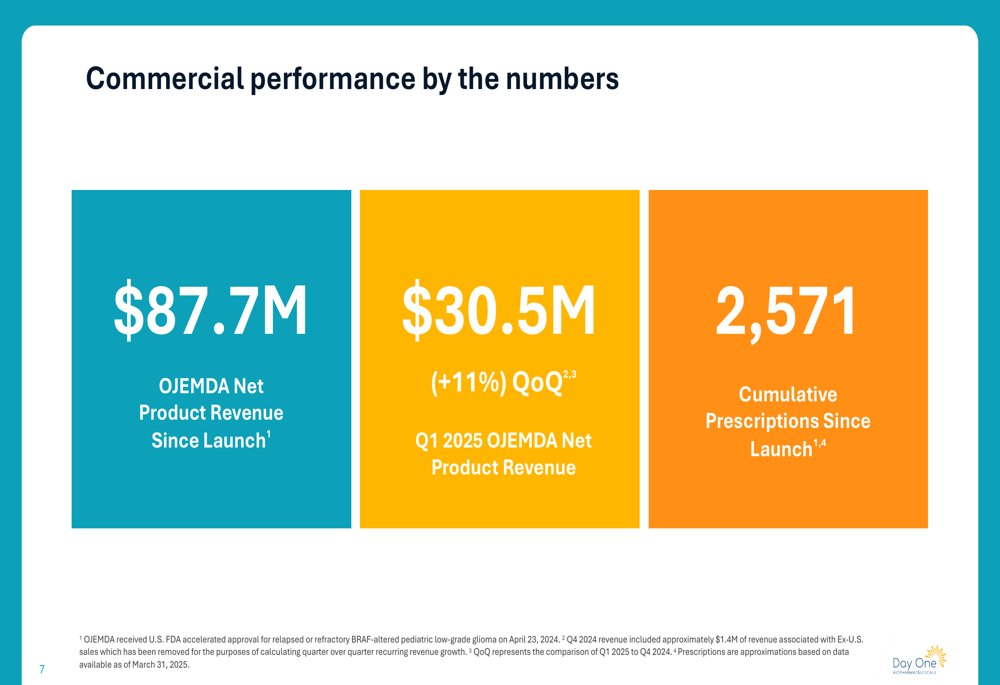

OJEMDA’s commercial performance showed continued growth, though at a more moderate pace compared to previous quarters. The company reported key metrics demonstrating the product’s market penetration and prescription trends.

The following chart illustrates the commercial performance by the numbers:

Day One has achieved 2,571 cumulative prescriptions since OJEMDA’s launch, reflecting the product’s growing adoption among healthcare providers. The quarterly revenue progression demonstrates consistent growth, though the pace has moderated compared to the 44% quarter-over-quarter growth seen in Q4 2024.

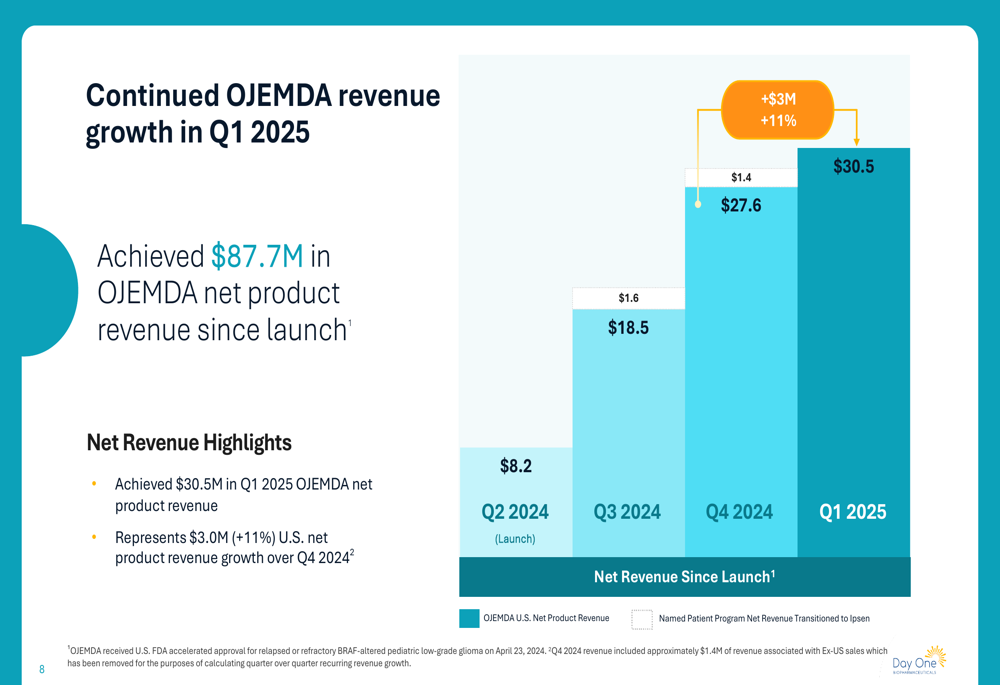

The revenue growth trajectory is clearly visualized in this chart:

OJEMDA’s net product revenue increased by $3.0 million (11%) in Q1 2025 compared to Q4 2024, reaching $30.5 million. This represents a slower growth rate than previous quarters but still demonstrates positive momentum for the relatively new product.

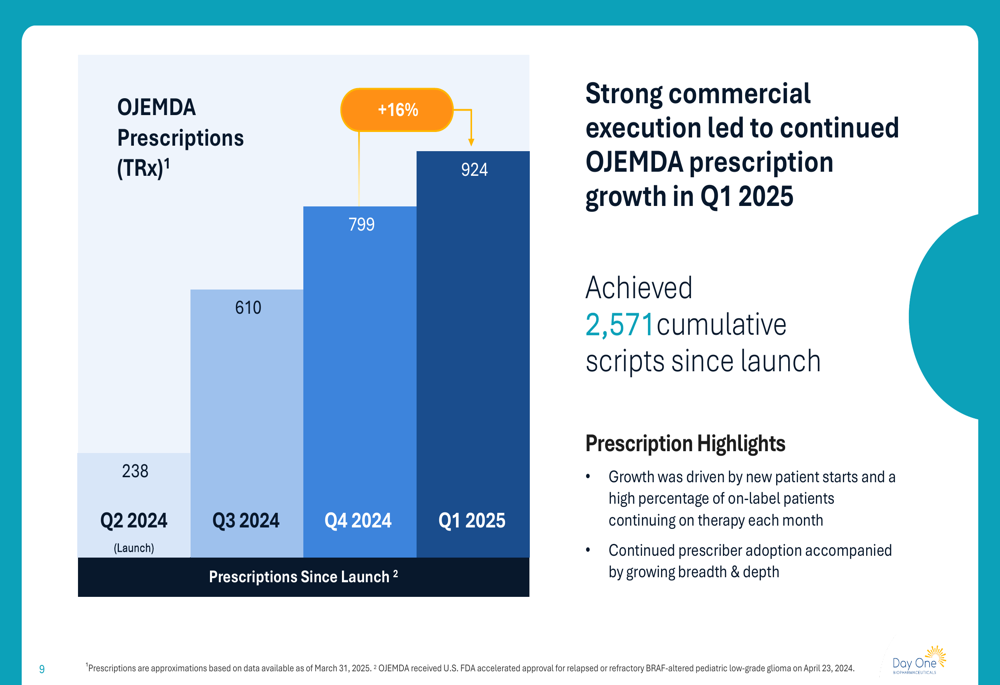

Prescription growth has followed a similar pattern, as shown in the following chart:

OJEMDA prescriptions grew by 16% quarter-over-quarter to 924 in Q1 2025, driven by new patient starts and high continuation rates among existing patients. The company noted that prescriber adoption continues to expand in both breadth and depth.

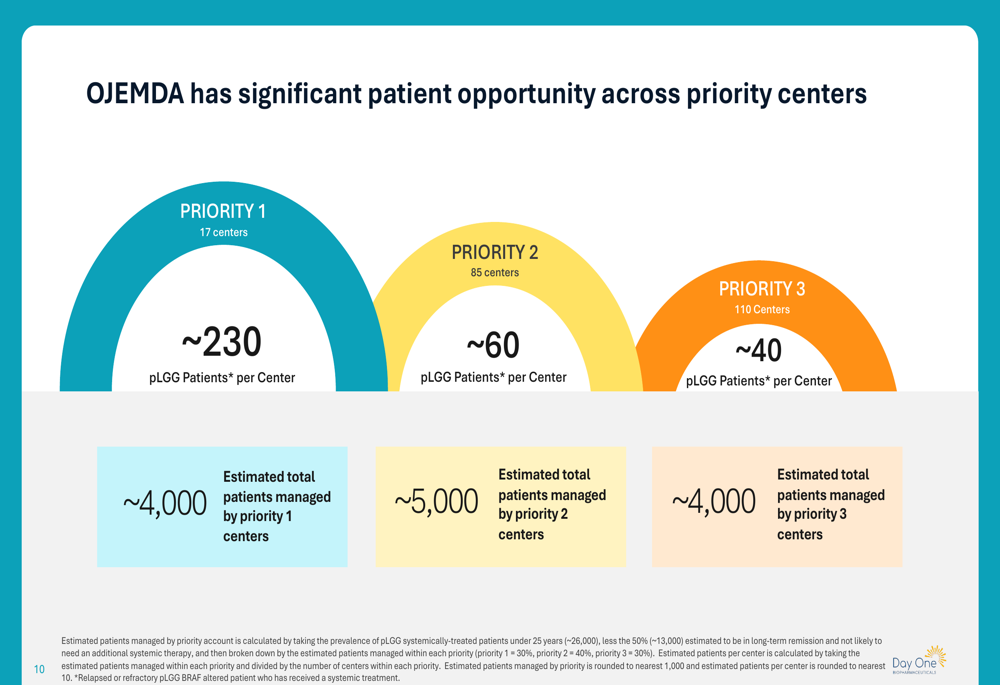

Day One identified significant market opportunity across different types of treatment centers:

The company has segmented its target market into three priority tiers, with approximately 13,000 potential pLGG patients managed across 212 centers. This structured approach allows for focused commercial efforts to maximize market penetration.

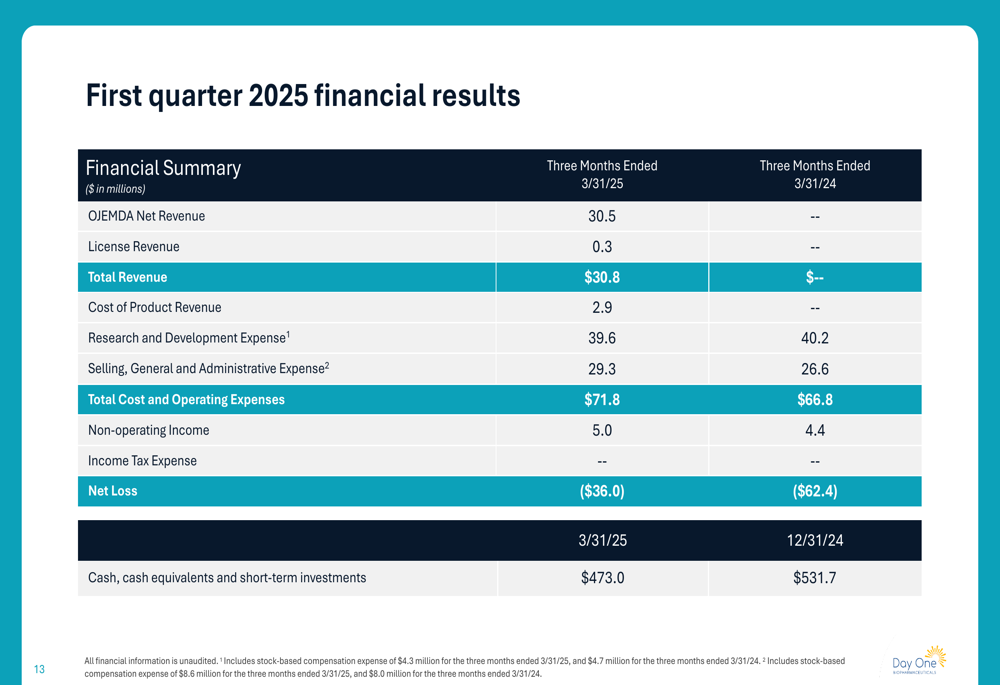

Detailed Financial Analysis

Day One’s financial results for Q1 2025 showed improvement in several key metrics compared to the same period last year, particularly in net loss reduction.

The following table provides a comprehensive overview of the company’s financial performance:

Total (EPA:TTEF) revenue for Q1 2025 reached $30.8 million, including $30.5 million from OJEMDA net product revenue and $0.3 million from license revenue. The company reported a net loss of $36.0 million, a significant improvement from the $62.4 million loss in Q1 2024.

Research and development expenses decreased slightly to $39.6 million from $40.2 million in the prior-year period. Meanwhile, selling, general, and administrative expenses increased to $29.3 million from $26.6 million, reflecting continued investment in commercial infrastructure.

The company’s cash position stood at $473.0 million as of March 31, 2025, down from $531.7 million at the end of December 2024. This cash burn reflects ongoing investments in commercial activities and pipeline development.

Strategic Initiatives & Outlook

Day One outlined several strategic priorities to drive OJEMDA revenue growth in 2025:

1. Increasing prescribing depth with current prescribers

2. Encouraging non-user healthcare providers to try OJEMDA for their next relapsed/refractory pLGG patient

3. Establishing OJEMDA as the standard of care in second-line relapsed or refractory BRAF-altered pLGG

4. Supporting prescribers and patients to optimize treatment duration

The company’s management, led by CEO Jeremy Bender, expressed confidence in executing these priorities while maintaining financial discipline. The strong cash position provides runway to continue commercial expansion and pipeline advancement without immediate need for additional financing.

Despite the positive narrative from management, investors appear cautious, as reflected in the stock’s recent performance. The company will need to demonstrate accelerating growth in coming quarters to shift market sentiment and drive stock price recovery from current levels near 52-week lows.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.