United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

DigitalBridge Group Inc (NYSE:DBRG) released its Q2 2025 earnings presentation on August 7, 2025, highlighting continued growth in fee revenue and fee-related earnings despite challenges in distributable earnings. The company emphasized its strategic positioning in the rapidly expanding AI infrastructure market, where hyperscaler capital expenditure has increased by 50% year-over-year to $380 billion.

The digital infrastructure investor reported that markets recovered in Q2 as macroeconomic concerns abated and AI demand surged, creating favorable conditions for its portfolio of data center and digital power investments. This market environment has enabled DigitalBridge to advance its strategy of building "AI factories" at unprecedented scale.

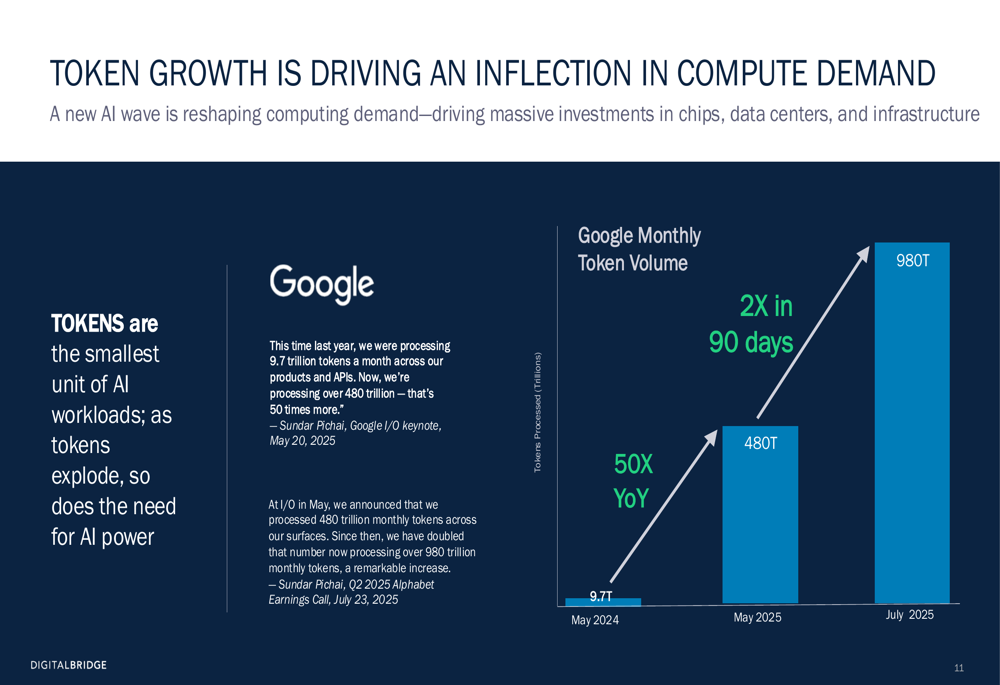

As shown in the following slide, Google (NASDAQ:GOOGL)’s token volume growth illustrates the explosive demand for compute resources that is driving DigitalBridge’s investment strategy:

Quarterly Performance Highlights

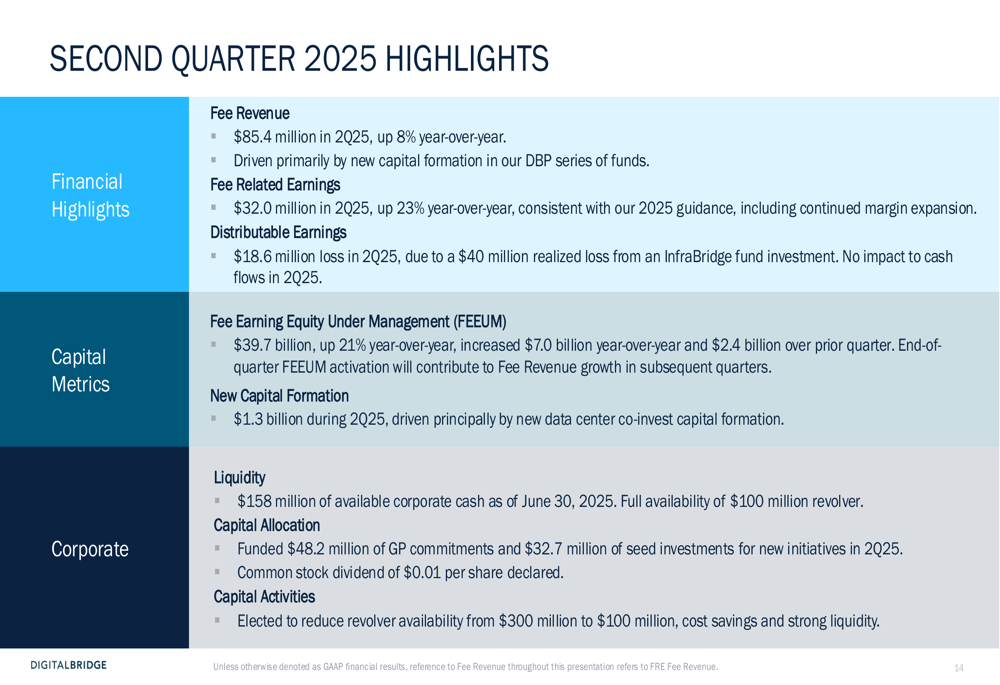

DigitalBridge reported GAAP net income attributable to common stockholders of $17 million, or $0.10 per share, for the second quarter of 2025. However, the company posted distributable earnings of negative $18.6 million, or $0.10 loss per share, representing a significant shift from the $19.6 million in distributable earnings reported in the same period last year.

Despite this challenge, the company achieved solid growth in its core fee business. Fee revenue increased 8% year-over-year to $85.4 million, while fee-related earnings (FRE) grew 23% to $32.0 million, with FRE margin improving to 37%. The company also reported $1.3 billion in new capital formation during Q2 and maintained $158 million in corporate cash.

The comprehensive financial results are detailed in the following slide:

CEO Marc Ganzi highlighted the company’s performance, stating: "DigitalBridge delivered a solid quarter of growth with fee-related earnings, leveraging AI-driven tailwinds and landmark investments including the Yondr acquisition and the Takanock power infrastructure platform."

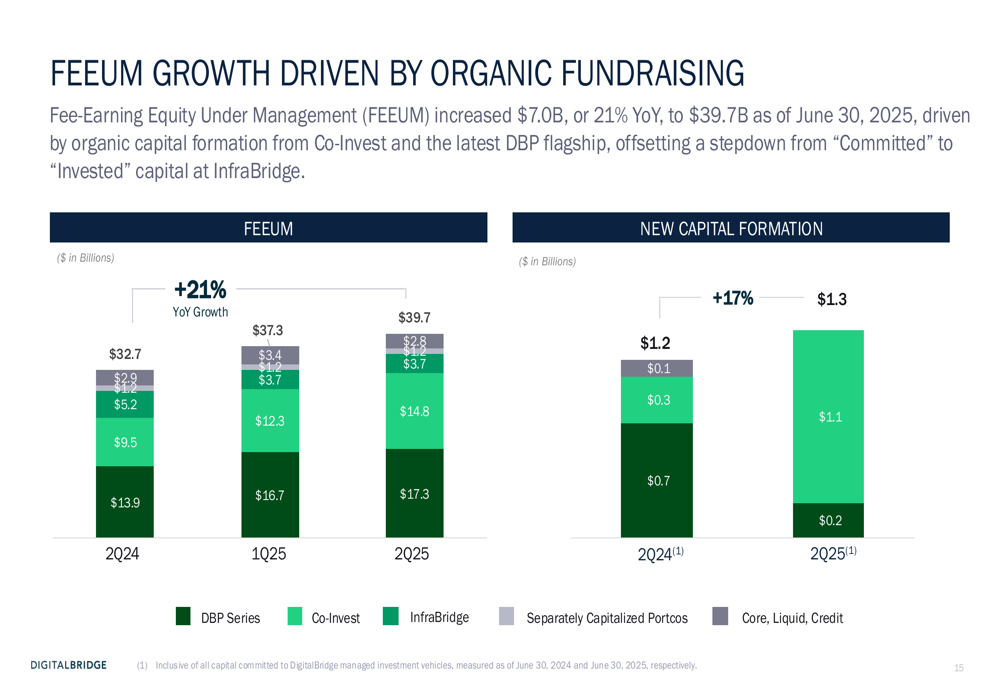

The company’s fee-earning equity under management (FEEUM) reached $39.7 billion, representing 21% growth year-over-year, as shown in the following chart:

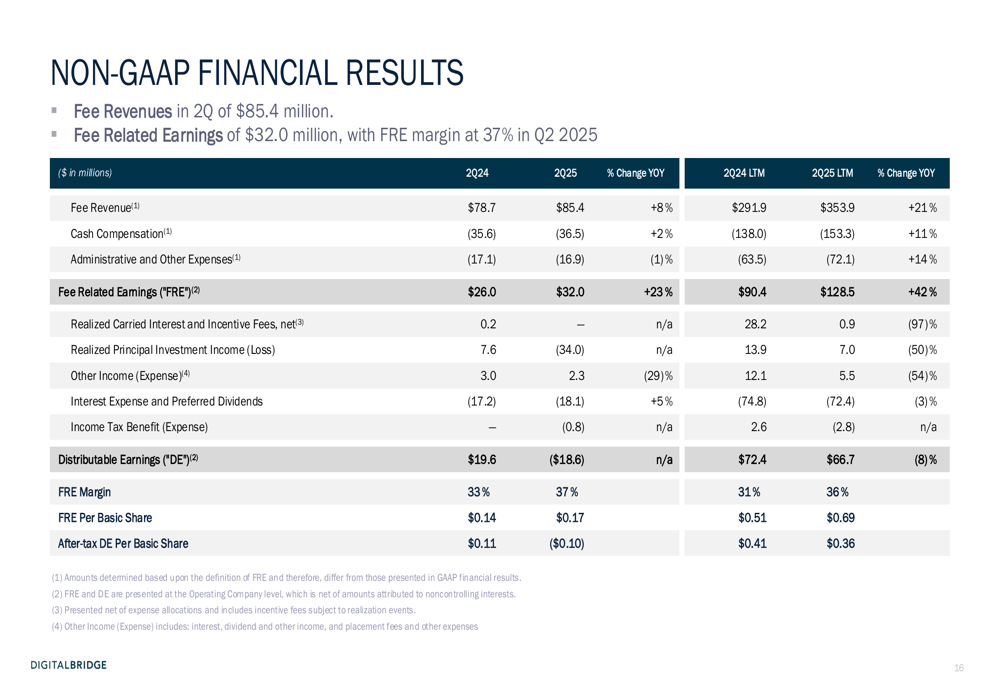

A closer examination of the non-GAAP financial results reveals the contrast between strong fee-related earnings growth and challenges in other areas:

Strategic Investments in AI Infrastructure

DigitalBridge has made significant strategic investments to capitalize on the growing demand for AI infrastructure. The company highlighted four key platforms in its presentation: Yondr, Takanock, Switch, and Vantage.

The following slide provides an overview of these investment platforms:

The acquisition of Yondr, a global hyperscale data center developer and operator with approximately 1GW of potential capacity, represents a major expansion of DigitalBridge’s AI infrastructure portfolio. Yondr strengthens the company’s global hyperscale presence with sites spanning from Toronto to Jakarta.

As illustrated in the following slide, DigitalBridge is positioning Yondr as its "next AI factory":

The company also highlighted the expansion of Switch’s borrowing base and revolving credit facilities to $10 billion, demonstrating the scale of capital being deployed to support AI infrastructure growth.

Power Infrastructure Focus

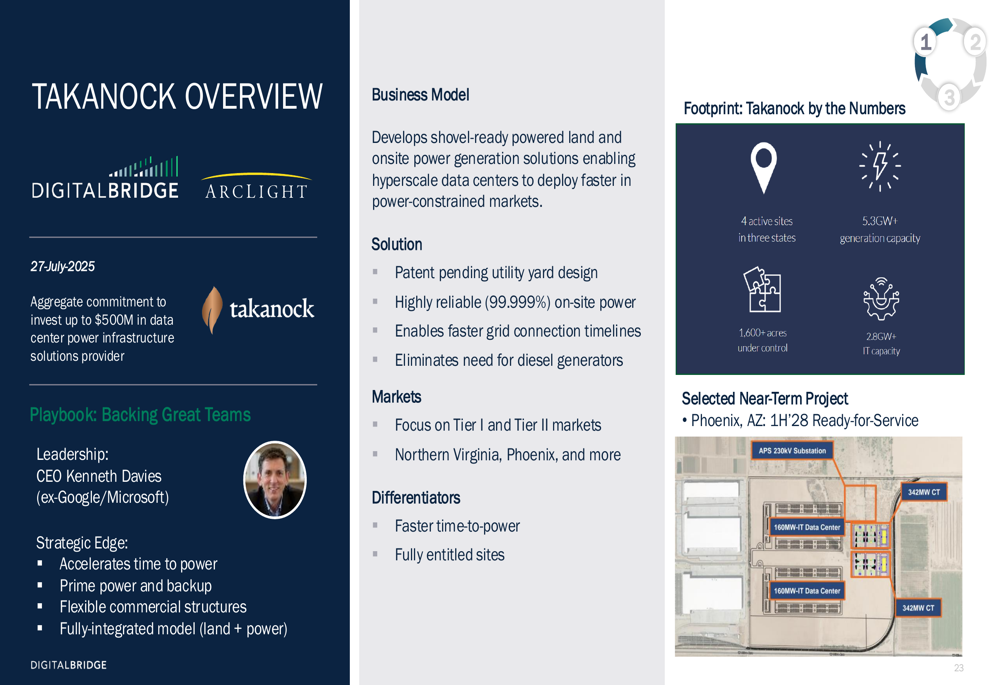

Recognizing that power is a critical constraint in AI infrastructure development, DigitalBridge has made strategic investments in data center power infrastructure. The company’s partnership with ArcLight to launch Takanock represents a significant commitment to addressing the growing power demands of AI data centers.

The following slide details this strategic partnership:

Takanock will focus on providing shovel-ready, powered land and onsite power generation for data centers, with an aggregate commitment to invest up to $500 million in data center power infrastructure solutions:

The importance of this power infrastructure strategy is underscored by projections that global data center electricity consumption will more than double from 416 TWh in 2024 to 946 TWh in 2030, driven largely by AI workloads.

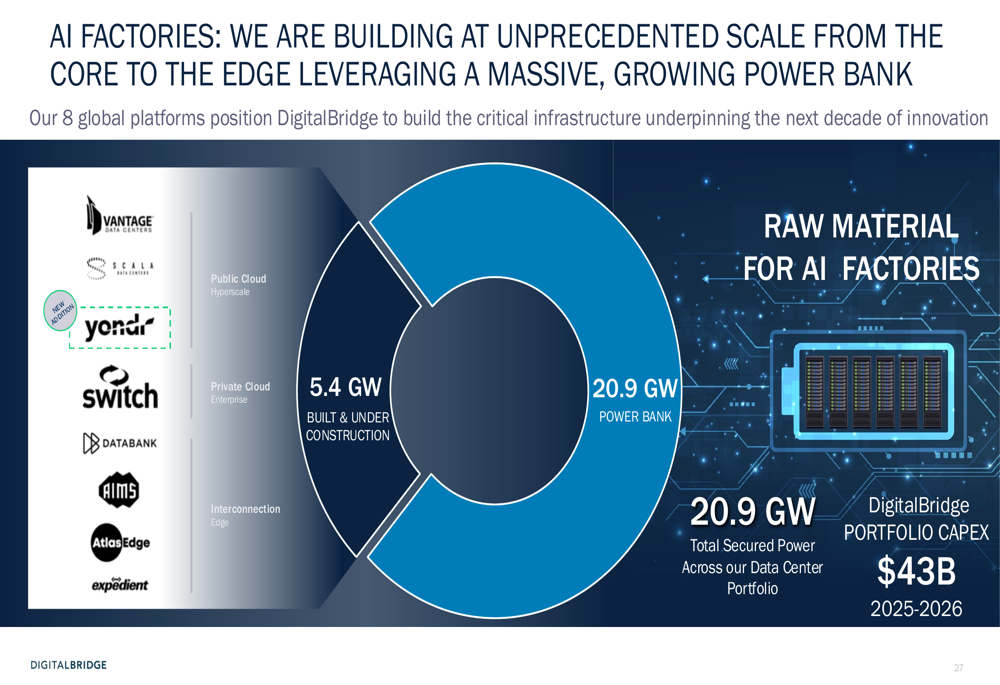

DigitalBridge’s combined portfolio now represents a significant power bank of 20.9GW with total capex of $43 billion, positioning the company to build critical infrastructure for the next decade of innovation:

Forward-Looking Statements

Looking ahead, DigitalBridge outlined its key priorities for the remainder of 2025, including delivering on financial metrics with fee-related earnings growth of 10-20% and reaching its target of $40 billion in FEEUM.

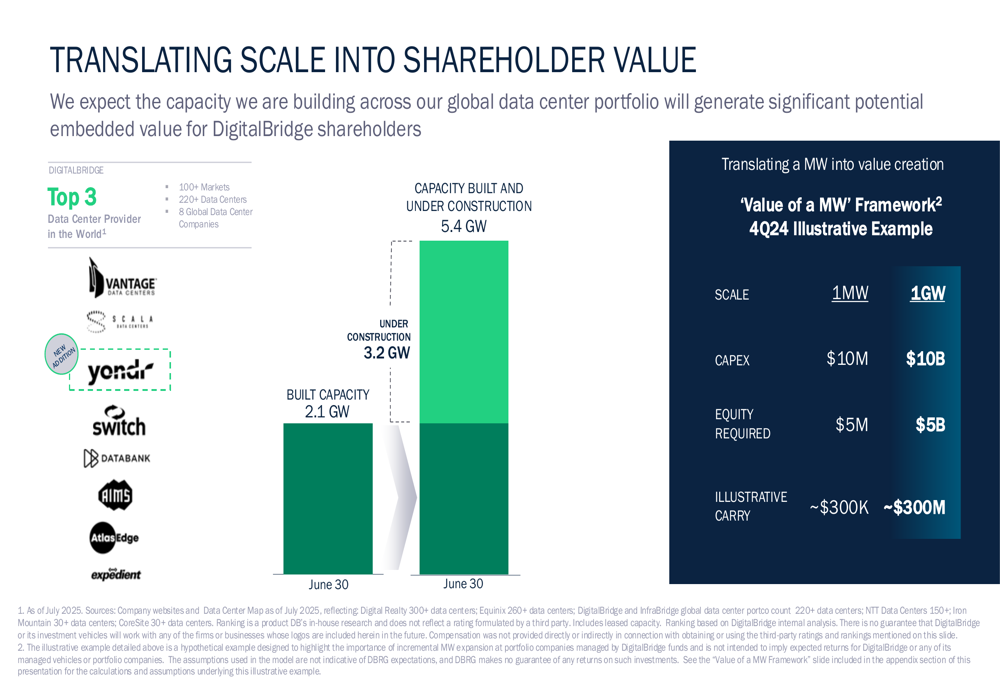

The company emphasized how its scale will translate into shareholder value, with a detailed analysis of the value creation potential from its growing megawatt capacity:

DigitalBridge faces both opportunities and challenges as it executes its strategy. While the company continues to benefit from strong demand for digital infrastructure and AI-related investments, the negative distributable earnings in Q2 2025 suggest potential headwinds in certain aspects of its business.

The company’s stock closed at $10.41 on August 6, 2025, down slightly by 0.19%, within its 52-week range of $6.41 to $17.33. This relatively stable performance indicates that investors are cautiously evaluating the company’s growth strategy against its current financial results.

As DigitalBridge continues to expand its digital infrastructure portfolio and capitalize on AI-driven demand, investors will be watching closely to see if the company can translate its strategic investments and fee revenue growth into improved distributable earnings in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.