S&P 500 falls as ongoing government shutdown, trade jitters weigh

Introduction & Market Context

Deutsche Konsum REIT-AG (XETRA:DKG) presented its H1 2024/2025 financial results on May 15, 2025, revealing significant financial challenges as the company continues its extensive restructuring efforts. The retail-focused German REIT reported sharp declines in key performance metrics while making progress on debt reduction initiatives.

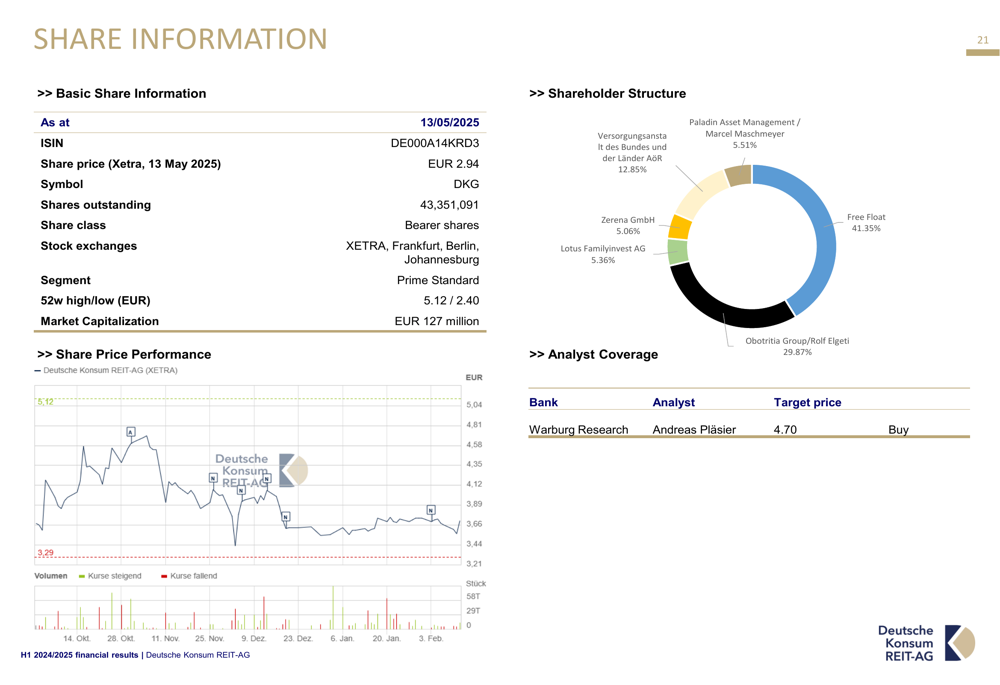

The company’s stock closed at €2.97 on May 14, 2025, up 1.02% for the day, but remains significantly below its 52-week high of €5.12 and closer to its 52-week low of €2.40, reflecting ongoing investor concerns about the company’s financial health and restructuring progress.

Financial Performance Highlights

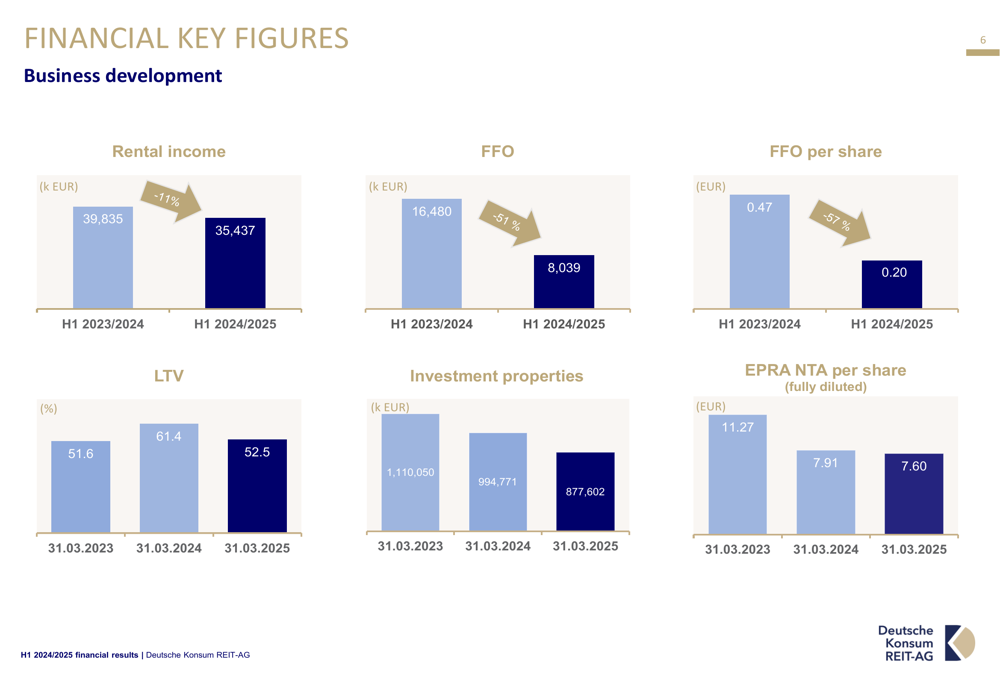

Deutsche Konsum reported substantial declines across major financial metrics for H1 2024/2025 compared to the same period last year. Rental income decreased by 11% to €35.4 million, while Funds From Operations (FFO) plummeted by 51.2% to €8.0 million. The company’s total period income saw an even more dramatic drop of 90.6% to just €1.03 million.

As shown in the following chart of key financial figures, these declines represent a continuation of negative trends across multiple metrics:

The sharp reduction in FFO per share, which fell from €0.47 to €0.20 (-57%), reflects both operational challenges and the dilutive effect of recent capital measures. Earnings per share (undiluted) similarly collapsed by 91.8% to just €0.03.

Restructuring Plan and Debt Reduction

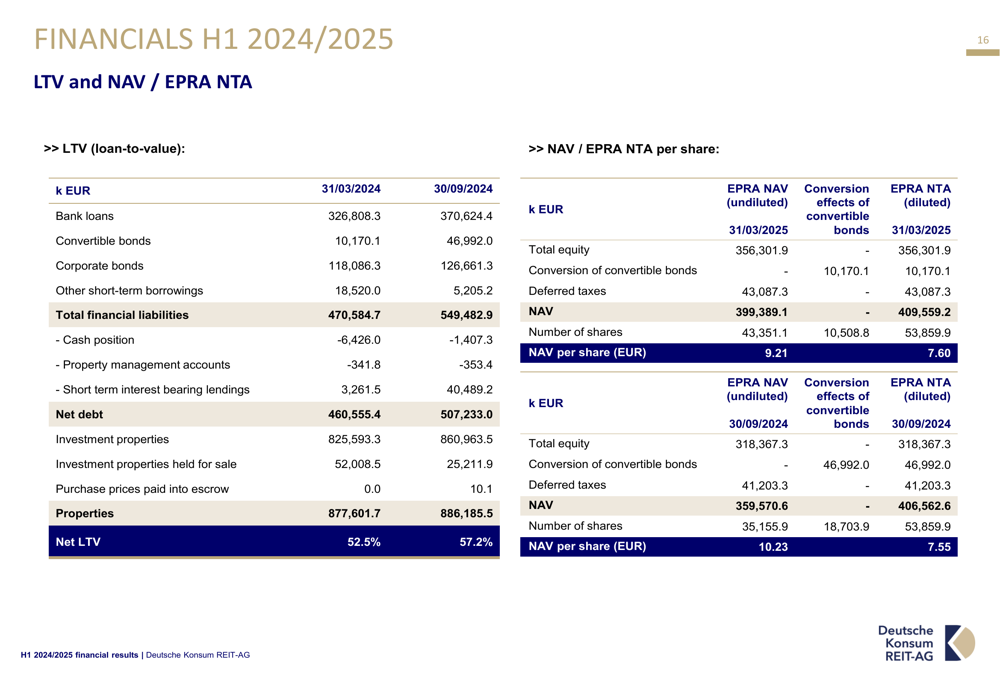

Despite the concerning operational performance, Deutsche Konsum has made significant progress in strengthening its balance sheet. The company reduced its debt by approximately €79 million (-14%), bringing total financial debt down to €470.6 million. This reduction was achieved through various measures, including the conversion of €30 million in debt, with an additional €7 million conversion in progress, repayment of €10 million in registered bonds, and other repayments totaling €35.9 million.

The company’s restructuring efforts are substantial, as detailed in their current plan:

A formal restructuring opinion is being prepared by FTI-Andersch, with completion expected by the end of August 2025. The company has secured standstill agreements with various lenders until the end of May 2025 and is negotiating extensions until August. Additionally, bridge financing of up to €14 million has been secured at 5.5% interest.

Most notably, Deutsche Konsum indicated that property disposals of €350-450 million might be necessary during the restructuring period, which is expected to last until the end of 2027. This represents a significant portion of the company’s current property portfolio valued at €877.6 million.

The debt reduction efforts have helped improve the company’s loan-to-value (LTV) ratio, which decreased to 52.5% from 61.4% a year earlier:

However, the interest coverage ratio (ICR) has deteriorated significantly, falling from 3.3x to just 1.2x, highlighting the pressure of debt servicing costs on the company’s reduced income.

Property Portfolio and Tenant Structure

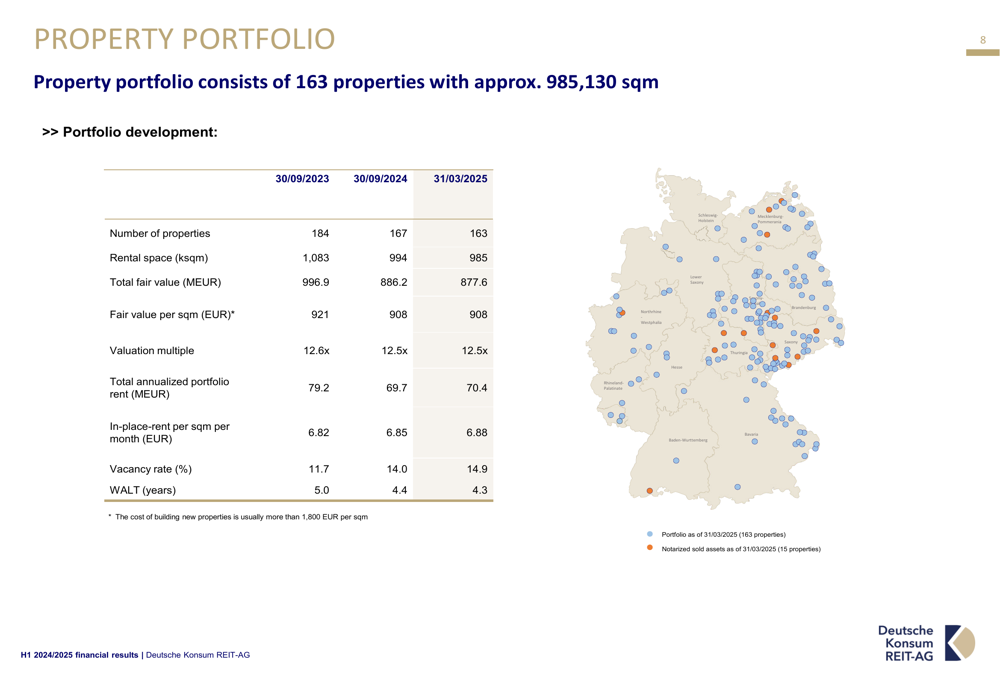

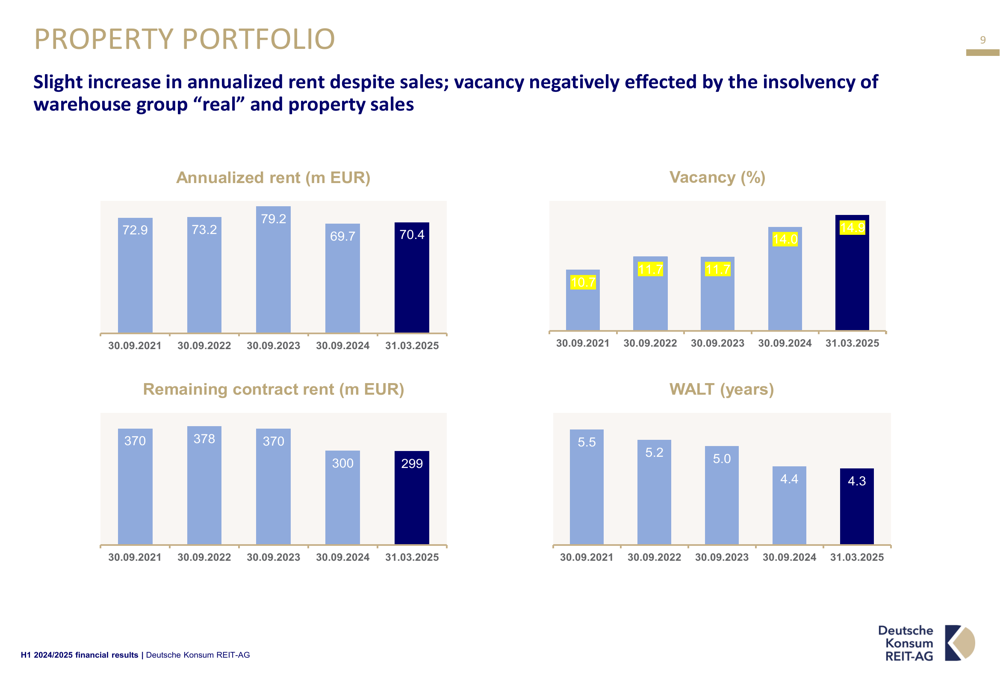

Deutsche Konsum’s property portfolio consisted of 163 properties with approximately 985,130 square meters as of March 31, 2025, a reduction from 167 properties at the end of September 2024. The portfolio’s total fair value stood at €877.6 million, down from €886.2 million six months earlier.

The following overview provides key metrics on the company’s property portfolio:

Portfolio performance metrics show concerning trends, with the vacancy rate increasing to 14.9% from 14.0% six months earlier, and the weighted average lease term (WALT) decreasing to 4.3 years from 4.4 years:

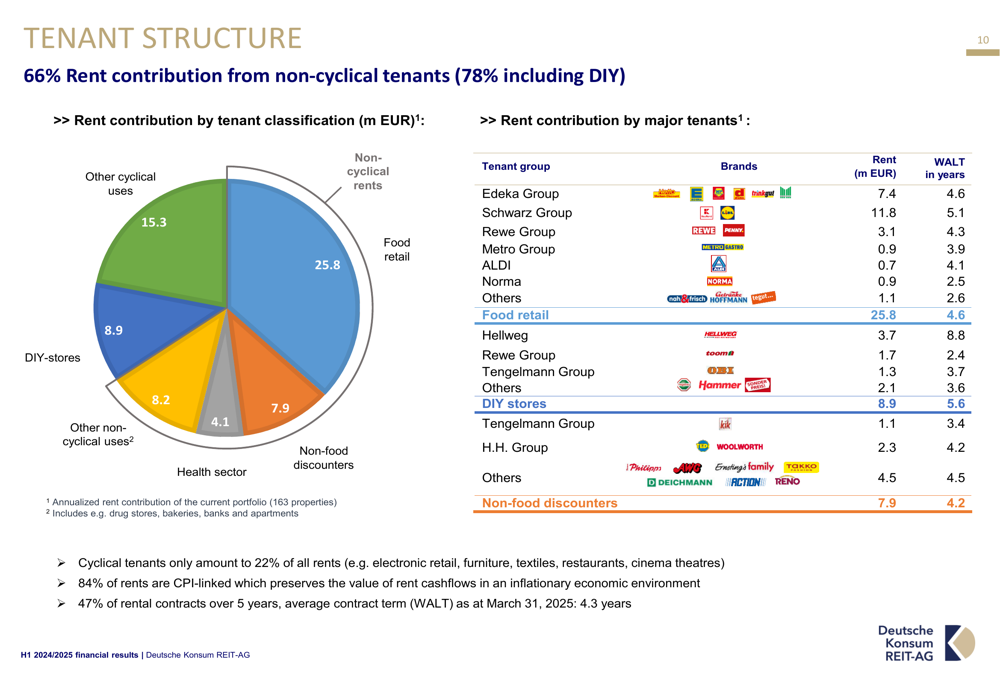

Despite these challenges, Deutsche Konsum maintains a relatively stable tenant structure, with 66% of rent contribution coming from non-cyclical tenants, rising to 78% when including DIY stores. Major tenants include the Schwarz Group (€11.8 million annual rent), Edeka Group (€7.4 million), and Rewe Group (€3.1 million).

The following chart breaks down the company’s tenant structure by rent contribution:

The company highlighted that 84% of its rents are CPI-linked, providing some inflation protection, and 47% of rental contracts extend beyond five years, offering a degree of income stability despite the declining WALT.

Forward-Looking Statements

Deutsche Konsum declined to provide specific guidance for FY 2024/2025, citing ongoing restructuring uncertainties, but indicated that rental income is expected to be between €66-71 million. This cautious approach aligns with the significant challenges facing the company.

The company’s share information and analyst coverage suggest some potential for recovery, with Warburg Research maintaining a "Buy" rating and a target price of €4.70, substantially above the current trading price:

However, investors should consider the substantial risks outlined in the presentation, including the need for extensive property disposals, ongoing refinancing challenges, and deteriorating operational metrics. The success of the restructuring plan and the company’s ability to stabilize its operational performance will be critical factors for Deutsche Konsum’s future prospects.

With the restructuring opinion expected by August 2025 and significant property disposals planned through 2027, Deutsche Konsum faces a prolonged period of transformation that will likely continue to impact its financial results and stock performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.