Micron to exit server chips business in China after 2023 ban- Reuters

Introduction & Market Context

Dollarama Inc (TSX:DOL), Canada’s leading value retailer, presented its Q1 FY2026 results on June 11, 2025, highlighting continued growth across its Canadian operations and Latin American subsidiary, Dollarcity. The company’s stock closed at C$175.76 on June 10, near its 52-week high of C$179.71, reflecting strong investor confidence in its business model and expansion strategy.

The presentation showcased Dollarama’s position as the only national pure-play dollar store chain in Canada, with a footprint that places 85% of Canadian households within 10 kilometers of a store. The company continues to leverage its strong brand recognition, which it claims ranks as the second strongest brand in Canada, to drive consistent performance in an increasingly competitive retail environment.

Quarterly Performance Highlights

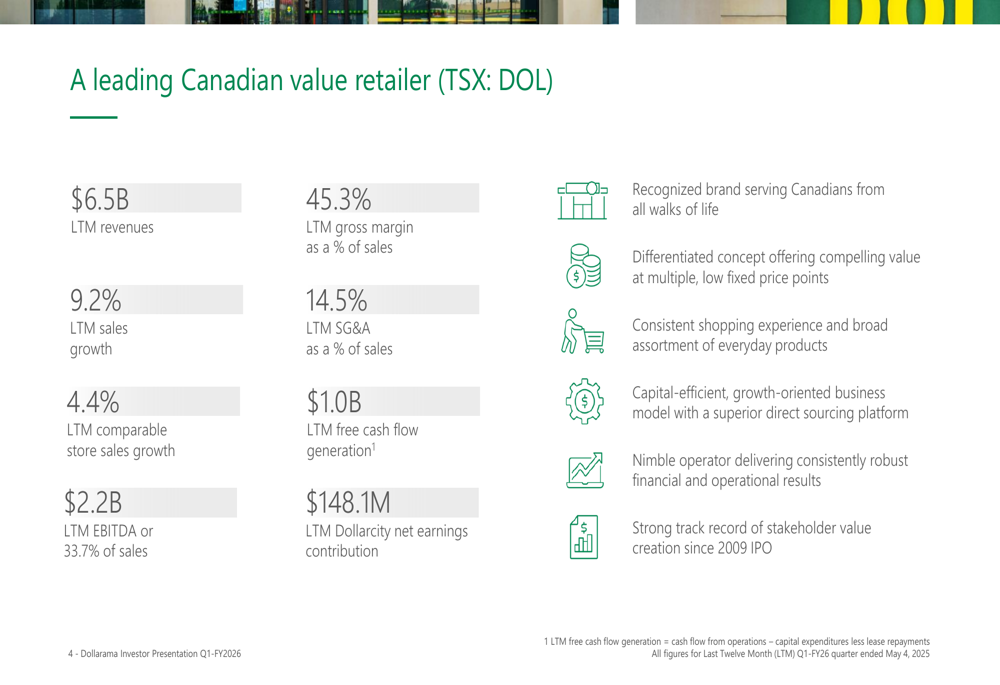

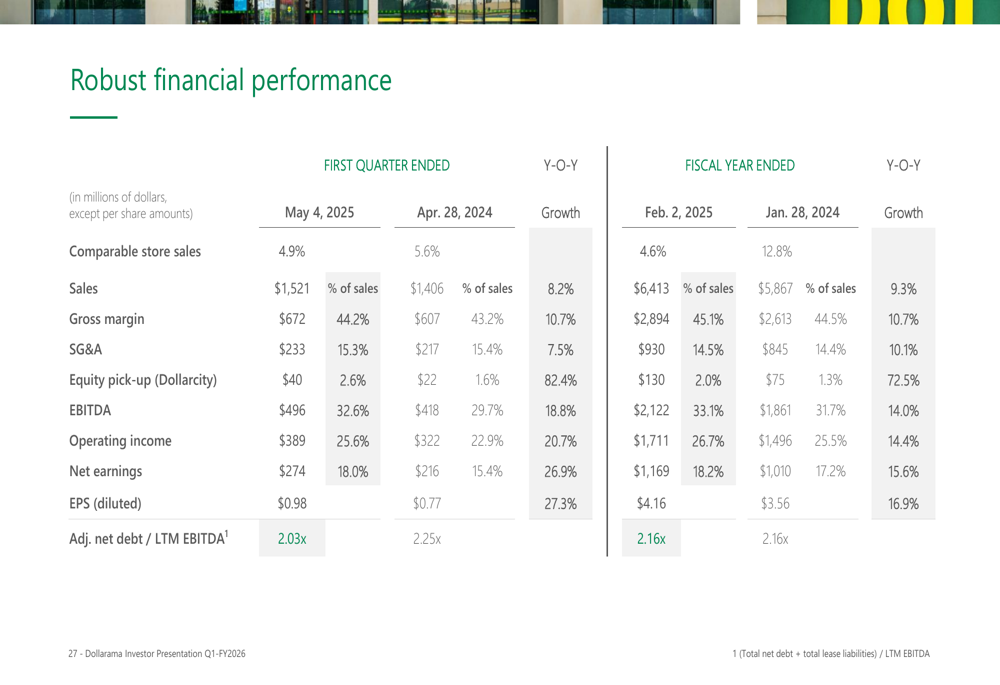

Dollarama reported an 8.2% increase in sales for Q1 FY2026, continuing its trajectory of steady growth. The company’s financial performance remains robust with last twelve months (LTM) metrics showing revenues of $6.5 billion, EBITDA of $2.2 billion (representing 33.7% of sales), and free cash flow generation of $1.0 billion.

As shown in the following chart of key financial highlights, Dollarama has maintained strong profitability metrics with a gross margin of 45.3% and SG&A expenses at 14.5% of sales:

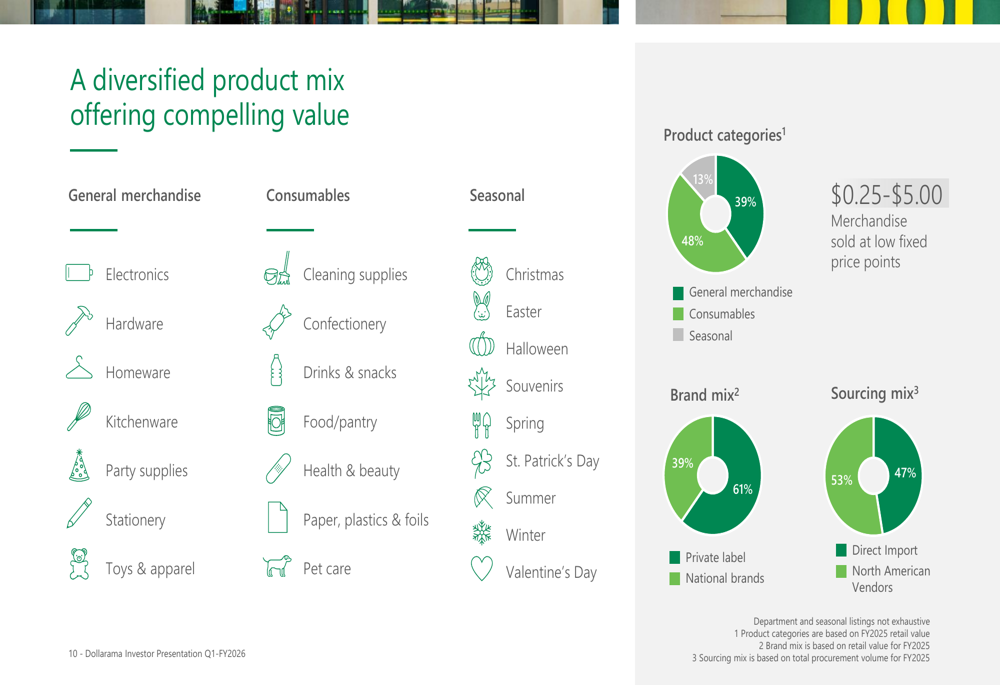

The company’s comparable store sales growth of 4.4% over the LTM period demonstrates Dollarama’s ability to drive traffic and increase basket size in existing locations. This performance is supported by a diversified product mix that balances general merchandise (39%), consumables (48%), and seasonal products (13%).

The product assortment strategy is clearly illustrated in this breakdown:

Strategic Growth Initiatives

Dollarama’s growth strategy focuses on three key pillars: expanding its Canadian store network, scaling up Dollarcity in Latin America, and pursuing strategic acquisitions.

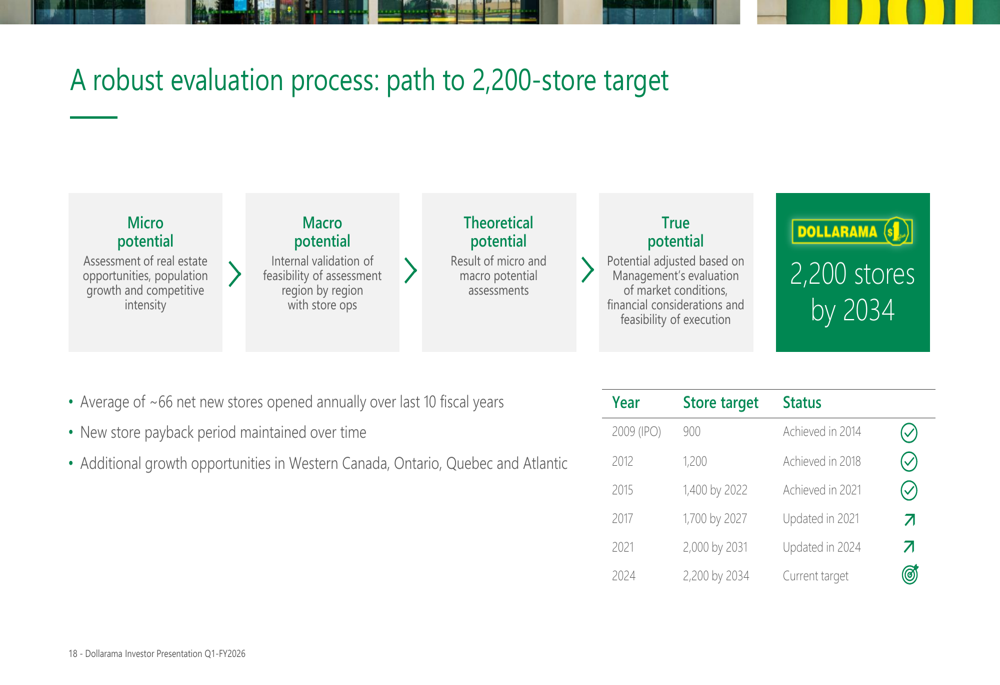

In Canada, Dollarama currently operates 1,638 stores across all 10 provinces and has set an ambitious target of 2,200 stores by 2034. The company’s store expansion model shows impressive efficiency, with new stores requiring an average investment of $920,000 and achieving payback within approximately two years.

The company’s methodical approach to store expansion is outlined in this evaluation process chart:

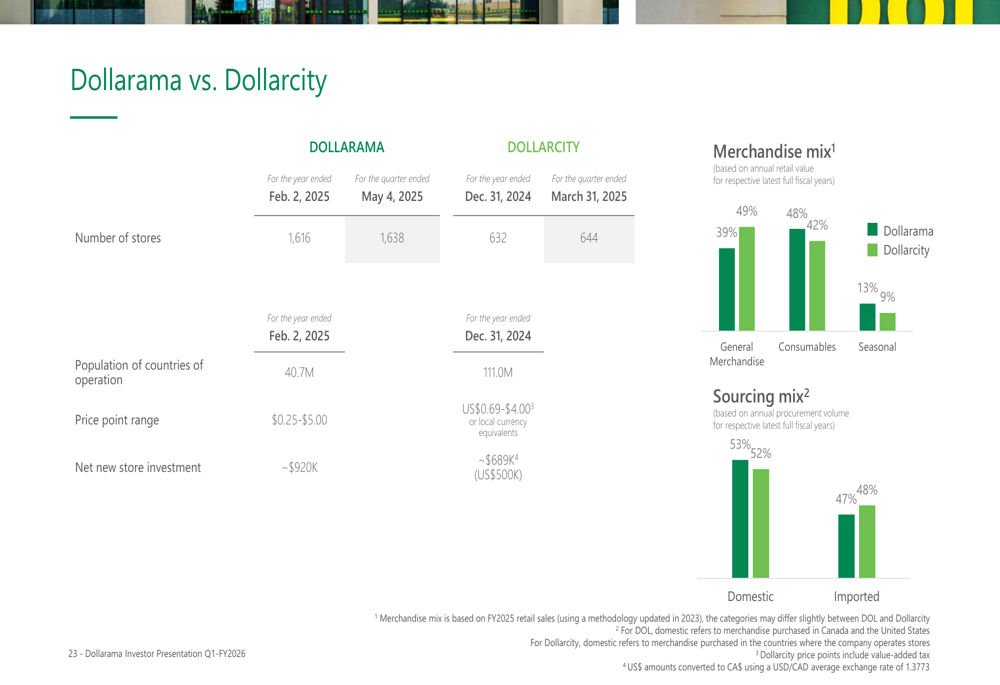

Internationally, Dollarama continues to scale up Dollarcity, in which it holds a 60.1% equity interest. Dollarcity currently operates 644 stores across Colombia (59% of stores), El Salvador (18%), Guatemala (13%), and Peru (10%). The presentation revealed plans to expand into Mexico in summer 2025, supporting Dollarcity’s target of 1,050 stores by 2031.

The following comparison highlights the similarities and differences between Dollarama and Dollarcity operations:

In a significant strategic move, Dollarama completed the acquisition of The Reject Shop in March 2025 for $259 million, representing an equity value of $6.68 per share. This acquisition marks Dollarama’s entry into a new market and demonstrates the company’s commitment to international expansion beyond its existing footprint.

Detailed Financial Analysis

Dollarama’s financial performance continues to impress, with the Q1 FY2026 results showing solid growth across key metrics. The company reported an 82.4% increase in equity pick-up from Dollarcity, which contributed $148.1 million to LTM earnings.

The company’s quarterly financial performance is detailed in the following chart:

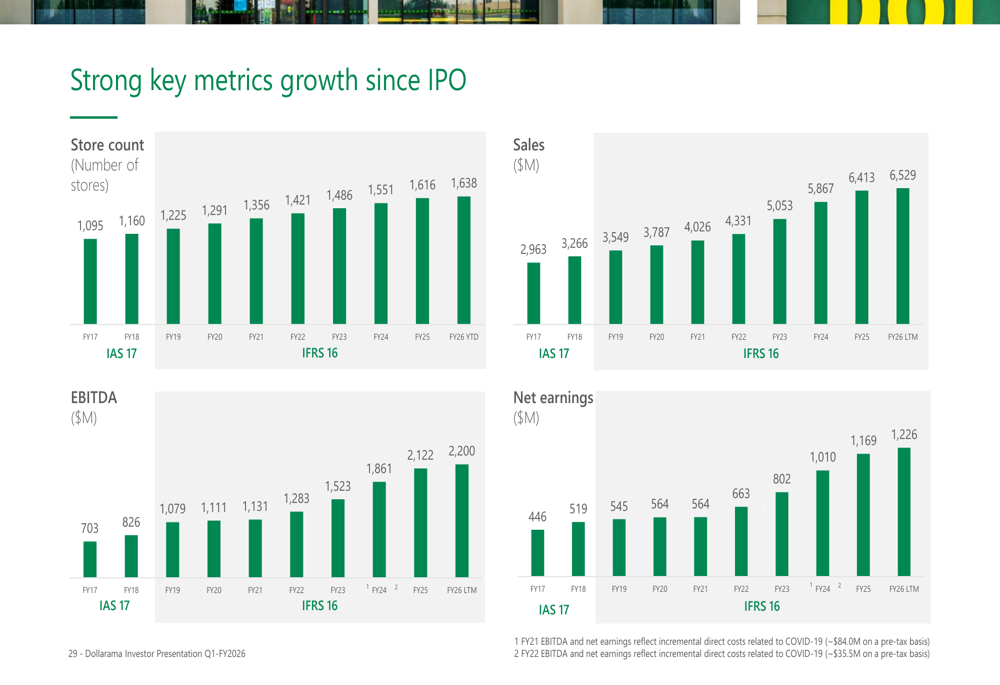

Since its IPO, Dollarama has demonstrated consistent growth in sales, EBITDA, and net earnings, as illustrated in this historical performance chart:

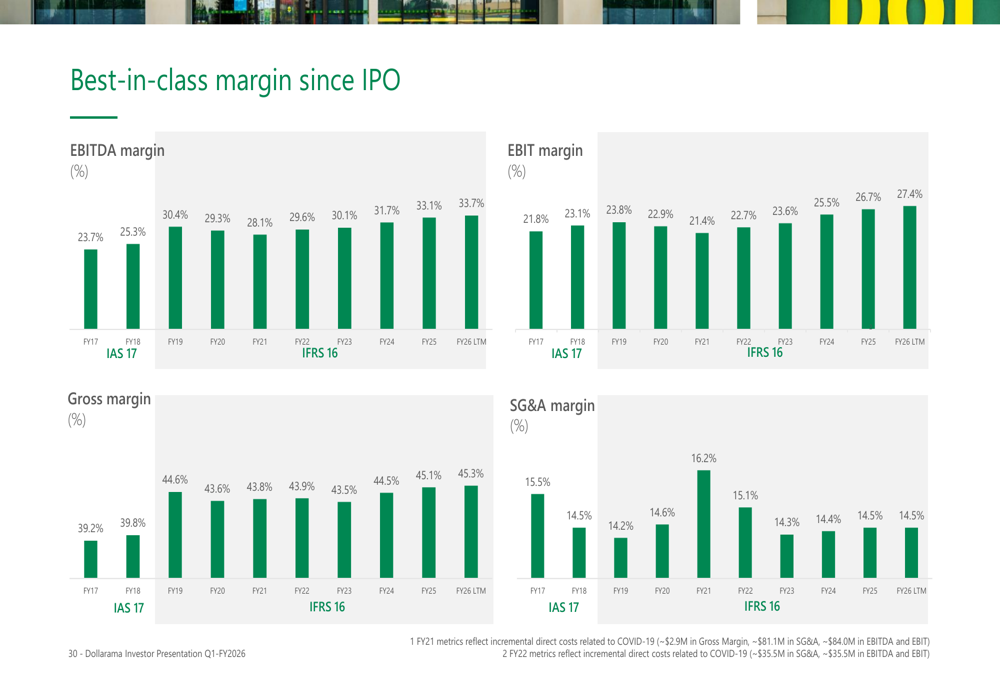

Dollarama has maintained strong profitability metrics over time, with stable gross margins and improving SG&A efficiency:

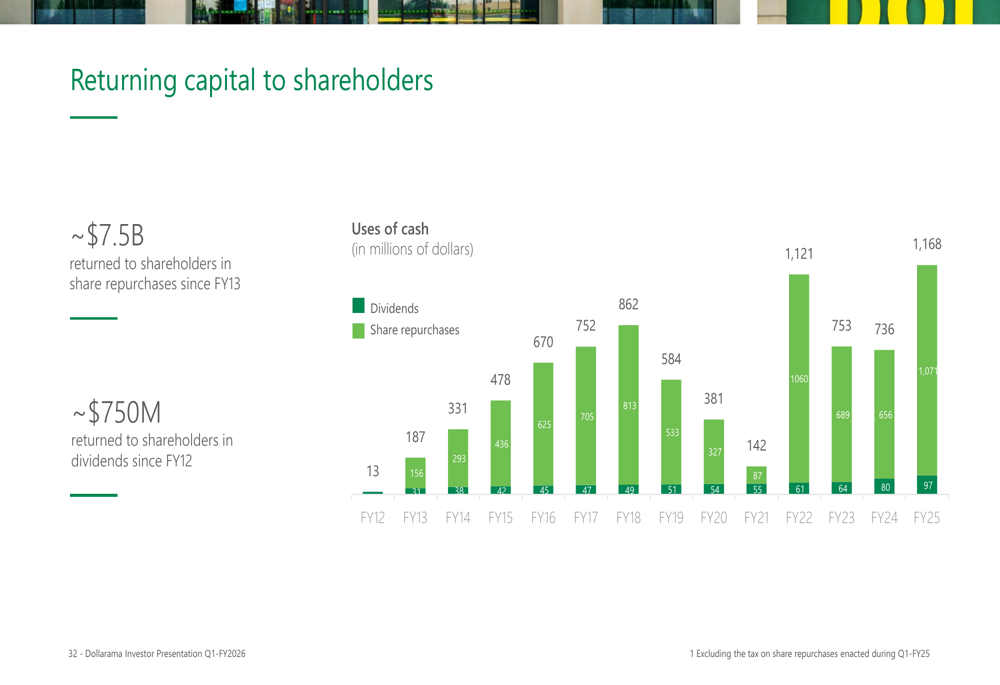

The company’s approach to capital allocation balances growth investments with returns to shareholders. Dollarama has returned $7.5 billion to shareholders through share repurchases, as shown in this chart:

Forward-Looking Statements

Looking ahead, Dollarama remains focused on its target of 2,200 stores in Canada by 2034, which would represent an addition of approximately 562 stores from its current footprint. The company plans to maintain its pace of opening about 66 new stores annually while preserving its disciplined approach to store economics.

For Dollarcity, the expansion into Mexico in summer 2025 represents a significant growth opportunity in a market with substantial potential. The target of 1,050 Dollarcity stores by 2031 would require more than 400 new store openings over the next six years.

The integration of The Reject Shop acquisition will be a key focus area in the coming quarters, as Dollarama applies its operational expertise and sourcing capabilities to enhance the performance of this new asset.

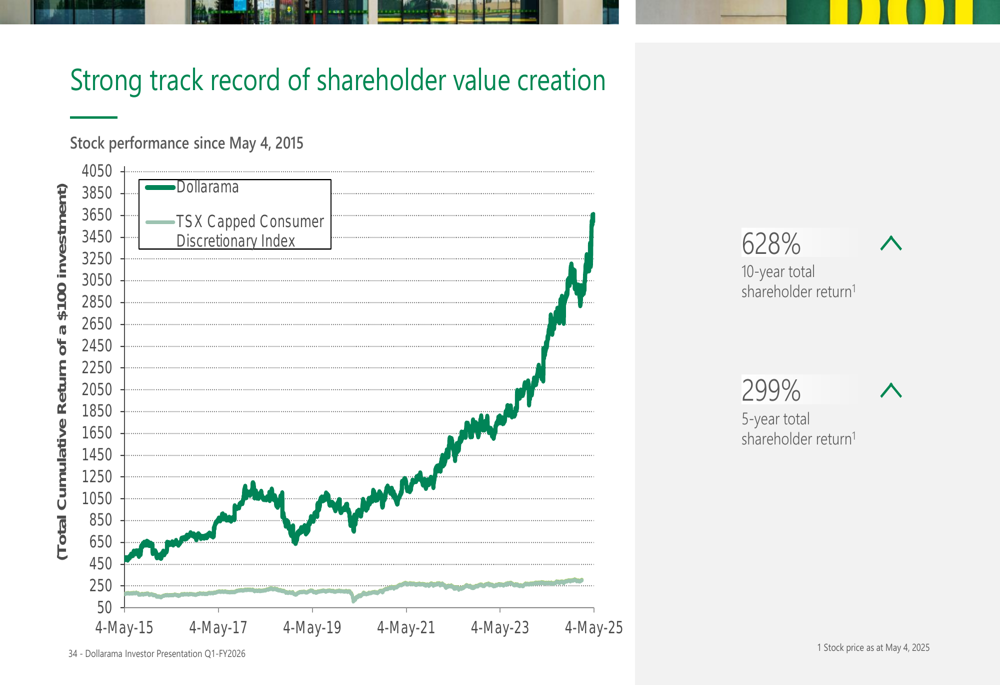

Dollarama’s long-term value creation record is impressive, with the stock significantly outperforming benchmark indices:

While the presentation maintains an optimistic outlook, investors should note that in the previous quarter (Q2 FY2025), the company had reported some softness in seasonal product demand due to adverse weather conditions. Management had also anticipated pressure on gross margins in the second half of that fiscal year due to increased volume needs in Q3, factors that may continue to influence performance in the current fiscal year.

With a strong balance sheet, consistent operational execution, and clear growth strategy across multiple markets, Dollarama appears well-positioned to continue its trajectory of profitable growth despite the challenges of a cautious consumer environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.