One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

Dermapharm Holding SE (ETR:DMP) presented its first-half 2025 financial results on August 26, highlighting a mixed performance with declining revenue but improving profitability in the second quarter. The German pharmaceutical company, currently trading at €33.75, emphasized its strategic focus on high-margin branded pharmaceuticals and ongoing restructuring efforts in its parallel import business.

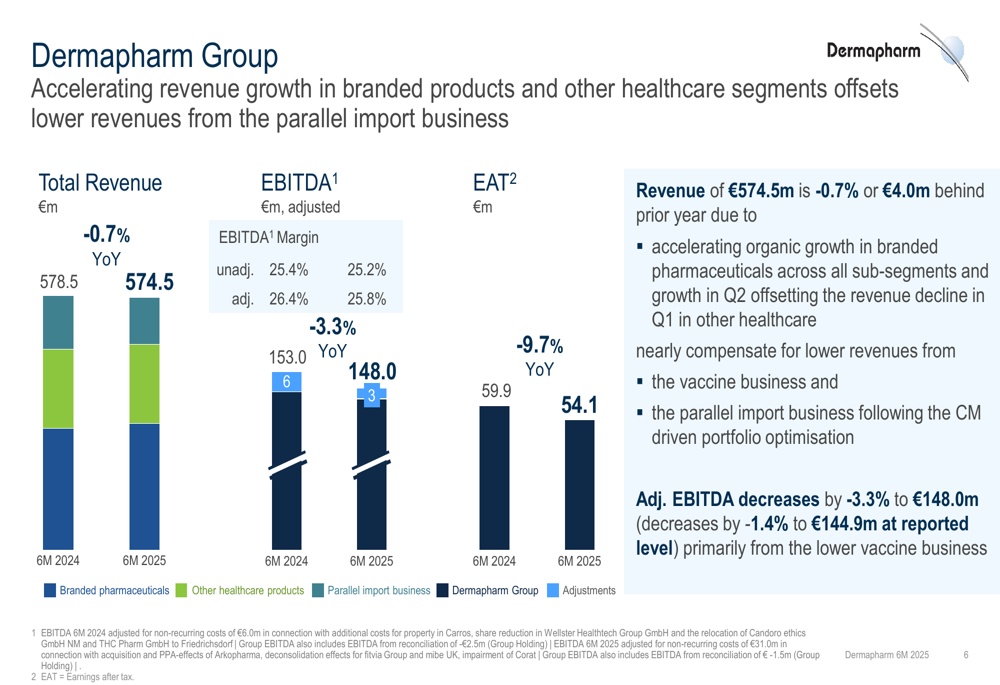

The company’s presentation revealed that while total H1 2025 revenue declined slightly by 0.7% year-over-year to €574.5 million, Q2 showed signs of operational improvement with adjusted EBITDA growing 3.7% despite a 2.8% revenue decrease in the quarter.

Quarterly Performance Highlights

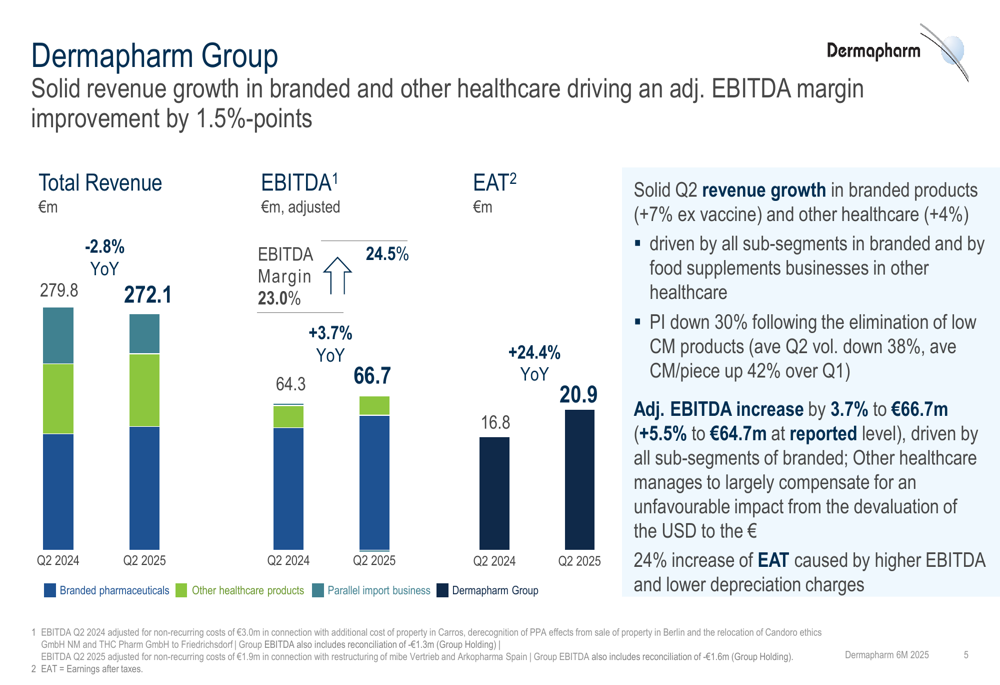

Dermapharm’s Q2 2025 results demonstrated the company’s ability to enhance profitability despite revenue headwinds. While revenue declined 2.8% to €272.1 million, adjusted EBITDA increased 3.7% to €66.7 million, resulting in an improved margin of 24.5%. Most notably, earnings after tax jumped 24.4% to €20.9 million.

As shown in the following chart of Q2 financial performance:

The company attributed this improvement to strong organic growth in branded products (+7% excluding vaccine business) and other healthcare segments (+4%). These gains helped offset significant declines in the parallel import business, which saw a 30% revenue drop following the elimination of low-contribution margin products.

For the first half of 2025, Dermapharm reported:

The slight revenue decline of 0.7% to €574.5 million was primarily due to lower vaccine business revenues and the restructuring of the parallel import business. However, the company noted accelerating organic growth in branded pharmaceuticals across all sub-segments, which nearly compensated for these declines.

Segment Analysis

Dermapharm’s three main business segments showed divergent performance in H1 2025:

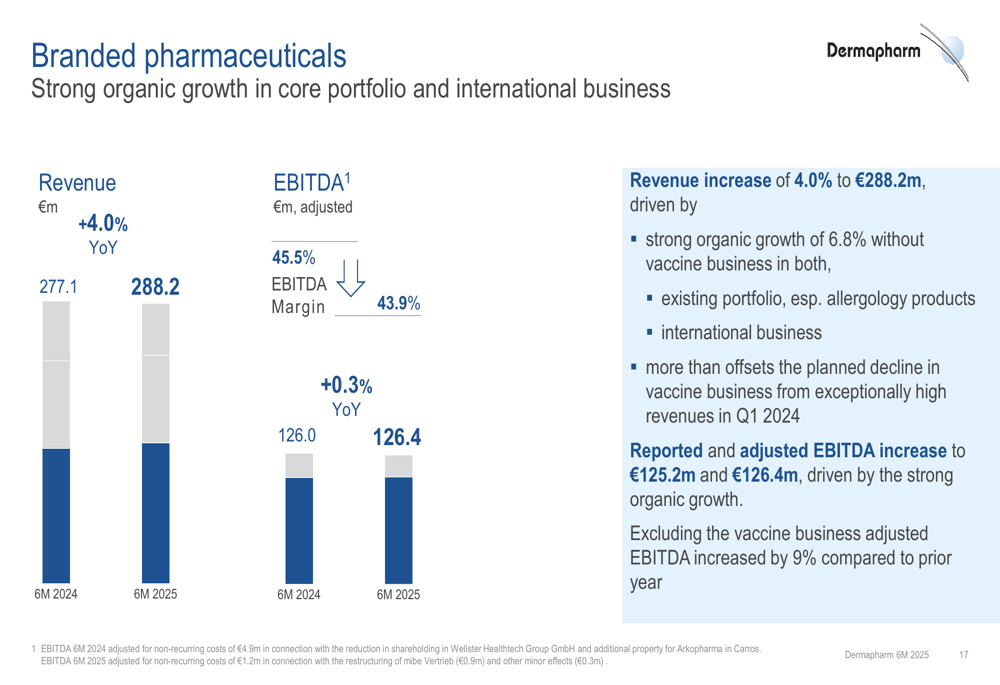

The Branded Pharmaceuticals segment, the company’s largest and most profitable division, delivered solid growth with revenue increasing 4.0% to €288.2 million and adjusted EBITDA rising slightly by 0.3% to €126.4 million. Excluding the vaccine business, which saw exceptionally high revenues in Q1 2024, adjusted EBITDA increased by an impressive 9%.

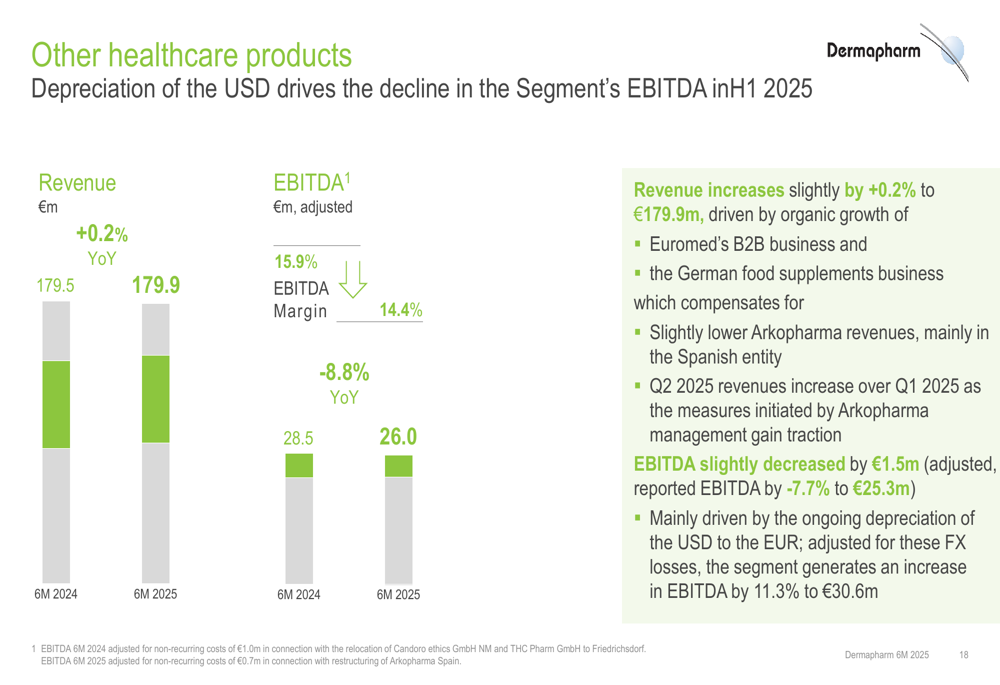

The Other Healthcare Products segment showed stable revenue at €179.9 million (+0.2%) but experienced an 8.8% decline in adjusted EBITDA to €26.0 million. This decrease was primarily attributed to currency effects from the depreciation of the USD against the EUR. Adjusting for these FX losses, the segment would have shown an 11.3% EBITDA increase.

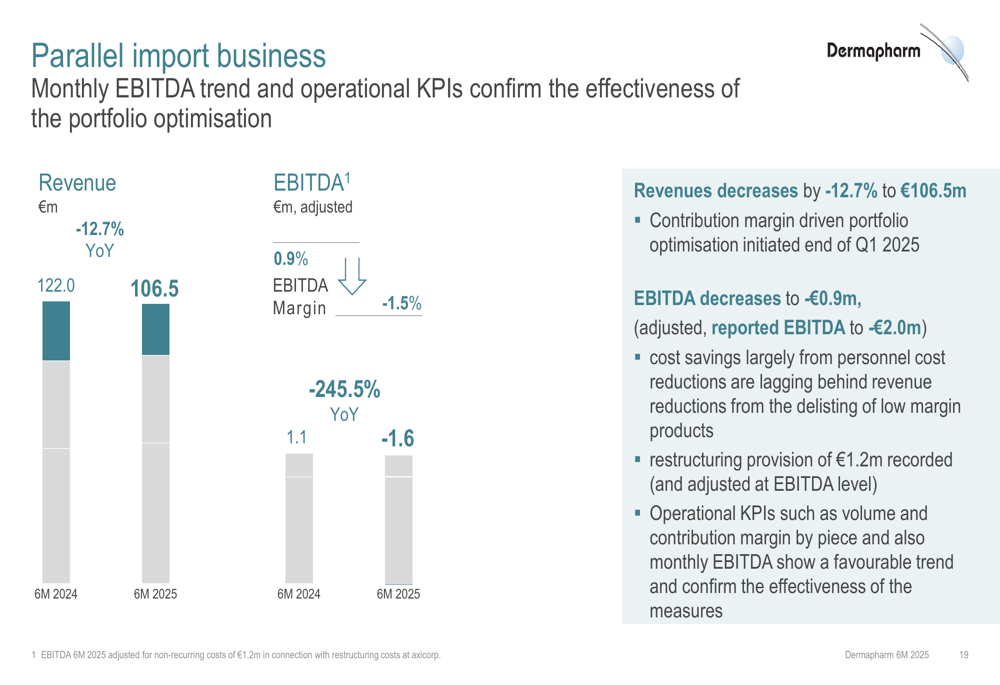

The Parallel Import Business continued to face challenges with revenue declining 12.7% to €106.5 million and adjusted EBITDA falling to -€1.6 million. However, management emphasized that operational KPIs such as volume, contribution margin per piece, and monthly EBITDA trends confirm the effectiveness of their portfolio optimization strategy.

Financial Health & Cash Flow

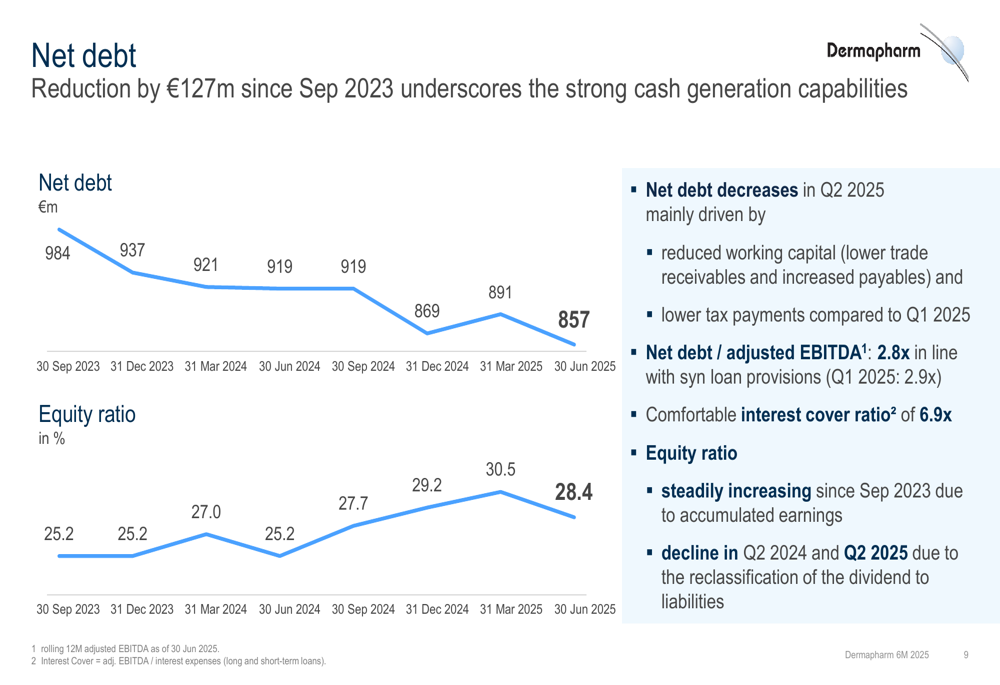

Dermapharm made significant progress in strengthening its financial position during the first half of 2025. Net debt decreased to €857 million, representing a reduction of €127 million since September 2023, while the equity ratio improved to 28.4%.

The following chart illustrates this positive trend:

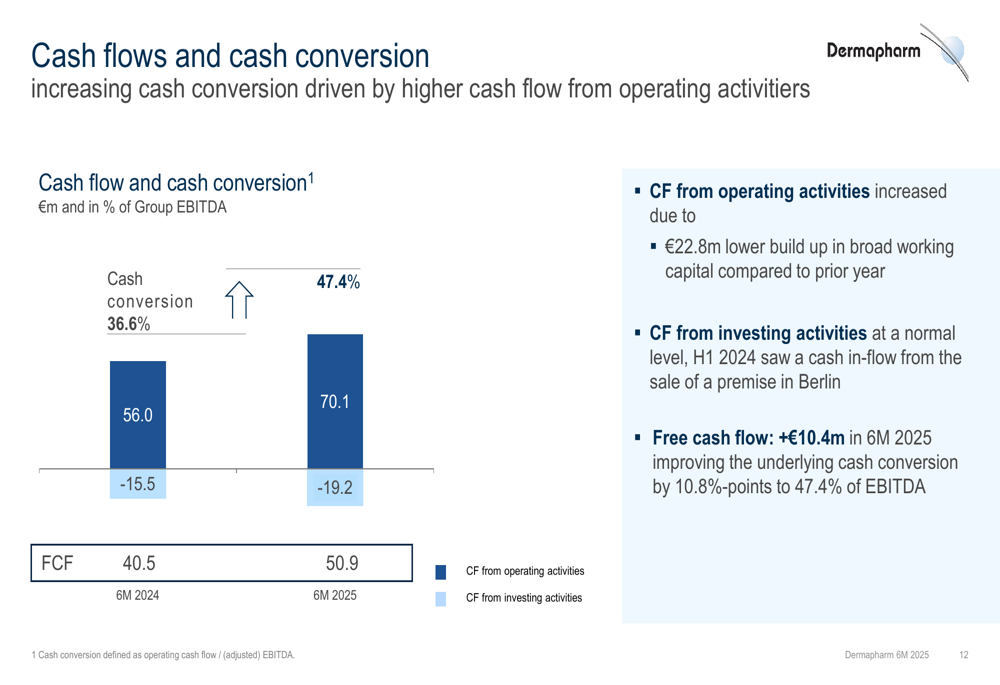

Cash flow metrics showed notable improvement, with cash conversion increasing from 36.6% in H1 2024 to 47.4% in H1 2025. Free cash flow rose by €10.4 million to €50.9 million, driven by a €22.8 million lower build-up in working capital compared to the prior year.

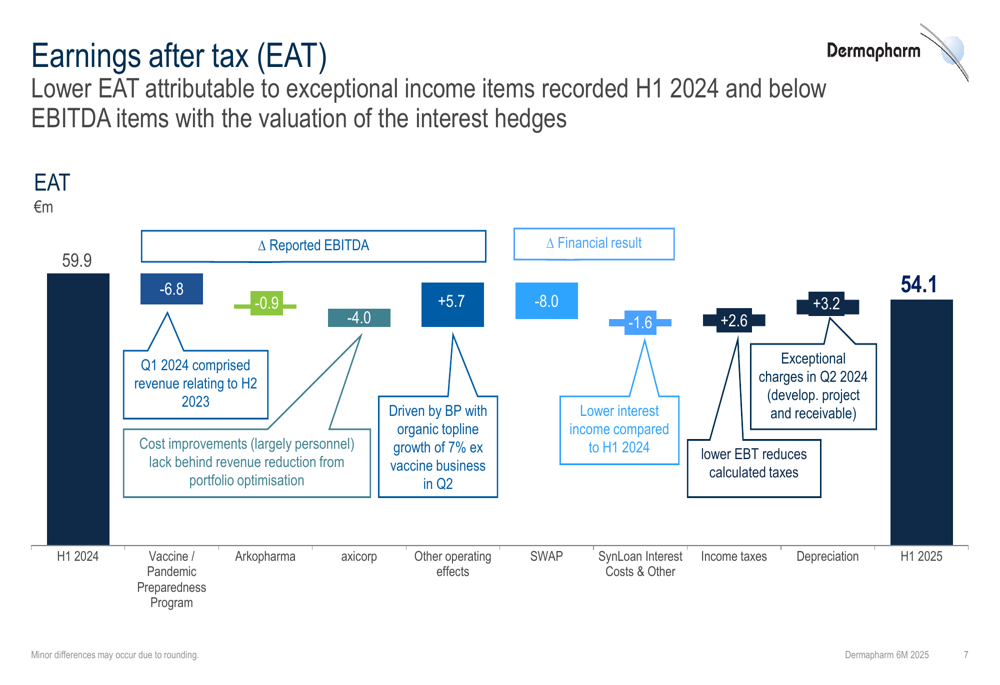

The company’s earnings after tax bridge analysis reveals that the 9.7% decline in H1 EAT to €54.1 million was primarily attributable to exceptional income items recorded in H1 2024 and the valuation of interest hedges:

Forward-Looking Statements

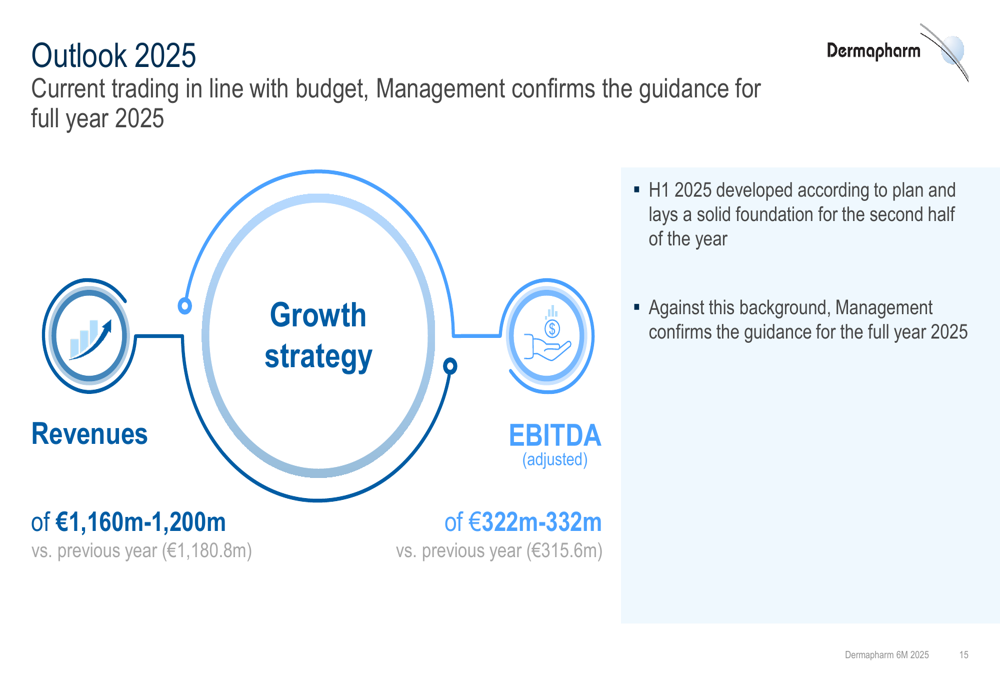

Dermapharm confirmed its full-year 2025 guidance, expressing confidence that current trading is in line with budget expectations. The company projects:

For the full year 2025, Dermapharm expects revenue between €1,160-1,200 million, compared to €1,180.8 million in the previous year. Adjusted EBITDA is forecast to reach €322-332 million, representing potential growth from the €315.6 million achieved in the prior year.

Management stated that H1 2025 developed according to plan and provides a solid foundation for the second half of the year. The company’s growth strategy continues to focus on expanding its high-margin branded pharmaceuticals segment while completing the restructuring of its parallel import business.

With its improving cash flow, reduced debt levels, and strategic focus on higher-margin products, Dermapharm appears positioned to deliver on its full-year targets despite the mixed performance in the first half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.