Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

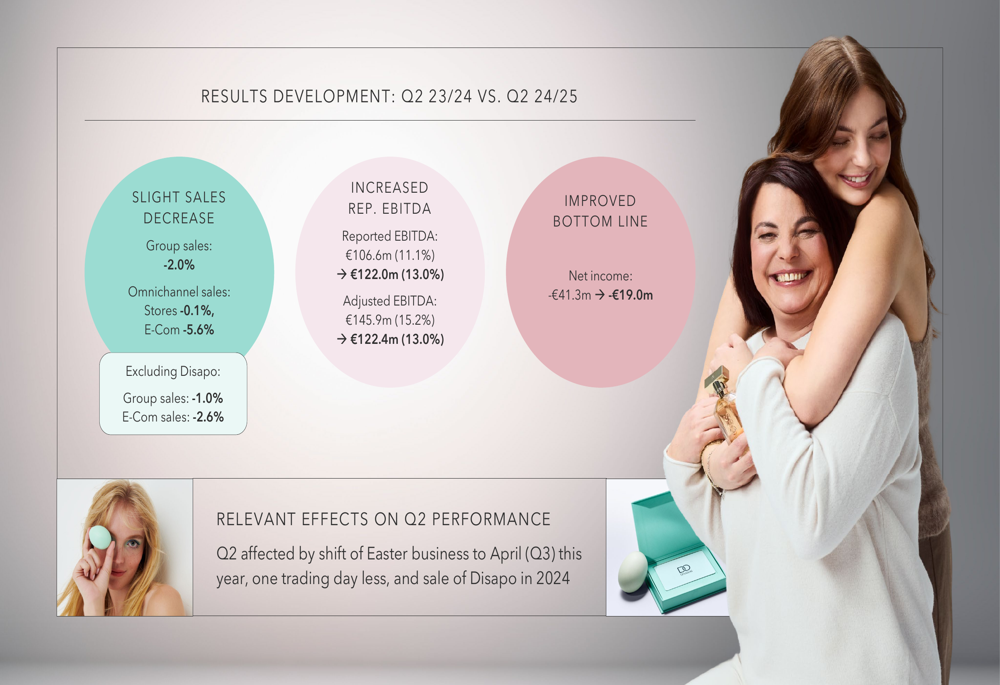

Douglas AG (DOU) presented its Q2 and H1 FY 2024/25 financial results on May 15, 2025, in Düsseldorf, revealing a mixed performance characterized by sales challenges but improved profitability. The European beauty retailer, which closed at €11.60 on May 14, up 1.38% for the day, reported that Q2 results were affected by the shift of Easter business to April (Q3) and one less trading day compared to the previous year.

Quarterly Performance Highlights

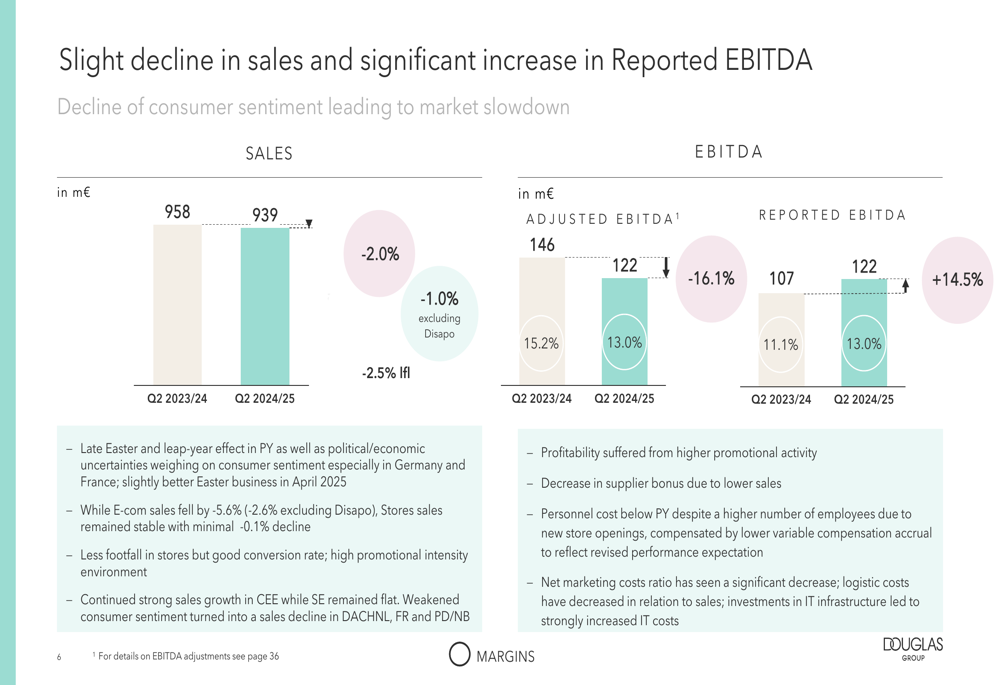

Douglas reported a 2.0% decrease in group sales to €939 million for Q2 2024/25, compared to €958 million in the same period last year. Excluding the impact of the Disapo divestiture, sales declined by 1.0%.

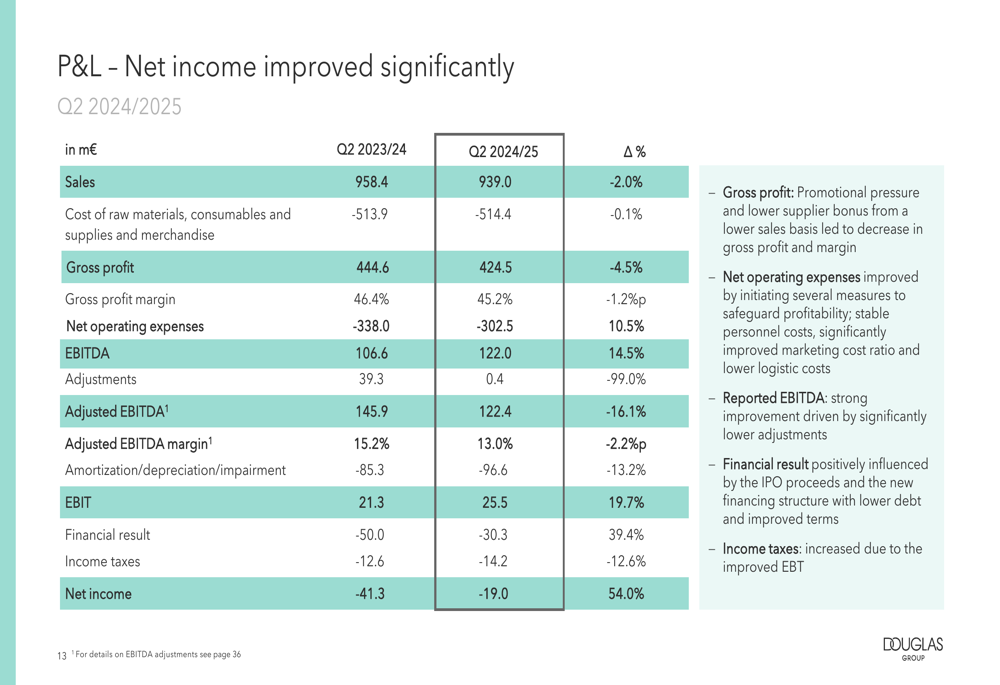

Despite the sales dip, the company’s profitability metrics showed improvement. Reported EBITDA increased by 14.5% to €122.0 million, representing a margin of 13.0%, up from 11.1% in the prior year. Net income also improved significantly, with losses narrowing from €41.3 million to €19.0 million, a 54.0% improvement.

As shown in the following comprehensive financial performance overview:

The company’s adjusted EBITDA, however, decreased by 16.1% to €122.4 million, with margin declining from 15.2% to 13.0%. This decline was attributed to higher promotional activity, decreased supplier bonuses, and increased IT costs, partially offset by lower personnel and marketing expenses.

A detailed breakdown of sales and EBITDA performance shows the contrasting trends:

The company’s P&L statement reveals the factors contributing to improved bottom-line results, including a 39.4% improvement in financial results and stable cost management:

Regional Performance Analysis

Douglas’s performance varied significantly across its regional segments, highlighting the company’s diverse market exposure:

DACHNL (Germany, Austria, Switzerland, Netherlands, and Luxembourg): Sales declined by 3.7% to €442 million, with adjusted EBITDA falling by 14.9% to €74 million. The region faced a challenging market environment with increased competition and reduced footfall.

France: Sales decreased by 2.5% to €164 million, with adjusted EBITDA declining by 22.2% to €27 million, impacted by weakened consumer sentiment and significantly decreased footfall.

Southern Europe: Sales remained relatively stable with a slight increase of 0.4% to €142 million, though adjusted EBITDA declined by 3.9% to €26 million.

Central Eastern Europe: This region was the standout performer with sales growth of 7.6% to €146 million, while adjusted EBITDA remained flat at €30 million. The company noted continuous sales momentum in both stores (+5.5%) and e-commerce (+14.6%) channels.

Parfumdreams/NICHE BEAUTY: Sales declined slightly by 0.7% to €43 million, while adjusted EBITDA turned negative at -€2 million compared to €2 million in the prior year.

Strategic Initiatives

Douglas continues to implement its "Let it Bloom" strategy, focusing on four key areas: becoming the #1 beauty destination in all markets, offering the most relevant range of brands, delivering a customer-friendly omnichannel experience, and building a focused and efficient operating model.

The company’s strategic framework is illustrated here:

Key strategic initiatives highlighted in the presentation included:

1. Loyalty Program: Rollout of a new loyalty program in the Netherlands and Belgium, building on a successful program with 62.1 million members.

2. Sustainability: Integration of sustainability measures in the store network, including LED lighting, timeless design, furniture reuse, and eco-friendly air conditioning.

3. Exclusive Product Launches: Introduction of several exclusive products, including TYPEBEA haircare line by Rita Ora launched across 20 countries and 900 stores, XO Khloe fragrance by Khloe Kardashian, and THE BOTANIST Line, a premium vegan brand.

4. Store Network Expansion: The company is proceeding with its plan for 200 new store openings and 400 refurbishments, maintaining a network of 1,901 stores.

5. Omnichannel Warehouses: Development of a network of seven omnichannel warehouses across Europe to support the company’s integrated retail strategy.

Financial Position & Outlook

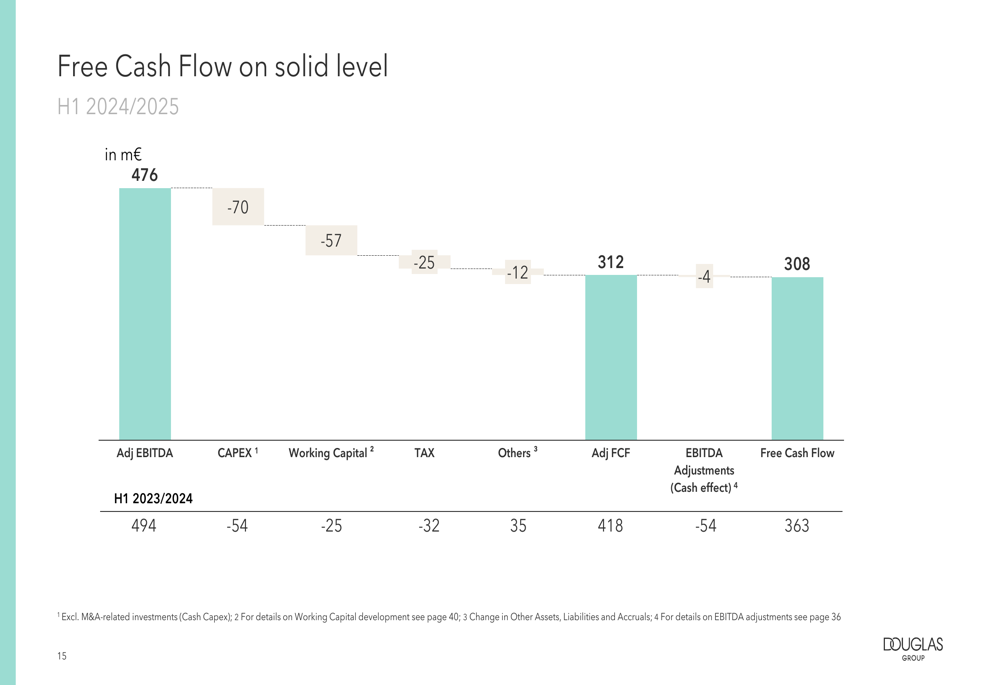

Douglas’s financial position showed some improvements, with free cash flow of €308 million for H1 2024/25, though down from €363 million in the prior year:

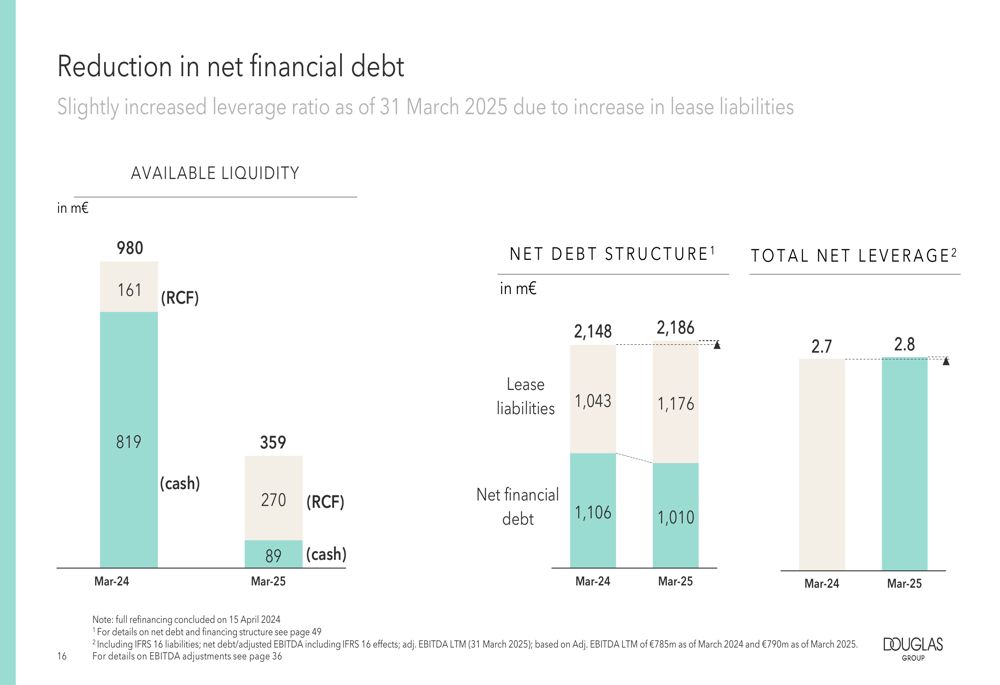

The company’s net financial debt structure showed a reduction in net financial debt to €1,010 million from €1,106 million, though total net leverage increased slightly to 2.8x from 2.7x:

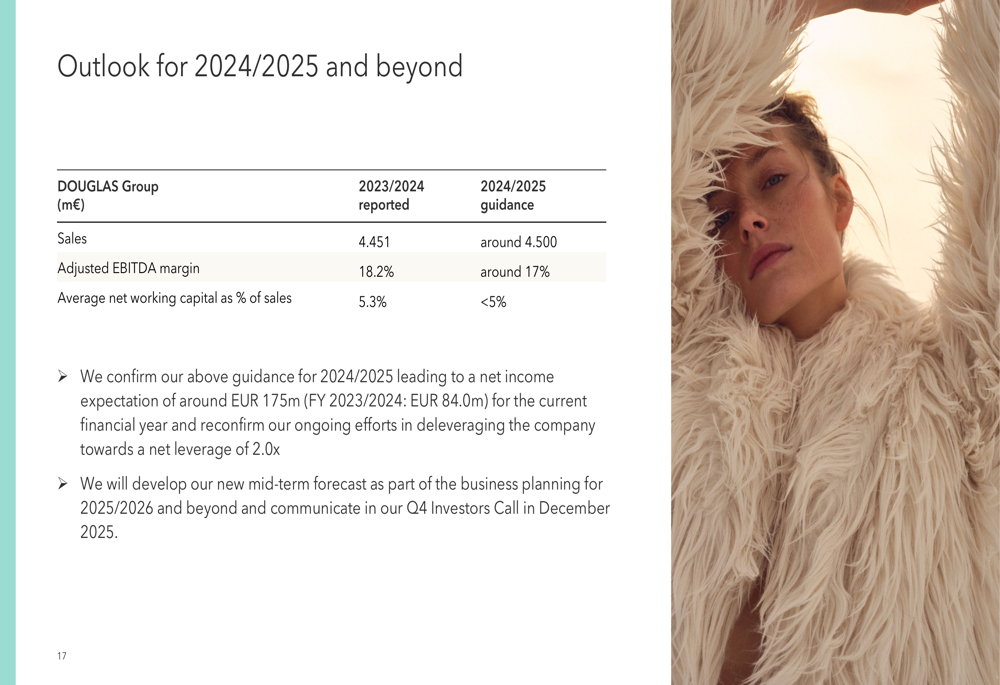

Looking forward, Douglas confirmed its guidance for FY 2024/25, projecting:

- Sales of around €4,500 million (up from €4,451 million)

- Adjusted EBITDA margin of around 17% (down from 18.2%)

- Average net working capital as percentage of sales below 5%

- Net income expectation of around €175 million

- Progress toward a leverage target of 2.0x

The company’s outlook is summarized in this guidance:

In conclusion, Douglas’s Q2 and H1 2024/25 results reflect a company navigating challenging market conditions with a focus on profitability improvement and strategic initiatives. While sales faced headwinds in several key markets, the strong performance in Central Eastern Europe and improved bottom-line results suggest the company’s diversified approach is providing some resilience. Management’s confirmation of full-year guidance indicates confidence in the company’s ability to execute its strategy despite the challenging consumer environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.